Gold prices edge lower; heading for weekly losses ahead of U.S.-Russia talks

Introduction & Market Context

CareDx, Inc. (NASDAQ:CDNA) presented its Q2 2024 financial results on July 31, 2024, revealing strong revenue growth and a return to profitability. The transplant diagnostics company reported significant improvements across all business segments while highlighting clinical validation of its key products through major studies.

The company’s performance represents a notable turnaround from previous quarters, with positive adjusted EBITDA and cash flow generation. This comes as CareDx continues to strengthen its position in the transplant diagnostics market through both clinical validation and expanded insurance coverage.

Quarterly Performance Highlights

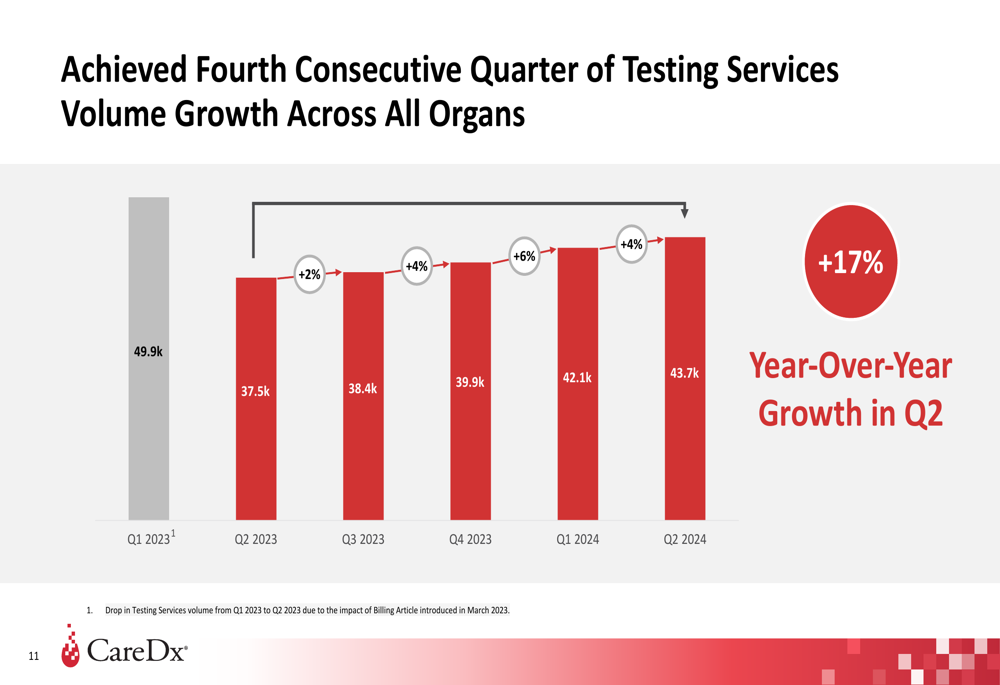

CareDx reported total revenue of $92.3 million for Q2 2024, representing a 31% increase year-over-year. Testing Services volume grew to 43,700 tests, up 17% compared to the same period last year. The company noted that this growth follows the impact of a Billing Article introduced in March 2023, which had caused a significant drop in testing volume in Q2 2023.

As shown in the following chart of quarterly testing services volume:

The company reported a GAAP net loss of $1.4 million for the quarter, but achieved non-GAAP net income of $13.6 million and positive adjusted EBITDA of $12.9 million. Cash from operations totaled $18.9 million, with the company maintaining a strong balance sheet showing $228.9 million in cash, equivalents, and marketable securities with no debt.

