Stock market today: S&P 500 closer lower on fresh economic concerns

Introduction & Market Context

Bruker Corporation (NASDAQ:BRKR) presented its Q2 2025 earnings results on August 4, 2025, revealing significant profitability challenges despite relatively stable reported revenue. The scientific instruments manufacturer’s stock fell 3.11% in premarket trading to $36.81, reflecting investor concerns about deteriorating performance metrics and reduced full-year guidance.

The company is navigating multiple headwinds including disruptions in U.S. academic funding, delays in China stimulus, postponed capital expenditures in drug discovery and industrial research, and tariff uncertainties. These challenges represent a marked deterioration from Q1 2025, when Bruker reported 11% revenue growth and exceeded analyst expectations.

Quarterly Performance Highlights

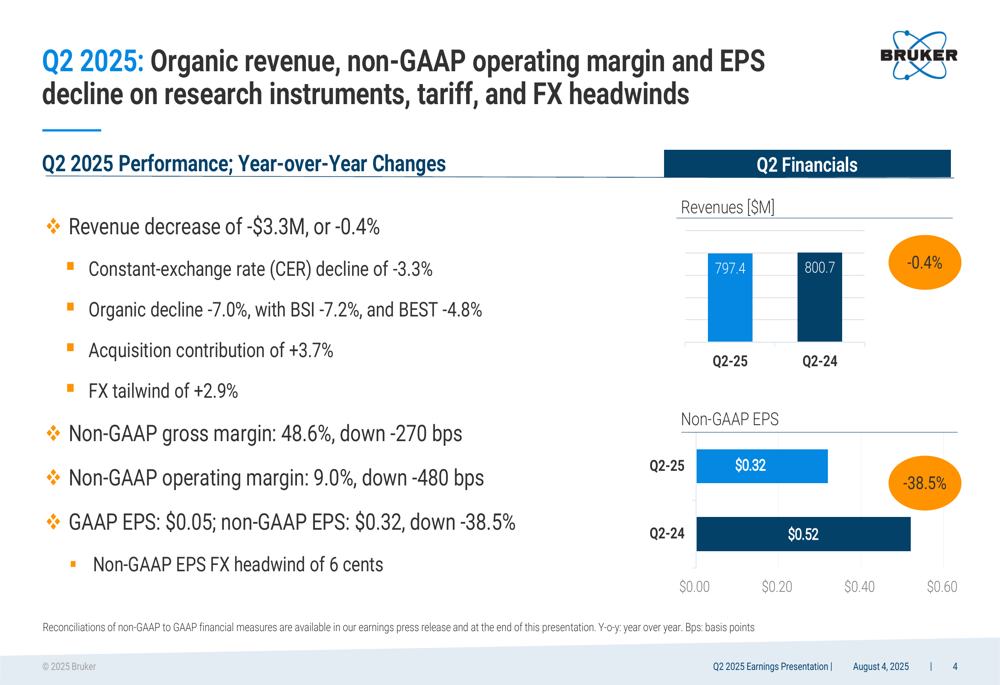

Bruker’s Q2 2025 revenue decreased slightly by $3.3 million or 0.4% year-over-year to $797.4 million. However, the constant exchange rate (CER) decline was more pronounced at 3.3%, with organic revenue falling 7.0%. Acquisition contributions of 3.7% and favorable currency effects of 2.9% partially offset the organic decline.

As shown in the following quarterly performance overview:

Profitability metrics deteriorated significantly, with non-GAAP gross margin dropping 270 basis points to 48.6% and non-GAAP operating margin falling 480 basis points to 9.0%. Non-GAAP earnings per share declined 38.5% to $0.32 from $0.52 in Q2 2024, with foreign exchange headwinds accounting for approximately 6 cents of the decline.

