Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

Bristol Myers Squibb (NYSE:BMY) presented its Q1 2025 financial results on April 24, 2025, highlighting the company’s ongoing portfolio transformation and improved financial outlook. The pharmaceutical giant reported mixed results but demonstrated progress in its strategic shift from legacy products to its growth portfolio, prompting management to raise full-year guidance.

The presentation comes amid challenging market conditions for pharmaceutical companies, with BMY’s stock currently trading around $45, well below its 52-week high of $63.33. Despite the earnings beat in subsequent quarters, the stock has faced downward pressure, reflecting broader market concerns about the pharmaceutical sector.

Quarterly Performance Highlights

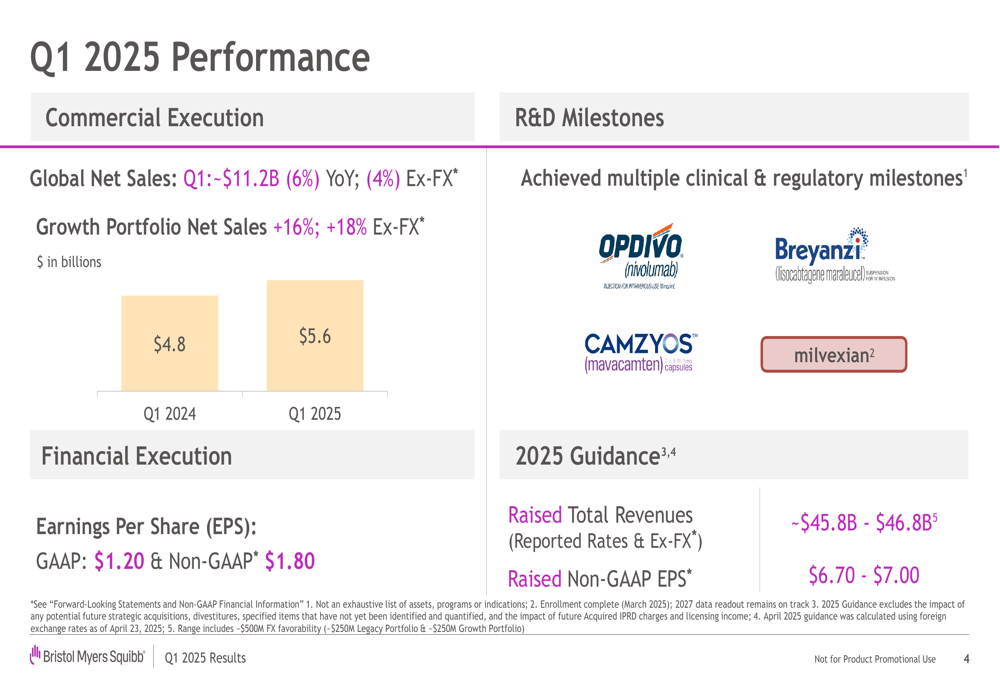

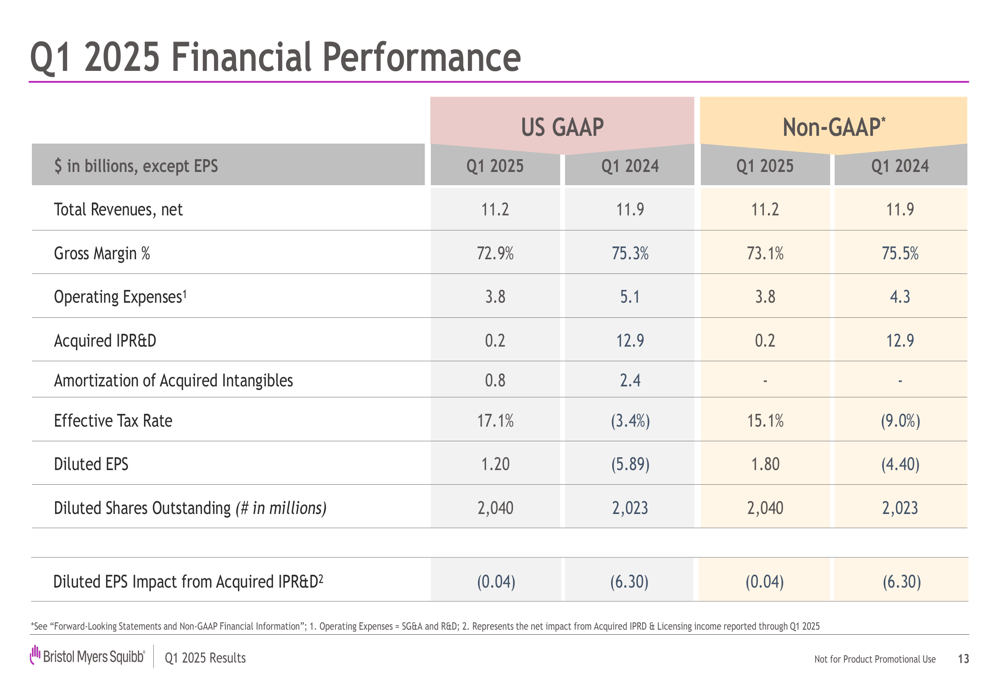

