Bitcoin price today: gains to $120k, near record high on U.S. regulatory cheer

Introduction & Market Context

Bridgewater Bancshares, Inc. (NASDAQ:BWB) released its second quarter 2025 earnings presentation on July 24, 2025, highlighting continued momentum across key financial metrics. The Minnesota-based bank reported diluted earnings per share (EPS) of $0.38, representing a 19% increase from the $0.32 reported in the first quarter. The stock closed at $16.07 on July 23, up 0.37% for the day, and has shown resilience with a 52-week range of $11.93 to $17.66.

The bank’s performance builds on its strong first quarter results, with notable improvements in net interest margin, loan growth, and operational efficiency. This comes as the banking sector navigates a changing interest rate environment, with Bridgewater positioning itself to benefit from anticipated rate cuts.

Quarterly Performance Highlights

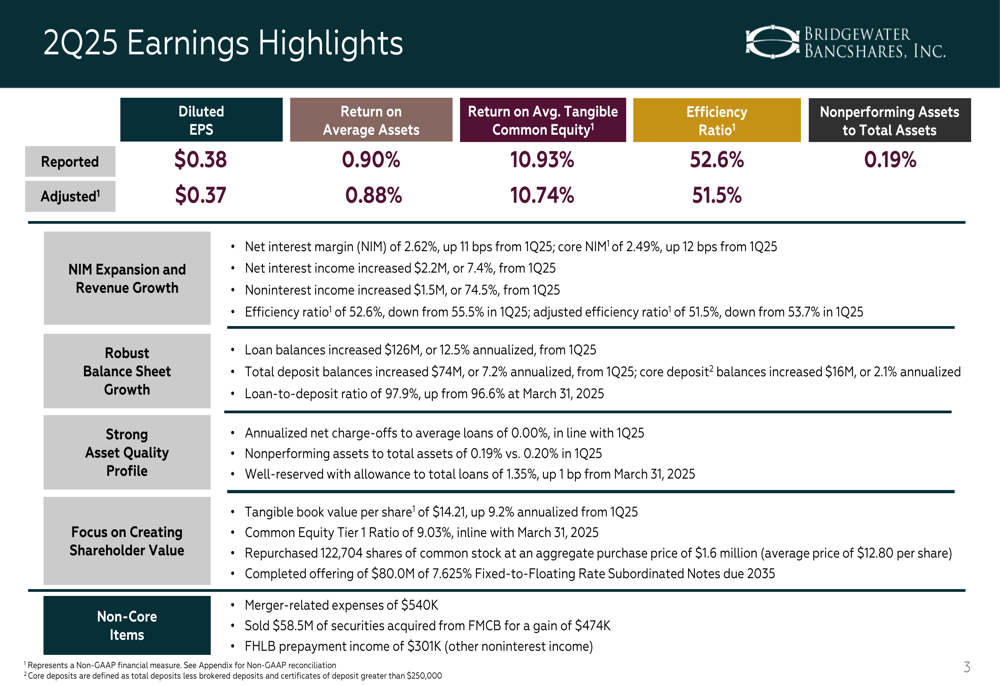

Bridgewater reported diluted EPS of $0.38 for Q2 2025, with adjusted EPS of $0.37 excluding merger-related expenses and securities gains. Return on average assets reached 0.90% (0.88% adjusted), while return on average tangible common equity was 10.93% (10.74% adjusted). The efficiency ratio improved to 52.6% from 55.5% in the previous quarter.

