D-Wave Quantum falls nearly 3% as earnings miss overshadows revenue beat

Introduction & Market Context

Bumble Inc. (NASDAQ:BMBL) released its second-quarter 2025 earnings presentation on August 6, revealing a company prioritizing profitability over growth. The dating app operator reported declining revenue and user metrics but achieved substantial improvements in profitability margins through cost-cutting initiatives.

Following the earnings release, Bumble’s stock, which closed at $7.55, gained 3.44% in after-hours trading to reach $7.81. The stock has experienced significant volatility over the past year, trading between $3.55 and $9.22.

Quarterly Performance Highlights

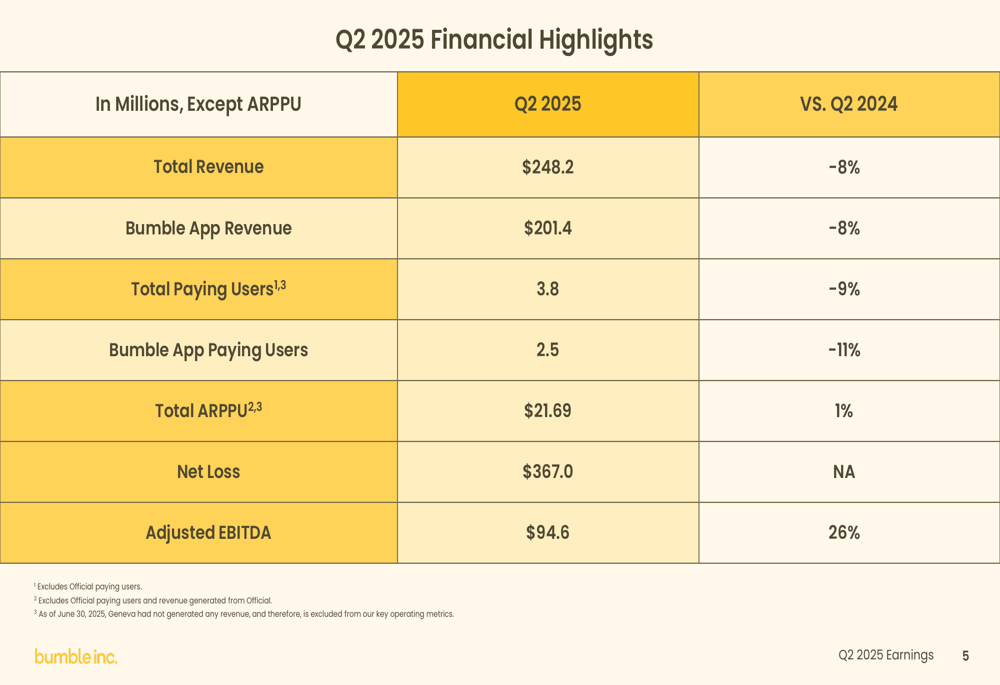

Bumble reported total revenue of $248.2 million for Q2 2025, representing an 8% year-over-year decline. The company’s flagship Bumble App generated $201.4 million in revenue, also down 8% compared to the same period last year. Despite these declines, the company posted a substantial 26% increase in Adjusted EBITDA, reaching $94.6 million with a 38.1% margin.

As shown in the following financial highlights chart:

The presentation revealed a 9% year-over-year decrease in total paying users to 3.8 million, with Bumble App paying users declining 11% to 2.5 million. However, the company managed to increase its Total (EPA:TTEF) Average Revenue Per Paying User (ARPPU) by 1% to $21.69, suggesting improved monetization of its remaining user base.

