Nucor earnings beat by $0.08, revenue fell short of estimates

Introduction & Market Context

Blackbaud Inc (NASDAQ:BLKB), a leading provider of software for social impact organizations, presented its Q1 2025 investor update on April 30, highlighting the achievement of its Rule of 40 milestone despite revenue headwinds from strategic divestments. The company, which serves approximately 40,000 customers across 100+ countries, reported progress on its long-term financial goals while maintaining its position in the $10B+ total addressable market for social impact software.

The presentation comes after Blackbaud’s Q4 2024 earnings report in February showed mixed results, with the company beating EPS expectations but falling short on revenue targets. Despite the Q1 revenue decline, Blackbaud emphasized its organic growth story and margin expansion as key drivers of shareholder value.

Quarterly Performance Highlights

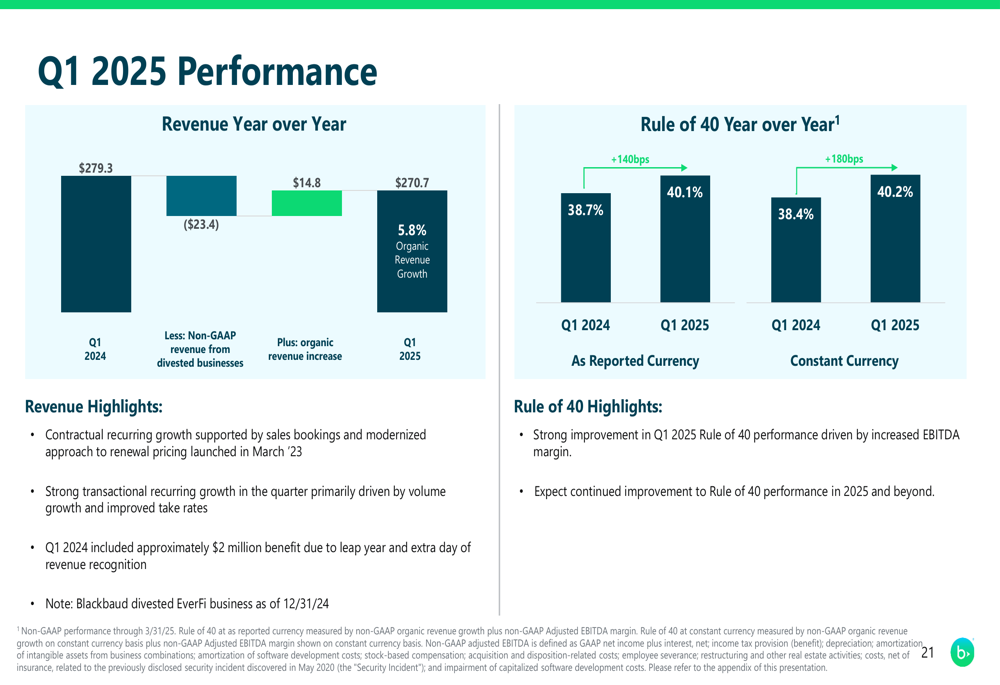

Blackbaud reported Q1 2025 revenue of $270.7 million, down from $279.3 million in Q1 2024. However, the company achieved 5.8% organic revenue growth after accounting for $23.4 million in revenue reduction from divested businesses.

As shown in the following chart detailing Q1 performance, Blackbaud reached a significant milestone by achieving a Rule of 40 score of 40.1%, up from 38.7% in the prior year:

The Rule of 40 - a metric combining revenue growth and profit margin that’s widely used to evaluate software companies - improved despite the headline revenue decline, demonstrating the company’s focus on profitable growth. This achievement aligns with management’s strategic priorities outlined in previous earnings calls.

Strategic Initiatives

Blackbaud’s presentation detailed a five-point operating plan designed to drive improved financial performance, focusing on product innovation, bookings growth, transactional revenue optimization, modernized pricing, and cost management.