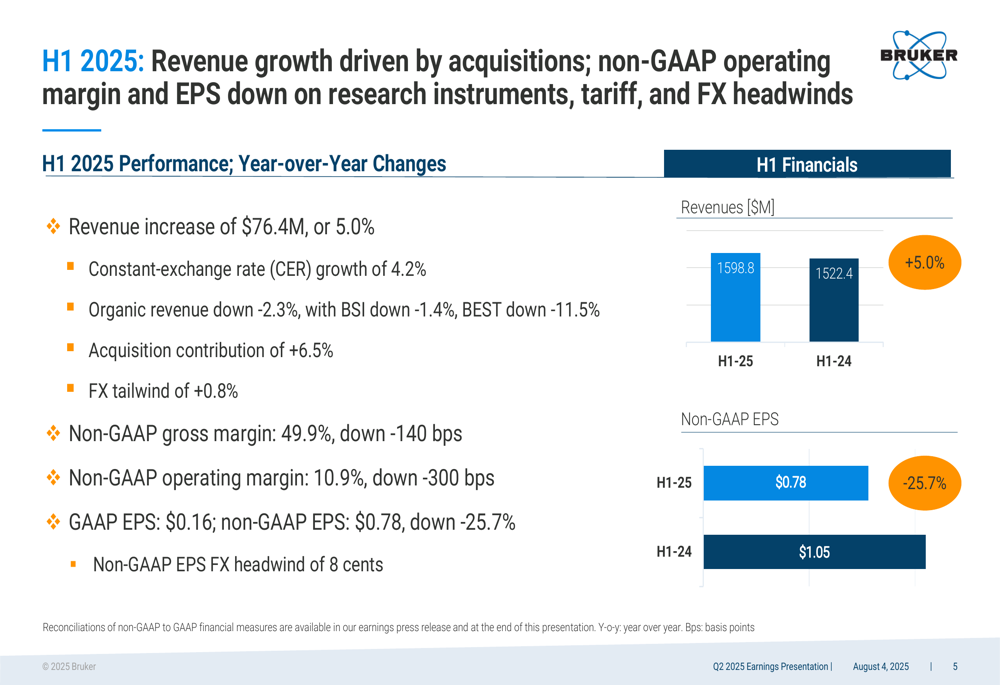

First-half 2025 results showed more favorable revenue trends but similar profitability challenges:

For H1 2025, Bruker reported revenue growth of 5.0% to $1.6 billion, though organic revenue still declined by 2.3%. Acquisitions contributed 6.5% to growth, while currency effects added 0.8%. Non-GAAP EPS for the first half fell 25.7% to $0.78 from $1.05 in the prior year period.

Detailed Financial Analysis

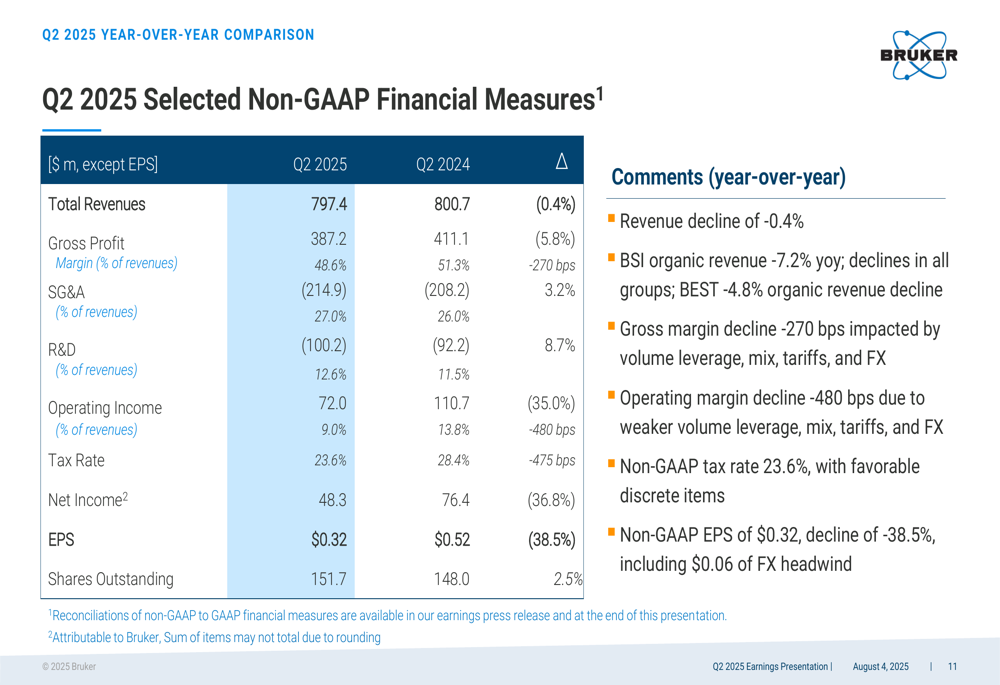

A closer examination of Bruker’s Q2 2025 financial metrics reveals the extent of the profitability challenges:

The financial data shows significant increases in both SG&A expenses (up 3.2%) and R&D expenses (up 8.7%), contributing to a 35.0% decline in operating income to $72.0 million. Despite a lower tax rate of 23.6% compared to 28.4% in Q2 2024, net income still fell 36.8% to $48.3 million.

