Gold prices cool after hitting over 2-week high on Fed independence fears

Introduction & Market Context

Black Rifle Coffee Company (NASDAQ:BRCC) reported mixed second-quarter 2025 results on August 5, showing continued revenue growth but facing significant margin pressure. The veteran-focused coffee brand continues to expand its retail presence while navigating challenges from coffee inflation and increased competition.

The company’s stock has struggled in recent months, trading at $1.65 as of August 4, 2025, significantly below its 52-week high of $5.47. Following its Q1 results, the stock experienced a 16.46% drop, reflecting investor concerns about declining margins despite revenue growth.

Quarterly Performance Highlights

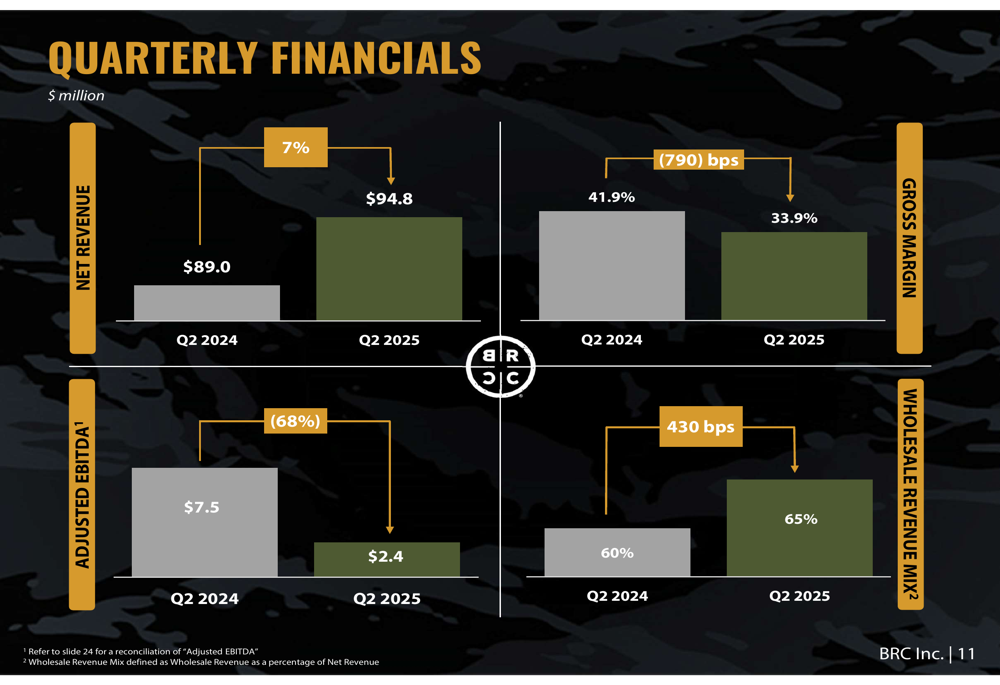

Black Rifle Coffee reported Q2 2025 net revenue of $94.8 million, representing a 6.5% increase year-over-year. However, profitability metrics showed considerable pressure, with gross margin declining to 33.9% from 41.9% in the prior year period, a significant drop of 790 basis points.

As shown in the following quarterly financials chart:

Adjusted EBITDA fell to $2.4 million, down 68% from $7.5 million in Q2 2024, with EBITDA margin contracting to 2.5% from 8.4%. The company reported a net loss of $14.5 million, substantially wider than the $1.4 million loss in the same quarter last year.

