Verizon to cut 15,000 jobs amid growing competition pressures - WSJ

Introduction & Market Context

Camurus AB (STO:CAMX) presented its first quarter 2025 results on May 15, revealing strong financial performance despite challenging market conditions. The Swedish biopharmaceutical company, which specializes in long-acting drug delivery systems, reported significant revenue and profit growth, though its stock price fell 12.95% to 541 SEK following the announcement.

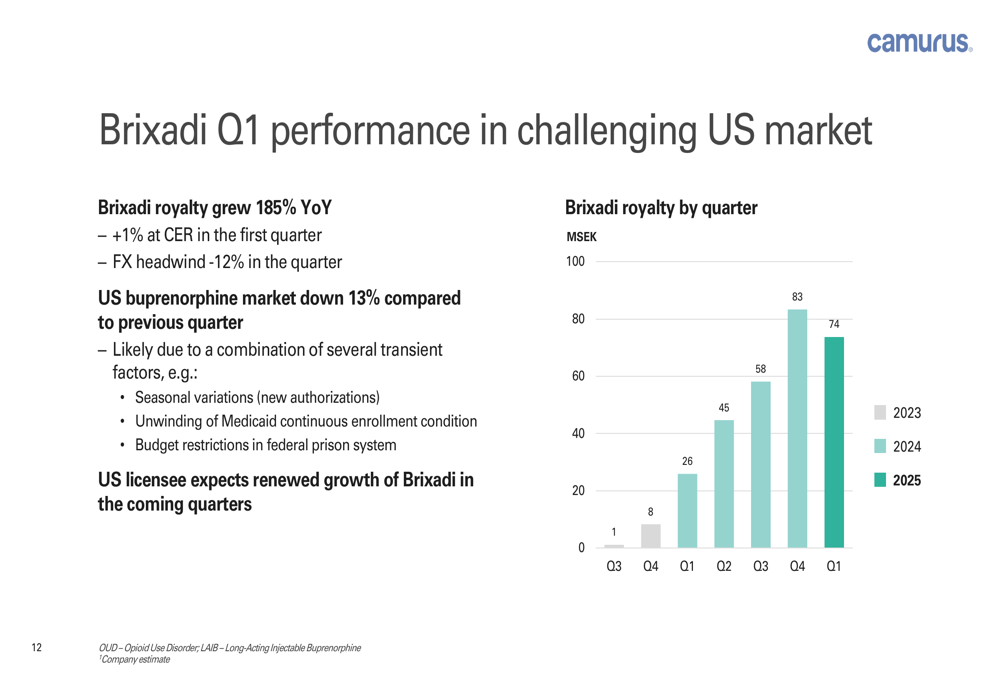

The company continues to strengthen its position in the opioid dependence treatment market, particularly in Australia and Europe where it maintains over 80% market share. However, the US opioid use disorder market experienced a 13% decline during the quarter, creating headwinds for Camurus’ US-marketed product Brixadi.

