5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

CenterPoint Energy (NYSE:CNP) reported strong third-quarter results and unveiled an ambitious long-term growth strategy during its Q3 2025 investor presentation on October 23. The utility company’s shares rose 0.37% in premarket trading to $40.20, approaching its 52-week high of $40.50, as investors responded positively to the earnings beat and expansive capital plan.

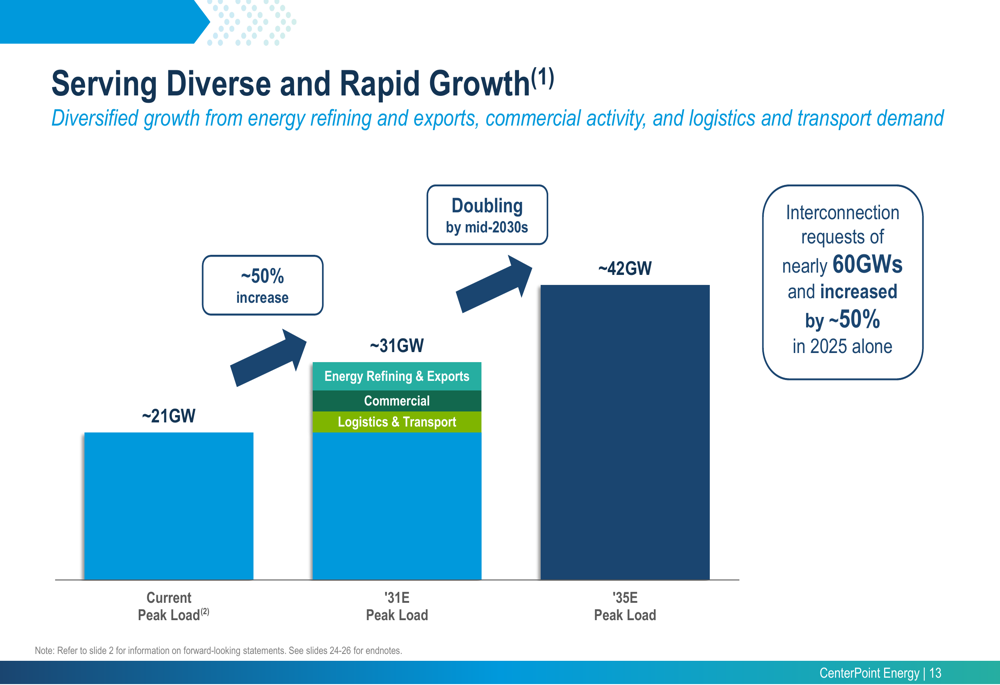

The company’s performance comes amid growing energy demand in its service territories, particularly from data centers, with interconnection requests increasing by approximately 50% in 2025 alone. This growth trajectory has positioned CenterPoint to make significant infrastructure investments while maintaining strong financial metrics.