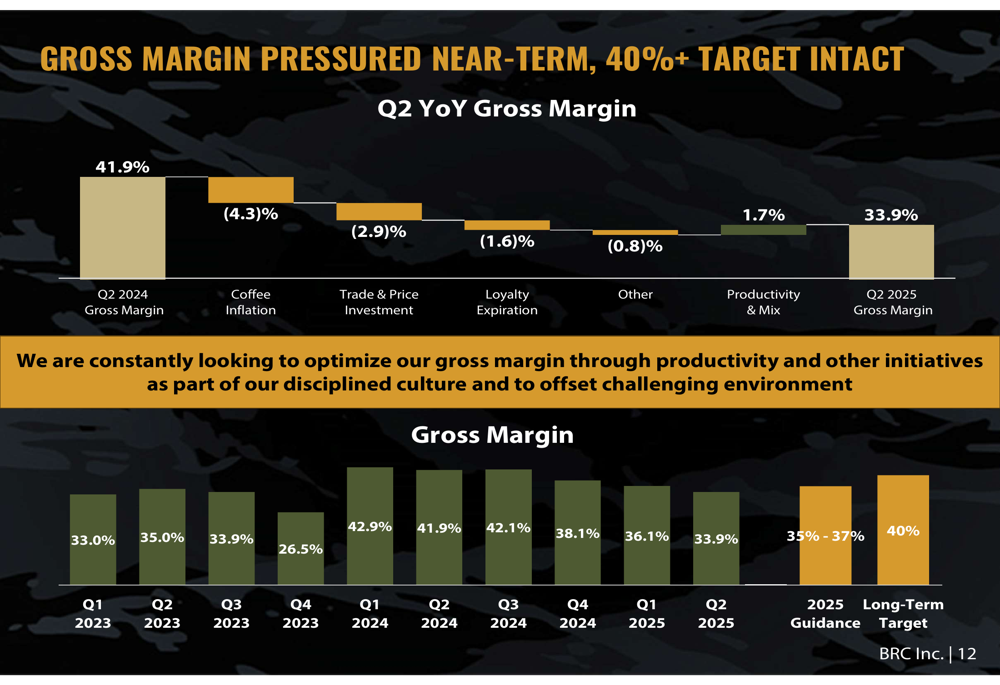

The decline in gross margin was attributed to several factors, as illustrated in this detailed breakdown:

Coffee inflation had the most significant negative impact at 4.3 percentage points, followed by trade and price investments at 2.9 percentage points. The company partially offset these pressures through productivity improvements and favorable mix, which contributed a positive 1.7 percentage points to gross margin.

Channel Strategy and Expansion

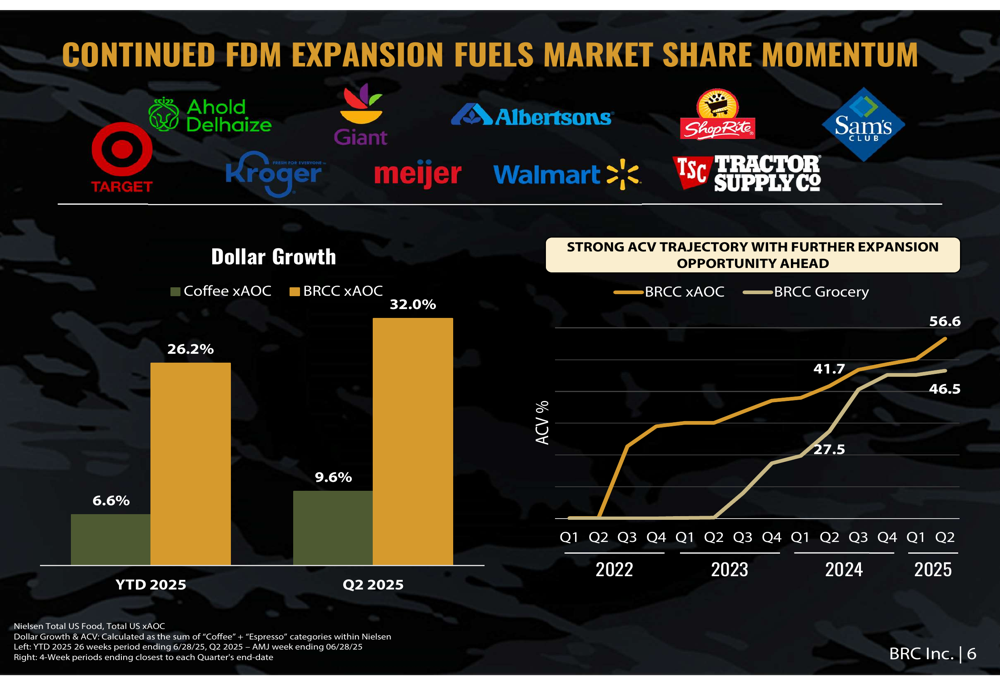

Black Rifle Coffee’s wholesale channel continues to drive growth, with revenue increasing 14.1% year-over-year to $61.3 million (21.0% excluding barter transactions). The company is aggressively expanding its presence in food, drug, and mass (FDM) retail channels, which is fueling market share gains.

