EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

Box Inc. (NYSE:BOX) presented its first quarter fiscal year 2026 financial results on May 27, 2025, showcasing steady revenue growth alongside significant increases in billings and remaining performance obligations (RPO). The content management platform provider’s stock responded positively, surging 11.35% in aftermarket trading to $35.02, approaching its 52-week high of $35.74.

The company’s Q1 performance reflects its continued focus on expanding Suite adoption among customers while maintaining a balance between growth and profitability. Box’s results generally aligned with or exceeded analyst expectations, with particular strength in forward-looking indicators like billings and RPO.

Quarterly Performance Highlights

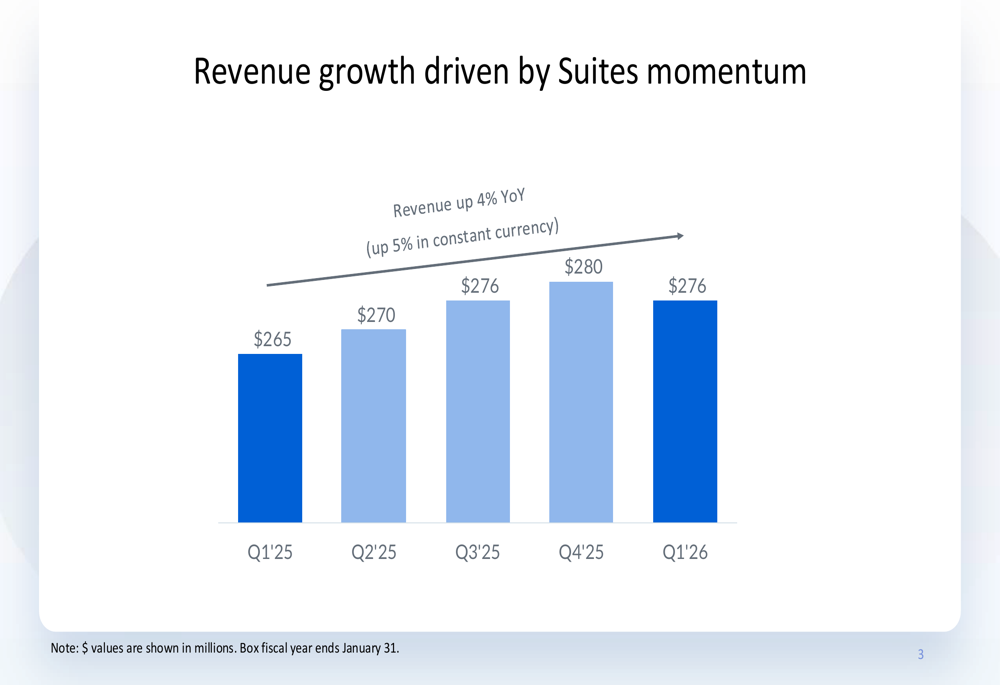

Box reported Q1 FY26 revenue of $276 million, representing a 4% year-over-year increase (5% in constant currency). While this growth rate remains modest, the company’s billings showed substantial momentum, increasing 27% year-over-year to $242 million (17% in constant currency).

As shown in the following chart of quarterly revenue growth:

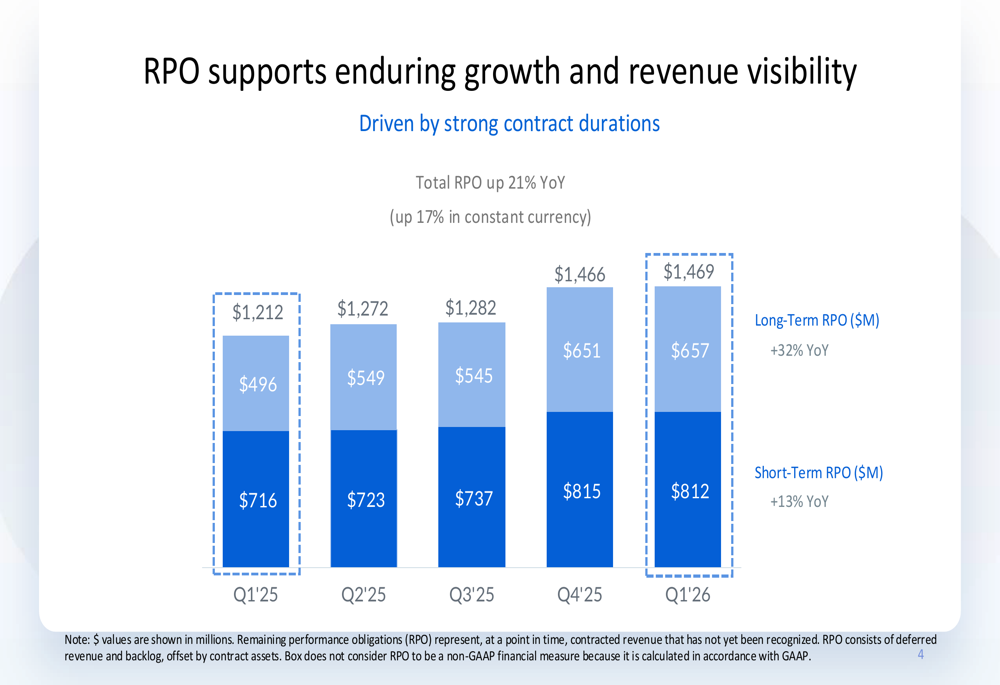

The company’s total remaining performance obligations (RPO) reached $1.47 billion, up 21% year-over-year (17% in constant currency), providing strong visibility into future revenue streams. The RPO breakdown shows particularly strong growth in long-term commitments, which increased 32% year-over-year to $657 million.

As illustrated in this RPO breakdown:

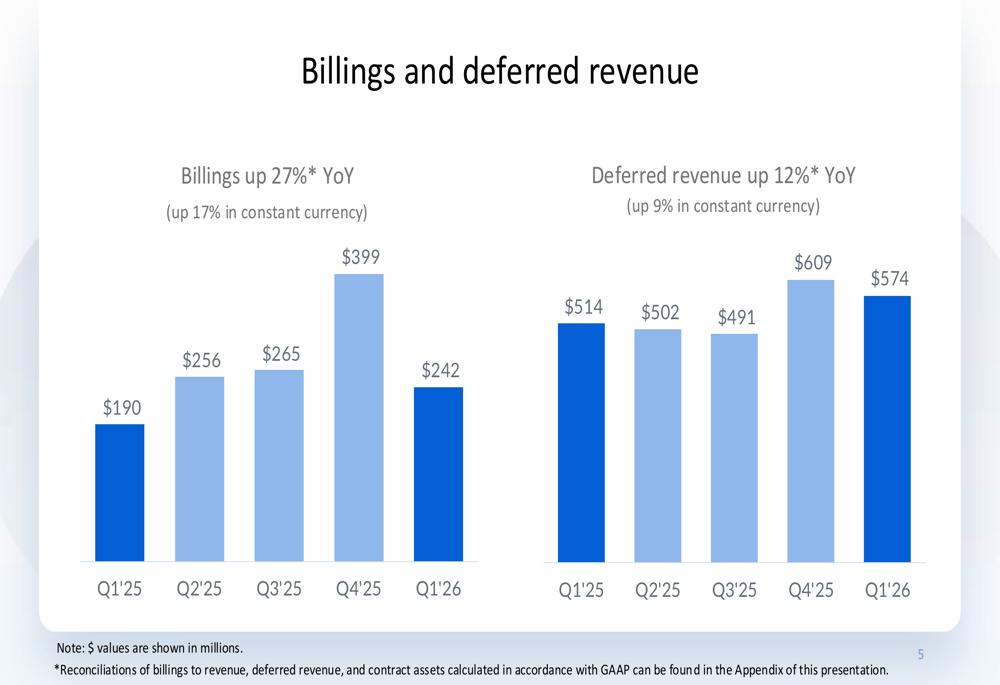

Box’s billings growth significantly outpaced revenue growth, suggesting accelerating business momentum. The deferred revenue balance grew to $574 million, up 12% year-over-year.

