S&P 500 rises as health care, tech gain to overshadow Fed independence concerns

Introduction & Market Context

Caesars Entertainment (NASDAQ:CZR) released its Q1 2025 investor presentation on April 29, revealing mixed financial results with digital operations emerging as a bright spot. Despite missing analyst expectations with an EPS of -$0.54 (versus forecasted -$0.17) and revenue of $2.79 billion (below the anticipated $2.82 billion), the company’s stock rose 1.89% in aftermarket trading, closing at $28.52.

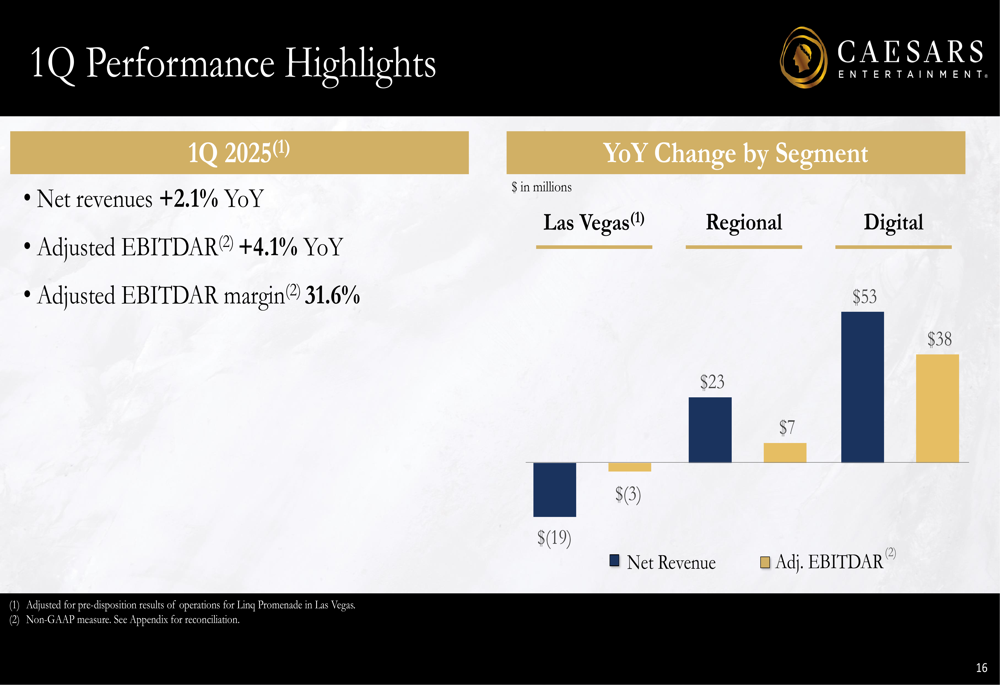

The presentation highlighted a 2.1% year-over-year increase in net revenues and a 4.1% growth in Adjusted EBITDAR, reaching $884 million for the quarter. While Las Vegas operations remained flat compared to the previous year, the digital segment demonstrated remarkable growth, helping to offset challenges in other areas.

Quarterly Performance Highlights

Caesars reported overall net revenue growth of 2.1% year-over-year for Q1 2025, with segment performance varying significantly. The company achieved an Adjusted EBITDAR margin of 31.6%, demonstrating stable operational efficiency despite mixed results across business units.

As shown in the following performance breakdown by segment, Las Vegas properties experienced a slight decline in revenue while Regional properties and Digital operations showed positive growth:

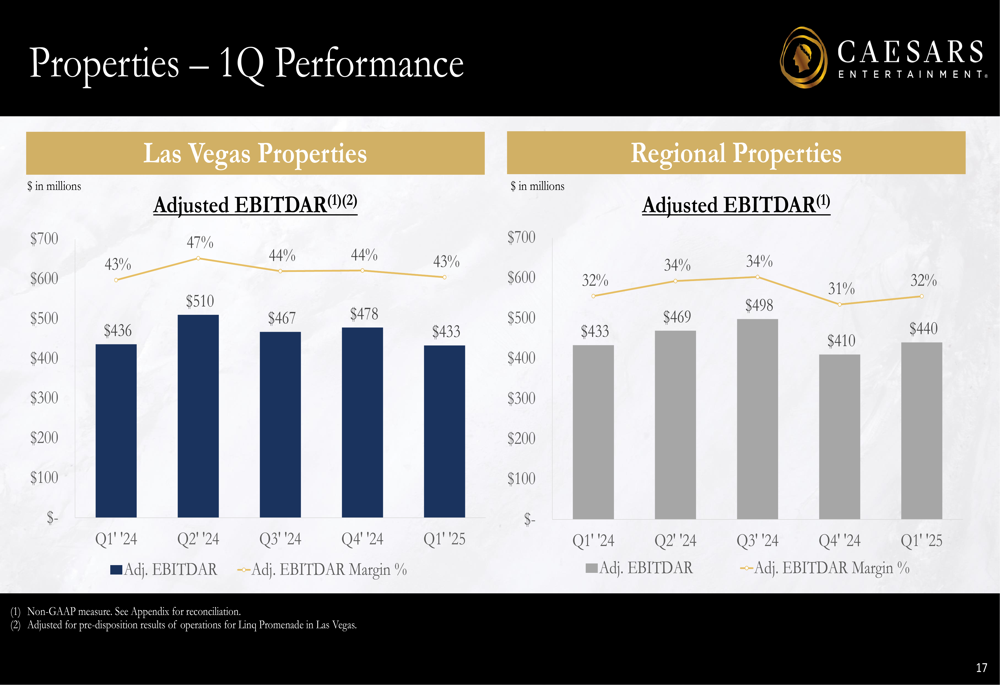

Las Vegas properties generated $433 million in Adjusted EBITDAR for Q1 2025, essentially flat compared to the $436 million reported in Q1 2024. Regional properties performed slightly better with $440 million in Adjusted EBITDAR, representing a $7 million increase year-over-year. The quarterly performance trends for both segments over the past year show relatively consistent results:

Digital Growth Strategy

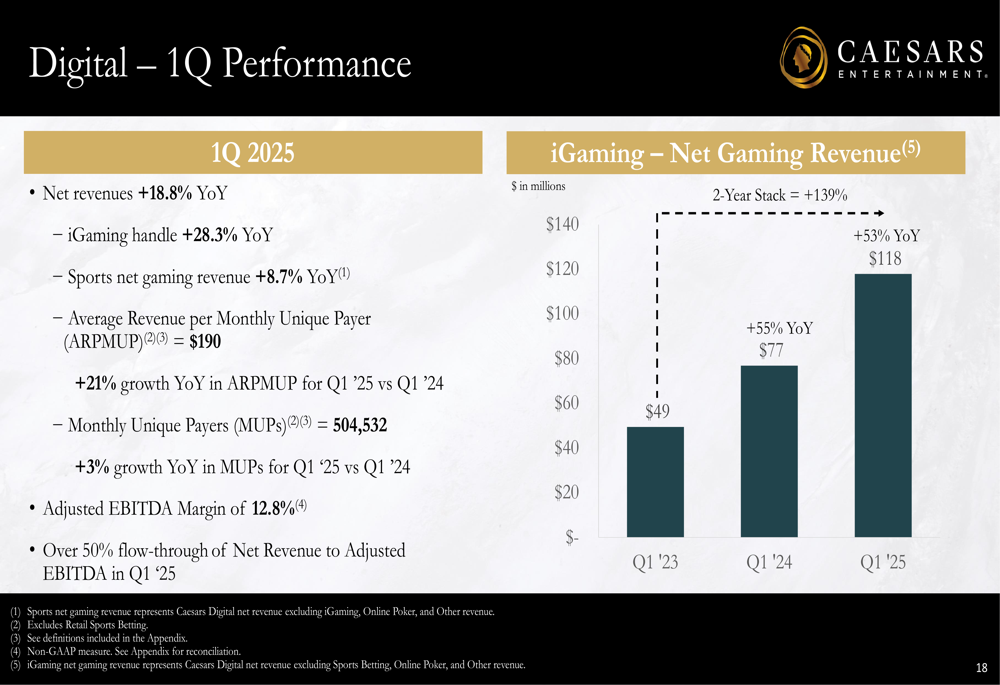

The standout performer in Caesars’ portfolio was undoubtedly its digital segment, which demonstrated impressive growth across multiple metrics. Digital net revenues increased by 18.8% year-over-year to $335 million in Q1 2025, while Adjusted EBITDA surged by $38 million compared to the same period last year.

