CVS Group profit drops 7.4% as revenue rises on Australia expansion, asset sale

Introduction & Market Context

Boot Barn Holdings Inc (NYSE:BOOT) released its fiscal year 2025 financial presentation on May 14, 2025, showcasing strong performance with significant sales and earnings growth. The western wear retailer’s stock responded positively, rising 6.52% to $141.50 in after-hours trading following the presentation, rebounding from a 1.61% decline during regular trading hours.

The company has maintained its aggressive expansion strategy while navigating potential headwinds from increased tariffs, particularly on Chinese imports. Boot Barn’s presentation highlighted its decade-long growth trajectory and outlined plans to continue store expansion while mitigating tariff impacts through diversified sourcing.

FY2025 Performance Highlights

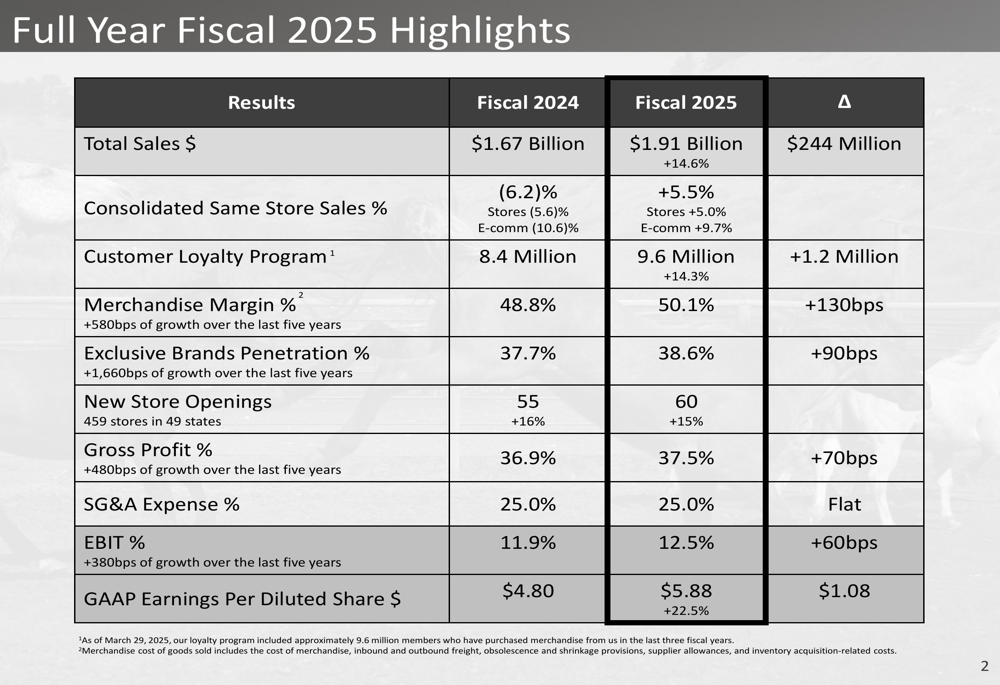

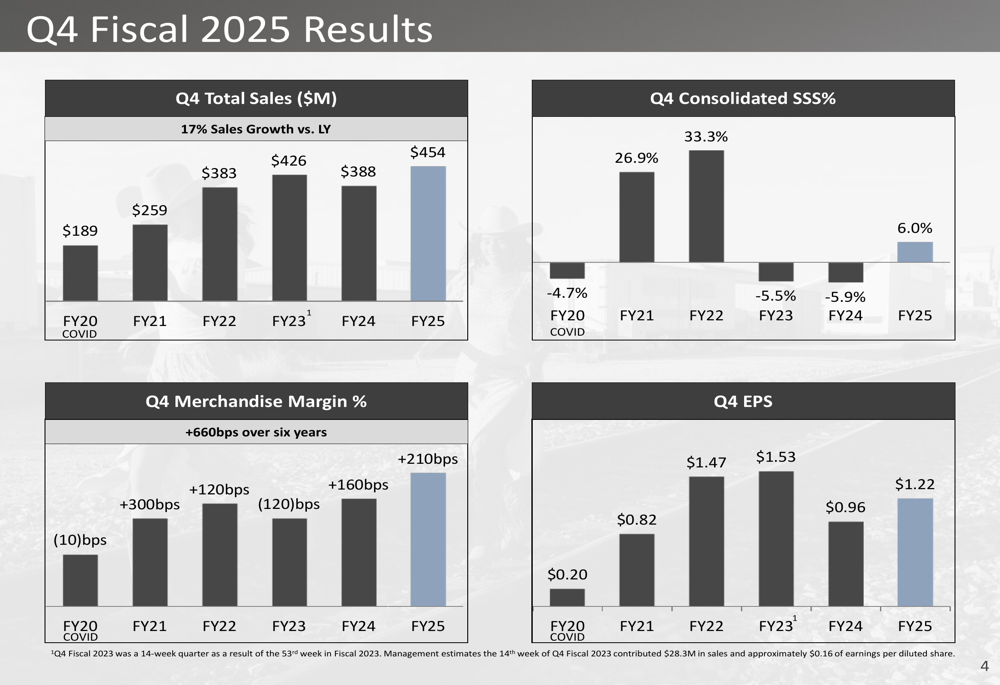

Boot Barn delivered impressive financial results for fiscal year 2025, with total sales reaching $1.91 billion, a 14.6% increase from $1.67 billion in fiscal 2024. The company reported consolidated same-store sales growth of 5.5%, with physical stores up 5.0% and e-commerce channels showing stronger growth at 9.7%. This represents a significant turnaround from the 6.2% same-store sales decline experienced in fiscal 2024.