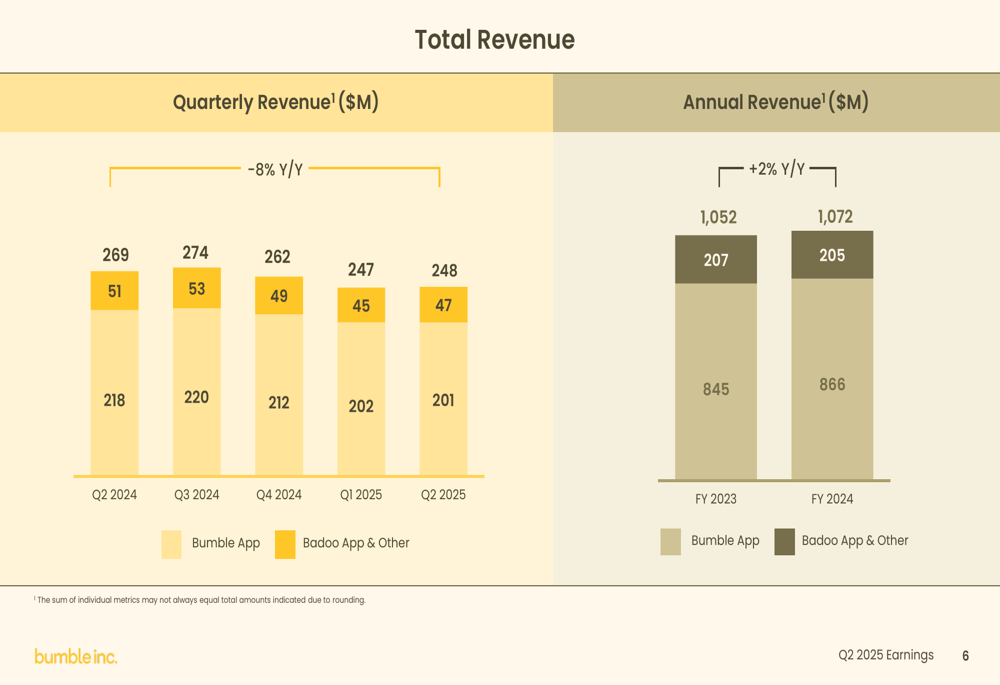

The quarterly revenue trend illustrates the consistent decline over recent quarters:

Detailed Financial Analysis

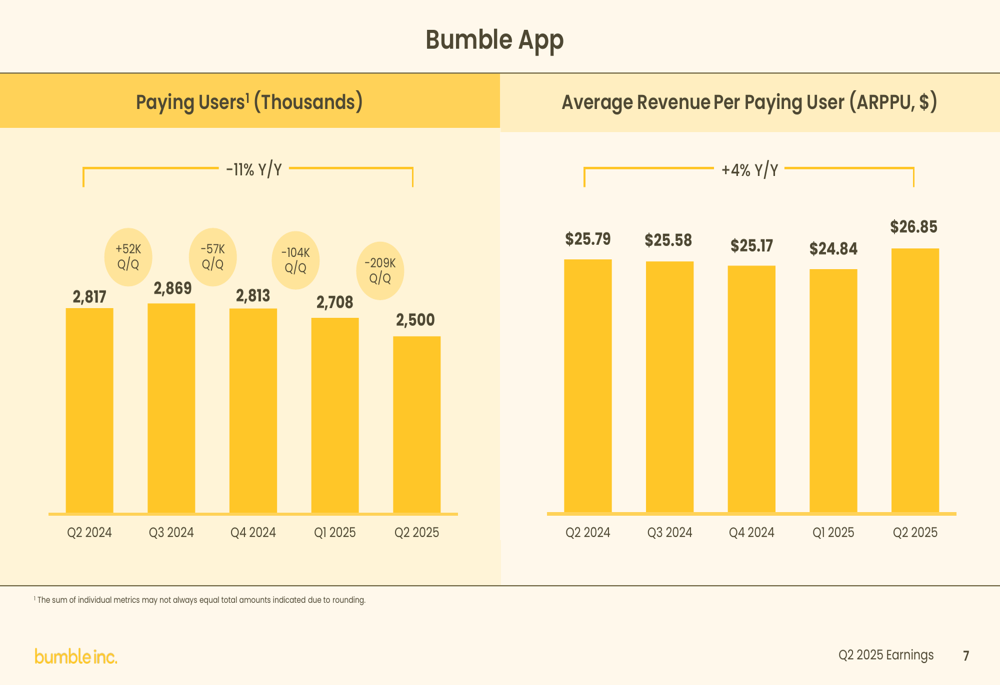

Bumble’s flagship app showed contrasting trends in user metrics and monetization. While paying users declined by 11% year-over-year to 2.5 million, the company successfully increased ARPPU by 4% to $26.85, partially offsetting the impact of user losses.