Detailed Financial Analysis

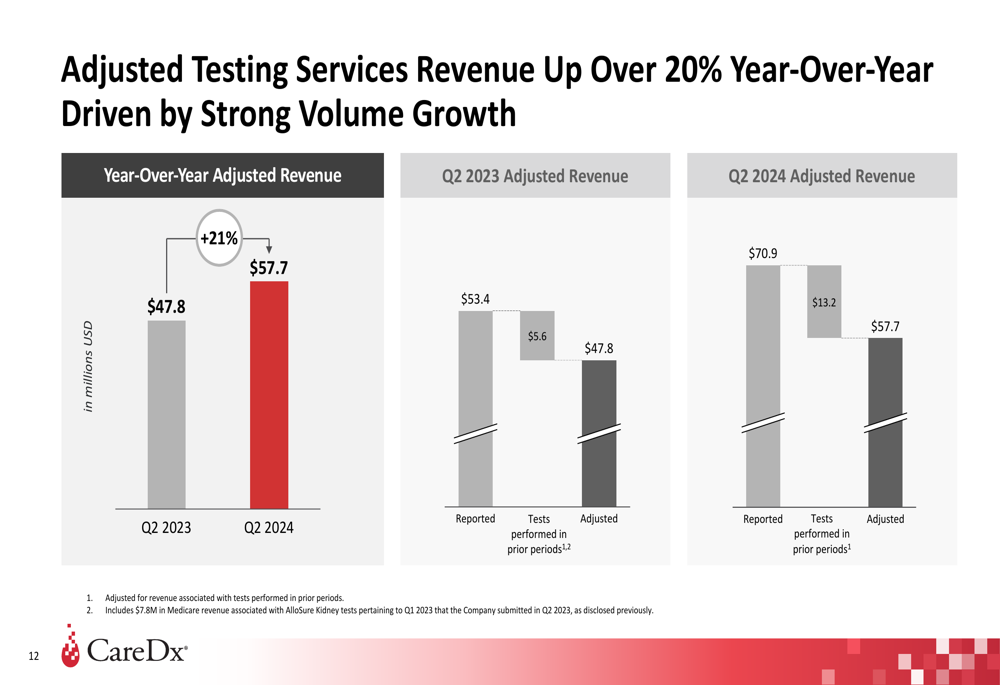

Testing Services revenue, which represents CareDx’s largest business segment, showed strong growth in Q2 2024. The company reported $70.9 million in Testing Services revenue, including $13.2 million from tests performed in prior periods. When adjusted to exclude revenue from prior periods, Testing Services revenue was $57.7 million, representing a 21% increase from the adjusted $47.8 million in Q2 2023.

The following chart illustrates this growth:

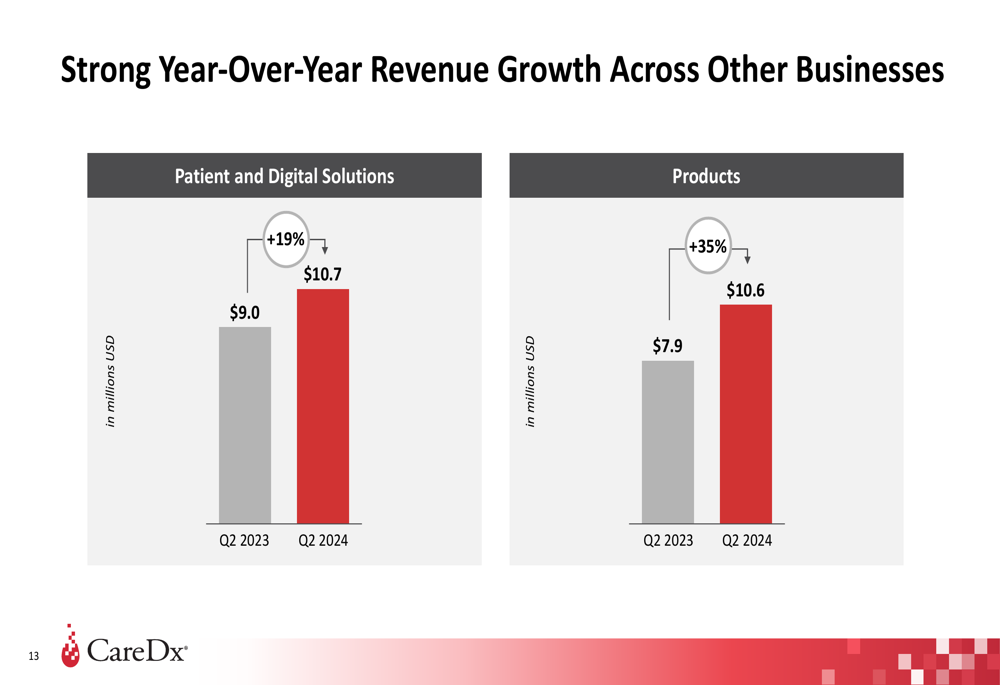

CareDx’s other business segments also demonstrated robust performance. Patient and Digital Solutions revenue increased by 19% year-over-year to $10.7 million, while Products revenue grew by 35% to $10.6 million compared to Q2 2023.