As shown in the following comprehensive financial metrics, Boot Barn achieved substantial margin improvements and bottom-line growth:

The company’s earnings per diluted share reached $5.88, representing a 22.5% increase from $4.80 in the previous fiscal year. Merchandise margin improved to 50.1%, up 130 basis points year-over-year and an impressive 580 basis points over the past five years. This margin expansion has been driven largely by the company’s exclusive brands strategy, which now accounts for 38.6% of sales, up 90 basis points from fiscal 2024 and 1,660 basis points over five years.

Boot Barn’s long-term growth trajectory is illustrated in this decade-long sales chart, showing a compound annual growth rate of approximately 19%:

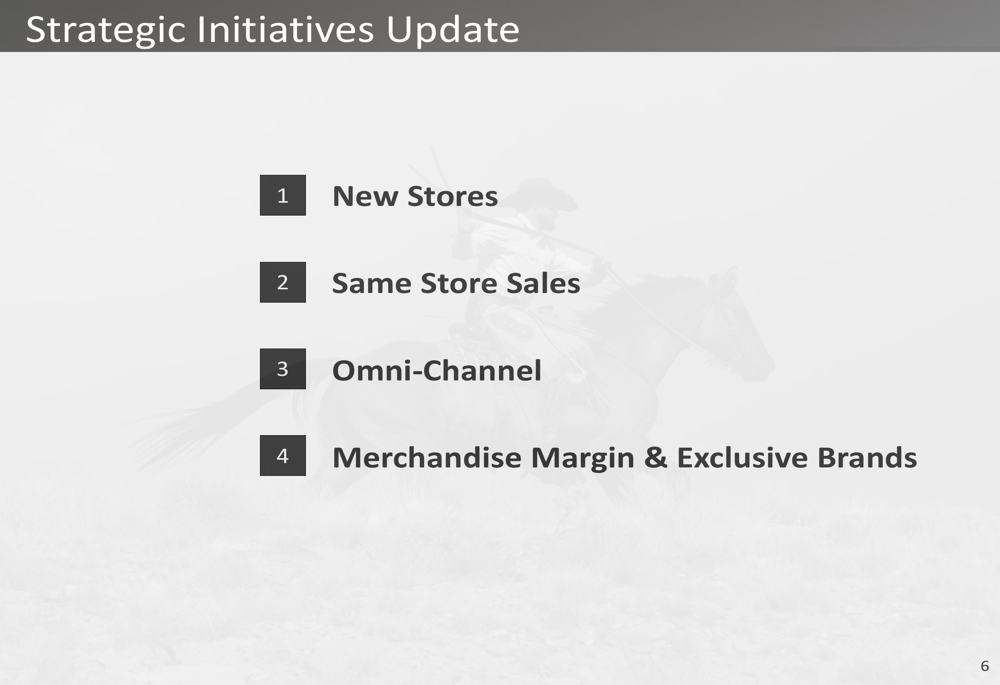

Strategic Initiatives

Boot Barn’s growth strategy centers around four key initiatives: new store openings, same-store sales growth, omni-channel capabilities, and merchandise margin expansion through exclusive brands.