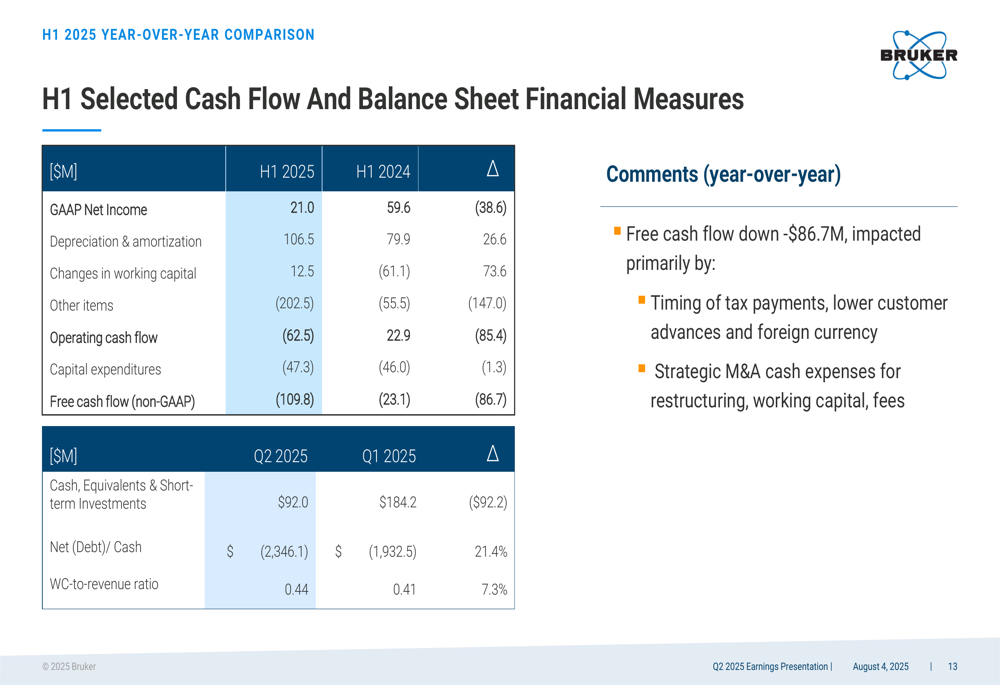

Cash flow and balance sheet metrics also deteriorated in the first half of 2025:

Free cash flow was negative $109.8 million for H1 2025, compared to negative $23.1 million in H1 2024, representing a worsening of $86.7 million. The company attributed this decline partly to strategic M&A cash expenses. Net debt increased to $2.35 billion, up 21.4% from the previous quarter.

Strategic Initiatives

In response to these challenges, Bruker outlined several strategic initiatives aimed at navigating the current headwinds:

The company announced plans for $100-$120 million in annualized cost reductions to improve margins and profitability, with a significant portion of these savings expected to materialize in fiscal year 2026. Management emphasized continued investment in innovation to reaccelerate growth in the post-genomic era.

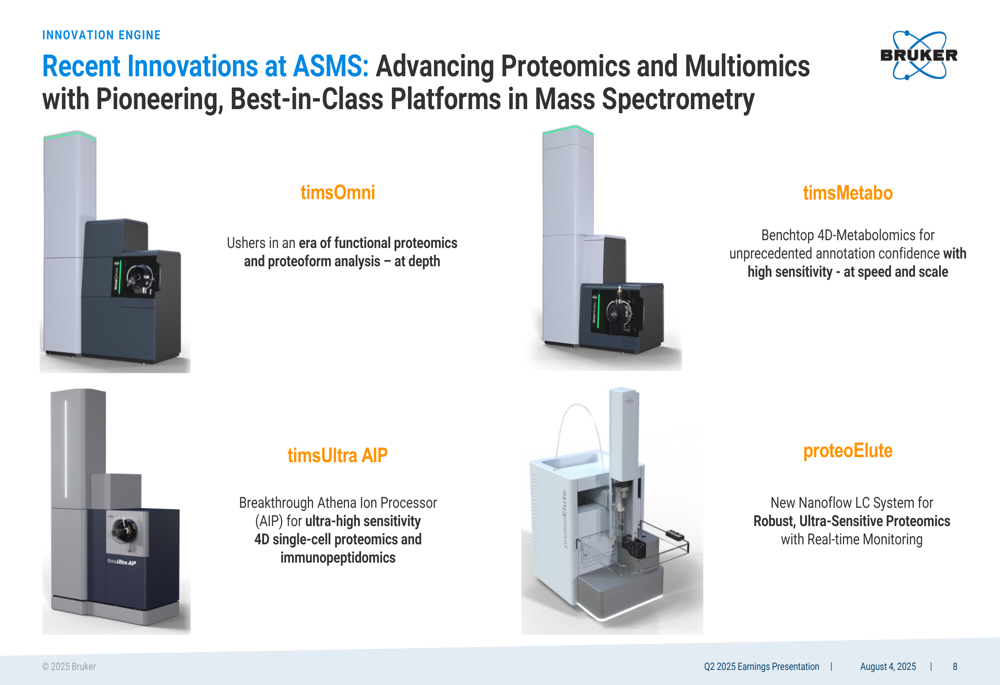

At the American Society for Mass Spectrometry conference, Bruker showcased several new product innovations in proteomics and multiomics:

These innovations include the timsOmni platform for functional proteomics, timsUltra AIP for single-cell proteomics, timsMetabo for metabolomics, and proteoElute for ultra-sensitive proteomics. The company is positioning these technologies to drive future growth once market conditions improve.