This segment performance is visualized in the following chart:

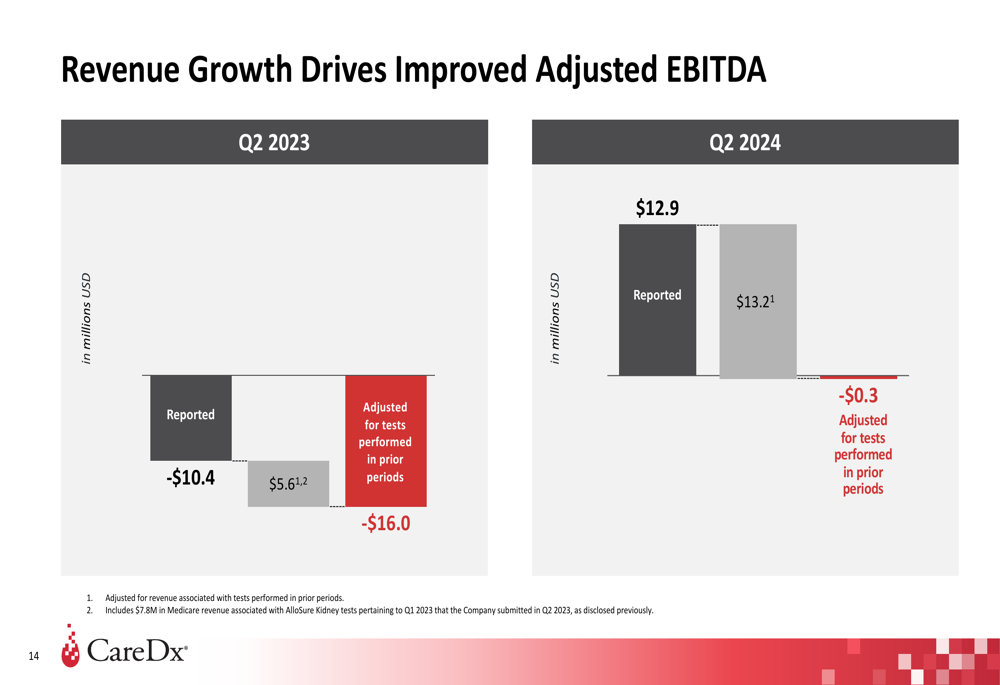

Perhaps most notably, CareDx achieved a dramatic improvement in adjusted EBITDA, moving from -$10.4 million in Q2 2023 to $12.9 million in Q2 2024. When adjusted for tests performed in prior periods, the company nearly reached breakeven with -$0.3 million in Q2 2024, compared to -$16.0 million in the prior year period.

The following chart demonstrates this significant improvement:

Strategic Initiatives

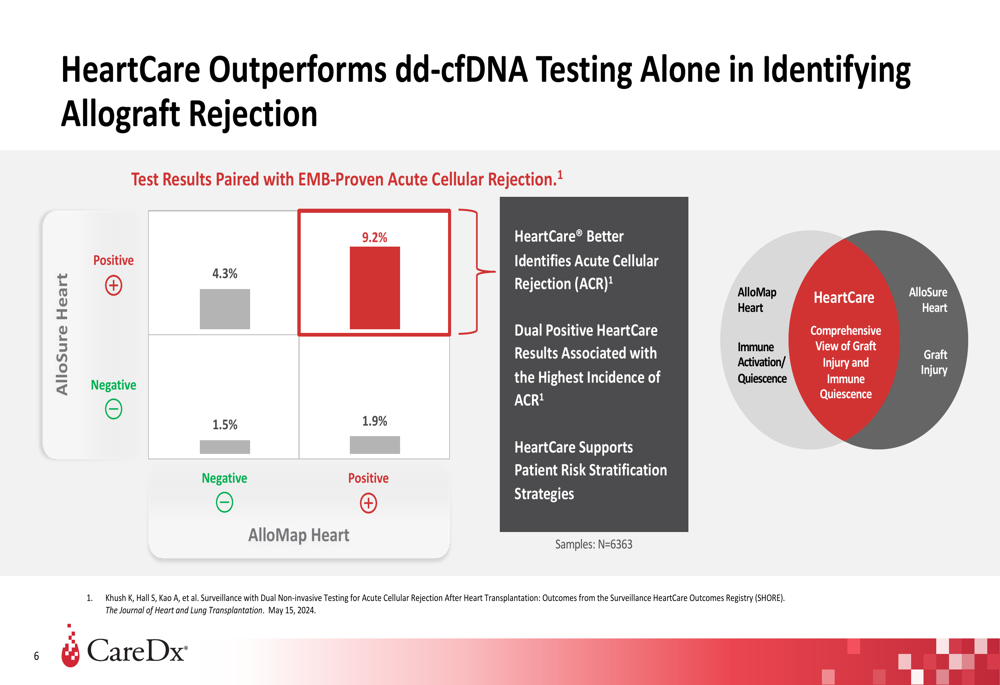

CareDx highlighted two major clinical validations that strengthen its market position. The SHORE study, published in the Journal of Heart and Lung Transplantation, demonstrated that HeartCare outperforms dd-cfDNA alone in identifying allograft rejection. This study, which is described as the largest heart transplant study of its kind, encompassed over 2,700 patients across 67 transplant centers in the US.