The company’s FDM expansion strategy is showing strong results, as demonstrated in this chart:

While the overall coffee category in XAOC (expanded all-outlet combined) channels grew 9.6% in Q2 2025, Black Rifle Coffee achieved 32.0% growth. The company’s grocery ACV (all-commodity volume) reached 56.6% in Q2 2025, indicating strong retail penetration.

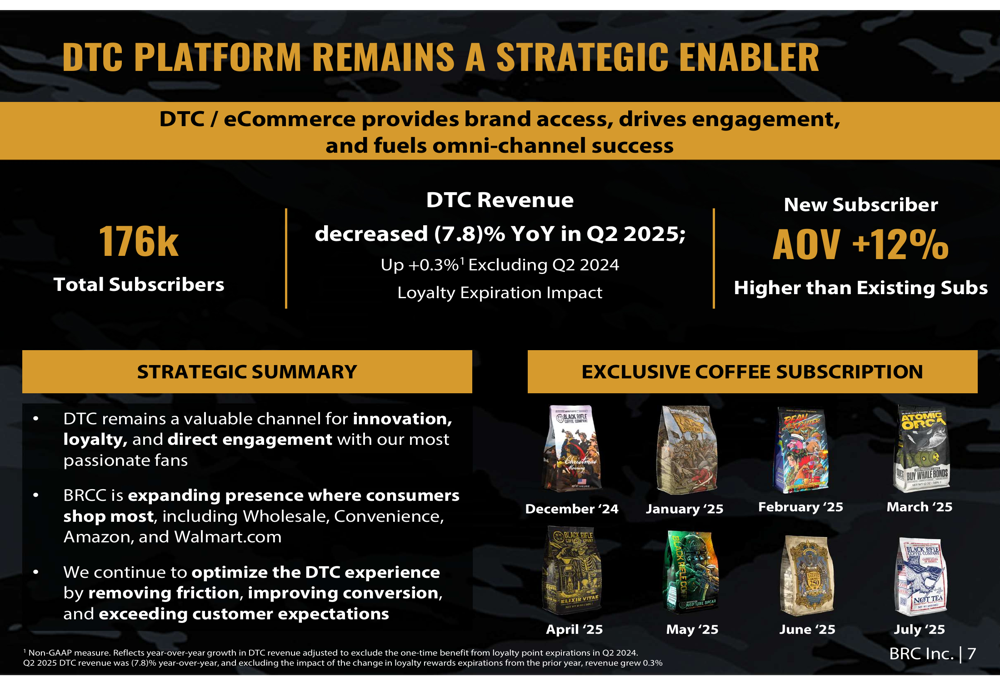

Meanwhile, the direct-to-consumer (DTC) platform remains an important strategic channel despite revenue declining 7.8% year-over-year. The company maintains 176,000 total subscribers and notes that new subscriber average order value is 12% higher than existing subscribers.

New Product Initiatives

Black Rifle Coffee continues to expand its ready-to-drink (RTD) coffee distribution, maintaining its position as a top-3 brand in the category. The RTD segment achieved 53.5% ACV across XAOC and convenience channels in Q2 2025, with a 4.6% market share.