The digital segment’s performance is illustrated in the following detailed breakdown:

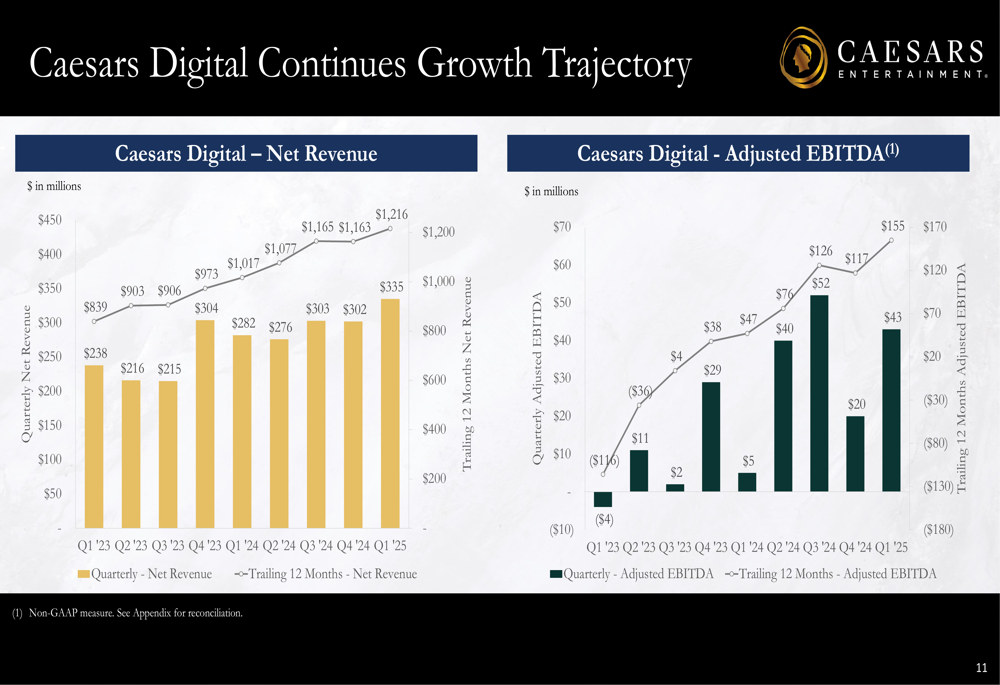

This strong performance is part of a longer-term growth trajectory for Caesars Digital, which has shown consistent improvement in both revenue and profitability over recent quarters:

Key drivers behind this digital growth include improvements in sportsbetting hold rates, which increased from 4.30% in 2021 to 7.00% in 2024 (with a long-term target of 10.0%), and significant expansion in iGaming handle, which grew from $5,621 million in 2021 to $14,920 million in 2024. The company’s multi-casino brand strategy, including Caesars Palace Online Casino (EPA:CASP) (launched in Q3 2023) and Horseshoe Online Casino (launched in Q4 2024), has also contributed to this success.

