Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

Bioventus Inc. (NASDAQ:BVS) presented its first quarter 2025 financial results on May 6, 2025, revealing a mixed performance characterized by organic growth despite headline revenue decline. The medical device company’s stock fell 8.39% to $6.44 following the presentation, extending losses beyond the 1.85% premarket decline reported earlier, as investors weighed positive operational metrics against cash flow challenges.

The company’s presentation emphasized resilience in an uncertain macroeconomic environment, with management expressing confidence in accelerated growth for the second half of 2025 despite current headwinds.

Quarterly Performance Highlights

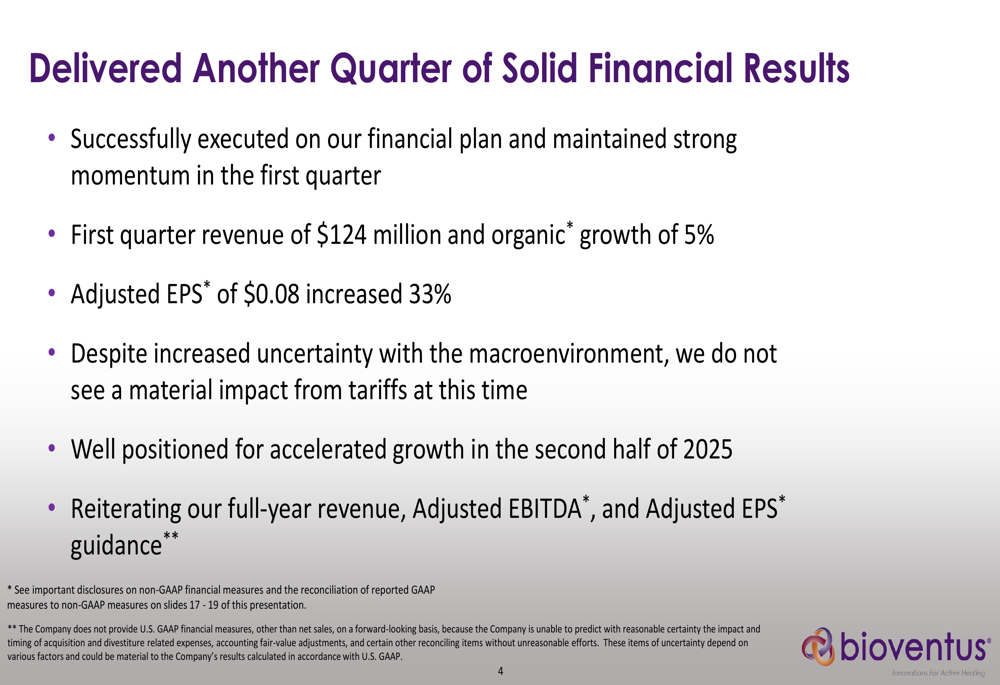

Bioventus reported Q1 2025 revenue of $124 million, representing a 4% year-over-year decline but achieving 5% organic growth across its three business segments. The revenue decline was primarily attributed to the divestiture of the Advanced Rehabilitation business completed at the end of 2024.

"We successfully executed on our financial plan and maintained strong momentum in the first quarter," noted Rob Claypoole, President and CEO, highlighting the company’s ability to navigate market challenges.

As shown in the following financial results summary:

Adjusted earnings per share reached $0.08, a 33% increase compared to the prior year period, driven largely by reduced interest expenses. The company generated Adjusted EBITDA of $19 million, which was $3 million lower than the same period last year, impacted by both the Advanced Rehabilitation divestiture and an unexpected $1.1 million foreign currency loss related to the Swedish krona.