Quarterly Performance Highlights

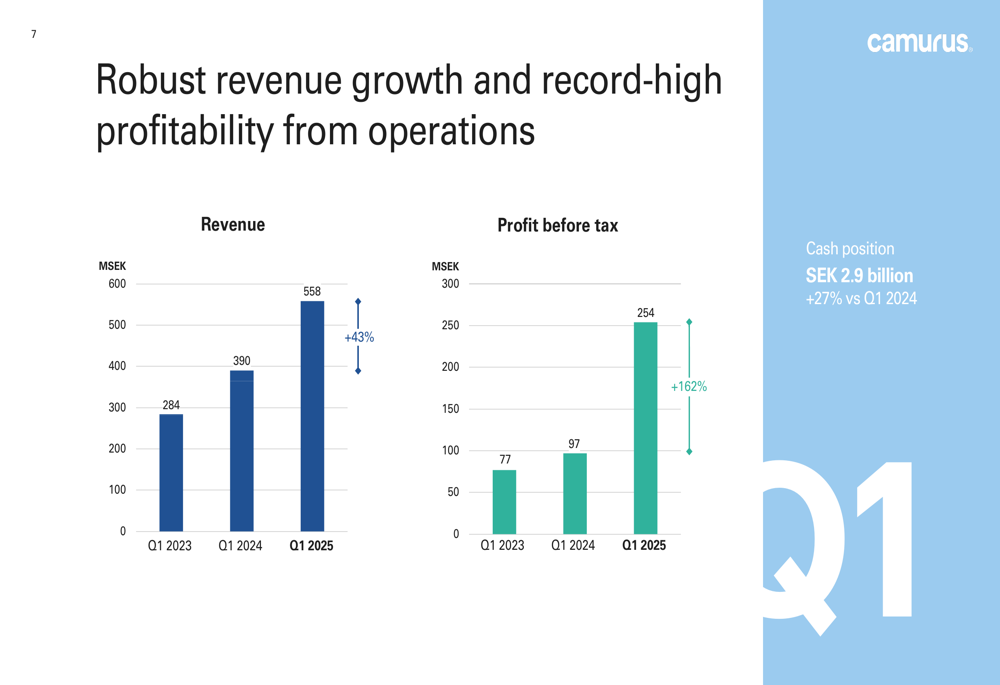

Camurus delivered exceptional financial results in Q1 2025, with total revenue reaching SEK 558 million, representing a 43% increase year-over-year. The company achieved record-high profitability with profit before tax surging 162% to SEK 254 million, accounting for 45.5% of sales.

As shown in the following chart of quarterly revenue and profit growth:

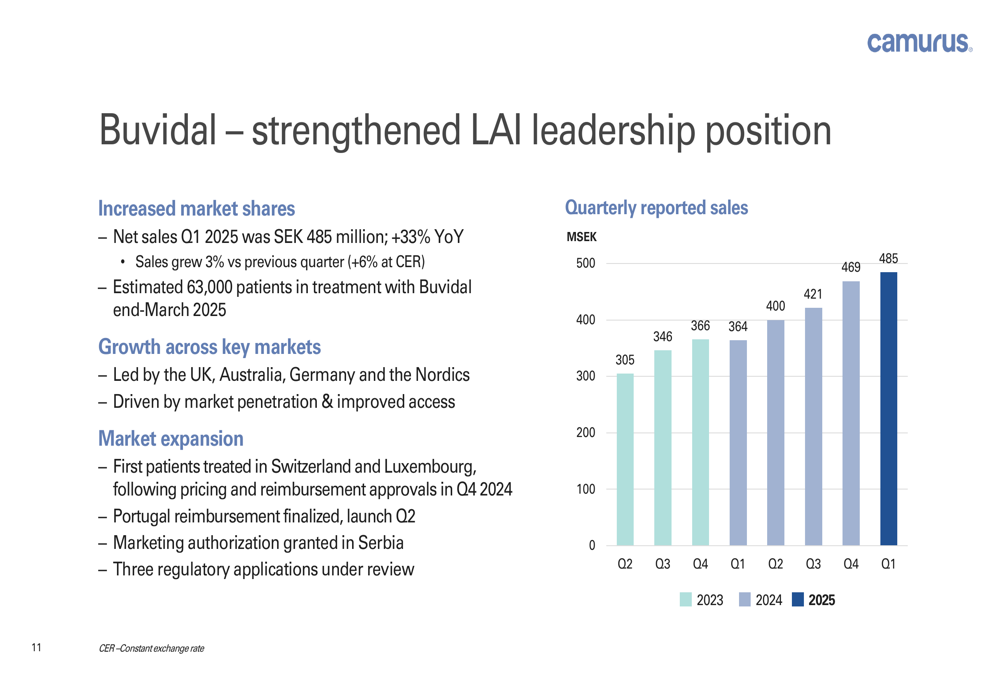

Buvidal, Camurus’ flagship product for opioid dependence, continued its strong performance with sales increasing 33% year-over-year to SEK 485 million. The company estimates approximately 63,000 patients were being treated with Buvidal by the end of March 2025, with key growth markets including the UK, Australia, Germany, and the Nordics.