Portfolio Overview and Investment Cycle

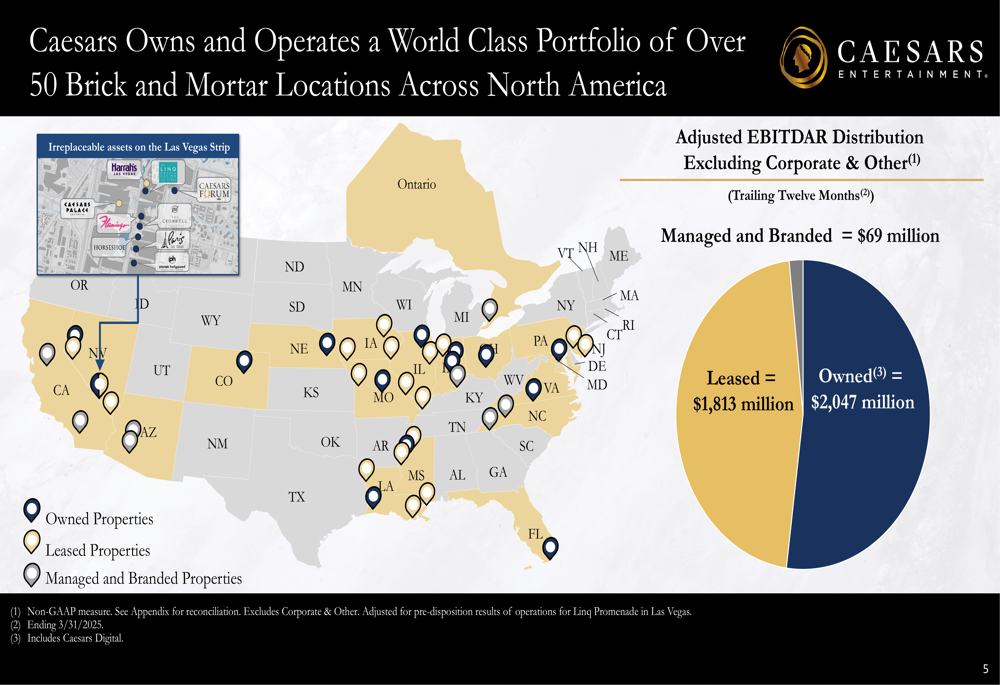

Caesars operates a diverse portfolio of 50 brick-and-mortar locations across North America, with its digital platform extending across 32 jurisdictions. The company’s property distribution and EBITDAR breakdown demonstrate the balance between owned, leased, and managed properties:

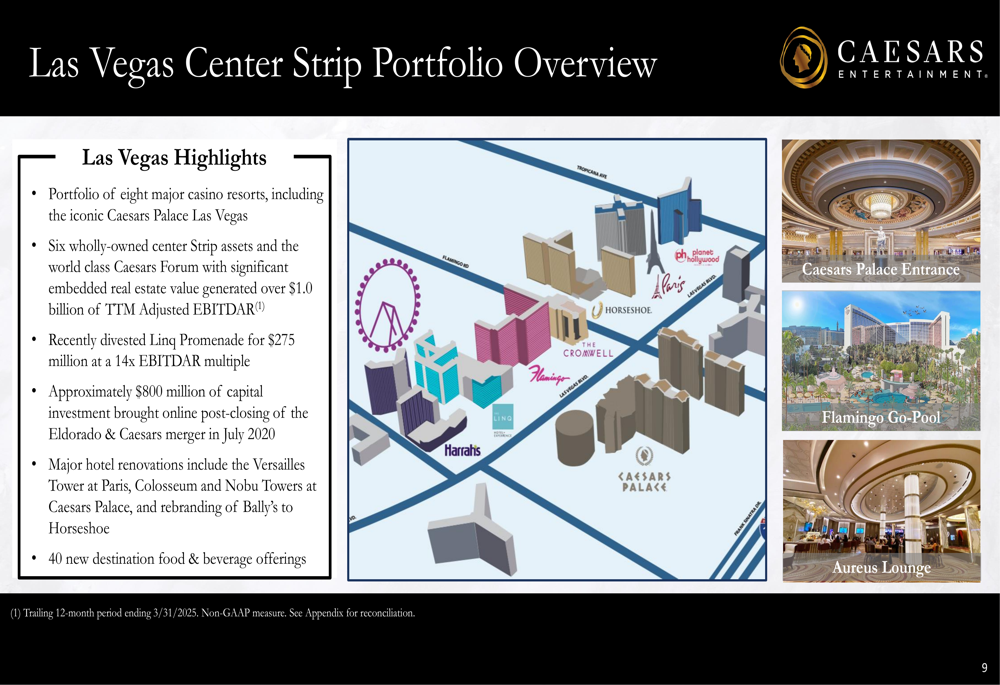

The Las Vegas Center Strip remains a core focus for Caesars, with eight major casino resorts including the flagship Caesars Palace Las Vegas. These properties collectively generate over $1.0 billion in trailing twelve-month Adjusted EBITDAR:

The company has recently completed a major regional investment cycle, having deployed over $2.6 billion of capital since the Eldorado (SO:ELDO11B) & Caesars merger. This investment has supported renovations and expansions across 38 regional properties that are now integrated into the Caesars Rewards program.