As shown in the following earnings highlights summary:

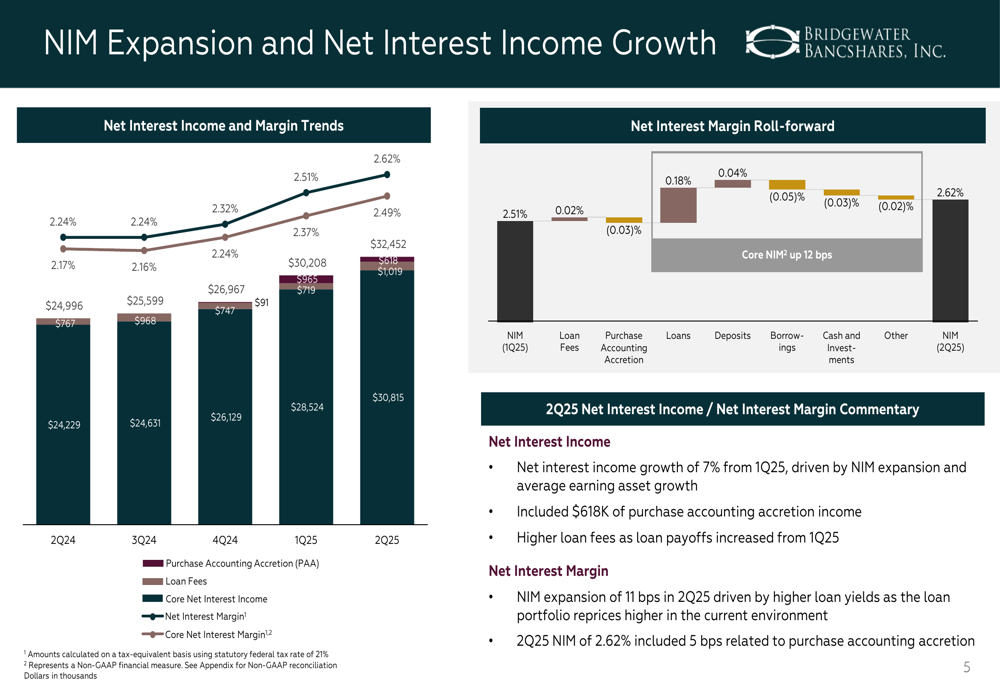

Net interest margin (NIM) expanded to 2.62%, up 11 basis points from Q1 2025, while core NIM increased to 2.49%, up 12 basis points quarter-over-quarter. This margin expansion contributed to a $2.2 million (7.4%) increase in net interest income compared to the previous quarter. Noninterest income also showed significant growth, increasing by $1.5 million or 74.5% from Q1 2025.

The following chart illustrates the bank’s NIM expansion and net interest income growth trajectory:

Balance sheet growth remained robust, with loan balances increasing by $126 million (12.5% annualized) and total deposit balances growing by $74 million (7.2% annualized) from the previous quarter. The loan-to-deposit ratio stood at 97.9%, up slightly from 96.6% at the end of March 2025.

