Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

Cambi ASA (OB:CAMBI) presented its Q2 2025 results on August 19, 2025, revealing a significant financial recovery from its disappointing first quarter. The company’s stock, which had dropped 8.4% following Q1 results, has since rebounded to NOK 21.6, reflecting renewed investor confidence in the wastewater treatment technology provider.

The Q2 presentation highlighted record revenue performance, strategic expansion through acquisition, and the company’s positioning amid evolving industry challenges including PFAS contamination concerns and international trade developments.

Quarterly Performance Highlights

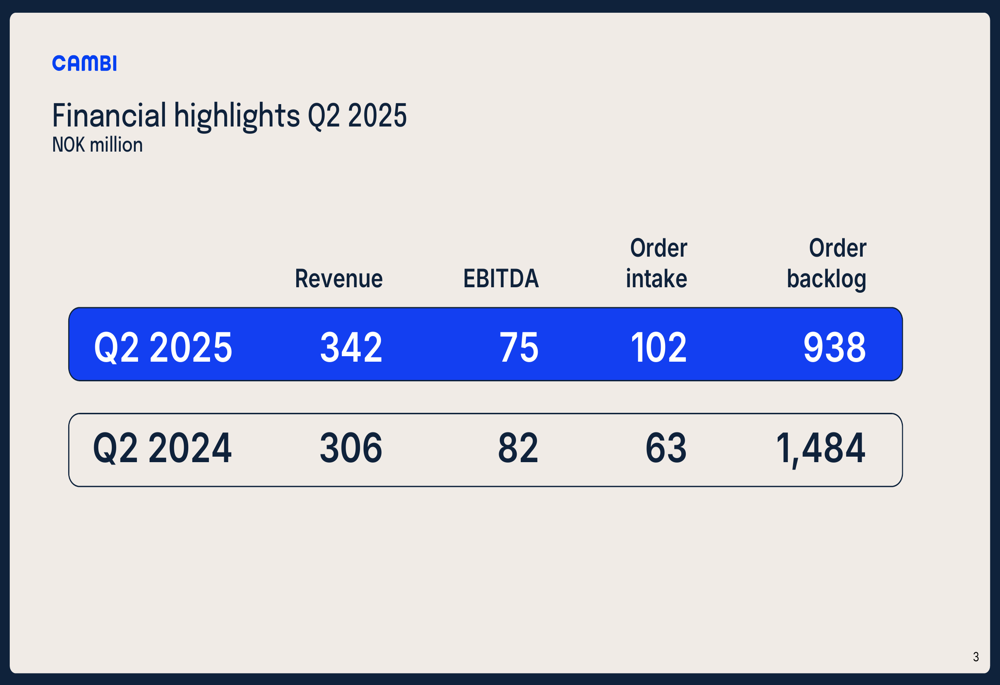

Cambi reported record quarterly revenue of NOK 342 million in Q2 2025, representing an 11.8% increase from NOK 306 million in Q2 2024 and a substantial 52% improvement from Q1 2025’s NOK 225 million.

As shown in the following financial highlights chart:

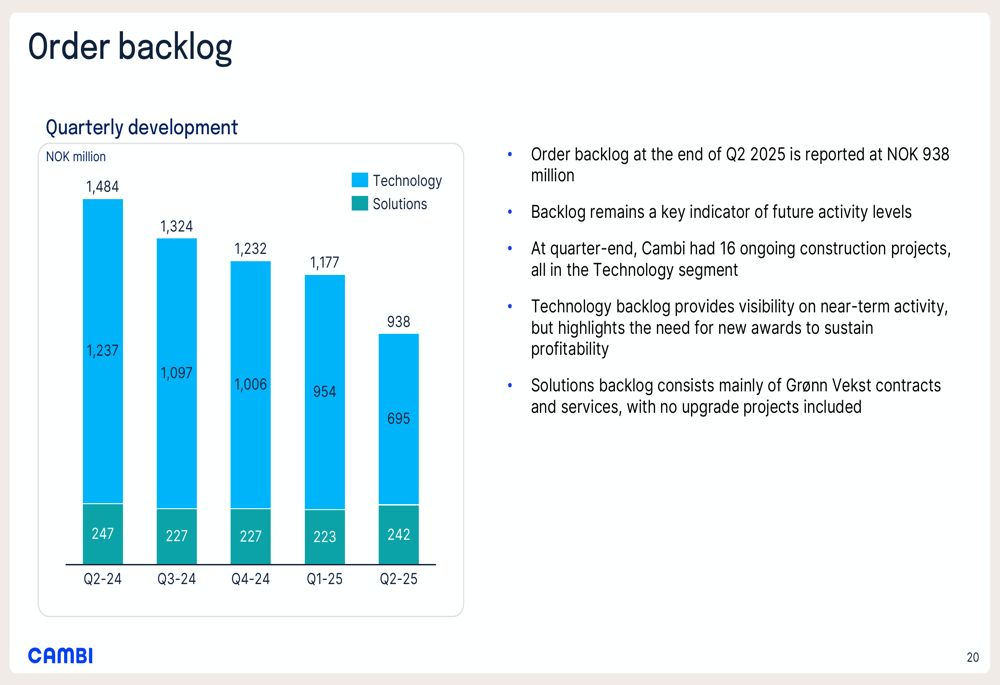

Despite the revenue growth, EBITDA declined 8.5% year-over-year to NOK 75 million, though this represents a dramatic 436% improvement from Q1’s disappointing NOK 14 million. Order intake increased by 61.9% to NOK 102 million, while the order backlog decreased to NOK 938 million from NOK 1,484 million a year earlier.

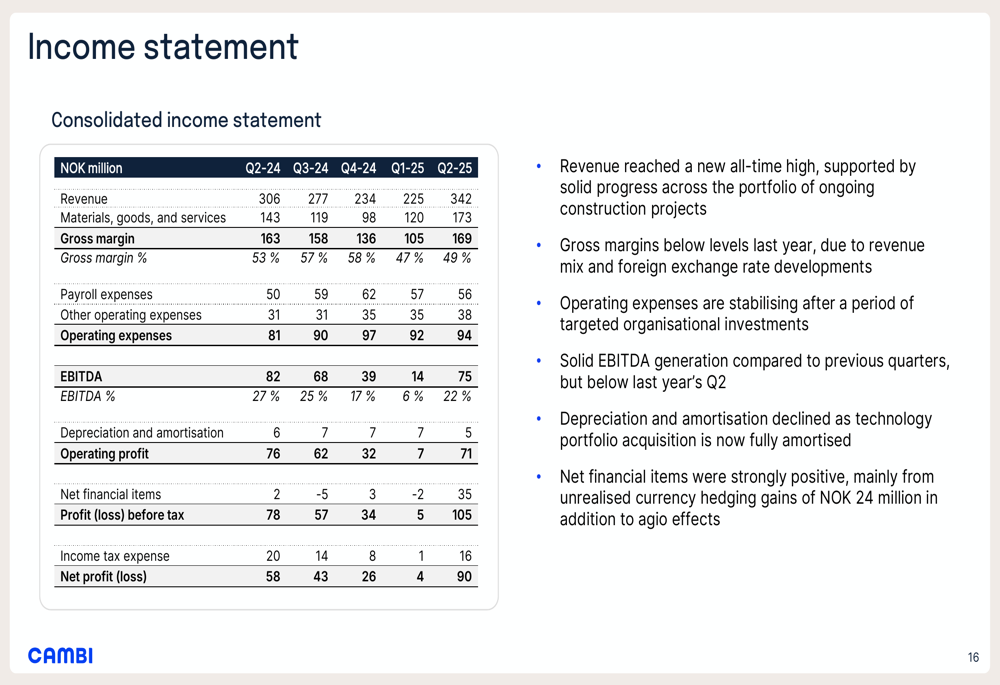

The company’s income statement reveals that while revenue reached an all-time high, gross margins have declined compared to last year, though operating expenses have begun to stabilize following a period of targeted organizational investments:

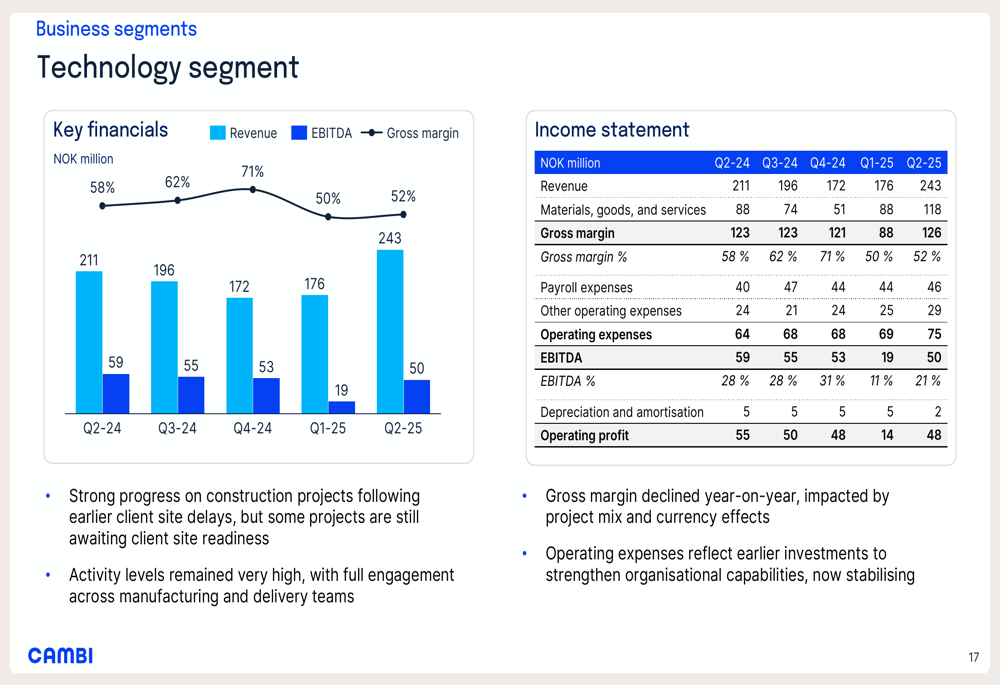

Cambi’s Technology segment showed particularly strong performance, with high activity levels across the global project portfolio:

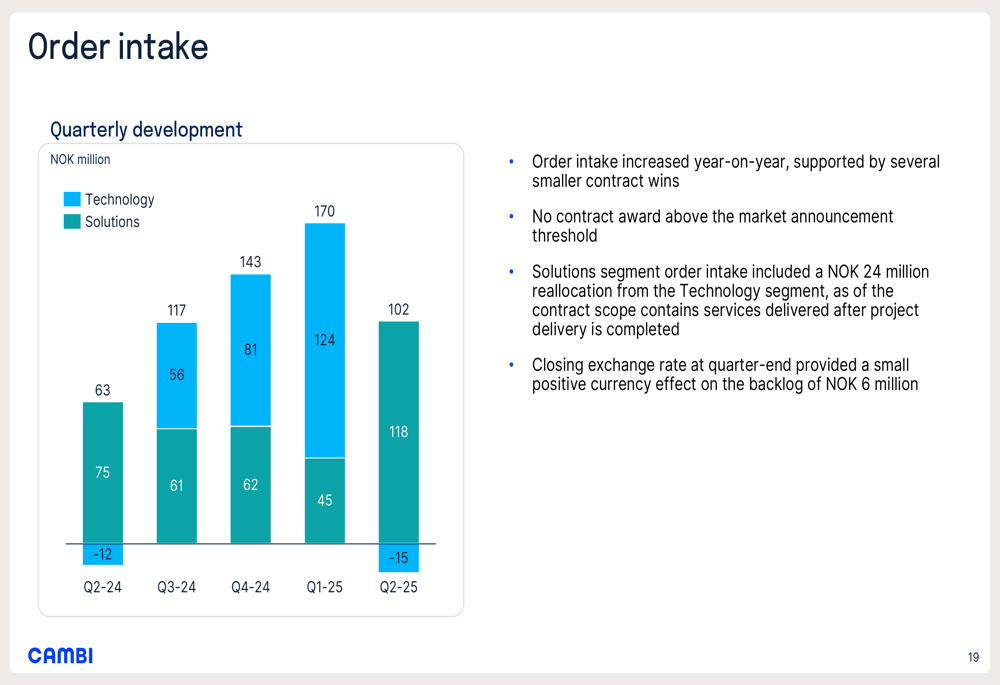

The company’s order intake has shown consistent improvement over recent quarters, providing confidence in future revenue streams:

However, the order backlog has declined significantly year-over-year, though it remains substantial at NOK 938 million:

Strategic Initiatives

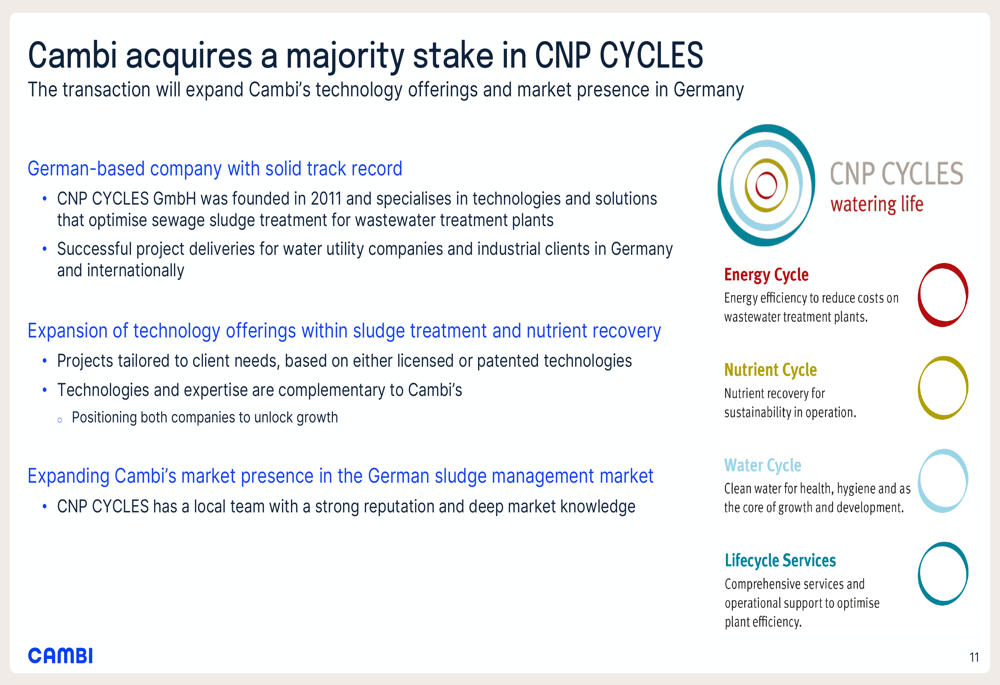

A key strategic development in Q2 was Cambi’s acquisition of a 51% stake in CNP CYCLES GmbH, a company specializing in technologies and solutions that optimize sewage sludge treatment. With 10 employees and annual revenues of EUR 3.0 million, this acquisition expands Cambi’s technology offerings and strengthens its market position.

The strategic rationale behind the acquisition is illustrated in the following slide:

The company also identified Germany as a potentially important growth market, citing a €500 billion infrastructure fund launched in March, with 20% earmarked for climate and energy transition projects. However, Cambi acknowledged intense technology competition in this market and noted that it has not been very successful in Germany to date.