Financial Outlook and Debt Management

Looking ahead to the remainder of 2025, Caesars provided financial guidance that includes a master lease rent of $1,350 million and interest expenses of approximately $775 million based on a 6.5% weighted average cost of debt. The company expects midpoint capital expenditures of $606 million (excluding the Caesars Virginia joint venture) and cash income taxes estimated at approximately 5% of Adjusted EBITDAR.

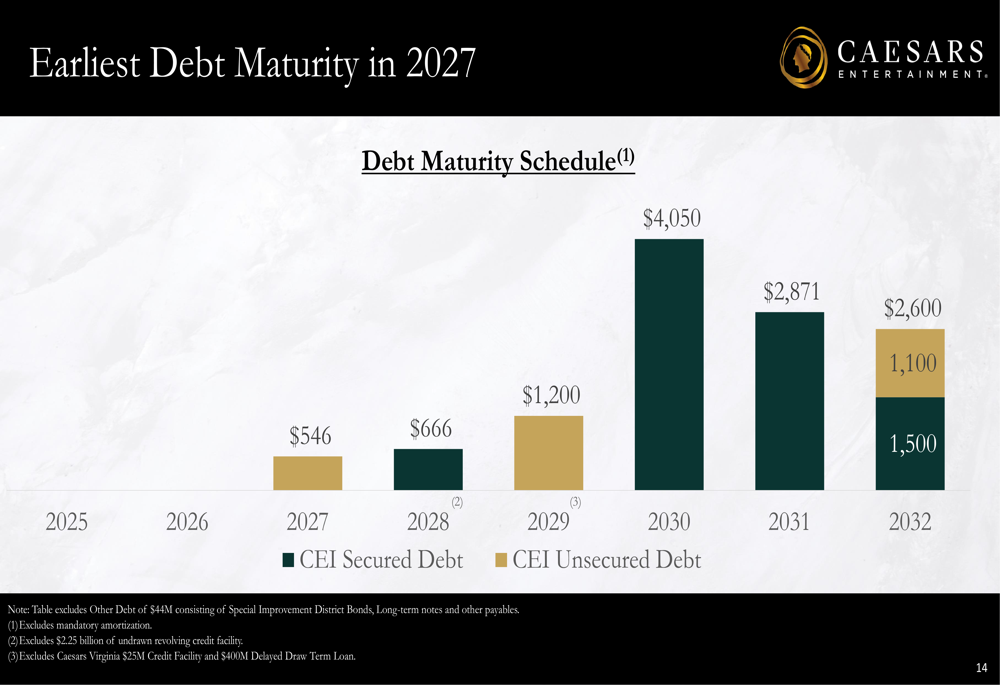

Management emphasized that growing free cash flow will enable debt repayment and/or share repurchases, addressing concerns about the company’s leverage. The debt maturity schedule shows manageable near-term obligations, with significant maturities not occurring until 2027 and beyond:

During the earnings call, CEO Tom Reeg expressed confidence in the company’s strategic position, stating, "Our digital segment is growing like we’ve never seen before in a prior downturn," and "We feel very good about where we sit."

Conclusion

Caesars’ Q1 2025 results present a mixed but generally positive picture, with digital operations emerging as the clear highlight amid more modest performance in traditional casino operations. While the company missed analyst expectations for both EPS and revenue, the 4.1% growth in Adjusted EBITDAR and particularly strong digital segment performance appear to have reassured investors, as evidenced by the positive stock movement following the announcement.

The completion of major capital investments positions Caesars to focus on debt reduction and free cash flow generation going forward. However, challenges remain, including high projected interest expenses and relatively flat performance in the key Las Vegas market. The company’s ability to continue digital growth while maintaining stable performance in its traditional casino operations will be crucial for long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.