5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Bravida Holding AB (STO:BRAV) presented its second-quarter 2025 results on July 11, highlighting improved profitability despite challenging market conditions across the Nordic region. The technical installation and service provider, which operates across 190 locations with 14,000 employees, demonstrated resilience through its "margin over volume" strategy in a period marked by uneven regional performance.

The company’s stock recently closed at 92.5 SEK, experiencing a minor decline of 0.16% in its latest trading session. Bravida continues to navigate a complex market environment where service activity remains stable while the installation segment faces ongoing challenges.

As shown in the following overview of Bravida’s scale and reach:

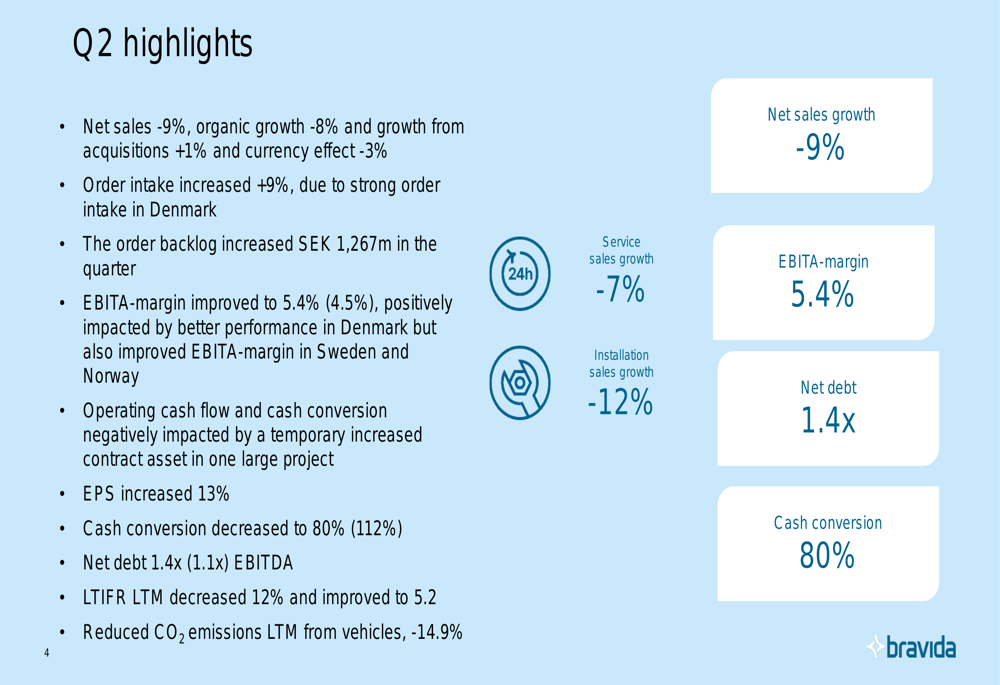

Quarterly Performance Highlights

Bravida reported a 9% decrease in net sales for Q2 2025, with organic growth at -8%, acquisition growth contributing +1%, and currency effects impacting results by -3%. Despite this revenue decline, the company achieved a significant improvement in its EBITA margin, which rose to 5.4% from 4.5% in the same period last year.

Order intake showed encouraging growth of 9% year-over-year, driven primarily by strong performance in Denmark, which included a large order from an industrial company. The order backlog increased by SEK 1,267 million during the quarter, providing a solid foundation for future operations.

The following slide summarizes the key Q2 highlights:

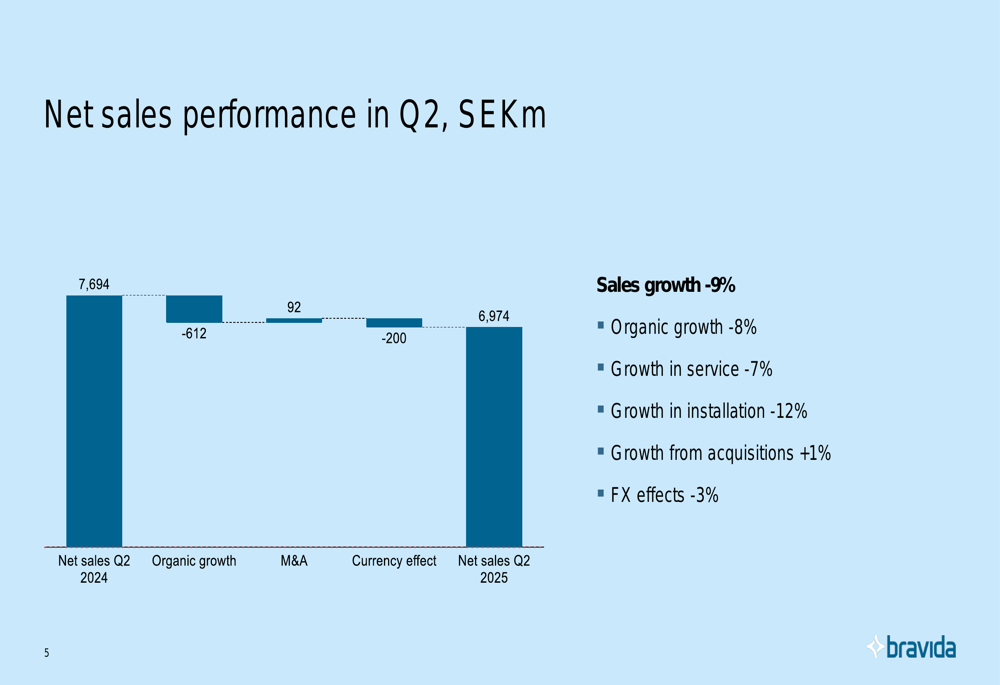

Breaking down the sales performance further, Bravida’s net sales declined from SEK 7,694 million in Q2 2024 to SEK 6,974 million in Q2 2025. The service segment performed better with a 7% decline, while installation experienced a steeper 12% drop.

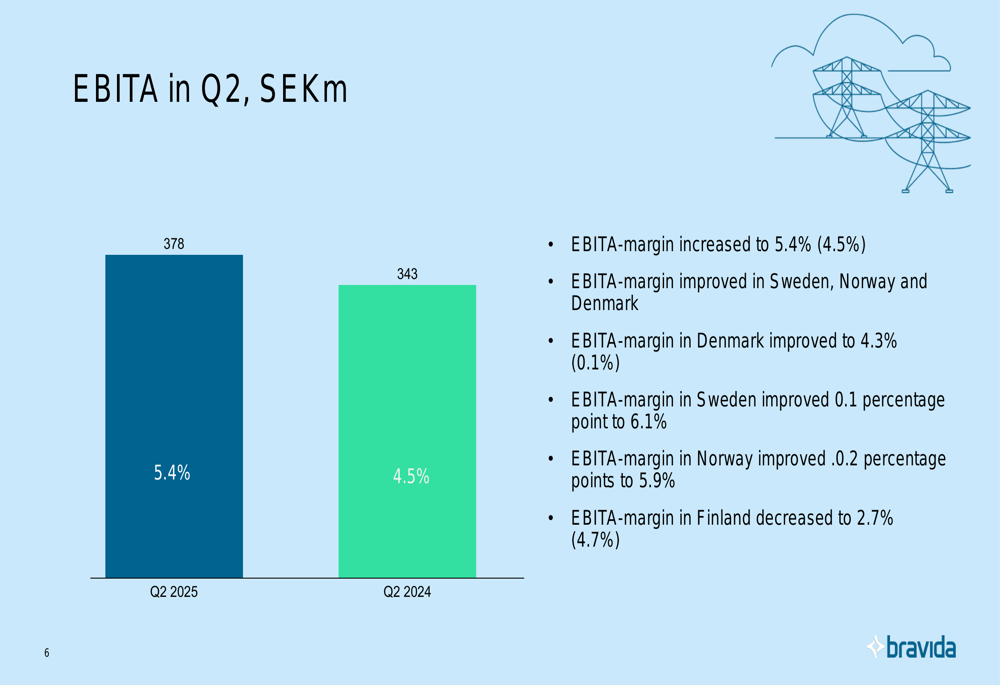

Despite lower sales, EBITA improved to SEK 378 million compared to SEK 343 million in Q2 2024. This improvement in profitability reflects the company’s successful implementation of its margin-focused strategy across most regions.