Segment Performance Analysis

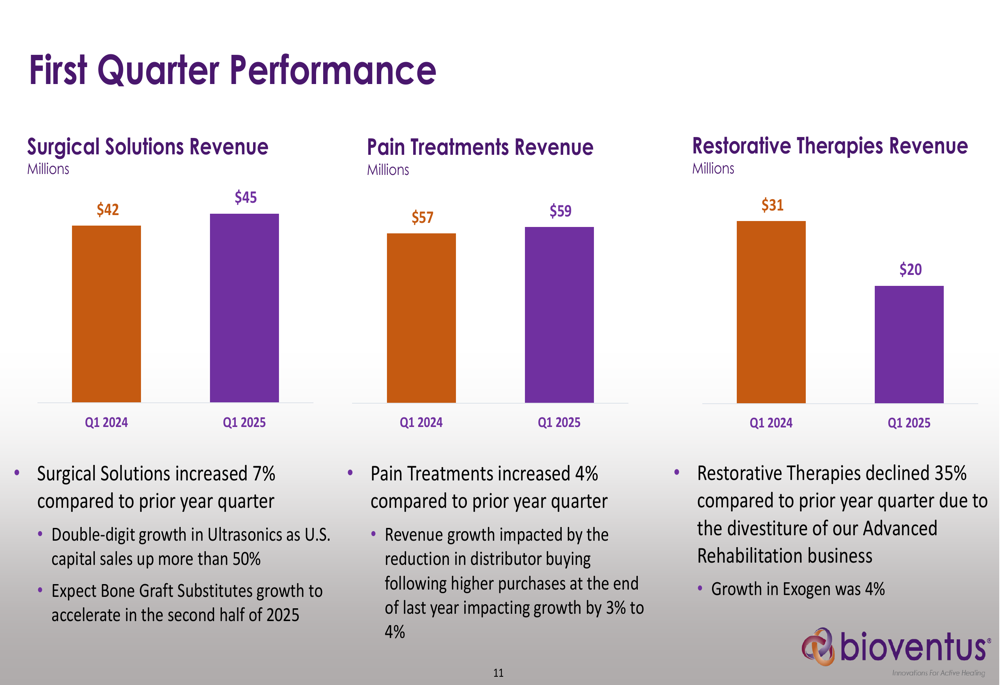

The company’s performance varied across its three primary business segments, with both Surgical Solutions and Pain Treatments showing growth while Restorative Therapies declined significantly due to the divestiture impact.

The revenue breakdown by segment reveals the following performance:

Surgical Solutions revenue increased 7% year-over-year to $45 million, driven by double-digit growth in Ultrasonics due to new capital placements. Management expressed confidence that Bone Graft Substitutes growth would accelerate in the second half of 2025.

Pain Treatments revenue grew 4% to $59 million, with double-digit growth in Durolane partially offset by a reduction in distributor buying. The company highlighted its expanded portfolio in this segment:

Restorative Therapies revenue declined 35% to $20 million, primarily due to the Advanced Rehabilitation divestiture. However, Exogen, the company’s ultrasound bone healing system, maintained momentum with 4% growth and high-single-digit growth in the U.S. market.