The following chart demonstrates this trend:

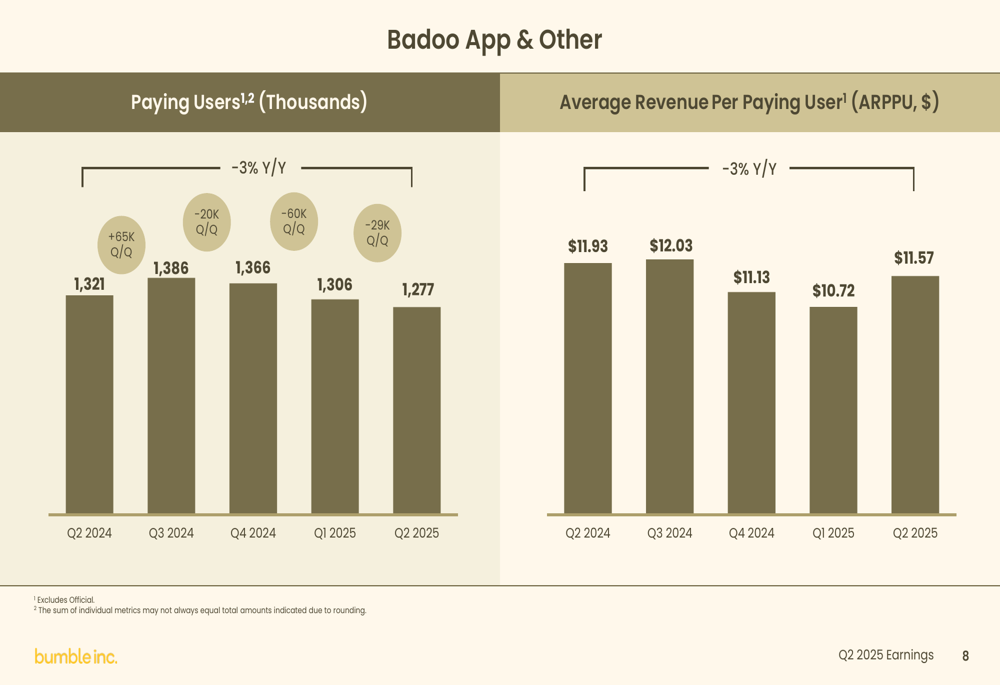

The company’s secondary offering, Badoo App & Other, experienced less severe user decline but also showed weaker monetization. Paying users decreased by 3% year-over-year to 1.28 million, while ARPPU also fell by 3% to $11.57.

This performance is illustrated in the following chart:

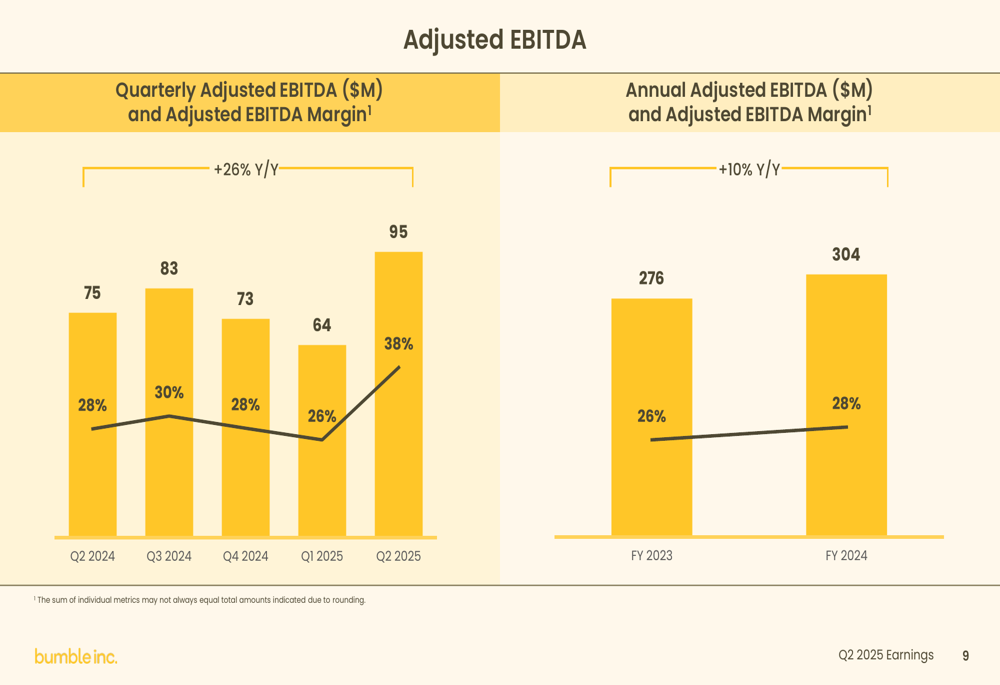

Despite the revenue challenges, Bumble achieved remarkable improvement in profitability. Adjusted EBITDA increased by 26% year-over-year to $94.6 million, with margin expanding to 38% from 28% in the same quarter last year. This suggests the company’s cost-cutting measures are yielding significant results.

The following chart shows the consistent improvement in Adjusted EBITDA:

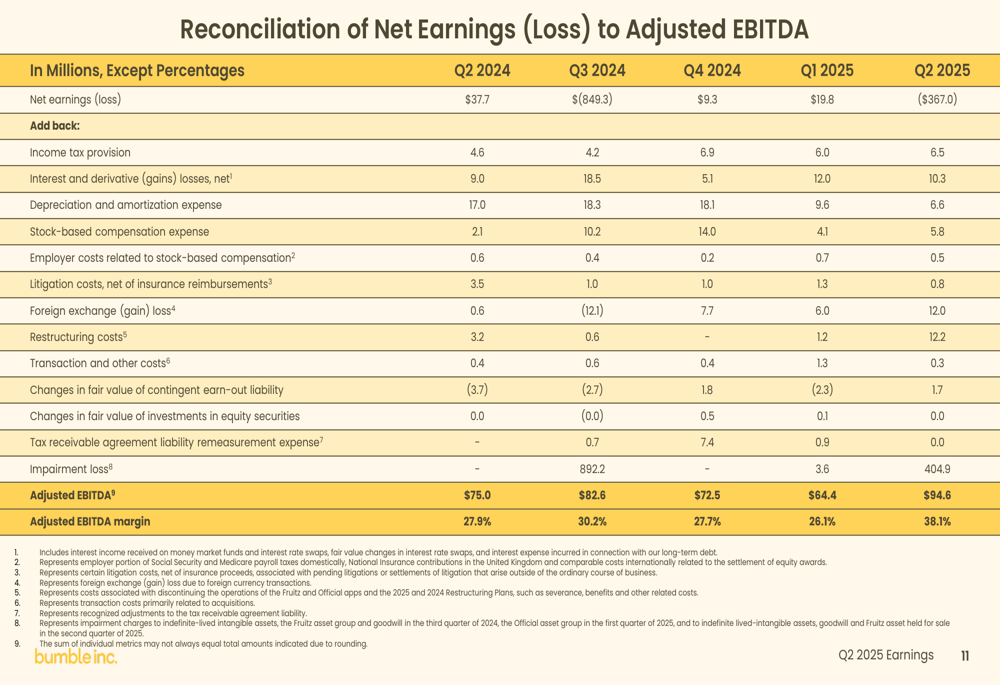

However, the company reported a substantial net loss of $367.0 million for the quarter, primarily due to a $404.9 million impairment charge. This non-cash charge likely reflects a reassessment of the company’s asset values in light of declining growth prospects.