Regional Performance Analysis

Bravida’s performance varied significantly across its four main markets, with Denmark showing remarkable improvement while Finland faced challenges.

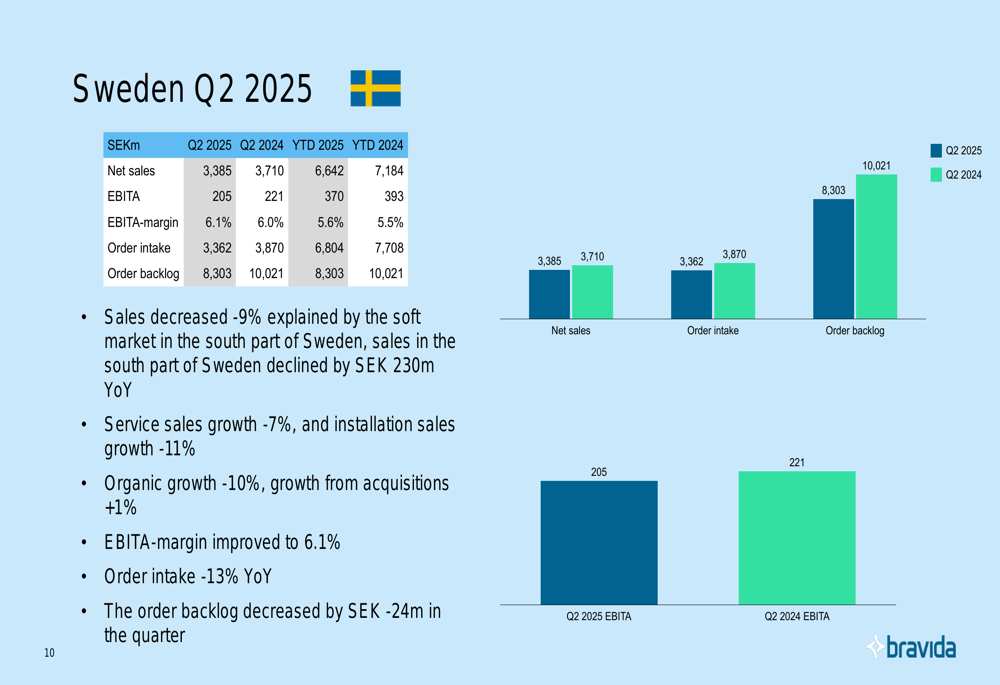

In Sweden, which remains Bravida’s largest market, net sales decreased by 9% to SEK 3,385 million. The decline was particularly pronounced in southern Sweden. Despite lower sales, the EBITA margin improved slightly to 6.1% from 6.0% in Q2 2024, demonstrating effective cost management.