The following chart details the billings and deferred revenue trends:

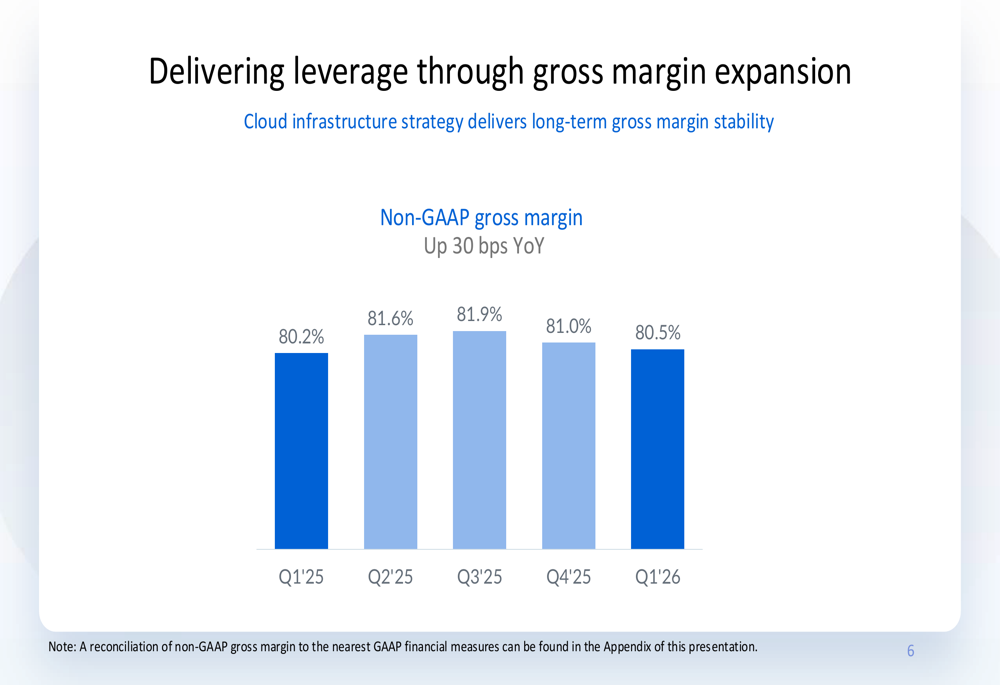

On the profitability front, Box maintained strong gross margins while experiencing a slight decline in operating margins. The non-GAAP gross margin was 80.5%, up 30 basis points year-over-year, demonstrating the company’s ability to deliver leverage through its cloud infrastructure strategy.

This gross margin expansion is visualized here:

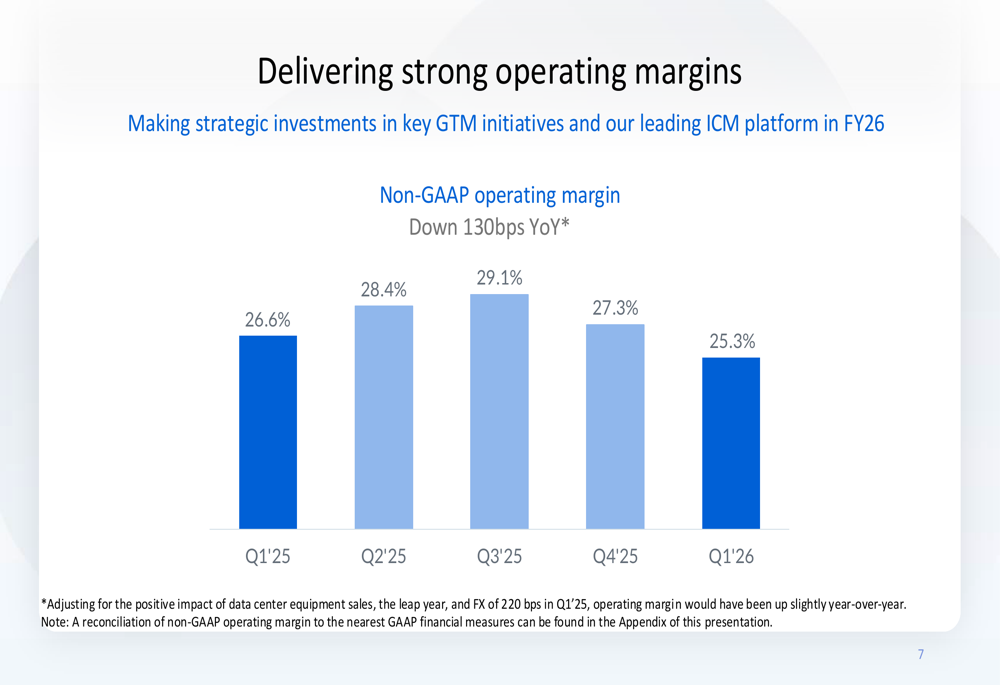

The non-GAAP operating margin was 25.3%, down 130 basis points year-over-year. However, the company noted that adjusting for one-time factors in Q1 FY25 (including data center equipment sales, leap year effects, and foreign exchange impacts totaling 220 basis points), the operating margin would have shown a slight year-over-year improvement.

The operating margin trend is shown below:

Box ended the quarter with a strong cash position of $792 million in cash, cash equivalents, restricted cash, and short-term investments, up from $724 million in the previous quarter. The company generated $127 million in operating cash flow while returning $50 million to shareholders through share repurchases.

Strategic Initiatives

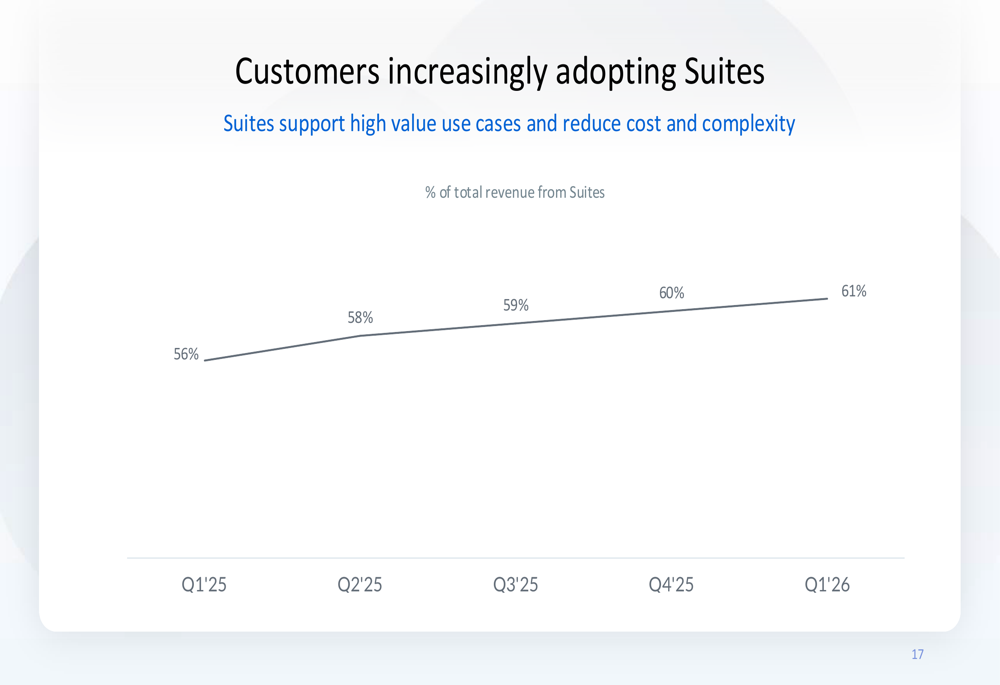

A key driver of Box’s business model is the increasing adoption of its Suite offerings, which bundle multiple capabilities to address high-value use cases while reducing cost and complexity for customers. The percentage of total revenue from Suites reached 61% in Q1 FY26, continuing a steady upward trend from 56% a year earlier.