Strategic Initiatives & Cost Management

Bumble’s presentation suggests a strategic pivot toward profitability over growth, consistent with statements made during the previous quarter’s earnings call. CEO Whitney Wolfe Herd had emphasized quality over quantity, stating "We use AI to make love more human" and "Quality is the key to enduring growth."

The significant improvement in Adjusted EBITDA margin to 38.1% indicates successful implementation of cost-saving measures and organizational efficiency initiatives. This represents a substantial improvement from the 26% margin reported in Q1 2025.

The reconciliation of net loss to Adjusted EBITDA reveals the extent of the impairment charge and other adjustments:

Forward Guidance

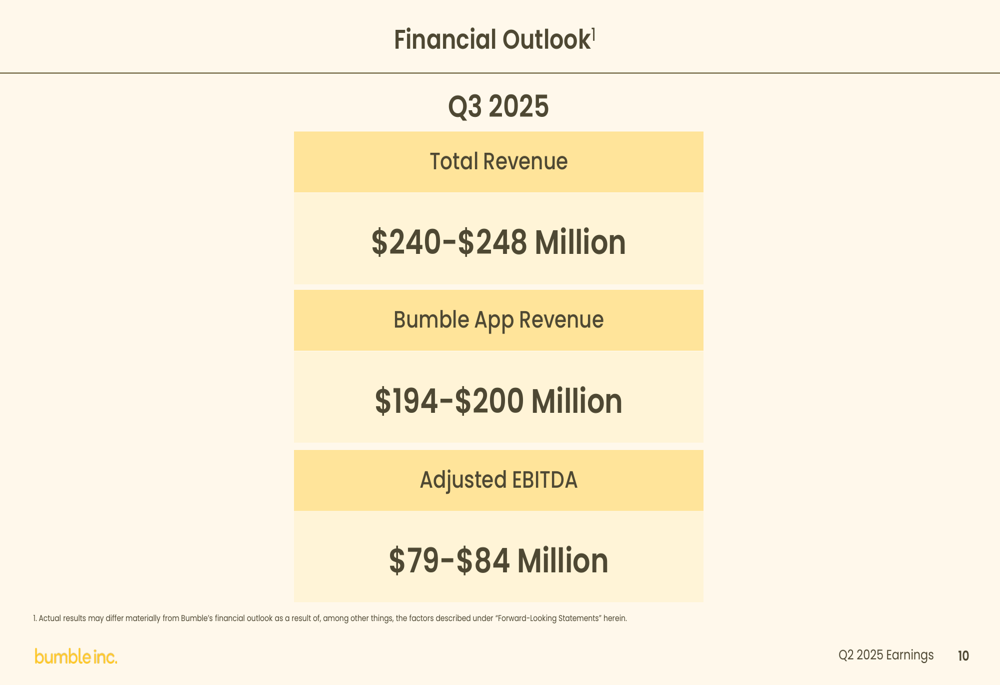

For the third quarter of 2025, Bumble projects total revenue between $240-248 million and Bumble App revenue between $194-200 million. This guidance suggests continued year-over-year revenue decline but relative stability compared to Q2 results.

The company expects Adjusted EBITDA between $79-84 million for Q3, representing a potential sequential decline from Q2’s $94.6 million but likely maintaining strong margins.

As shown in the outlook slide:

This guidance aligns with the company’s apparent strategy of managing for profitability rather than pursuing growth at all costs. The projected Q3 revenue range of $240-248 million would represent a slight sequential decline from Q2’s $248.2 million, suggesting the company does not anticipate an immediate reversal of current trends.

While Bumble continues to face challenges in growing its user base and revenue, its ability to significantly improve profitability metrics demonstrates effective cost management. Investors will be watching closely to see if the company can stabilize its user numbers while maintaining the improved profitability margins achieved in recent quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.