The company opened 60 new stores in fiscal 2025, up from 55 in the previous year, and plans to maintain its 15% annual store growth rate. New stores have demonstrated strong profitability metrics, with approximately $3.2 million in first-year sales, $0.9 million in EBITDA, and a 53% cash-on-cash return, resulting in a payback period of just 1.8 years.

The following chart illustrates Boot Barn’s historical and projected store count growth:

Exclusive brands represent a significant driver of margin expansion, with six proprietary brands accounting for approximately 35% of sales volume. The company expects exclusive brands penetration to reach 39.6% in fiscal 2026, contributing to continued margin accretion.

As shown in the following chart detailing exclusive brands growth and margin expansion:

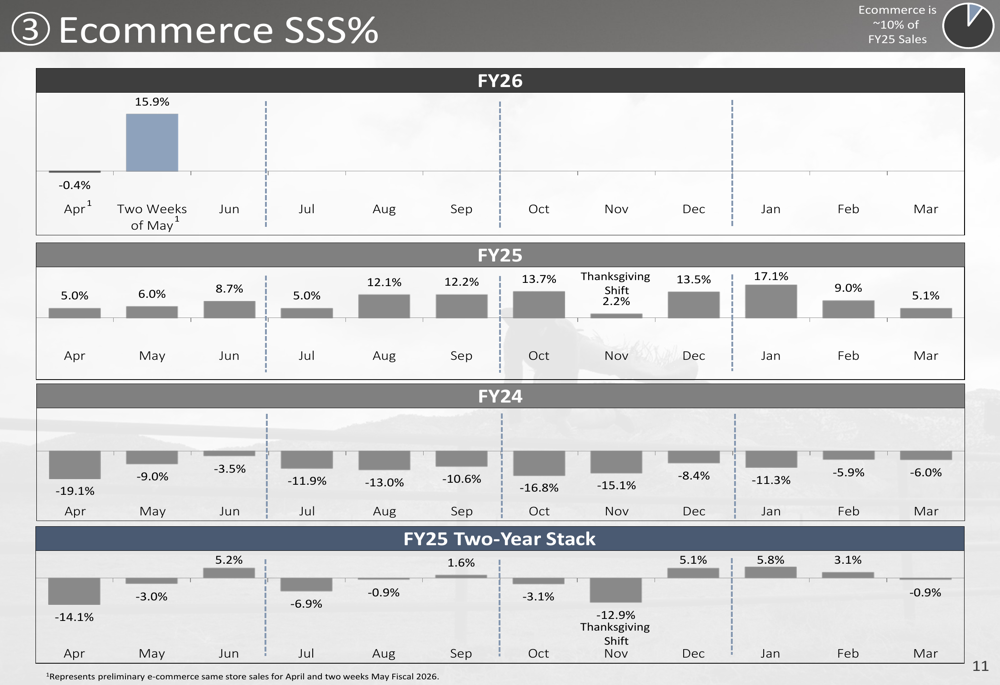

Boot Barn’s omni-channel strategy has shown success, with e-commerce same-store sales increasing 9.7% in fiscal 2025. The company has implemented various digital capabilities to drive store traffic, enhance in-store experiences, and efficiently fulfill online demand, including mobile apps, AI-enabled tools like Range Finder, and same-day delivery options.