Key findings from the study show that patients with dual positive HeartCare results had a 9.2% rate of EMB-proven Acute Cellular Rejection, significantly higher than the rates for patients with single positive or negative results. This supports HeartCare’s value in patient risk stratification strategies.

The following chart illustrates these findings:

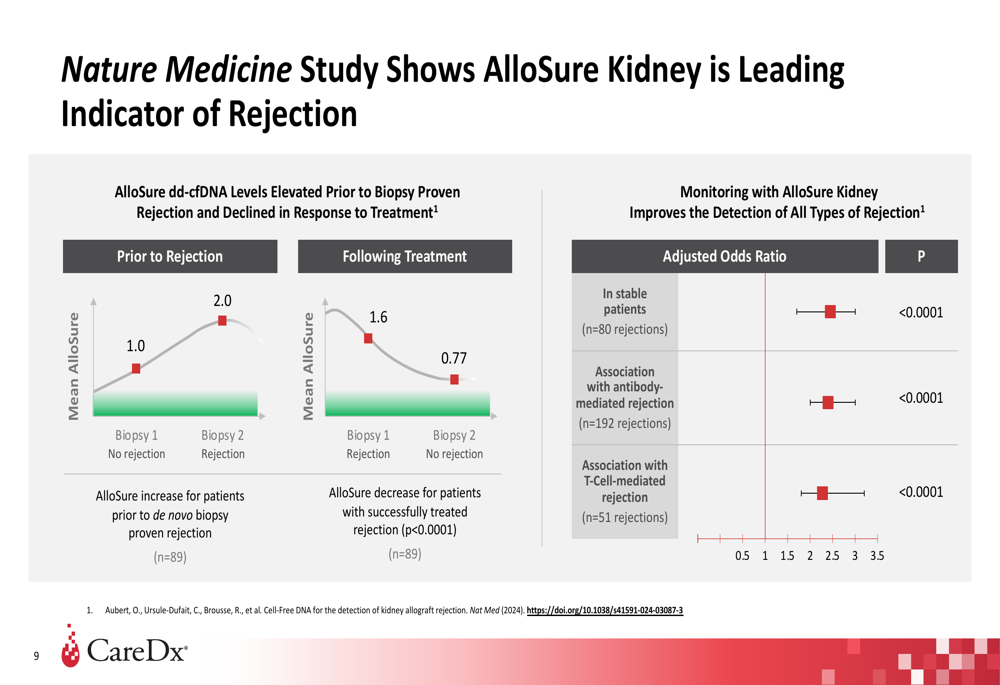

Additionally, a publication in Nature Medicine validated CareDx’s AlloView AI-enabled risk prediction model and demonstrated that AlloSure Kidney can detect subclinical rejection in clinically stable patients. The study showed that AlloSure dd-cfDNA levels elevated prior to biopsy-proven rejection and declined in response to treatment.

This clinical validation is illustrated in the following data:

The company also reported adding 27 million lives to existing coverage nationwide, expanding access to its diagnostic solutions.