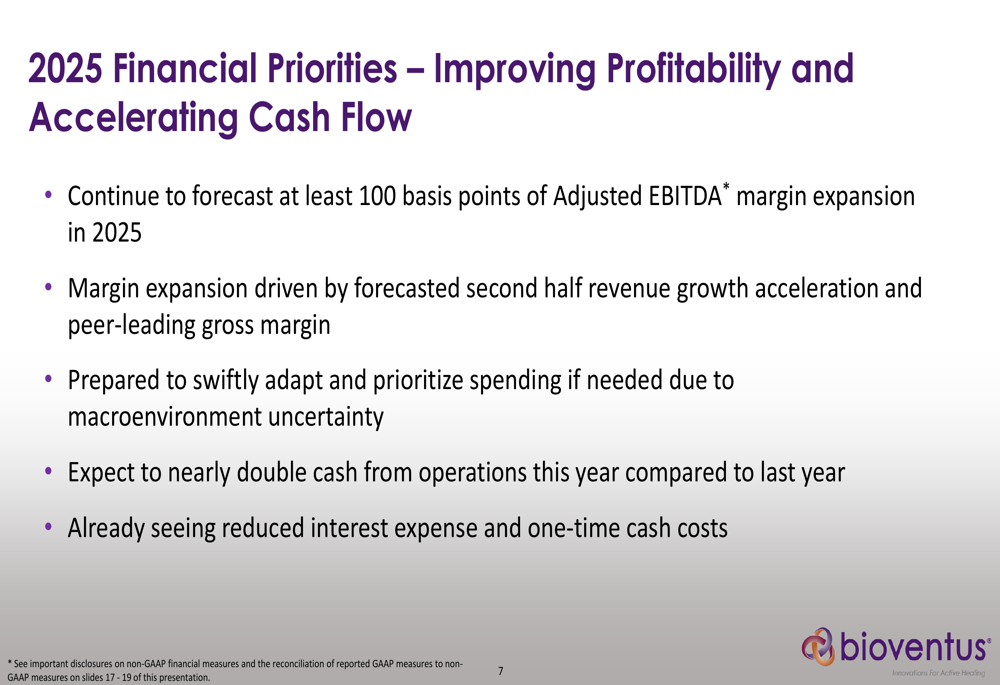

Balance Sheet and Cash Flow

Bioventus ended the quarter with $23 million in cash and $346 million in outstanding debt, including $10 million drawn on its revolving credit facility. As expected, cash from operations was negative at $19 million, though management expressed confidence in acceleration throughout the remainder of 2025.

"We expect to nearly double cash from operations this year compared to last year," stated Mark Singleton, Senior Vice-President and Chief Financial Officer. "We’re already seeing reduced interest expense and one-time cash costs."

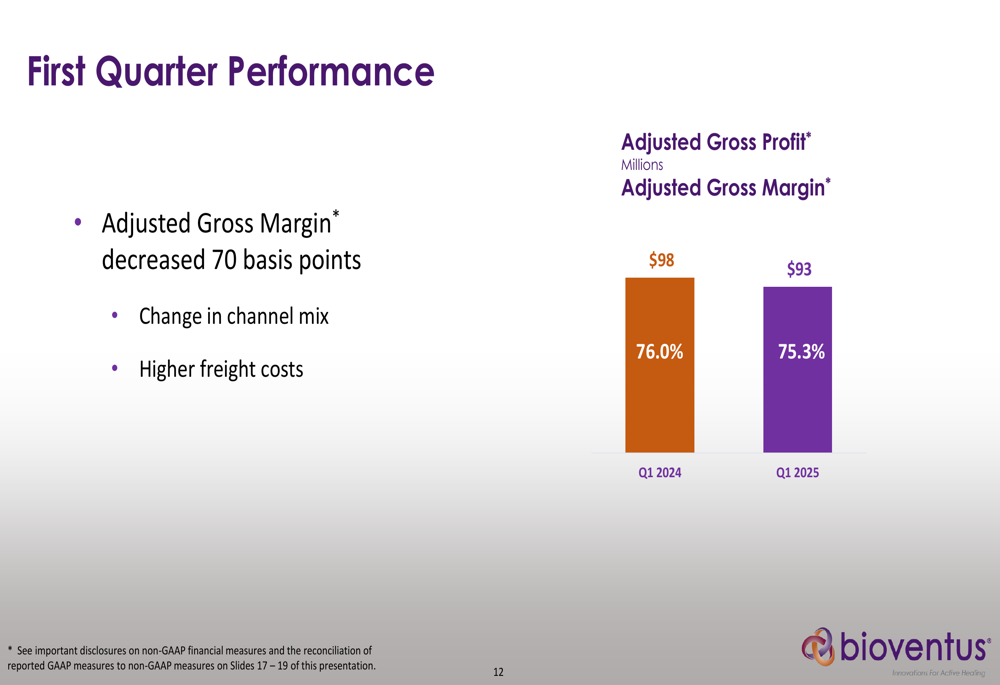

The company’s adjusted gross profit and margin showed slight compression:

Adjusted gross margin decreased 70 basis points to 75.3% due to changes in channel mix and higher freight costs. Despite this slight decline, management emphasized that the company’s gross margins remain peer-leading and will contribute to overall profitability improvement.