FY2026 Guidance and Tariff Impact

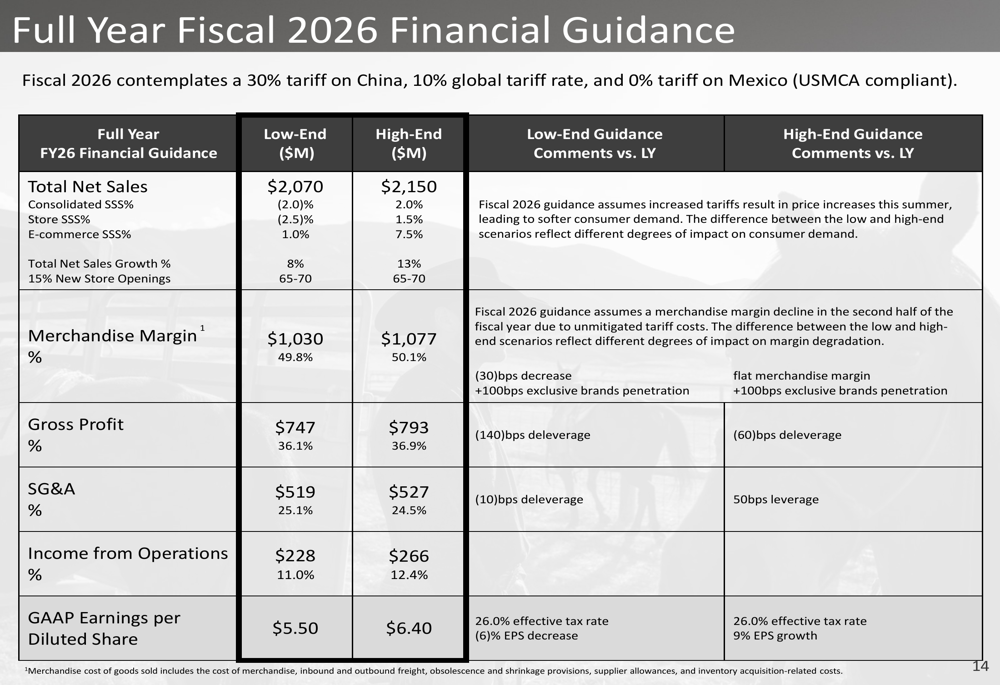

Looking ahead to fiscal 2026, Boot Barn provided guidance that incorporates the assumption of a 30% tariff on Chinese imports and a 10% global tariff rate, while assuming 0% tariff on Mexico-sourced products under USMCA compliance.

The following table details the company’s financial guidance for fiscal 2026:

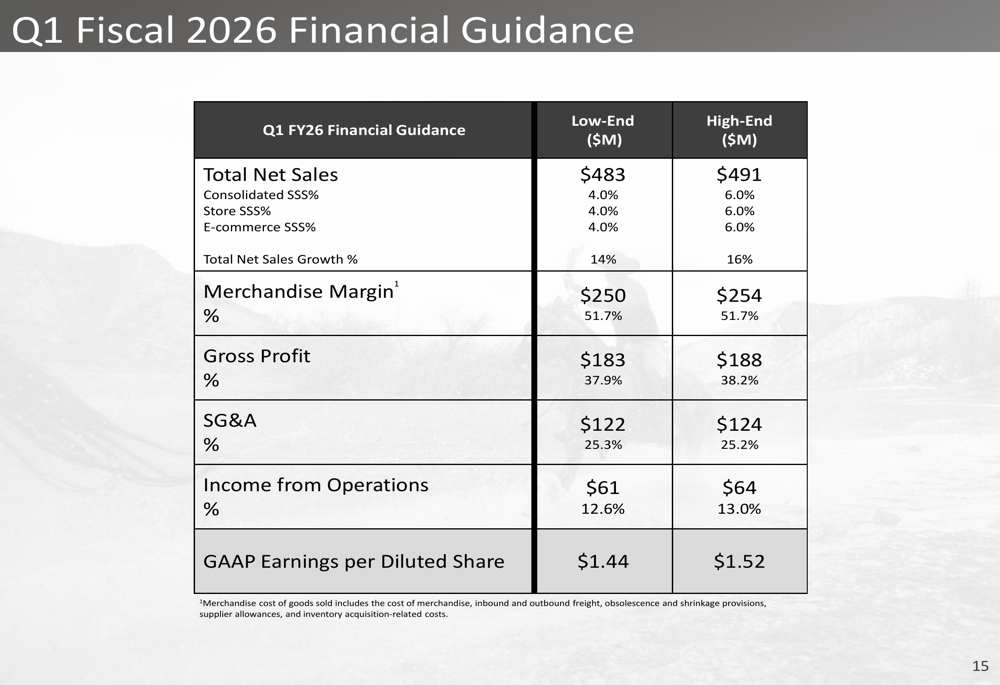

For the first quarter of fiscal 2026, Boot Barn expects:

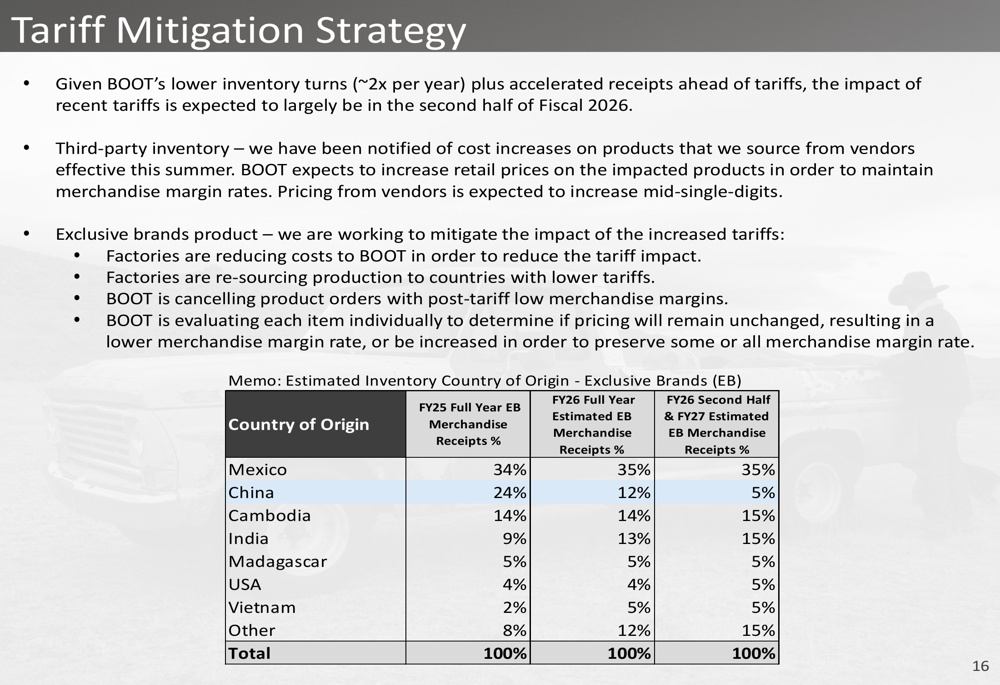

To mitigate tariff impacts, Boot Barn has developed a comprehensive strategy that includes leveraging lower inventory turns to accelerate receipts ahead of tariff implementation, increasing retail prices on affected third-party products, and re-sourcing production for exclusive brands. The company plans to significantly reduce its reliance on Chinese manufacturing, projecting a decrease in China-sourced exclusive brand merchandise from 24% in fiscal 2025 to just 5% by the second half of fiscal 2026 and fiscal 2027.

The following table illustrates Boot Barn’s planned shift in sourcing for exclusive brands:

The company estimates that tariffs will impact fiscal 2026 exclusive brands merchandise cost of goods sold by approximately $8 million, after accounting for mitigation efforts:

Additionally, Boot Barn announced a $200 million share repurchase program authorized by its Board of Directors. The company plans to execute approximately one-quarter of this authorization during fiscal 2026, with spending distributed roughly equally across quarters.

Investment Considerations

Boot Barn positioned itself as a national leader in the western wear market with significant growth opportunities. The company highlighted its proven ability to open profitable new stores with minimal sales cannibalization, world-class omni-channel capabilities, and continued margin expansion potential through exclusive brands and supply chain efficiencies.

The company’s guidance for fiscal 2026 reflects both confidence in its growth strategy and caution regarding potential tariff impacts. While Boot Barn expects continued sales growth of 8-13% and plans to open 65-70 new stores, it has incorporated potential consumer demand softness due to price increases resulting from tariffs.

Despite these challenges, Boot Barn’s long-term expansion plans remain intact, with management believing the company has the market potential to double its store count in the U.S. alone over the next several years. With a strong track record of growth, margin expansion, and strategic execution, Boot Barn appears well-positioned to navigate near-term tariff headwinds while continuing its national expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.