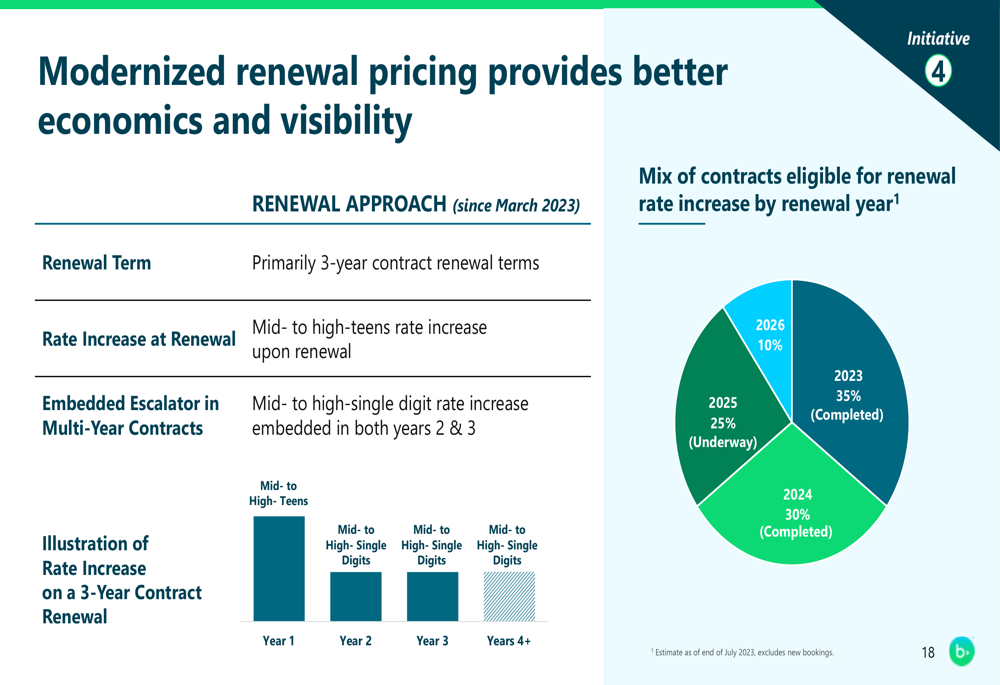

The company highlighted its modernized renewal pricing approach implemented since March 2023, which includes:

- Shifting primarily to 3-year contracts

- Mid-to-high teens rate increases at renewal

- Mid-to-high single digit escalators embedded in years 2 and 3 of multi-year contracts

This pricing strategy is illustrated in the following slide, showing the distribution of contracts eligible for renewal across different years:

Blackbaud also emphasized its product innovation initiatives, particularly in AI-driven solutions. The company is investing in corporate social impact innovation, Raiser’s Edge NXT enhancements with AI-powered fundraising tools, and optimized donation forms to improve conversion rates.