The quarterly sales progression for Buvidal demonstrates consistent growth:

Meanwhile, Brixadi royalties grew 185% year-over-year but remained flat quarter-over-quarter at SEK 74 million, reflecting challenges in the US market:

Detailed Financial Analysis

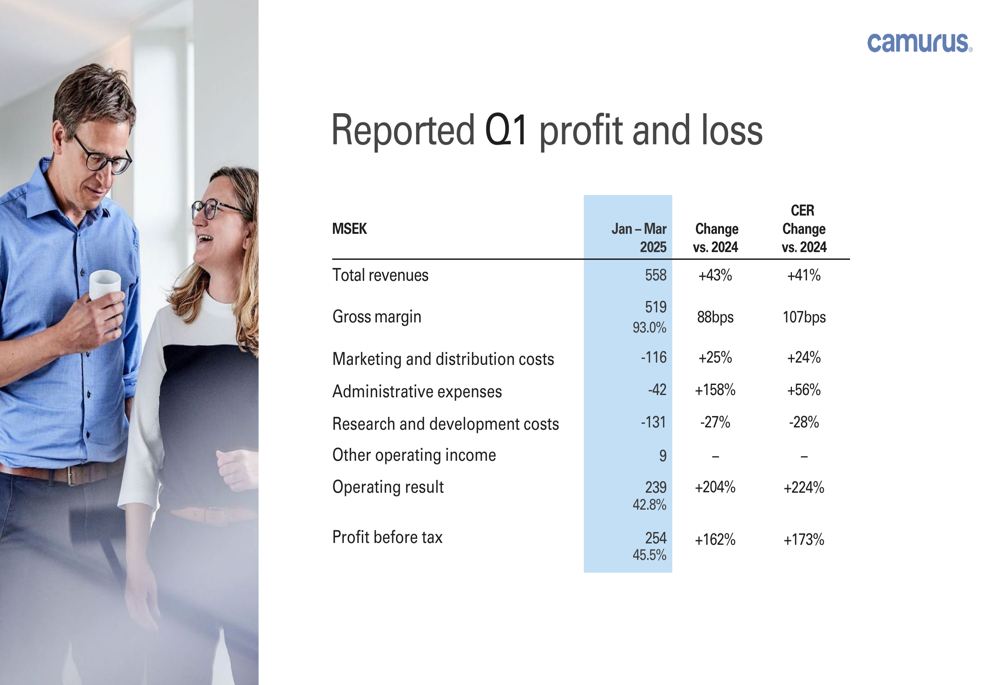

Camurus’ Q1 2025 financial performance showed impressive growth across key metrics. The company maintained a strong gross margin of 93.0%, an improvement of 88 basis points year-over-year. Operating result increased by 204% to SEK 239 million, representing 42.8% of revenue.

The detailed profit and loss statement reveals the company’s financial strength:

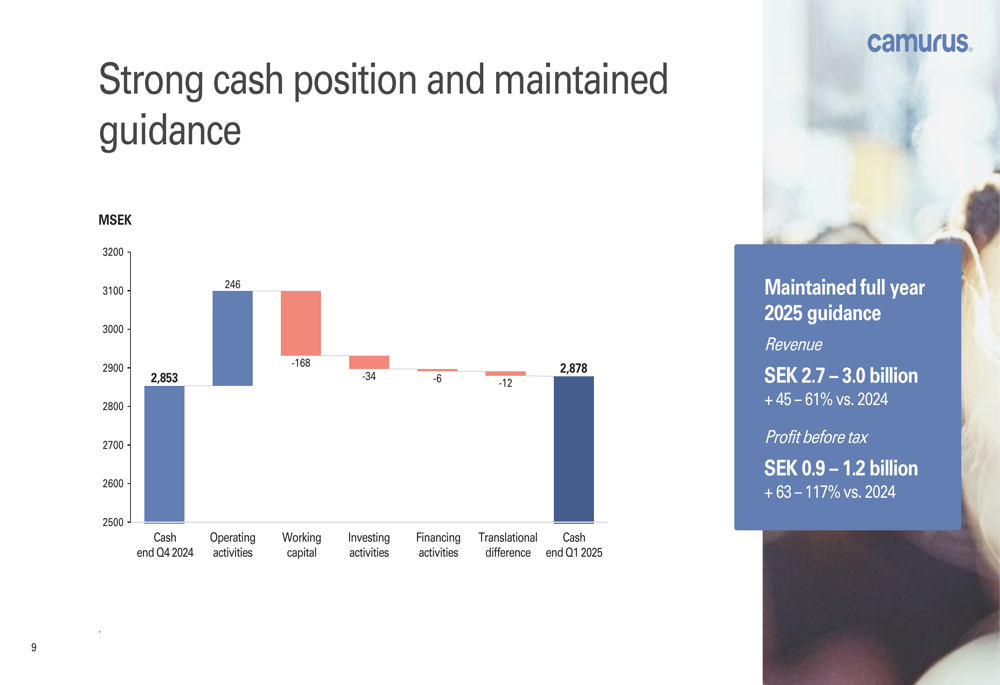

The company’s cash position remains robust at SEK 2.9 billion, a 27% increase compared to Q1 2024. This strong liquidity provides Camurus with significant flexibility to invest in its pipeline and commercial operations.

Cash flow details and maintained 2025 guidance are illustrated below:

Despite the strong financial performance, Camurus’ stock price declined 12.95% following the earnings announcement. This negative market reaction may be attributed to revenue falling short of market expectations, as the earnings forecast was reportedly $603.93 million compared to the actual revenue of SEK 558 million.