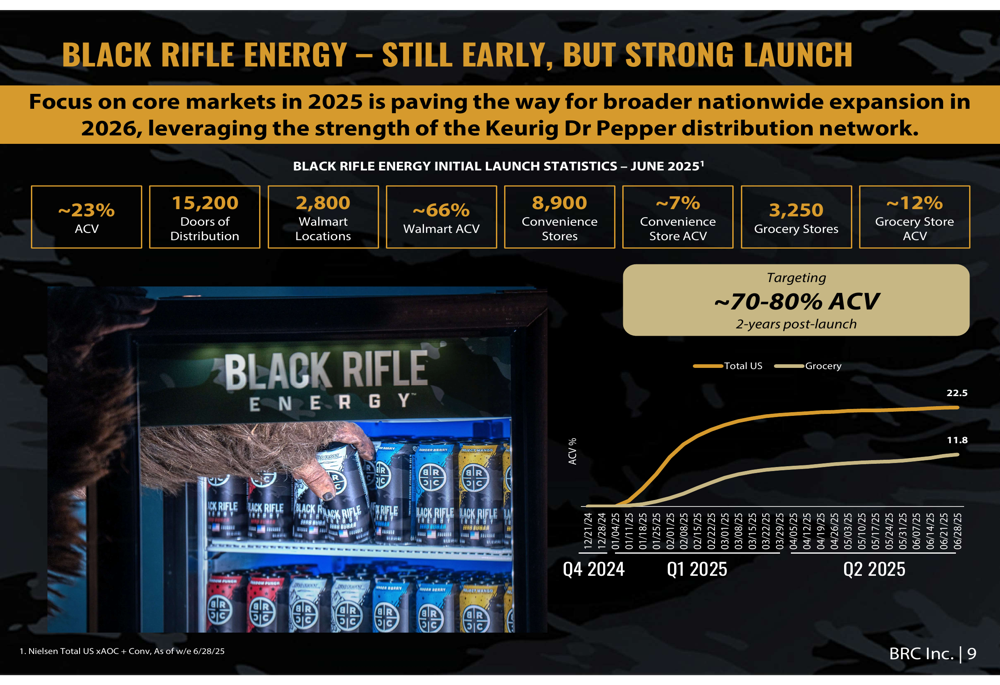

A key growth initiative is the company’s entry into the energy drink market with Black Rifle Energy. Early results show promising momentum:

As of June 2025, Black Rifle Energy had achieved approximately 23% ACV with distribution in 15,200 doors, including 2,800 Walmart (NYSE:WMT) locations. The company is targeting 70-80% ACV within two years of launch, positioning the energy drink line as a significant growth driver.

Outlook and Guidance

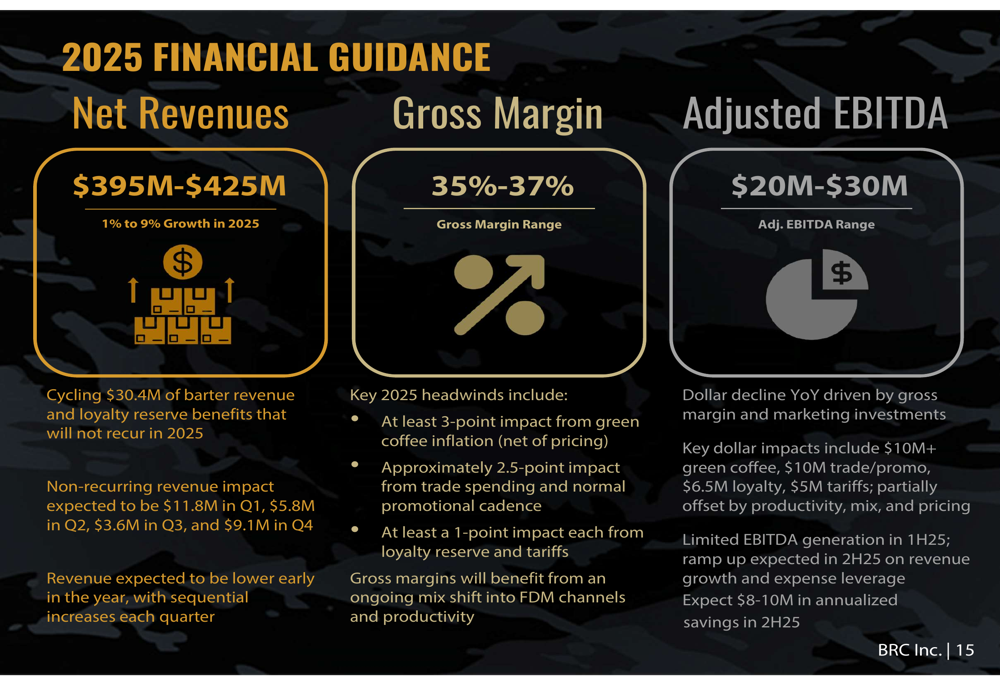

Despite near-term margin pressures, Black Rifle Coffee maintained its full-year 2025 guidance:

The company expects net revenues of $395-425 million, representing 1-9% growth, with gross margins of 35-37% and adjusted EBITDA of $20-30 million. Management noted that margins will benefit from an ongoing mix shift into FDM channels and productivity improvements, with EBITDA expected to ramp up in the second half of 2025. The company anticipates $8-10 million in cost savings initiatives.

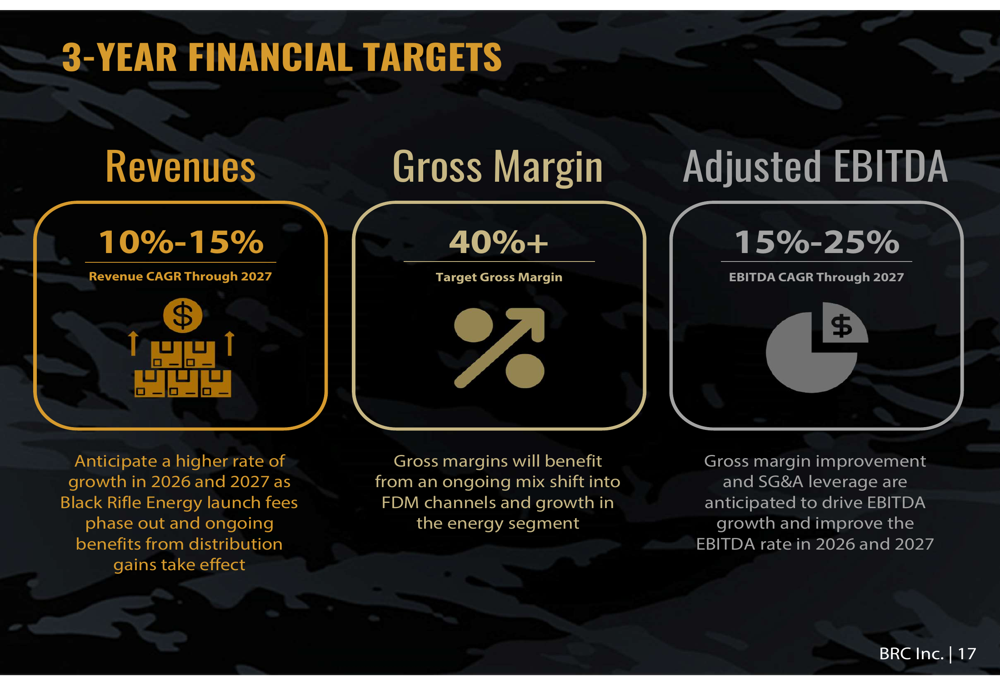

Looking beyond 2025, Black Rifle Coffee outlined ambitious three-year financial targets:

The company is targeting 10-15% revenue CAGR through 2027, with gross margins exceeding 40% and adjusted EBITDA growing at 15-25% CAGR. Management anticipates higher growth rates in 2026 and 2027 as their strategic initiatives gain traction.

Executive Commentary

Chris Mondzelewski, President and CEO, expressed confidence in the company’s strategic plan, stating they are positioned to "accelerate brand growth, deepen customer engagement and expand market presence with continued expansion across retail and e-commerce" with a strong marketing calendar into 2026.

Executive Chairman Evan Hafer and CFO Matthew Amigh also participated in the presentation, emphasizing the company’s commitment to supporting military, veterans, and first responders while executing on operational efficiency measures to improve profitability.

Challenges and Headwinds

The company faces several near-term challenges, including green coffee inflation, increased trade spending, loyalty reserve impacts, and tariffs. These factors contributed to the significant gross margin compression in Q2 2025.

Despite these headwinds, management remains focused on its long-term strategy of expanding retail distribution, growing its energy drink business, and improving operational efficiency to return to its target margin profile of 40%+ gross margin and higher EBITDA growth in 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.