Detailed Financial Analysis

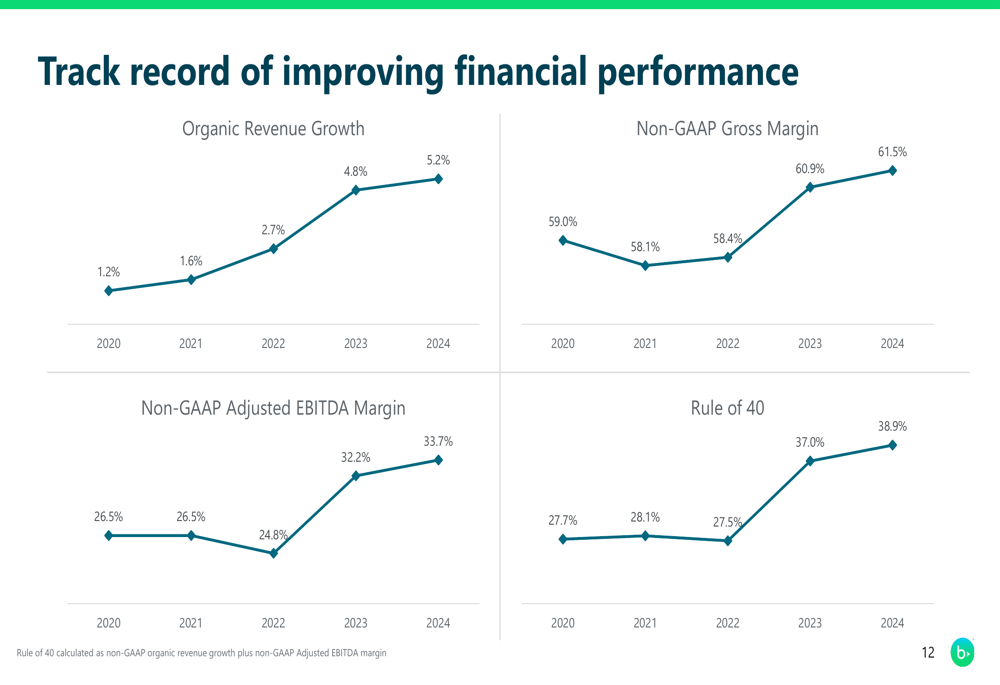

Blackbaud has demonstrated consistent improvement in key financial metrics over the past several years. The company’s track record shows steady progress in organic revenue growth, gross margin, EBITDA margin, and Rule of 40 performance:

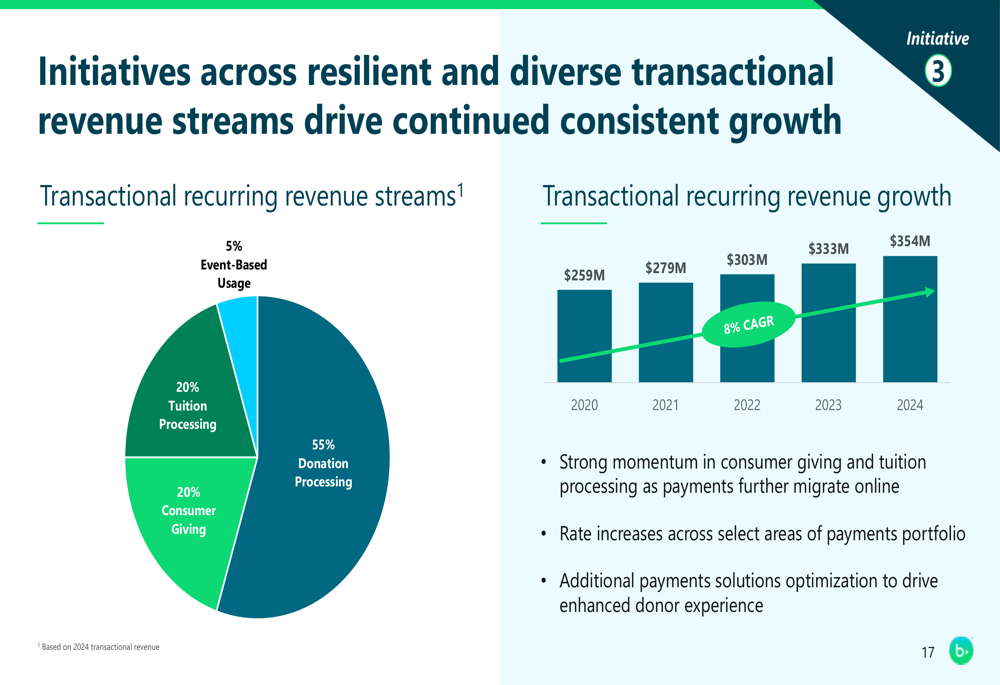

The company’s transactional revenue streams have grown at an 8% CAGR from 2020 to 2024, reaching $354 million. This revenue is diversified across donation processing (55%), consumer giving (20%), tuition processing (20%), and event-based usage (5%).