Industry Challenges & Positioning

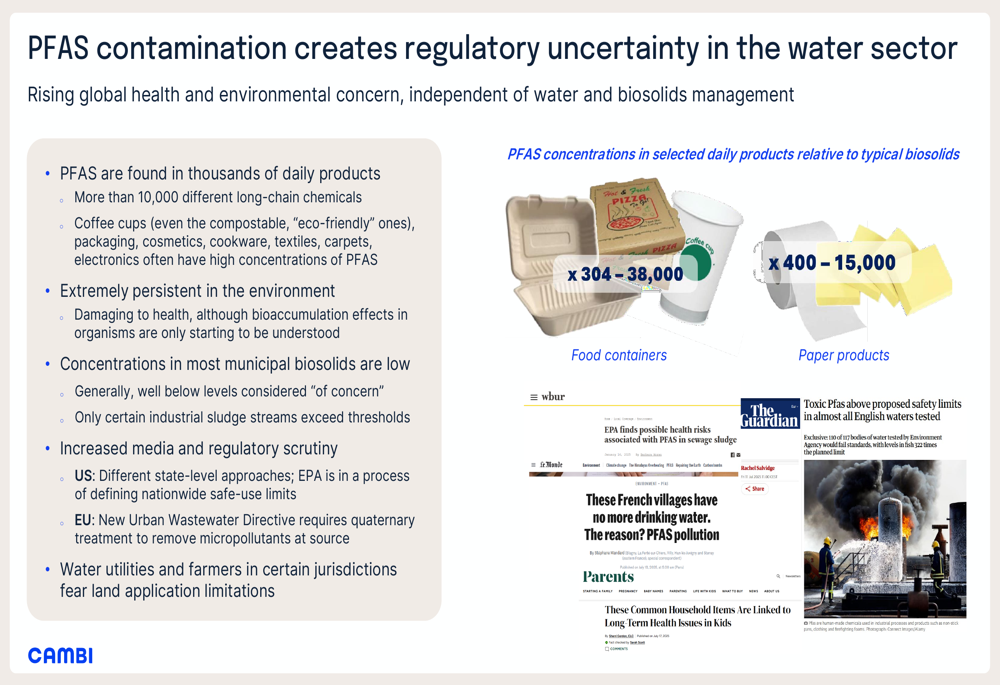

Cambi highlighted several industry challenges that are shaping its strategic positioning. One significant issue is the growing concern over PFAS contamination, which is creating regulatory uncertainty in the water sector. The company emphasized that its Thermal Hydrolysis Process (THP) technology is suitable for all biosolids routes, providing flexibility as regulations evolve.

The following slide illustrates the PFAS contamination issue:

Another challenge is the implementation of the US-UK Economic Prosperity Deal, which introduces a 10% base tariff. Cambi noted that its three ongoing US projects are contractually protected, but the company is exploring options for domestic US manufacturing to mitigate future tariff impacts.

Forward-Looking Statements

Looking ahead, Cambi expressed confidence in sustained global demand for sustainable sludge treatment solutions. The company plans to focus on project execution and securing new contracts while continuing strategic investments in organizational capabilities.

The order backlog breakdown indicates that 39% is scheduled for execution in 2025, 41% in 2026, and 20% in 2027 and beyond, providing good visibility into future revenue streams. In terms of currency exposure, 41% of the backlog is in NOK, 31% in EUR, and 28% in USD.

Cambi’s Board approved a dividend of NOK 0.30 per share, which has been distributed, and authorized additional dividends of up to NOK 0.70 per share, signaling confidence in the company’s financial position and future prospects.

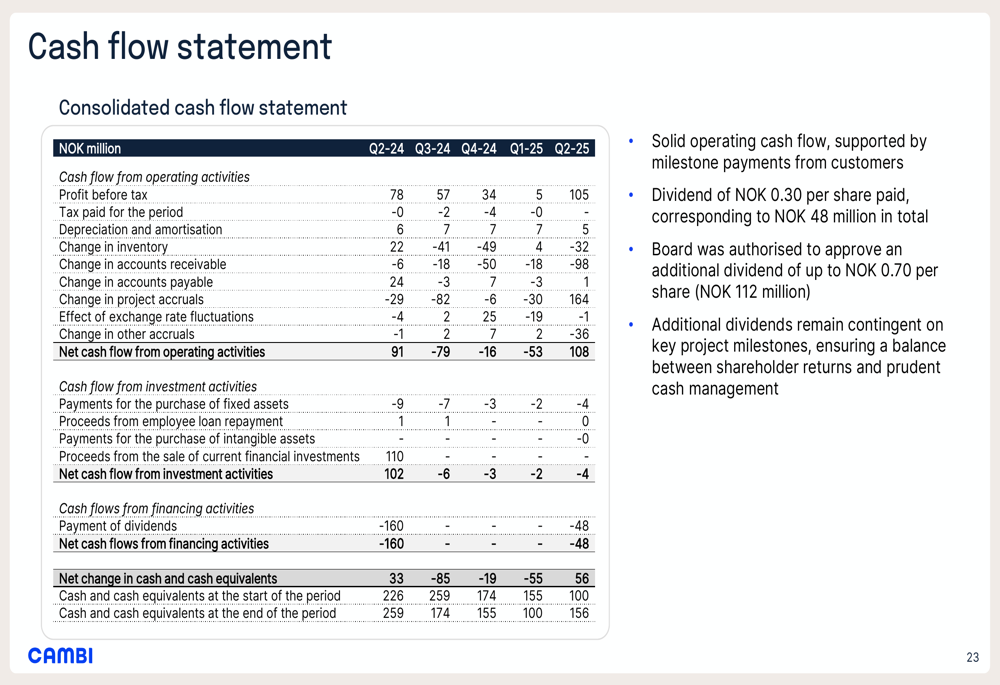

The company’s solid operating cash flow, supported by milestone payments from customers, further strengthens its financial foundation:

The Q2 2025 results represent a significant recovery from Cambi’s disappointing Q1 performance. While challenges remain, including declining gross margins and a reduced order backlog compared to the previous year, the record revenue and strategic initiatives position the company to capitalize on global demand for sustainable wastewater treatment solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.