S&P 500 rises as health care, tech gain to overshadow Fed independence concerns

Introduction & Market Context

Braemar Hotels & Resorts Inc. (NYSE:BHR) achieved record RevPAR in Q1 2025 despite facing expense pressures, according to the company’s first quarter earnings presentation. The luxury hotel REIT reported a net loss of $2.5 million or $0.04 per diluted share, outperforming analyst expectations of a $0.15 loss per share.

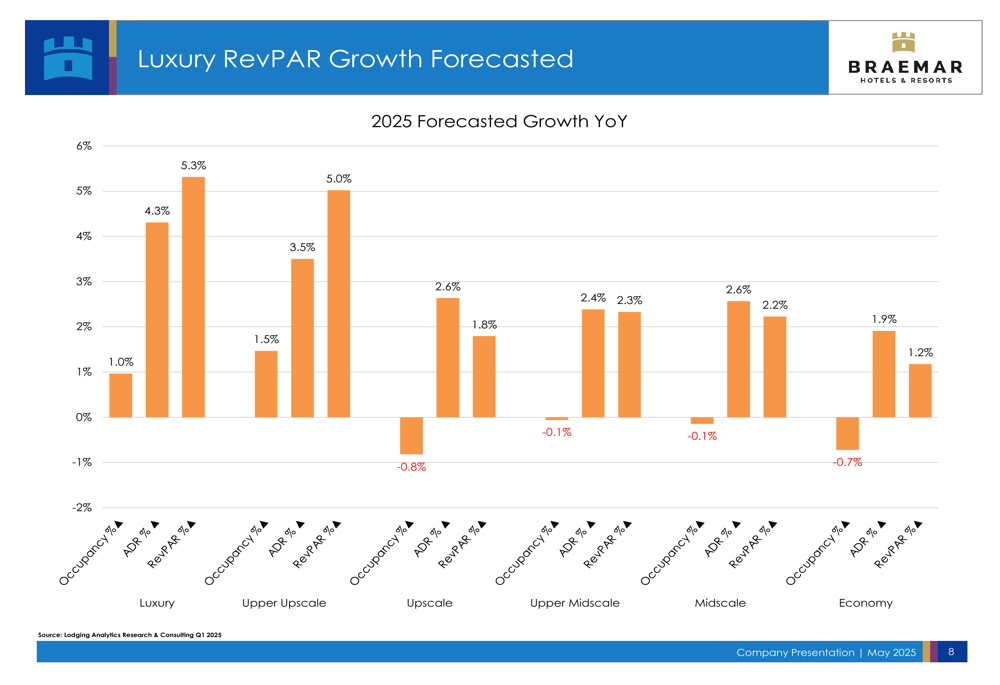

The company operates in a hospitality industry where luxury and upper upscale segments continue to outperform other categories. According to data presented by Braemar, industry RevPAR continues to exceed 2019 levels, with the luxury segment forecasted to see the strongest growth in 2025 at 5.3%.

As shown in the following chart illustrating industry RevPAR growth forecasts by segment:

Quarterly Performance Highlights

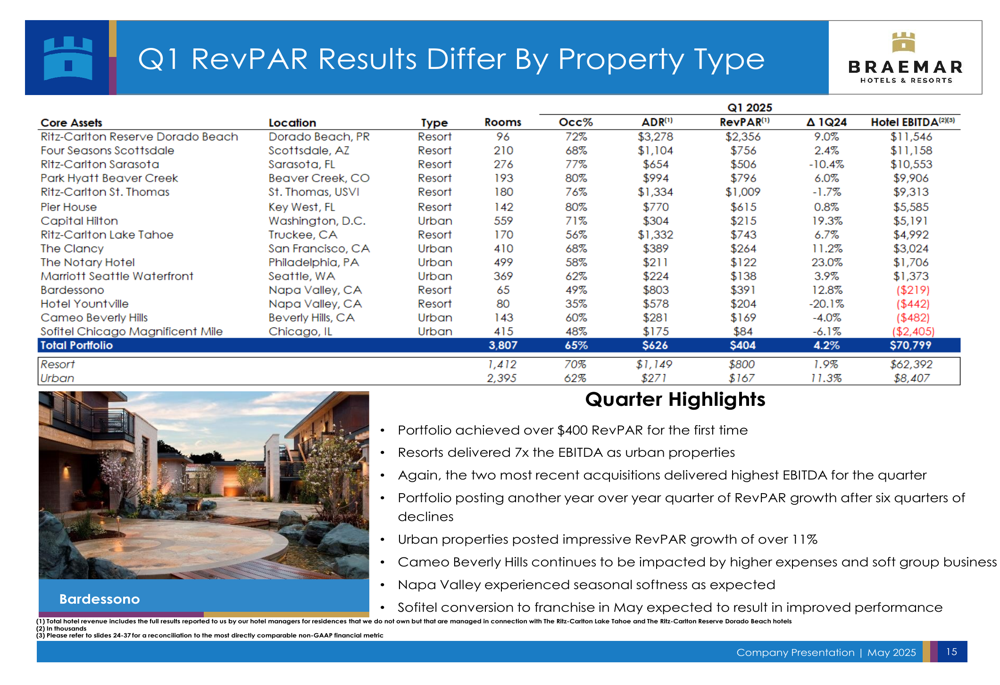

Braemar’s portfolio achieved over $400 RevPAR for the first time in Q1 2025, marking a significant milestone. Comparable Hotel EBITDA reached $70.8 million for the quarter, reflecting a 5.3% increase over the prior year period. Adjusted funds from operations (AFFO) was $0.40 per diluted share.

The company’s performance showed a stark contrast between property types, with resort properties delivering seven times the EBITDA of urban properties. However, urban properties posted impressive RevPAR growth of over 11% year-over-year, indicating potential recovery in city center locations.

The following table details Q1 2025 performance metrics by property:

Despite the record RevPAR achievement, Braemar faced challenges with higher expenses and interest rates. Revenue came in at $218.41 million, slightly below analyst forecasts of $221.68 million, according to the recent earnings report. The company’s stock rose 2.86% in after-hours trading following the earnings announcement, suggesting investor confidence in the operational improvements.

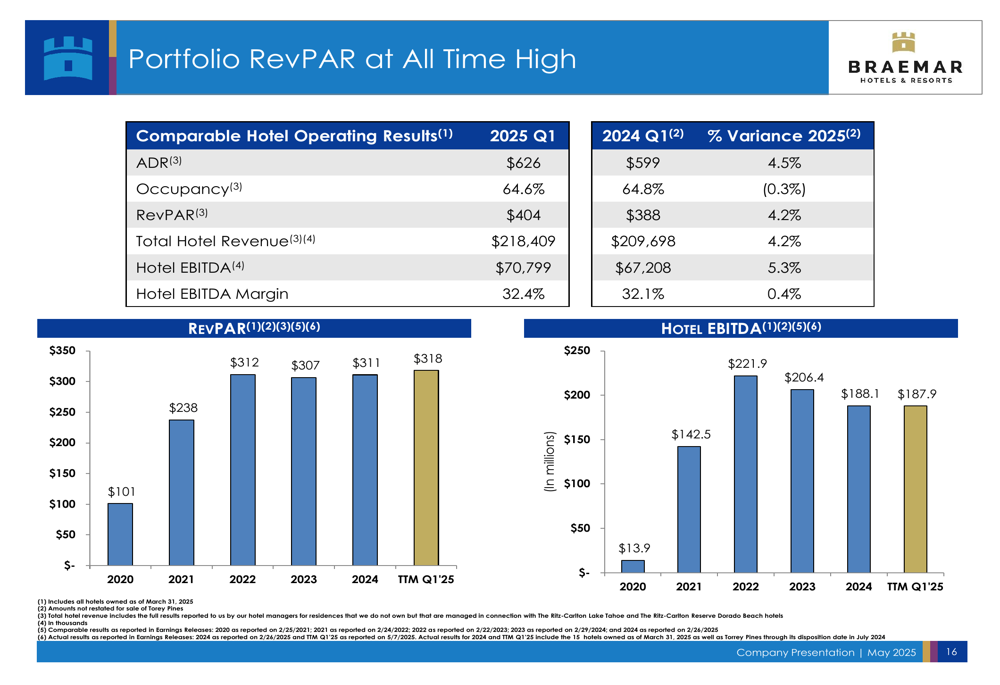

The presentation highlighted the company’s RevPAR trends over time, showing the portfolio’s performance at an all-time high:

Portfolio Strategy and Performance

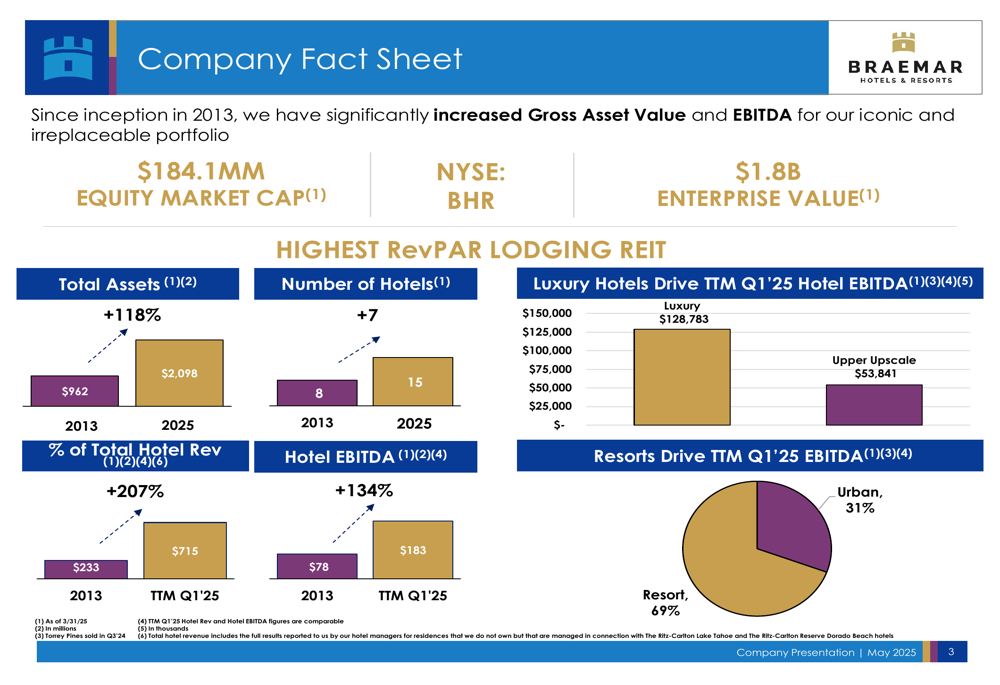

Since its inception in 2013, Braemar has significantly transformed its portfolio, focusing on luxury and resort properties. The company has increased its total assets by 118% and hotel EBITDA by 134%, while growing hotel revenue by 207%.