Detailed Financial Analysis

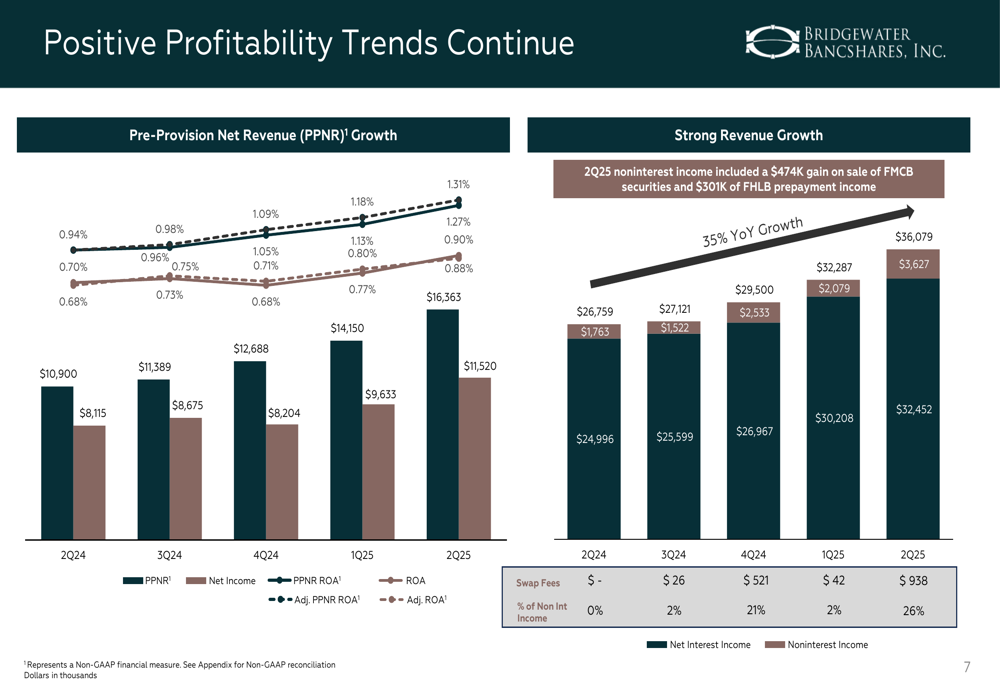

Bridgewater’s profitability metrics continued to improve in Q2 2025, with pre-provision net revenue (PPNR) showing strong growth. The bank’s revenue increased 35% year-over-year, driven by both net interest income growth and higher noninterest income.

The following chart demonstrates the positive profitability trends:

The bank’s efficiency ratio improved to 52.6% in Q2 2025, down from 55.5% in Q1 2025, reflecting strong revenue growth and well-controlled expenses. This improvement indicates the bank’s ability to generate more revenue while maintaining disciplined cost management.

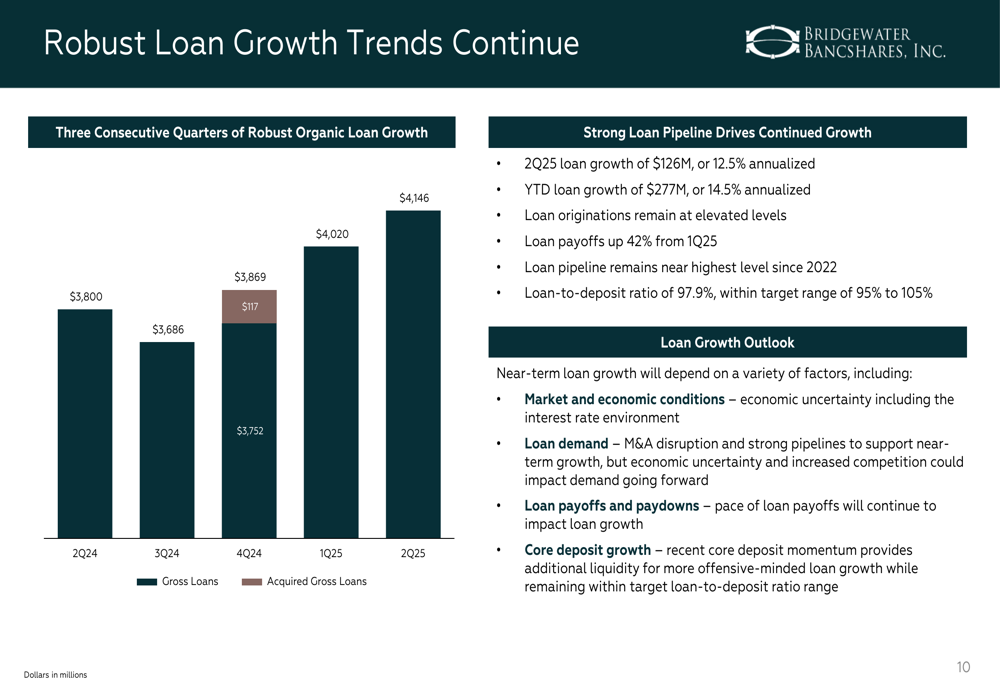

Loan growth remained strong for the third consecutive quarter, with gross loans increasing to $4.15 billion, up from $3.75 billion in Q2 2024. New loan originations reached $275 million in Q2 2025, compared to $141 million in the same quarter last year.