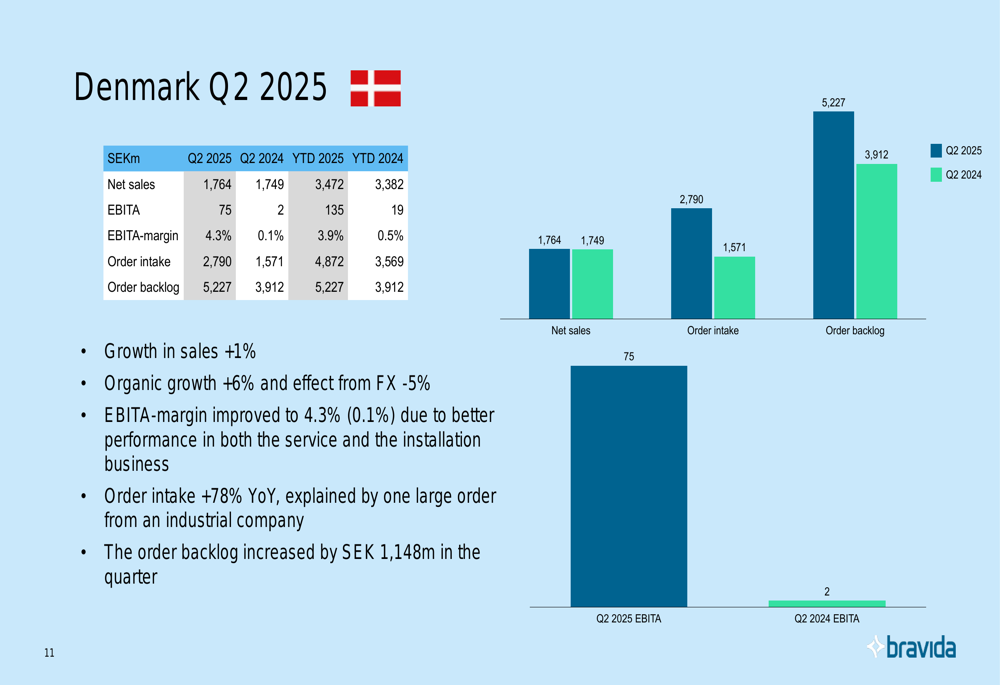

Denmark emerged as the standout performer, with sales growth of 1% and a dramatic improvement in EBITA margin from just 0.1% in Q2 2024 to 4.3% in Q2 2025. Order intake surged by 78% year-over-year, bolstered by a significant industrial contract, and the order backlog increased by SEK 1,148 million during the quarter.

Norway experienced an 18% decline in sales, with both installation (-27%) and service (-10%) segments contracting. Despite this, the EBITA margin improved to 5.9% from 5.7%. The Norwegian operation managed to increase its order backlog by SEK 143 million during the quarter.

Finland showed the most challenging performance, with a 15% sales decline and EBITA margin decreasing to 2.7% from 4.7% in Q2 2024. The Finnish market faced difficulties in both installation (-12%) and service (-20%) segments.

Strategic Initiatives & Outlook

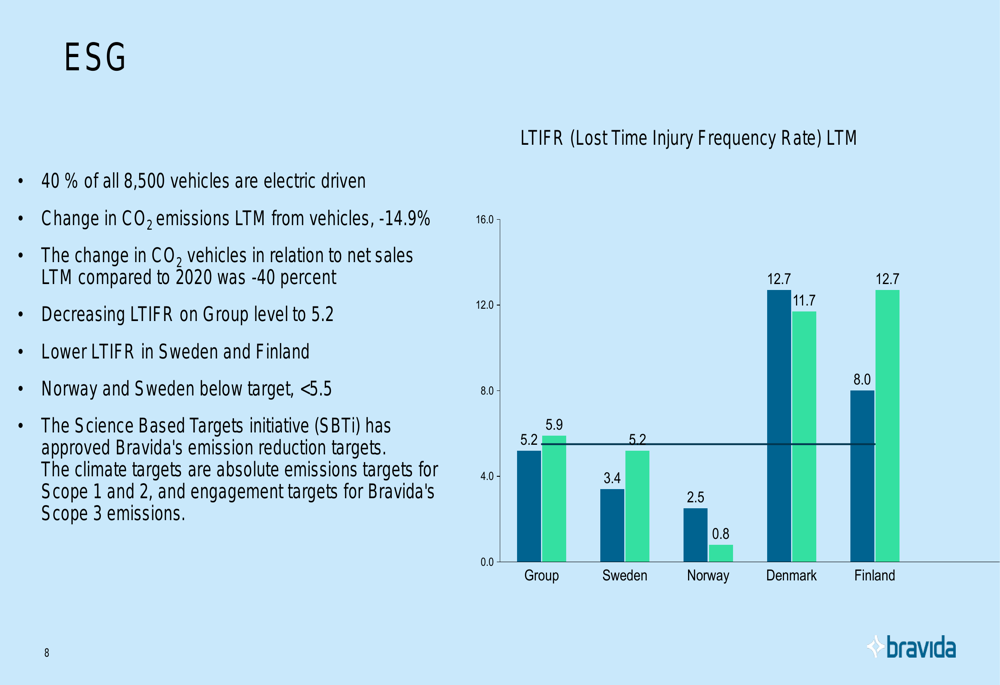

Bravida continues to advance its ESG agenda, with 40% of its 8,500-vehicle fleet now electric-powered. The company reported a 14.9% reduction in CO2 emissions from vehicles over the last twelve months, and a 40% decrease in CO2 emissions relative to net sales since 2020. Safety performance also improved, with the Lost Time Injury Frequency Rate decreasing by 12% to 5.2.