The following chart illustrates this Suite adoption trend:

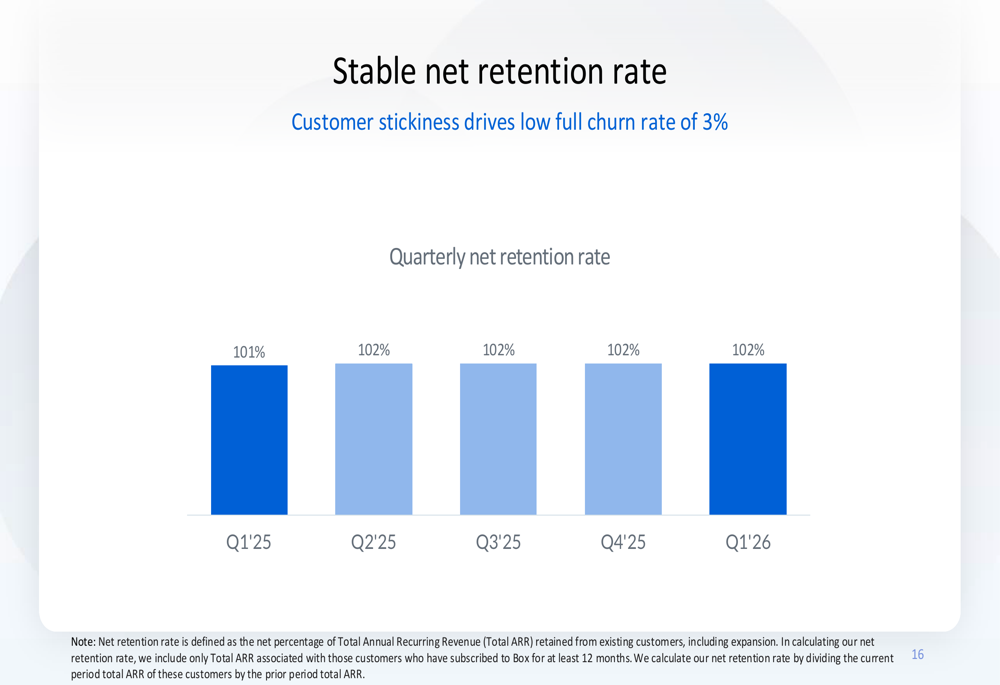

Box maintained a stable net retention rate of 102%, consistent with the previous three quarters. This metric, combined with a low full churn rate of 3%, demonstrates strong customer stickiness.

As shown in this net retention rate chart:

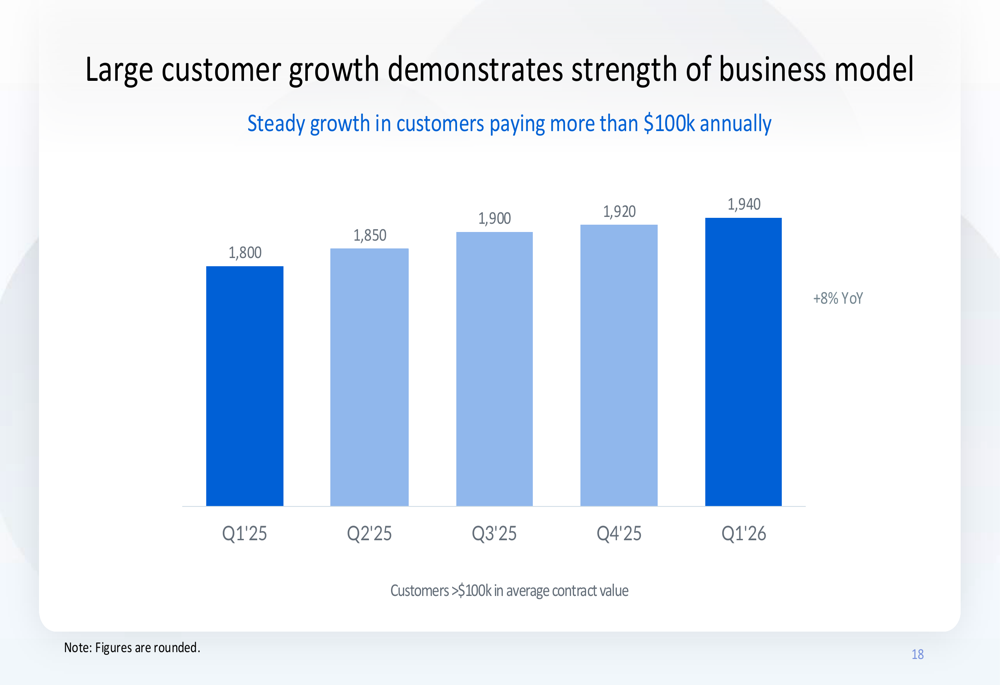

The company continues to see growth in its large customer segment, with customers paying more than $100,000 annually increasing 8% year-over-year to 1,940. These enterprise customers represent a significant growth opportunity as they adopt more Box capabilities.