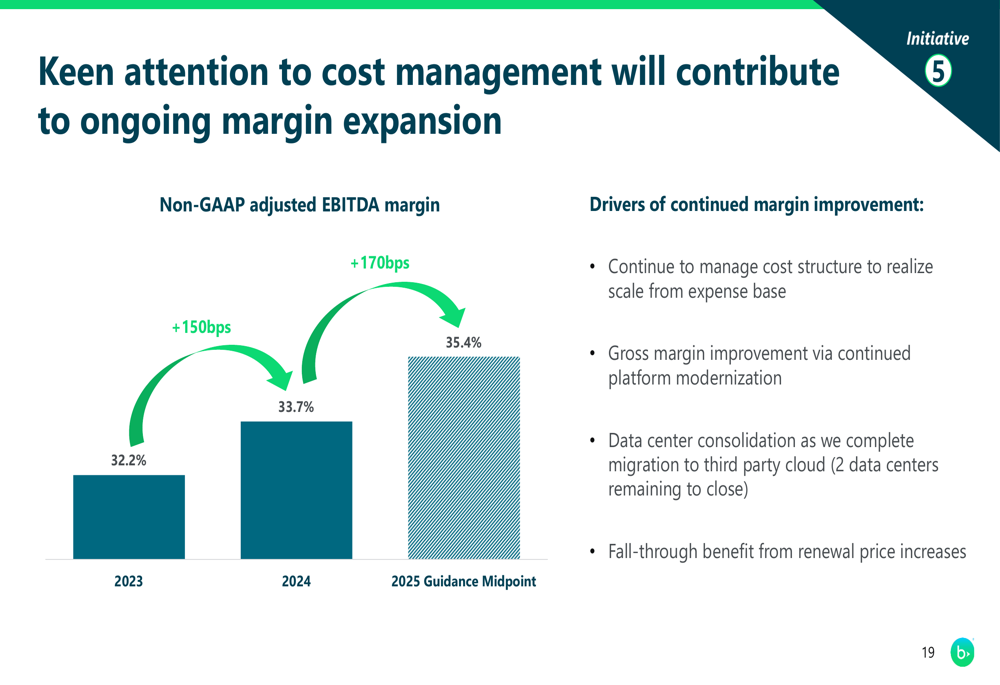

Cost management initiatives have contributed to ongoing margin expansion, with Non-GAAP adjusted EBITDA margin growing from 32.2% in 2023 to 33.7% in 2024, with guidance for further improvement to 35.4% (midpoint) in 2025.