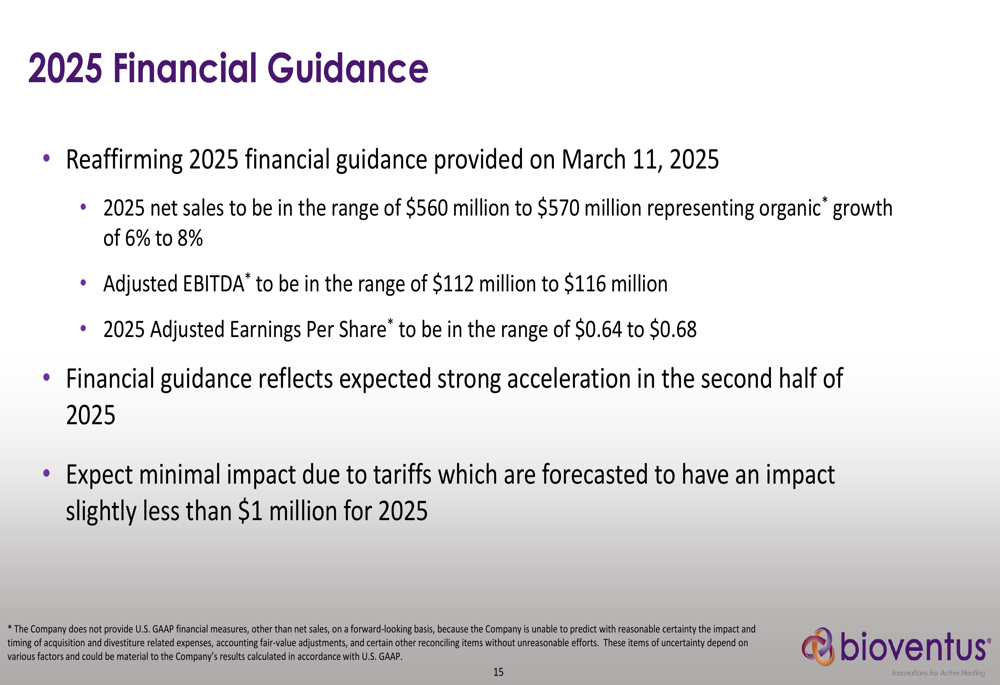

2025 Outlook and Guidance

Bioventus reaffirmed its full-year 2025 guidance, projecting:

The company expects net sales between $560-570 million, representing organic growth of 6-8%, with Adjusted EBITDA of $112-116 million and Adjusted EPS of $0.64-0.68. Management emphasized that this guidance reflects expected strong acceleration in the second half of 2025.

"Despite increased uncertainty with the macroenvironment, we do not see a material impact from tariffs at this time," noted Claypoole, adding that the company forecasts tariff impact to be less than $1 million for 2025.

Strategic Initiatives

Bioventus highlighted several strategic initiatives designed to drive long-term growth. The company recently signed an agreement with Apex Biologix to distribute their XCELL Platelet-Rich Plasma (PRP) system in the U.S., adding another potential growth driver leveraging its existing HA commercial infrastructure.

Management outlined its financial priorities for 2025, focusing on profitability improvement and cash flow acceleration:

The company forecasts at least 100 basis points of Adjusted EBITDA margin expansion in 2025, driven by second-half revenue growth acceleration and gross margin strength. Management emphasized preparedness to adapt and prioritize spending if needed due to macroeconomic uncertainties.

"Our solid foundation provides flexibility for an uncertain macroenvironment," Claypoole stated, pointing to the company’s enhanced financial liquidity, diverse portfolio of growth drivers, and resilient team that has successfully navigated past challenges.

As Bioventus works to strengthen its financial position and drive growth across its product portfolio, investors will be closely watching whether the promised second-half acceleration materializes and if cash flow improvements meet management’s optimistic projections.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.