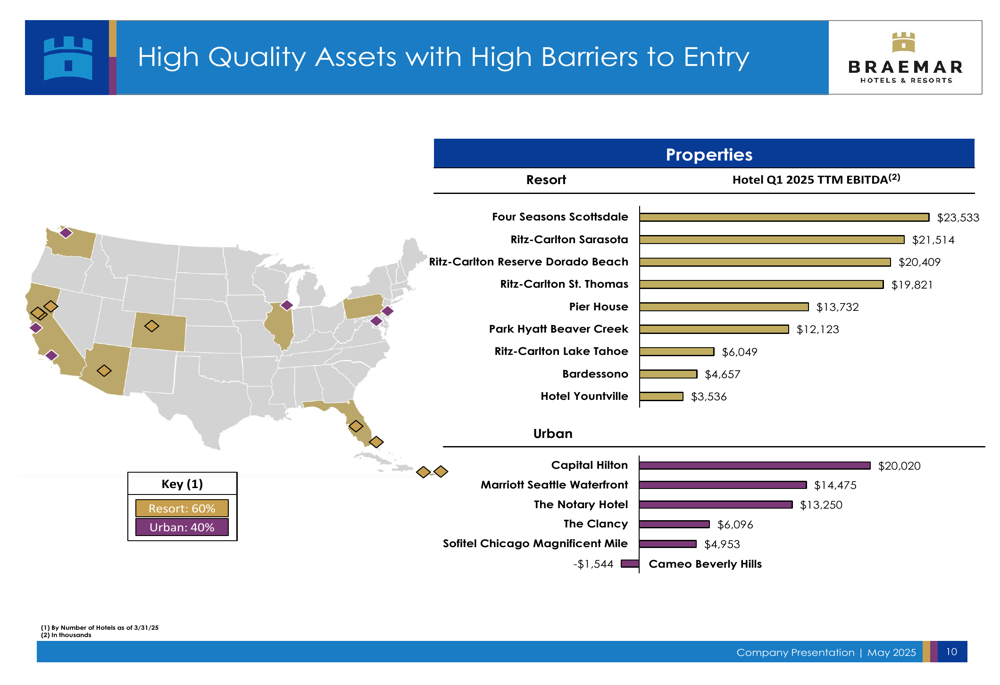

The company’s current portfolio consists of 60% resort and 40% urban properties by number of hotels, though resorts contribute 69% of the total EBITDA. This strategic positioning has allowed Braemar to benefit from strong leisure demand, particularly at high-end resort destinations.

As illustrated in this comprehensive fact sheet showing the company’s growth since inception:

Braemar’s portfolio includes prestigious properties across luxury brands including Ritz-Carlton, Four Seasons, and Park Hyatt, with high barriers to entry in desirable locations. The company’s RevPAR has stabilized at a higher level post-pandemic, with resort RevPAR showing a 5-year CAGR of 12.9%, significantly outpacing urban properties at 5.6%.

The following map and table highlight the company’s diverse portfolio of luxury assets:

Capital Expenditure Plans

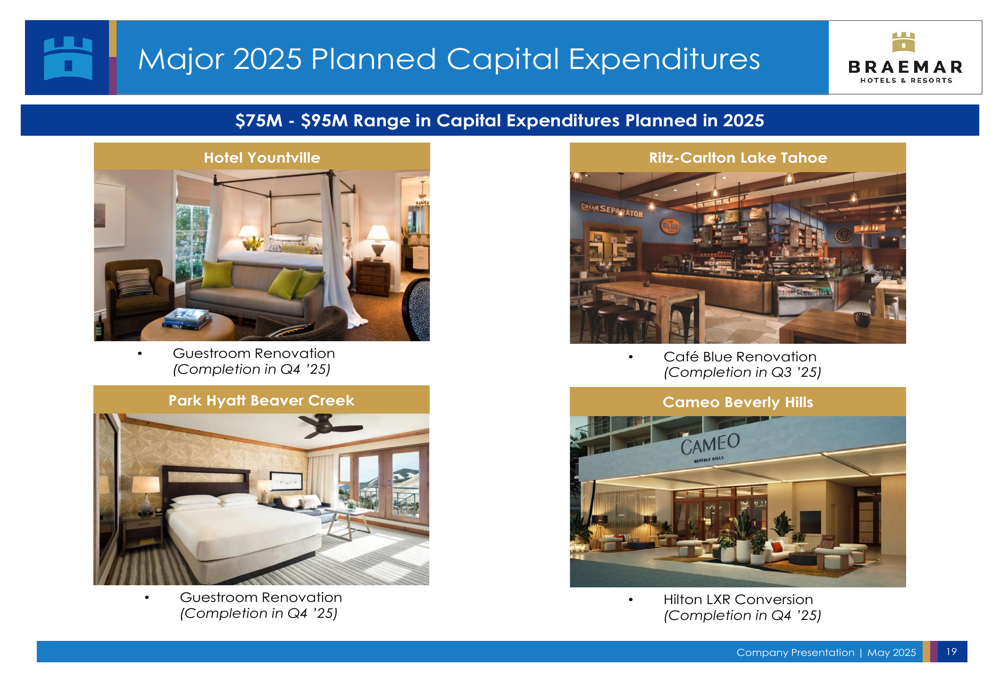

Braemar has outlined an ambitious capital expenditure plan for 2025, with total investments expected to range between $75 million and $95 million. Key projects include guestroom renovations at Hotel Yountville and Park Hyatt Beaver Creek, a Café Blue renovation at Ritz-Carlton Lake Tahoe, and a Hilton LXR conversion at Cameo Beverly Hills.