The company’s commitment to sustainability is illustrated in the following slide:

Acquisition strategy remains a key growth driver, with one acquisition completed in Q2 adding SEK 346 million in annual sales, and another in early Q3 in Finland contributing an additional SEK 45 million. However, management noted challenges in identifying suitable acquisition targets in the current uncertain market environment.

Looking ahead, Bravida expects service activity to remain stable while installation continues to face challenges. The company sees favorable opportunities in infrastructure, industry, defense facilities, and civil engineering projects. Management remains committed to its project-selective strategy with continued focus on cost control.

Financial Position & Cash Flow

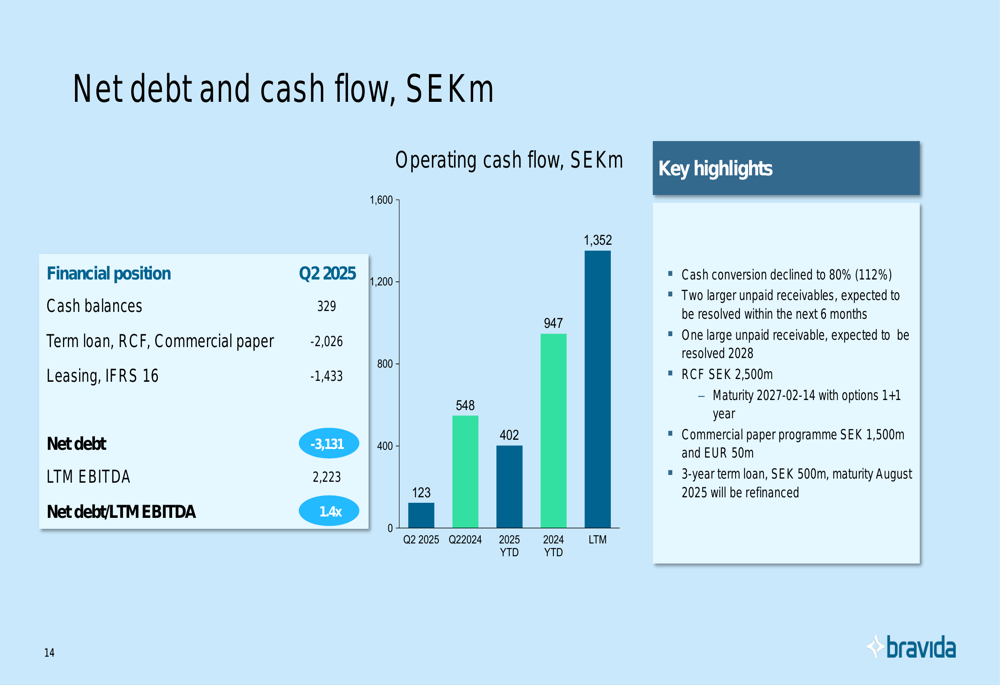

Bravida’s net debt stood at SEK 3,131 million at the end of Q2 2025, representing 1.4 times EBITDA compared to 1.1 times previously. Cash conversion declined to 80% from 112% in Q2 2024, primarily due to two larger unpaid receivables that management expects to resolve within the next six months.

The following slide details the company’s debt position and cash flow:

Earnings per share increased by 13% despite the sales challenges, reflecting improved operational efficiency and the success of the company’s margin-focused approach.

In summary, Bravida’s Q2 2025 results demonstrate the company’s ability to enhance profitability in a challenging market through disciplined cost management and strategic focus on higher-margin business. While regional performance varies significantly, with Denmark showing strong improvement and Finland facing headwinds, the overall trend of margin expansion and growing order backlog positions the company well for when market conditions improve, which management anticipates will begin in 2026-2027.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.