Bristol Myers Squibb reported global net sales of approximately $11.2 billion for Q1 2025, representing a 6% year-over-year increase, though this translated to a 4% decline when excluding foreign exchange impacts. The company posted GAAP earnings per share of $1.20 and non-GAAP EPS of $1.80.

As shown in the following comprehensive performance summary:

The company achieved multiple clinical and regulatory milestones during the quarter, particularly with key products like Opdivo, Breyanzi, Camzyos, and Milvexian. These achievements, combined with the financial performance, gave management confidence to raise the company’s 2025 guidance.

Portfolio Transformation

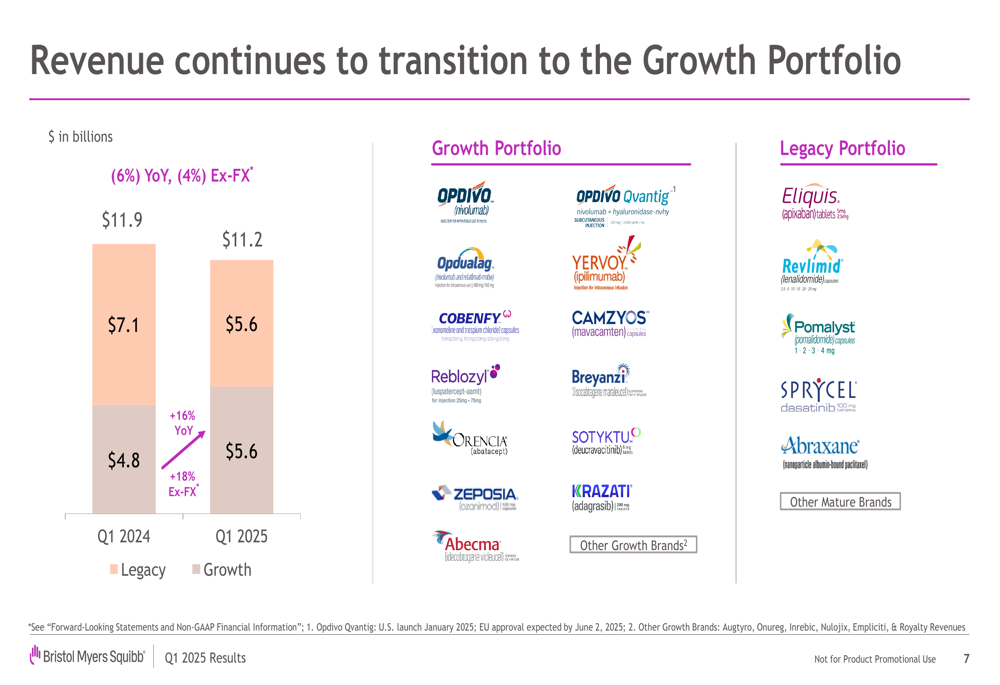

A significant milestone in Bristol Myers Squibb’s strategic evolution was reached in Q1 2025, with the growth portfolio now contributing equally to revenue as the legacy portfolio. Both segments generated $5.6 billion in the quarter, though they showed dramatically different trajectories.