The company invested $15.3 million in capex during Q1 2025, continuing its strategy of enhancing property values through strategic renovations and brand conversions.

As shown in the following slide detailing major planned capital expenditures for 2025:

Liability Management

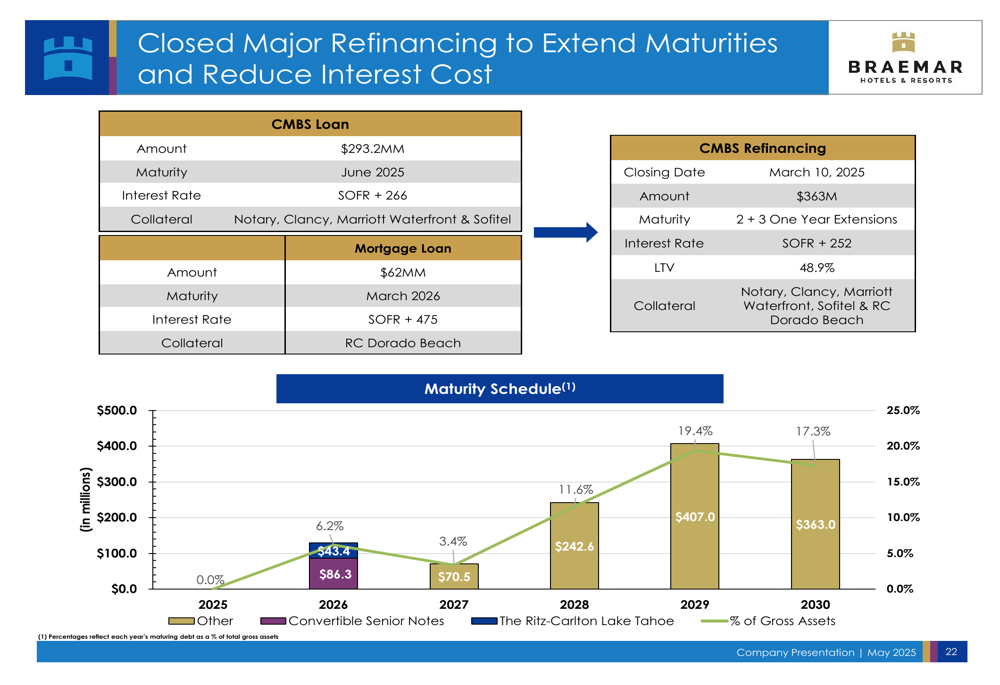

A significant development in Q1 2025 was Braemar’s completion of major refinancing to extend debt maturities and reduce interest costs. The company refinanced a $293.2 million CMBS loan maturing in June 2025 with a new loan at SOFR plus 266 basis points, and a $62 million mortgage loan maturing in March 2026 at SOFR plus 475 basis points.

As of March 31, 2025, Braemar reported a net debt to gross assets ratio of 42.3%, with a weighted average interest rate of 7.07% across its debt portfolio. The refinancing efforts have helped the company manage its debt maturity schedule more effectively.

The following slide illustrates the company’s refinancing achievements and maturity schedule:

Forward-Looking Statements

Looking ahead, Braemar remains cautiously optimistic about its portfolio performance while focusing on cost containment and operational efficiency. The luxury segment is forecasted to lead the industry in RevPAR growth for 2025, which aligns well with the company’s portfolio positioning.

Management indicated during the earnings call that they are considering potential asset sales of one to two upper upscale properties, with proceeds potentially directed toward preferred equity redemptions, share buybacks, or debt retirement. The company also expects the Sofitel Chicago’s conversion to a franchise model in May to result in improved performance.

Braemar added a new board director, Kellie Sirna, owner and principal of Studio 11 Design, bringing global travel and design expertise to the company’s leadership team. This addition strengthens the board’s hospitality industry knowledge as the company navigates the evolving luxury hotel landscape.

As of June 16, 2025, Braemar’s stock was trading at $2.475, up 3.13% on the day, with a 52-week range of $1.80 to $3.95. Despite operational improvements and beating EPS expectations, the company continues to face challenges with expense management and interest costs in a competitive luxury hospitality environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.