The large customer growth trend is visualized here:

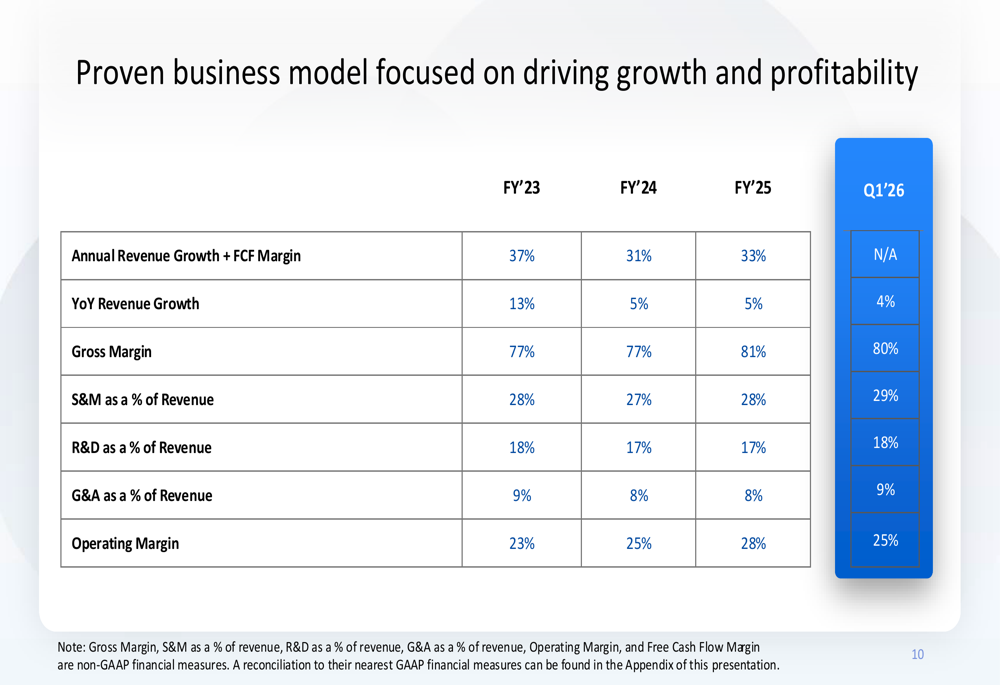

Box’s business model focuses on driving both growth and profitability, as evidenced by its consistent performance across key metrics over the past several years. The company has maintained strong gross margins while optimizing sales and marketing, R&D, and G&A expenses as percentages of revenue.

This balanced approach is summarized in the following business model overview:

Forward-Looking Statements

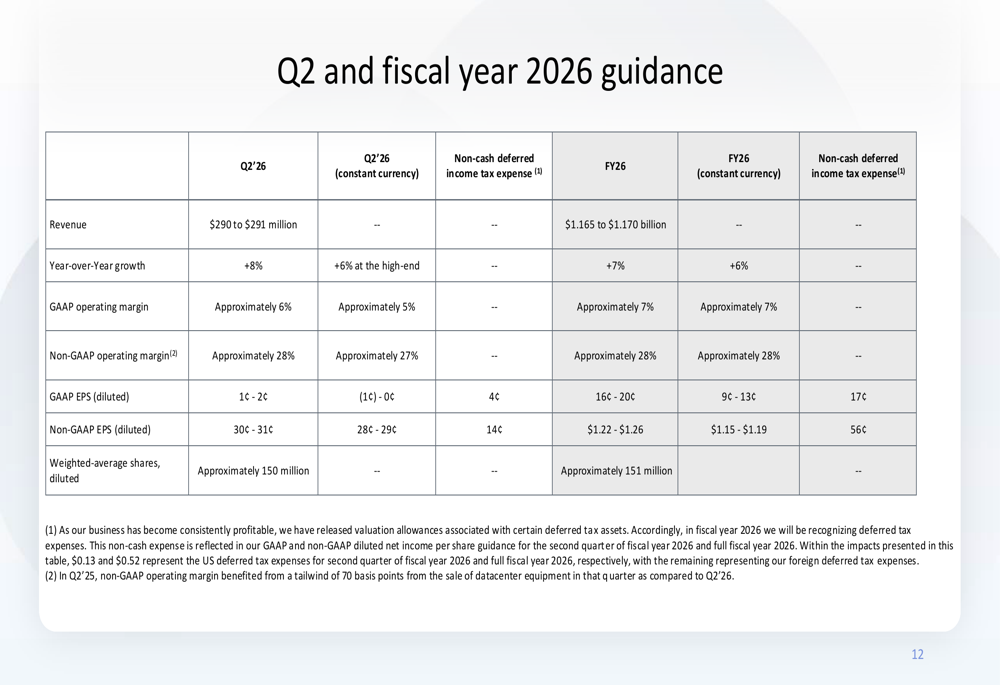

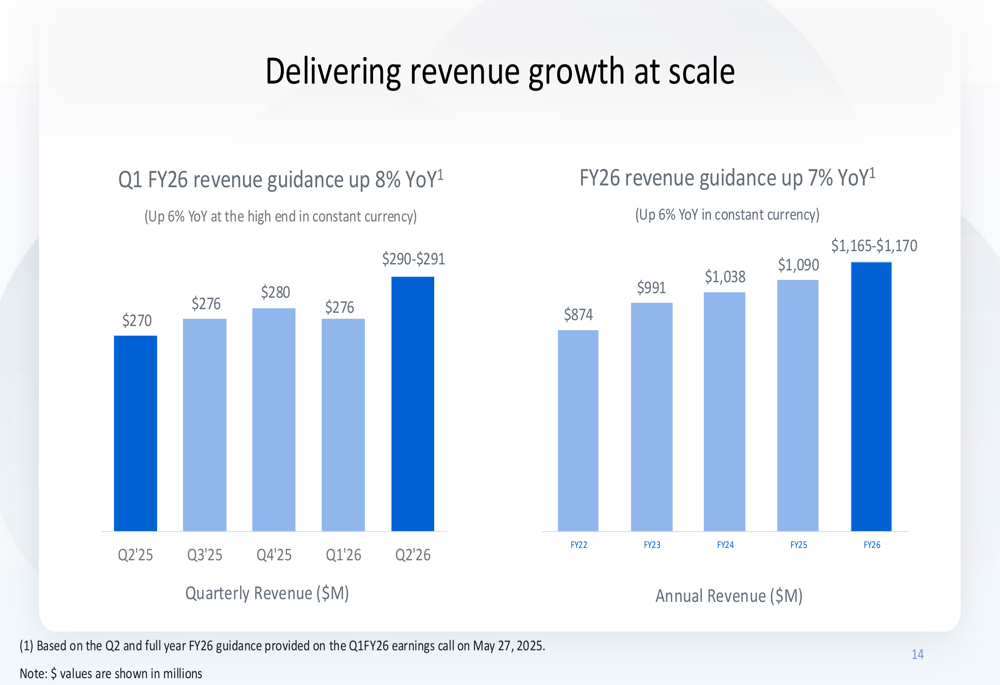

Box provided an optimistic outlook for both Q2 FY26 and the full fiscal year. For Q2, the company expects revenue between $290-$291 million, representing 8% year-over-year growth. The full-year revenue guidance of $1.165-$1.170 billion implies 7% year-over-year growth.

The detailed guidance includes:

The company’s revenue growth is projected to accelerate in the coming quarters, as illustrated in the following revenue trajectory chart:

Box expects to maintain its strong profitability profile, with a non-GAAP operating margin of approximately 28% for both Q2 and the full fiscal year. This represents an improvement from the 25.3% reported in Q1 FY26.

The company’s full-year non-GAAP EPS guidance of $1.22-$1.26 reflects confidence in its ability to drive both top-line growth and bottom-line results. With a stable net retention rate, increasing Suite adoption, and growing large customer base, Box appears well-positioned to execute on its growth strategy for the remainder of fiscal year 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.