The growth portfolio, which includes brands like Opdivo, Reblozyl, Camzyos, and Breyanzi, increased 16% year-over-year (18% excluding foreign exchange), while the legacy portfolio continued its expected decline. This transformation is clearly illustrated in the following chart:

Within the growth portfolio, several products delivered exceptional performance. Breyanzi led with 146% year-over-year growth, positioning itself as the "#1 CAR T in the U.S. with the best-in-class CD19 CAR T profile," according to the company. Camzyos, the company’s treatment for obstructive hypertrophic cardiomyopathy (oHCM), grew 89% year-over-year, with approximately 11,000 patients on commercial drug, including about 1,400 added in Q1 2025.

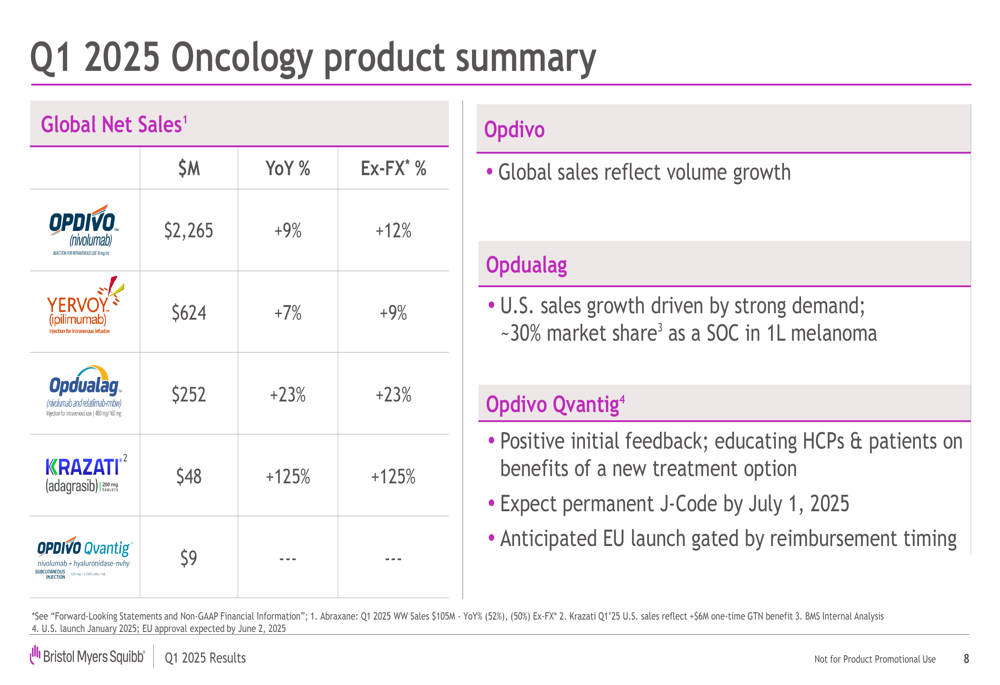

The oncology segment showed mixed results, with Opdivo declining 9% year-over-year but showing 12% growth excluding foreign exchange impacts. Opdualag achieved 23% growth and now holds approximately 30% market share as a standard of care in first-line melanoma:

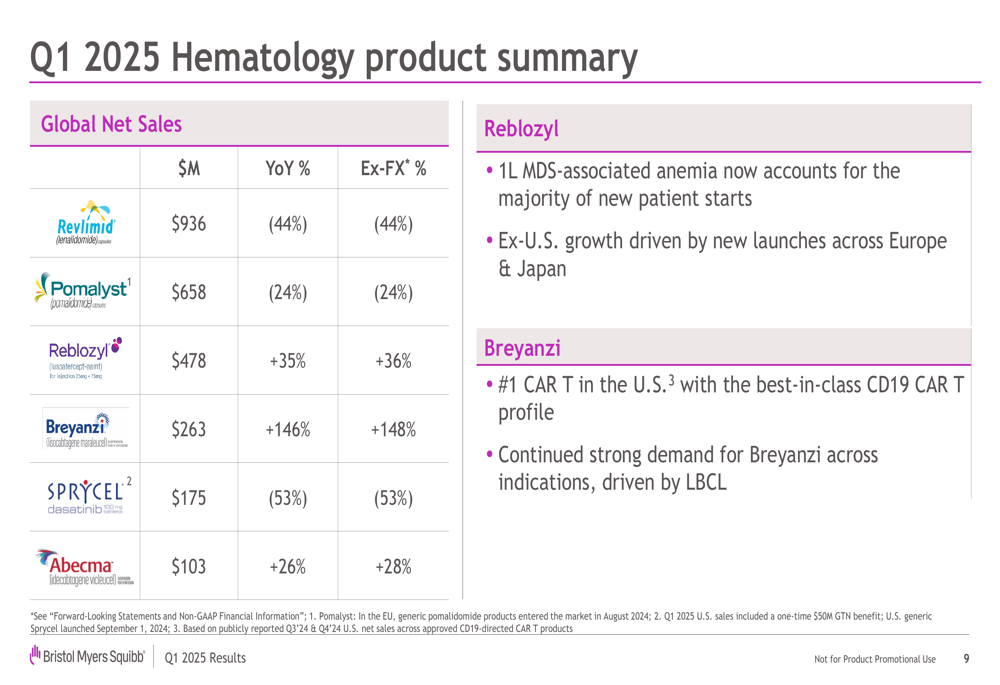

In hematology, Reblozyl grew 35% year-over-year, with first-line MDS-associated anemia now accounting for the majority of new patient starts. However, legacy products like Revlimid (-44%) and Pomalyst (-24%) continued their expected declines:

Financial Analysis

Bristol Myers Squibb’s Q1 2025 financial performance revealed some challenges despite the overall positive narrative. Total (EPA:TTEF) revenues declined from $11.9 billion in Q1 2024 to $11.2 billion in Q1 2025, while gross margin percentage decreased from 75.3% to 72.9%.

The company’s financial details show significant changes in several key metrics:

Operating expenses decreased substantially from $5.1 billion to $3.8 billion, while acquired IPR&D dropped dramatically from $12.9 billion to $0.2 billion. The effective tax rate shifted from -3.4% to 17.1%, and diluted EPS improved from -$5.89 to $1.20.