Competitive Industry Position

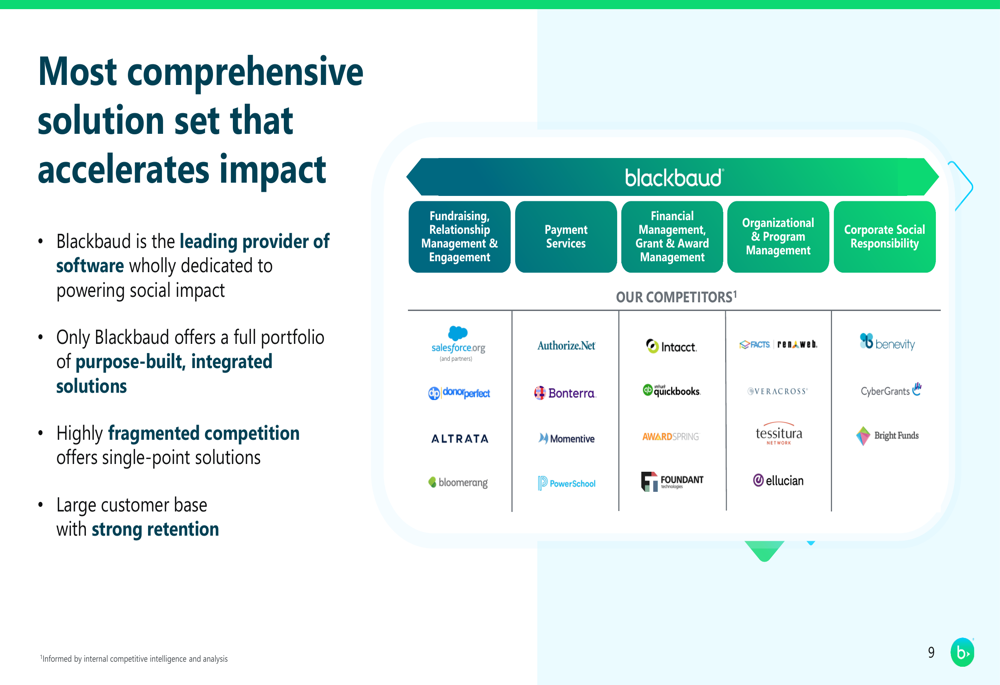

Blackbaud positions itself as having the most comprehensive solution set in a fragmented competitive landscape. The company highlighted its unique value proposition as the leading provider of software dedicated to powering social impact with a full portfolio of purpose-built, integrated solutions.

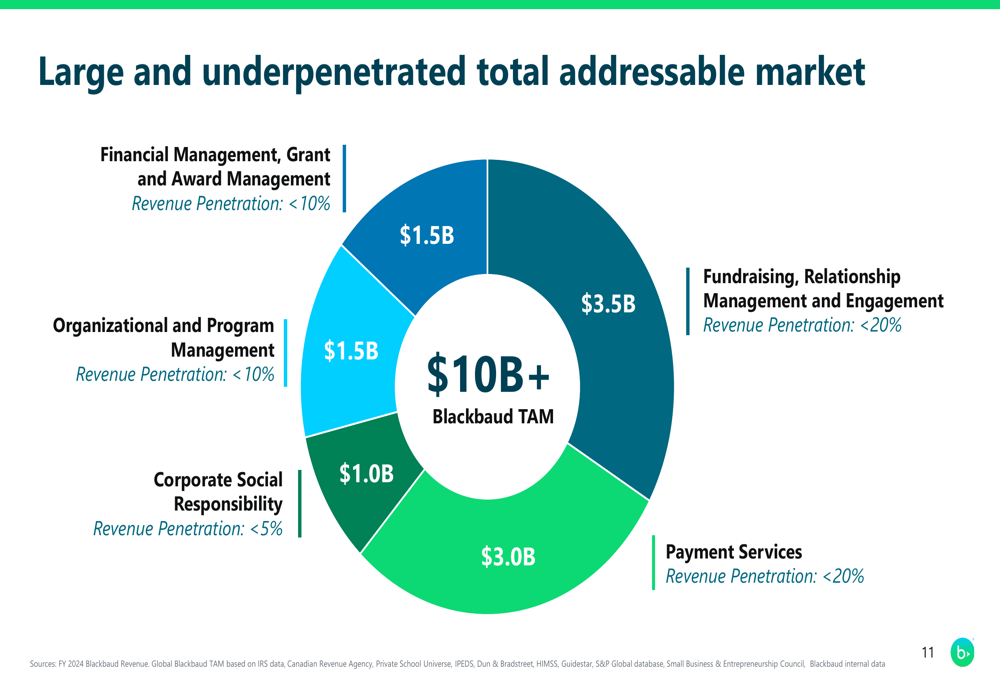

The company’s total addressable market exceeds $10 billion across five key segments, with varying levels of penetration:

This large and underpenetrated market provides significant runway for growth. Blackbaud’s competitive advantage stems from its comprehensive solution set compared to competitors offering single-point solutions:

Forward-Looking Statements

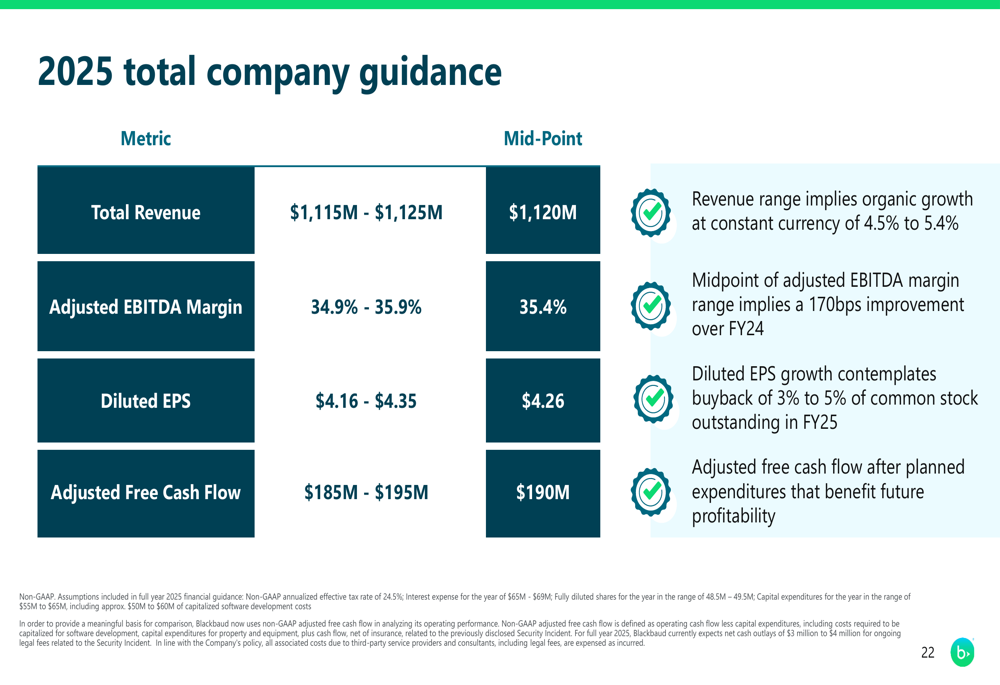

For 2025, Blackbaud provided guidance including:

- Total (EPA:TTEF) Revenue of $1,115M - $1,125M ($1,120M midpoint)

- Organic growth at constant currency of 4.5% to 5.4%

- Adjusted EBITDA Margin of 34.9% - 35.9% (35.4% midpoint)

- Diluted EPS of $4.16 - $4.35 ($4.26 midpoint)

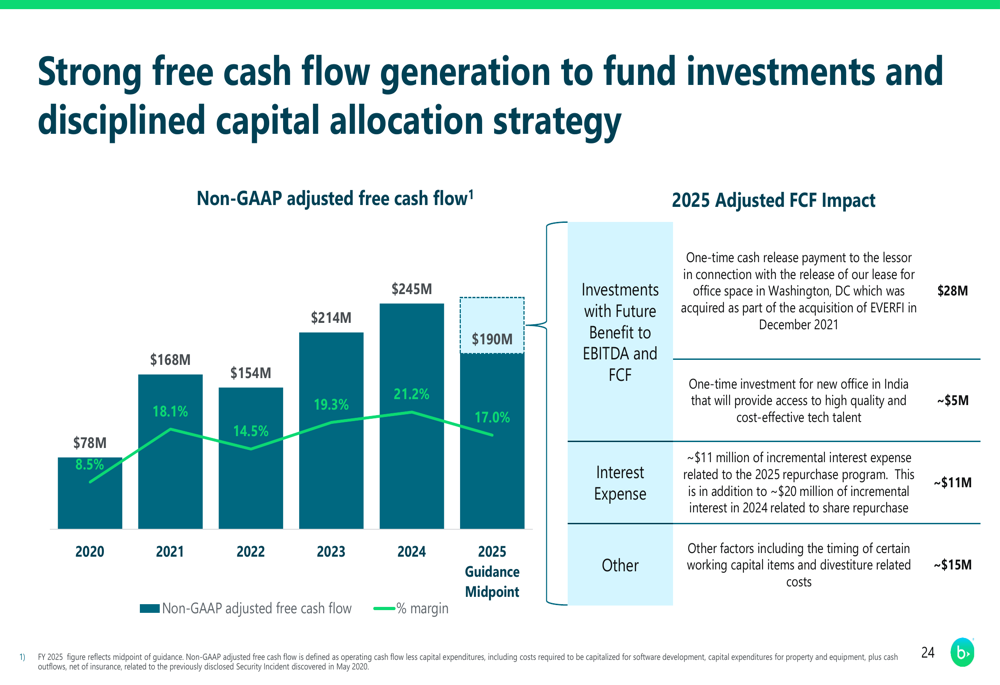

- Adjusted Free Cash Flow of $185M - $195M ($190M midpoint)

The company’s 2025 revenue guidance represents a decrease from the $1.155 billion reported for 2024, reflecting the impact of strategic divestments. However, the organic growth rate and margin expansion targets indicate continued operational improvement.