Forward-Looking Statements

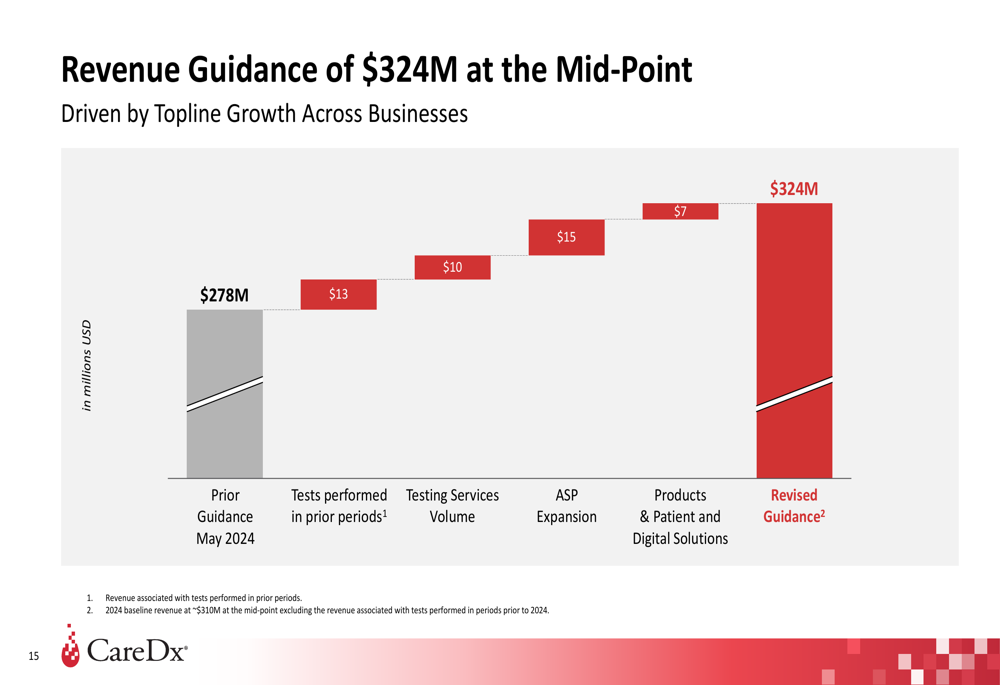

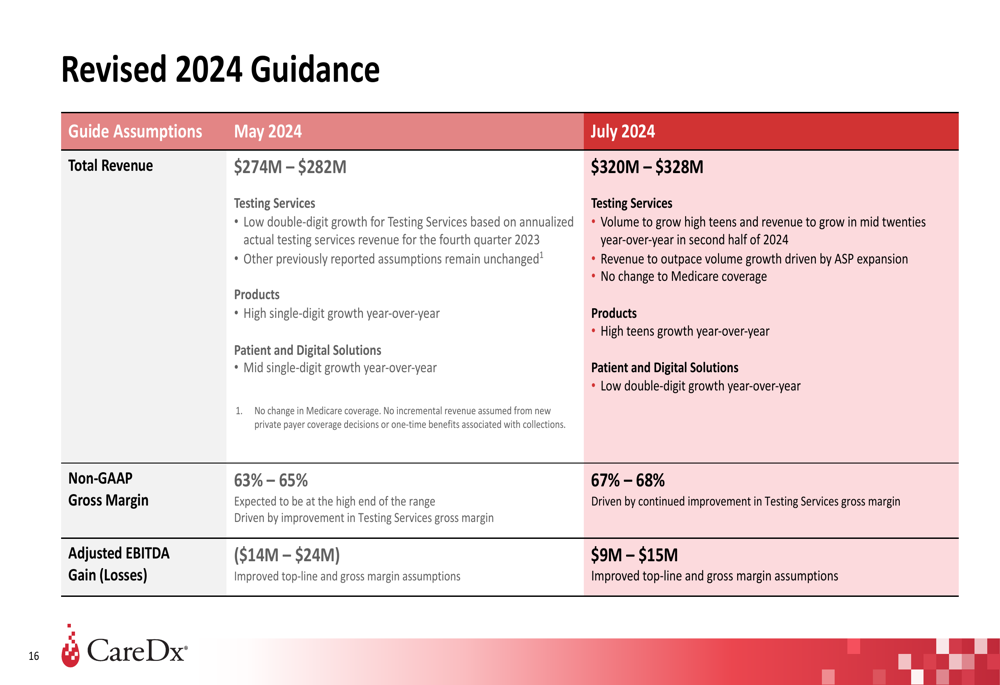

Based on its strong Q2 performance, CareDx raised its full-year 2024 guidance. The company now expects total revenue of $320-$328 million, up from its previous guidance provided in May 2024. This revision is attributed to several factors, including higher testing services volume, ASP expansion, and growth in Products and Patient and Digital Solutions.

The following chart breaks down the components contributing to the revised guidance:

The company also raised its adjusted EBITDA guidance to $9-$15 million. CareDx expects Testing Services volume to grow in the high teens and revenue to grow in the mid-twenties year-over-year in the second half of 2024, with revenue outpacing volume growth driven by ASP expansion.

The detailed revised guidance compared to previous assumptions is shown here:

Conclusion

CareDx’s Q2 2024 presentation reflects a company gaining momentum with strong revenue growth, a return to profitability, and significant clinical validation of its key products. The raised guidance suggests management’s confidence in continued growth throughout 2024, supported by volume expansion, pricing improvements, and broader insurance coverage.

The company’s focus on clinical validation through major studies appears to be strengthening its competitive position in the transplant diagnostics market. With a solid balance sheet and positive cash flow, CareDx seems well-positioned to continue its growth trajectory in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.