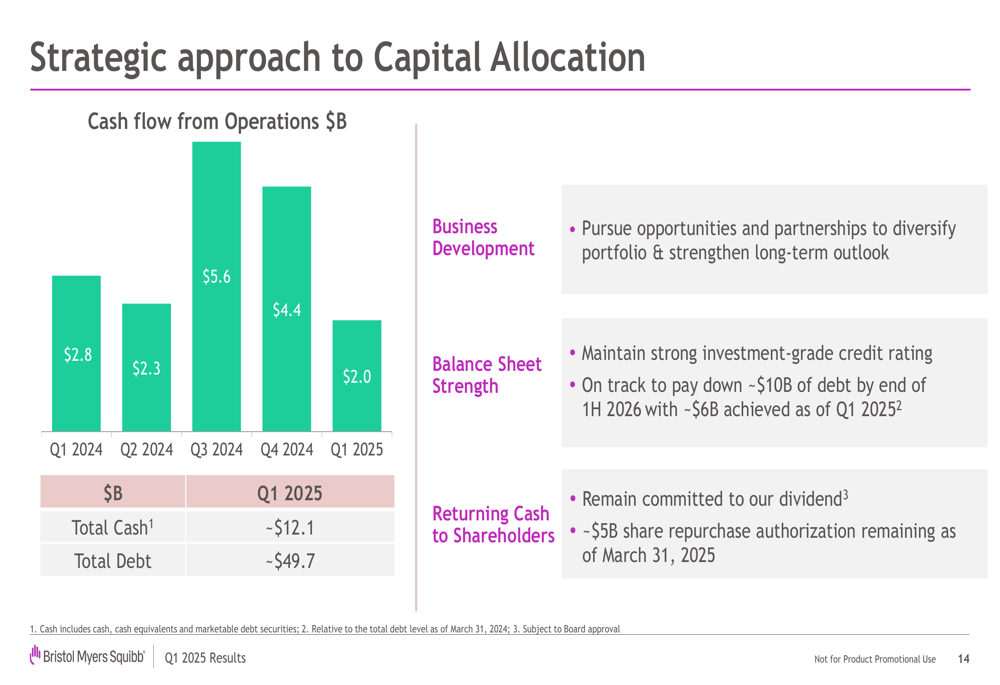

Cash flow from operations declined to $2.0 billion in Q1 2025, down from $4.4 billion in Q4 2024. The company’s capital allocation strategy focuses on three key areas: business development, balance sheet strength, and returning cash to shareholders:

Bristol Myers Squibb reported progress on its debt reduction plan, having achieved approximately $6 billion of its $10 billion debt reduction target (to be completed by the end of the first half of 2026). The company also reaffirmed its commitment to its dividend and noted approximately $5 billion in remaining share repurchase authorization as of March 31, 2025.

Revised Guidance & Strategic Outlook

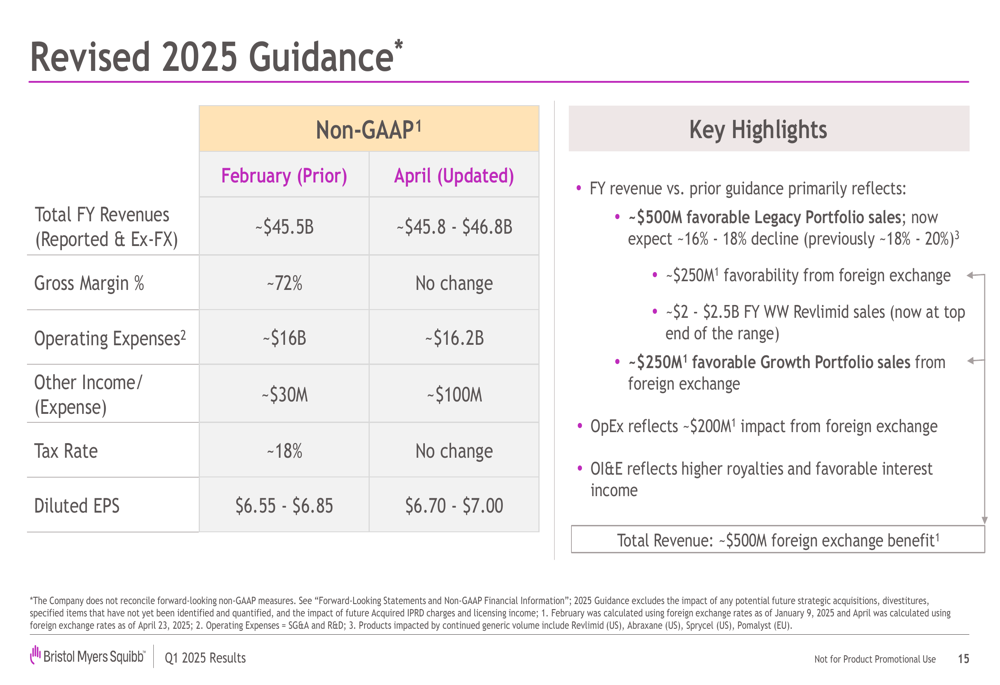

Based on Q1 performance, Bristol Myers Squibb raised its 2025 financial guidance. The company increased its total revenue projection from approximately $45.5 billion to a range of $45.8-$46.8 billion, and raised its diluted EPS guidance from $6.55-$6.85 to $6.70-$7.00:

The revised guidance primarily reflects approximately $500 million in favorable legacy portfolio sales, with the expected decline now projected at 16-18% (improved from the previous 18-20% decline forecast). The company also cited approximately $250 million in favorability from foreign exchange and now expects Revlimid sales to be at the top end of the $2-2.5 billion range.

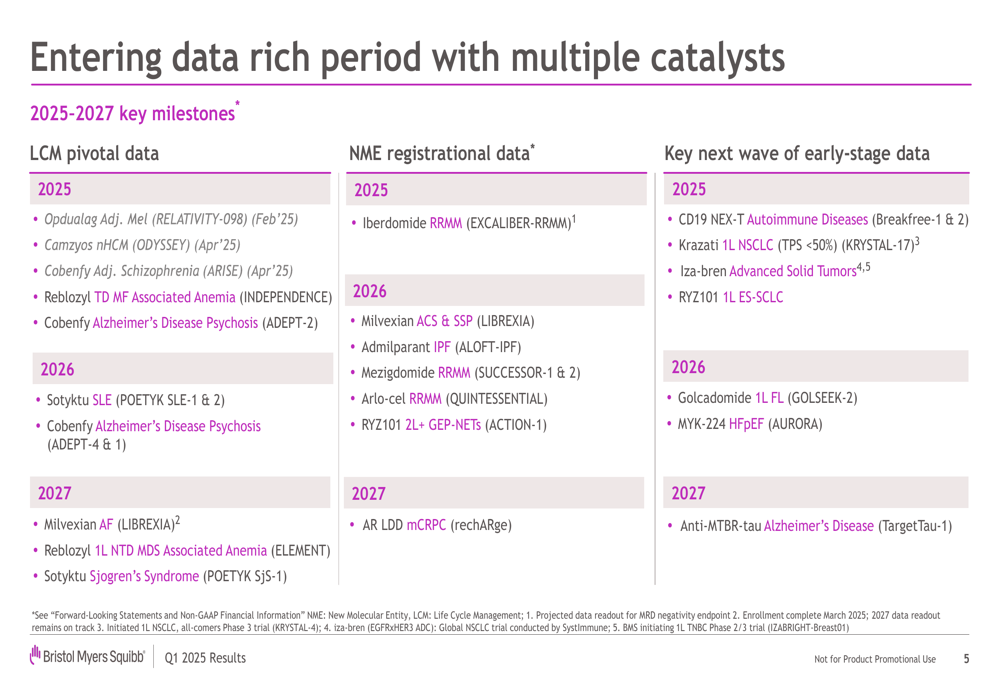

Looking ahead, Bristol Myers Squibb outlined an ambitious pipeline of clinical developments for 2025-2027, including numerous pivotal data readouts and potential regulatory approvals:

This robust pipeline underscores the company’s long-term growth strategy beyond its current portfolio transition. The upcoming milestones span multiple therapeutic areas, including oncology, immunology, hematology, and neuroscience, positioning Bristol Myers Squibb for potential future growth if these clinical programs prove successful.

Subsequent quarterly results have shown that Bristol Myers Squibb has continued to build on this momentum, with Q2 2025 showing revenue of $12.27 billion, exceeding analyst expectations. The company further raised its full-year revenue guidance to $46.5-$47.5 billion, suggesting continued confidence in its strategic direction despite ongoing market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.