Forward-Looking Statements

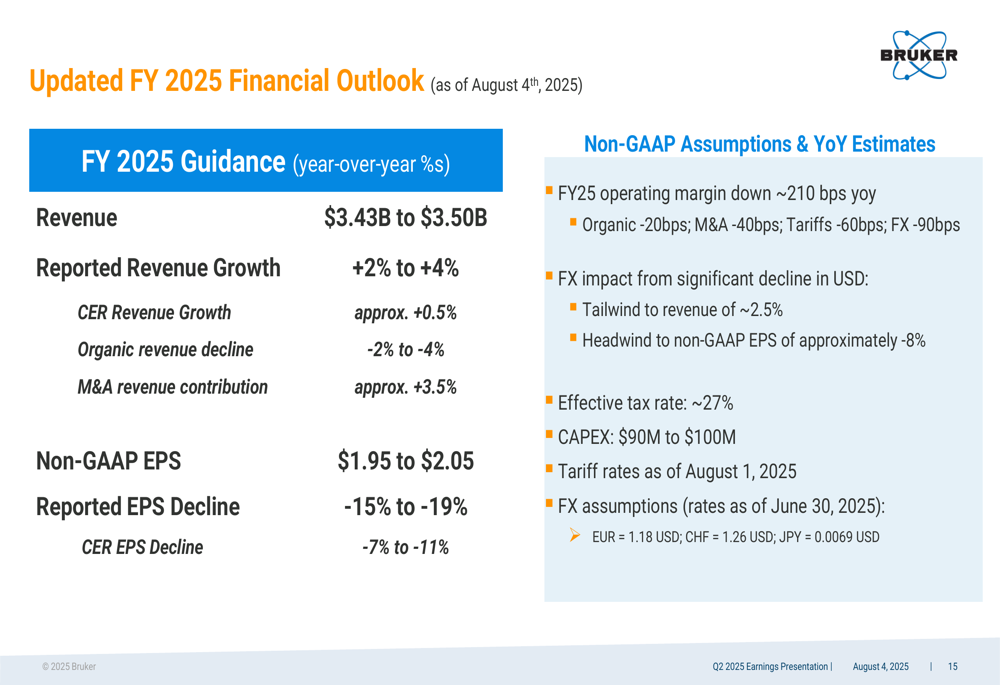

Bruker significantly revised its full-year 2025 guidance downward:

The updated outlook projects revenue of $3.43-$3.50 billion, representing 2-4% year-over-year growth, and non-GAAP EPS of $1.95-$2.05, reflecting a 15-19% year-over-year decline. This represents a substantial reduction from the guidance provided after Q1 2025, which projected revenue of $3.48-$3.55 billion and non-GAAP EPS of $2.40-$2.48.

The revised guidance incorporates assumptions about continued challenges in academic funding, particularly in the U.S., ongoing uncertainty in China, and the impact of tariffs. The company expects these headwinds to persist through the remainder of 2025, with potential improvement in 2026 as cost reduction measures take full effect.

Segment Performance

Bruker’s performance varied significantly across its business segments in the first half of 2025:

The BIOSPIN Group, which specializes in NMR and preclinical imaging, reported flat CER revenue with growth in NMR and lab automation offset by weakness in biopharma due to market uncertainty.

The CALID Group achieved low-teens percentage CER revenue growth, driven primarily by strong performance in microbiology and infection diagnostics, particularly from the ELITech MDx acquisition. However, life science mass spectrometry showed softness.

The NANO Group reported low single-digit percentage CER revenue growth, led by spatial biology (particularly the Nanostring acquisition), while experiencing softness in X-Ray and NanoAnalysis tools. Performance was strong in Japan and North America but weak in China.

The BEST (NYSE:BEST) segment (Bruker Energy & Supercon Technologies) saw CER revenue decline in the low teens percentage, affected by softness in demand for superconductors for clinical MRI and weaker research instruments performance.

As Bruker navigates through these challenging market conditions, management’s focus on cost reduction and continued innovation will be critical to restoring profitability and positioning the company for future growth when market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.