Pipeline and R&D Progress

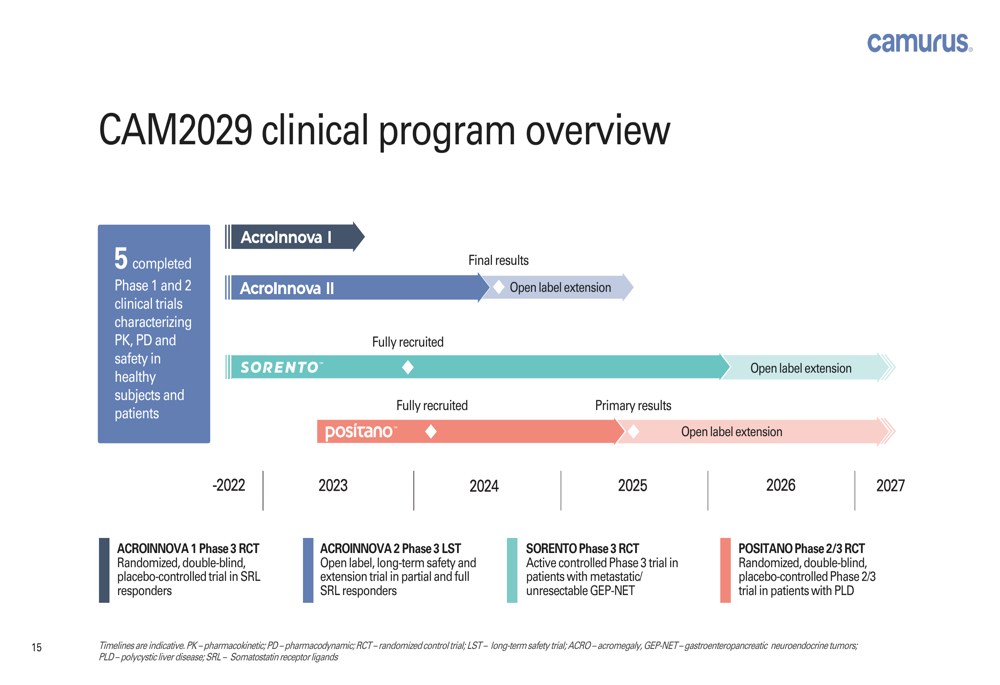

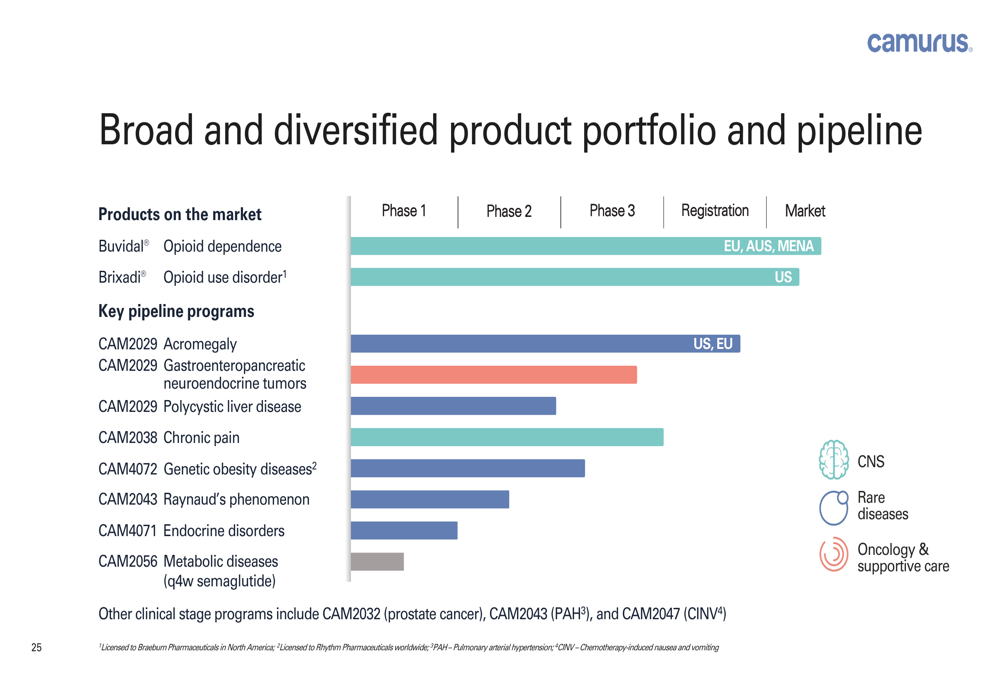

Camurus made significant progress with its pipeline during Q1 2025, particularly with CAM2029, its long-acting octreotide formulation being developed for multiple indications including acromegaly, gastroenteropancreatic neuroendocrine tumors (GEP-NET), and polycystic liver disease (PLD).

The company received a positive opinion from the Committee for Medicinal Products for Human Use (CHMP) in April 2025 for Oczyesa (CAM2029) in acromegaly, with final European Commission approval expected in June 2025. For the US market, Camurus plans to resubmit its New Drug Application after resolving manufacturing issues identified in a Complete Response Letter.

The clinical program for CAM2029 continues to advance:

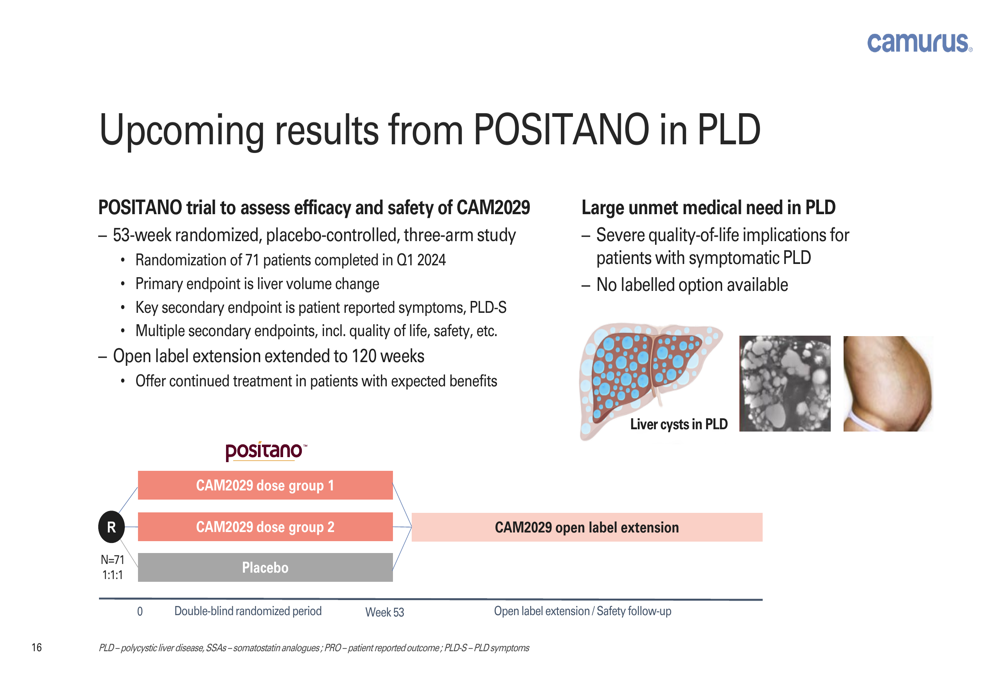

The POSITANO trial, evaluating CAM2029 in polycystic liver disease, completed randomization in Q1 2024 and is progressing toward important data readouts:

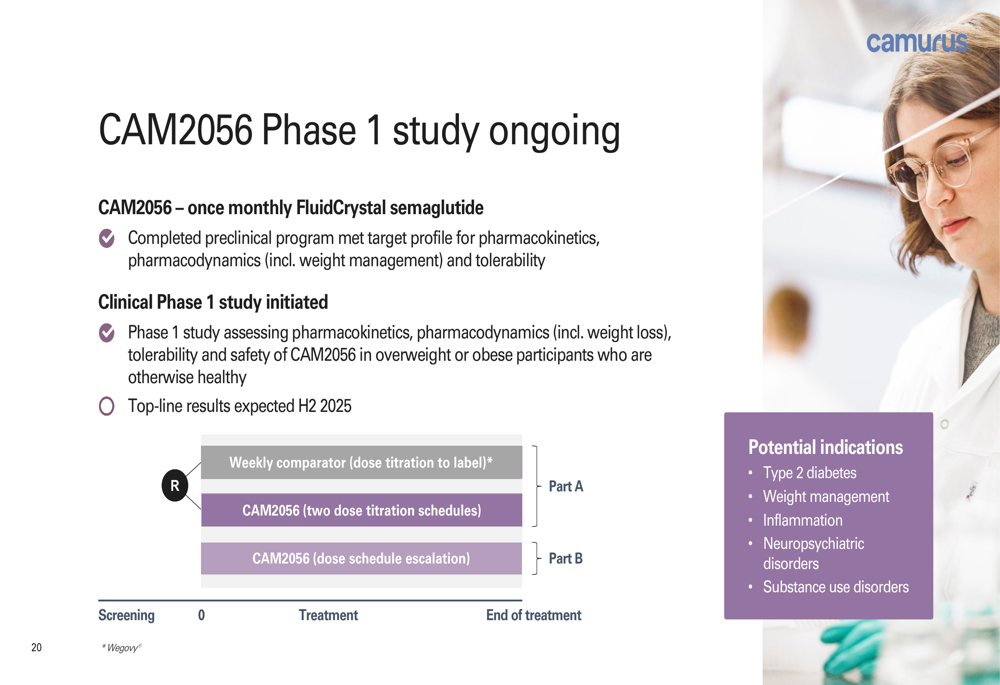

Additionally, Camurus initiated dosing in a Phase 1 study of CAM2056, a once-monthly formulation of semaglutide for metabolic diseases:

The company’s broad and diversified product portfolio and pipeline provide multiple growth opportunities:

Forward-Looking Statements

Camurus maintained its full-year 2025 guidance, projecting revenue between SEK 2.7-3.0 billion (45-61% growth versus 2024) and profit before tax of SEK 0.9-1.2 billion (63-117% growth versus 2024).

The company expects continued growth for Buvidal in Europe and other international markets, while its US licensee anticipates renewed growth for Brixadi in coming quarters despite current market challenges. Camurus is also preparing for the potential launch of Oczyesa in Europe following the expected approval in June 2025.

Key takeaways from the quarter highlight the company’s solid performance despite market headwinds:

CEO Fredrik Tiberg emphasized the company’s "solid first quarter with record high profitability from operations," while CFO Jon Garay Alonso highlighted Camurus’ continued market leadership with "a successful market share above 80%" in key regions.

Looking ahead, Camurus faces both opportunities and challenges, including potential impacts from Medicaid enrollment unwinding on US sales, market saturation in opioid dependence treatments, and regulatory hurdles for new product approvals. However, the company’s strong financial position and diversified pipeline position it well to navigate these challenges while pursuing long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.