The following chart shows the consistent loan growth trend:

Bridgewater’s loan portfolio remains well-diversified, with multifamily loans representing 37.5% of the total portfolio, followed by commercial real estate (non-owner occupied) at 27.4%. The bank emphasized its expertise in multifamily lending in the Twin Cities market, noting strong performance metrics including a weighted average loan-to-value ratio of 67% and minimal historical charge-offs.

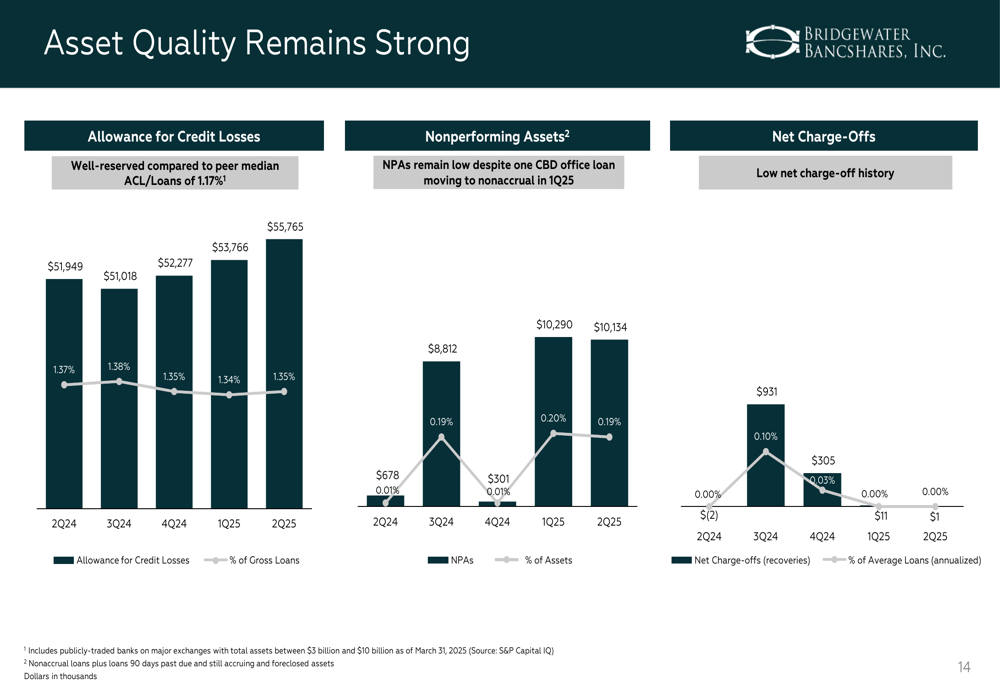

Asset quality metrics remained strong, with nonperforming assets to total assets at 0.19%, slightly improved from 0.20% in Q1 2025. The allowance for credit losses to total loans stood at 1.35%, up 1 basis point from March 31, 2025, and annualized net charge-offs to average loans remained at 0.00%.

The following chart illustrates the bank’s strong asset quality:

Strategic Initiatives & Outlook

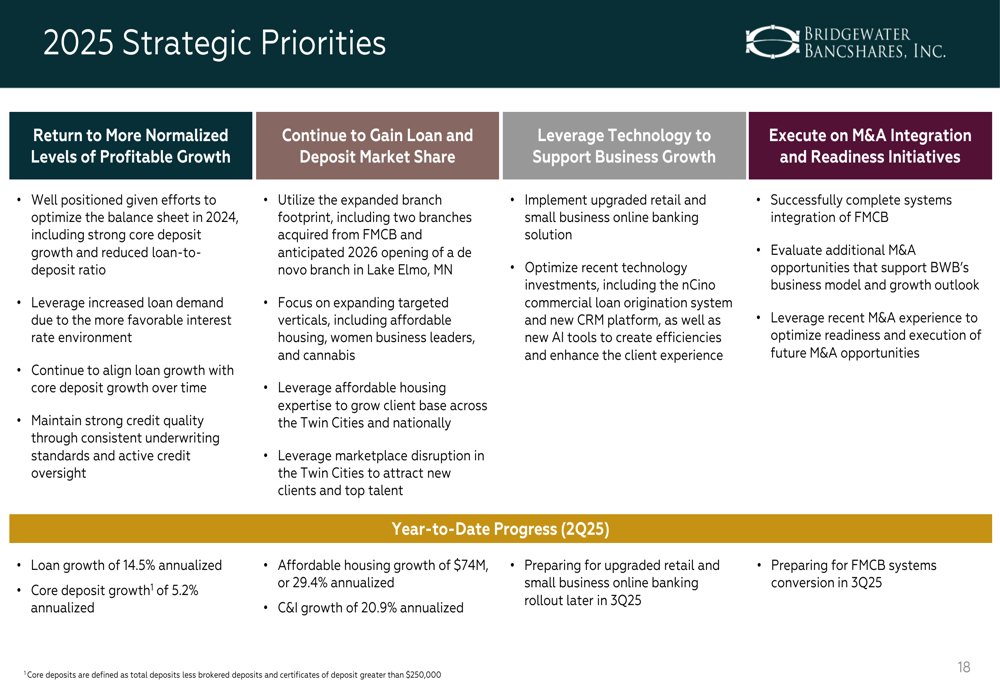

Bridgewater outlined its strategic priorities for 2025, focusing on returning to more normalized levels of profitable growth, gaining loan and deposit market share, leveraging technology to support business growth, and executing on M&A integration and readiness initiatives.

The bank’s strategic priorities are summarized in the following slide:

For the near term, Bridgewater expects mid-to-high single-digit loan growth and mid-single-digit deposit growth for the full year 2025. The bank anticipates NIM will continue to expand modestly in the second half of 2025, with the pace dependent on the timing and magnitude of Federal Reserve rate cuts.

Bridgewater is well-positioned to benefit in a rates-down environment, with a balanced mix of fixed-rate, variable-rate, and adjustable-rate loans. The bank also maintains ample liquidity and borrowing capacity, with 1.8x coverage of uninsured deposits.