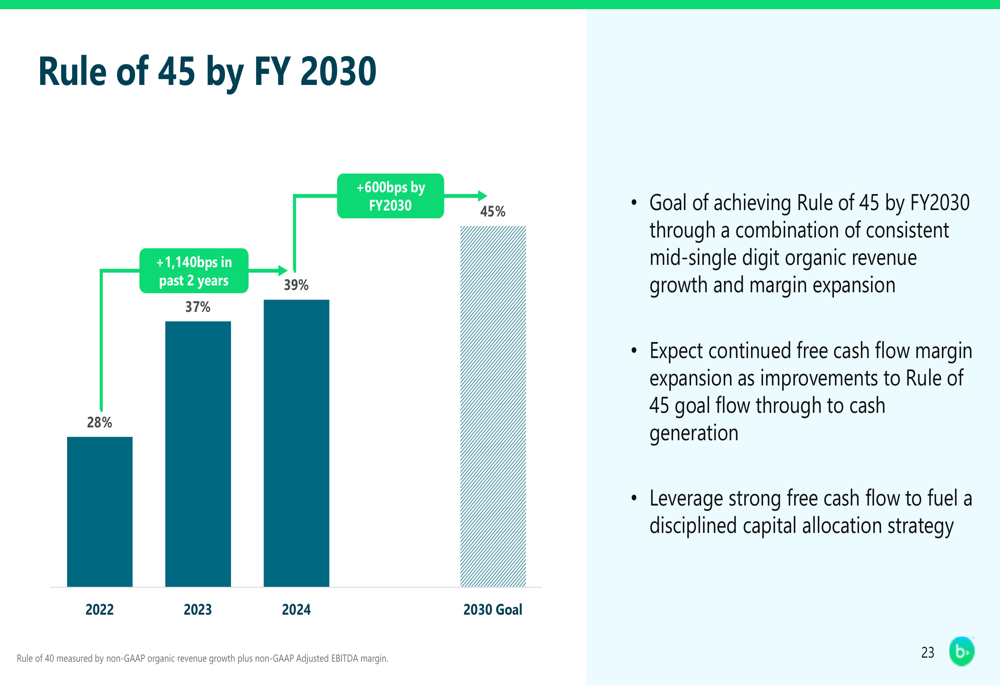

Looking further ahead, Blackbaud outlined its long-term goal of achieving a Rule of 45 by FY2030, representing an additional 600 basis points improvement from current levels through a combination of consistent mid-single digit organic revenue growth and margin expansion:

Capital Allocation Strategy

Blackbaud’s capital allocation strategy emphasizes shareholder returns through stock repurchases, with plans to buy back up to 5% of outstanding shares in 2025. The company reported it had already repurchased approximately 3% of common stock outstanding in Q1 2025.

The company’s free cash flow has grown significantly, from $78 million in 2020 to $245 million in 2024, though 2025 adjusted free cash flow will be impacted by one-time payments, interest expense related to the repurchase program, and other factors:

As of March 31, 2025, Blackbaud had approximately $545 million remaining under its $800 million share repurchase authorization, signaling continued commitment to returning capital to shareholders while maintaining flexibility for strategic investments and debt management.

The company’s long-term capital allocation strategy focuses on maximizing shareholder value through a balanced approach to stock repurchases, accretive M&A, and debt repayment, with the current emphasis on share buybacks reflecting management’s confidence in Blackbaud’s intrinsic value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.