Capital Management & Shareholder Value

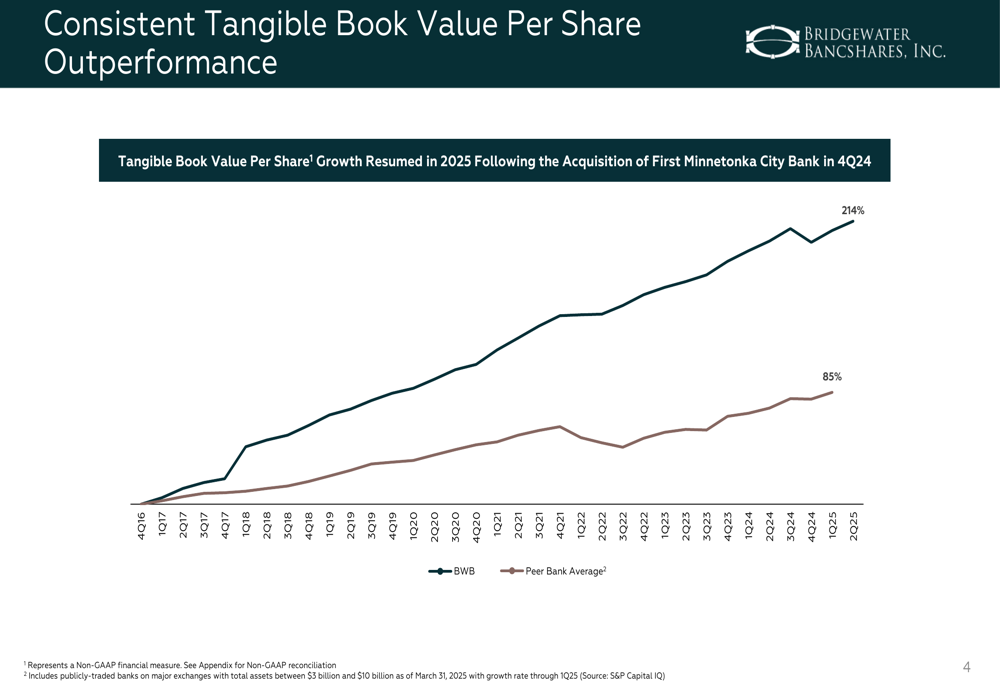

Bridgewater’s tangible book value per share reached $14.21 in Q2 2025, representing an annualized growth rate of 9.2% from Q1 2025. The bank’s tangible book value growth has significantly outperformed its peers, with a 214% increase compared to the peer average of 85%.

The following chart demonstrates this outperformance:

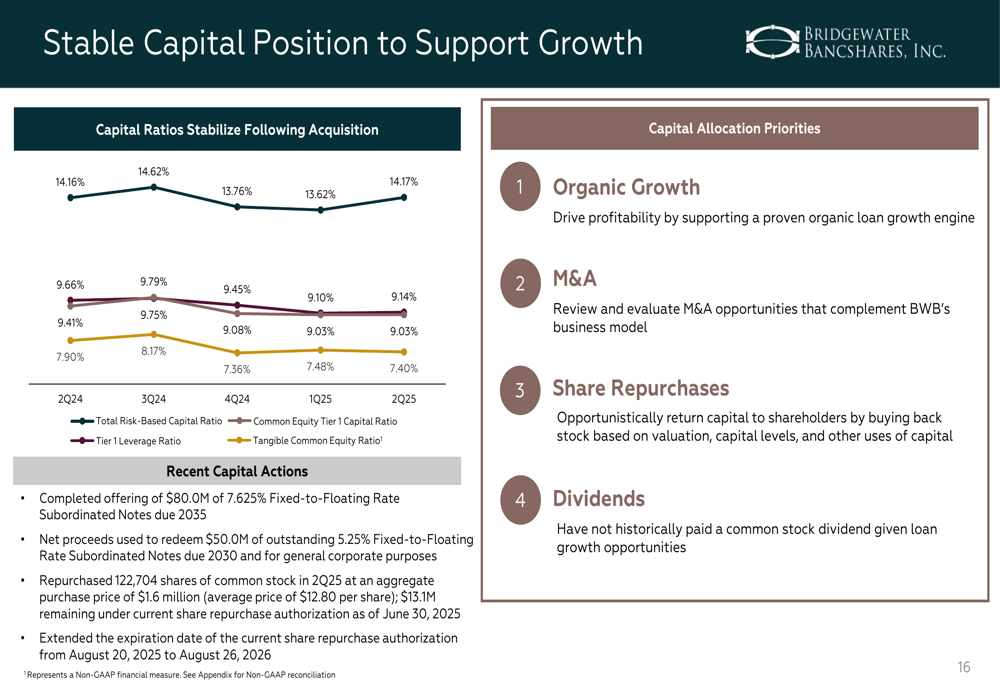

The bank’s Common Equity Tier 1 ratio remained stable at 9.03%, in line with the previous quarter. During Q2 2025, Bridgewater repurchased 122,704 shares of common stock at an average price of $12.80 per share, totaling $1.6 million. The bank also completed an offering of $80.0 million of 7.625% Fixed-to-Floating Rate Subordinated Notes due 2035, enhancing its capital position.

Bridgewater’s capital allocation priorities include supporting organic growth, pursuing strategic M&A opportunities, repurchasing shares, and potentially initiating dividends in the future. The bank’s stable capital position provides flexibility to execute on these priorities while maintaining regulatory capital requirements.

The bank’s capital position is illustrated in the following chart:

Bridgewater Bancshares continues to demonstrate strong financial performance, with expanding margins, robust loan growth, and improved efficiency. The bank’s strategic focus on gaining market share in the Twin Cities, particularly in multifamily lending, positions it well for continued growth in a changing interest rate environment. With strong asset quality and a stable capital position, Bridgewater appears well-equipped to execute on its strategic priorities for the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.