Quarterly Performance Highlights

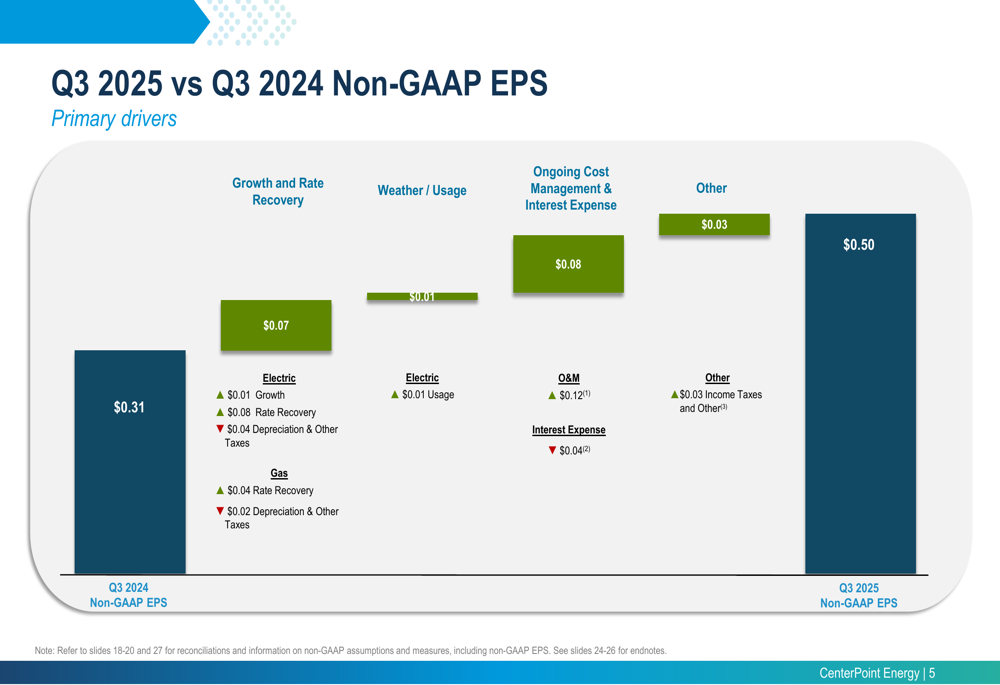

CenterPoint delivered a non-GAAP EPS of $0.50 for the third quarter, representing a substantial 60% increase from $0.31 in the same period last year and exceeding analyst expectations of $0.44. The company reaffirmed its 2026 non-GAAP EPS guidance range of $1.89-$1.91.

The presentation detailed the primary drivers behind the year-over-year EPS growth, highlighting contributions from multiple operational areas.

As shown in the following waterfall chart, the $0.19 EPS improvement was driven by growth and rate recovery (+$0.07), weather and usage factors (+$0.01), cost management and interest expense improvements (+$0.08), and other factors including income taxes (+$0.03):

Revenue for the quarter came in at $1.99 billion, slightly below the forecasted $2.05 billion, representing a 2.93% miss. Despite this revenue shortfall, the company’s strong earnings performance demonstrates effective cost management and operational efficiency.

Strategic Initiatives

The centerpiece of CenterPoint’s presentation was its new 10-year strategic plan, which outlines a comprehensive approach to capital deployment, financial targets, and operational improvements through 2035.

The plan features a $65 billion capital investment program plus over $10 billion in incremental opportunities, targeting 11%+ rate base growth through 2030 and annual non-GAAP EPS growth of 7-9% through 2035. The company expects to deliver in the mid-to-high end of this range for 2026-2028.

As illustrated in this overview slide of the 10-year plan:

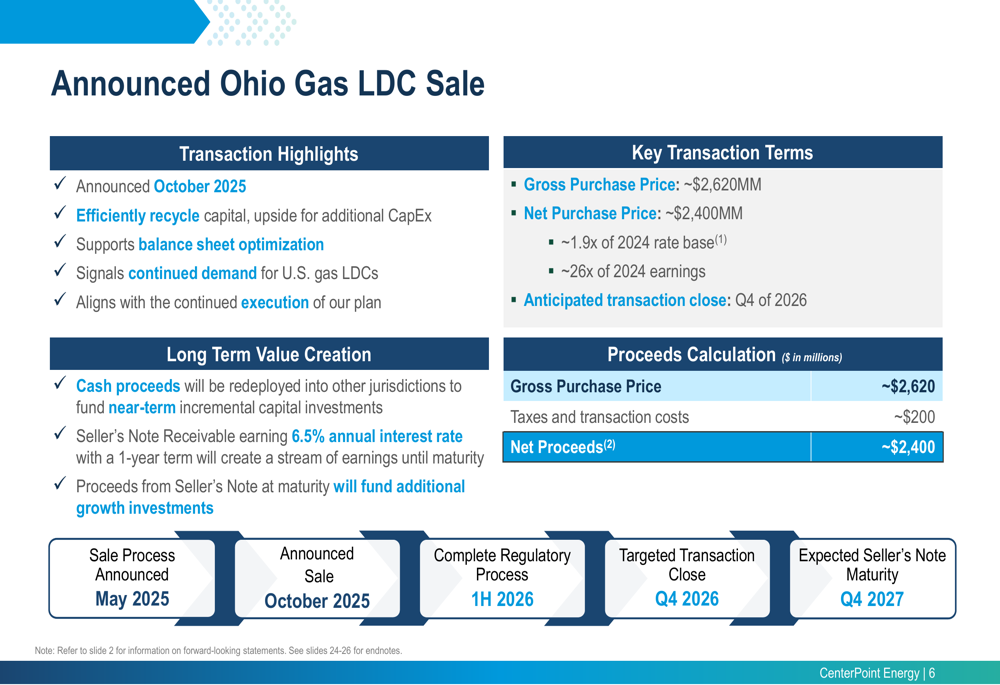

A key strategic development announced in the presentation was the sale of CenterPoint’s Ohio Gas LDC business, which is expected to generate approximately $2.62 billion in gross proceeds (about $2.4 billion net of taxes and transaction costs). The transaction, valued at approximately 1.9x 2024 rate base and 26x 2024 earnings, is anticipated to close in Q4 2026.

The following slide details the transaction structure, which includes a seller’s note receivable earning a 6.5% annual interest rate with a one-year term:

"This transaction allows us to efficiently recycle capital and provides upside for additional capital expenditures," management noted in the presentation. The proceeds will be redeployed to fund near-term incremental capital investments in other jurisdictions with higher growth potential.

Forward-Looking Statements

CenterPoint’s presentation highlighted the significant growth expected in its service territories, particularly in electric load. The company projects its peak load to increase from approximately 21GW currently to 31GW by 2031 (a 50% increase) and to 42GW by 2035 (a 100% increase).

The following chart illustrates this dramatic growth trajectory and the increasing interconnection requests, which have reached nearly 60GW:

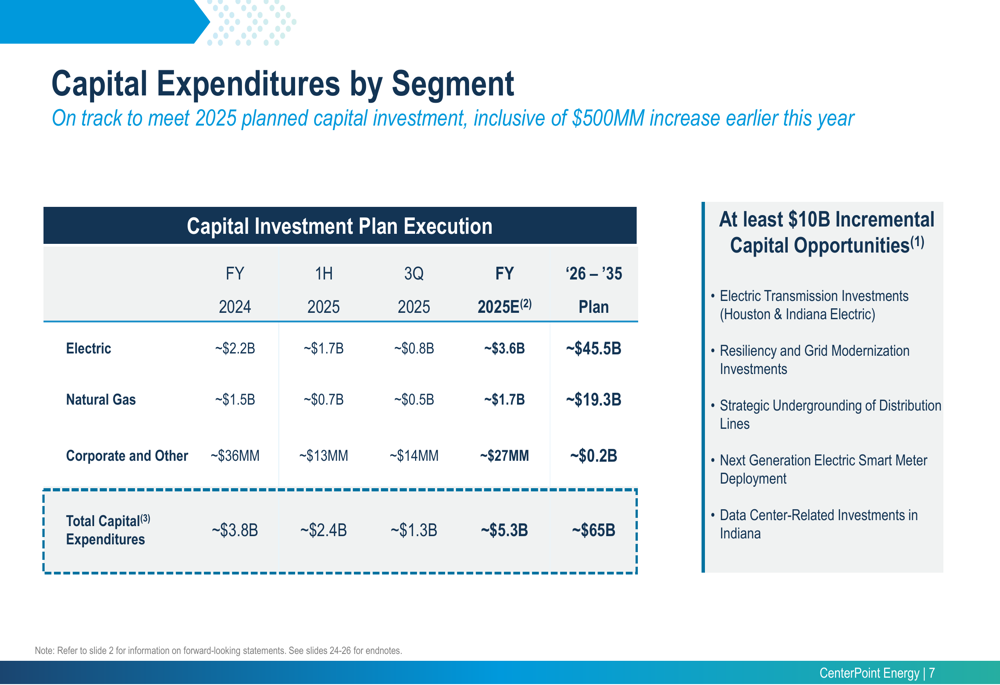

To address this growing demand, CenterPoint has outlined a detailed capital expenditure plan by segment. The electric segment will receive the majority of planned investments, with approximately $45.5 billion allocated through 2035, while natural gas will see approximately $19.3 billion in investments.

The capital plan breakdown is presented in this table:

The company has identified at least $10 billion in incremental capital opportunities beyond the base $65 billion plan, including electric transmission investments, resiliency and grid modernization initiatives, strategic undergrounding of distribution lines, next-generation electric smart meter deployment, and data center-related investments in Indiana.

Financial Position and Outlook

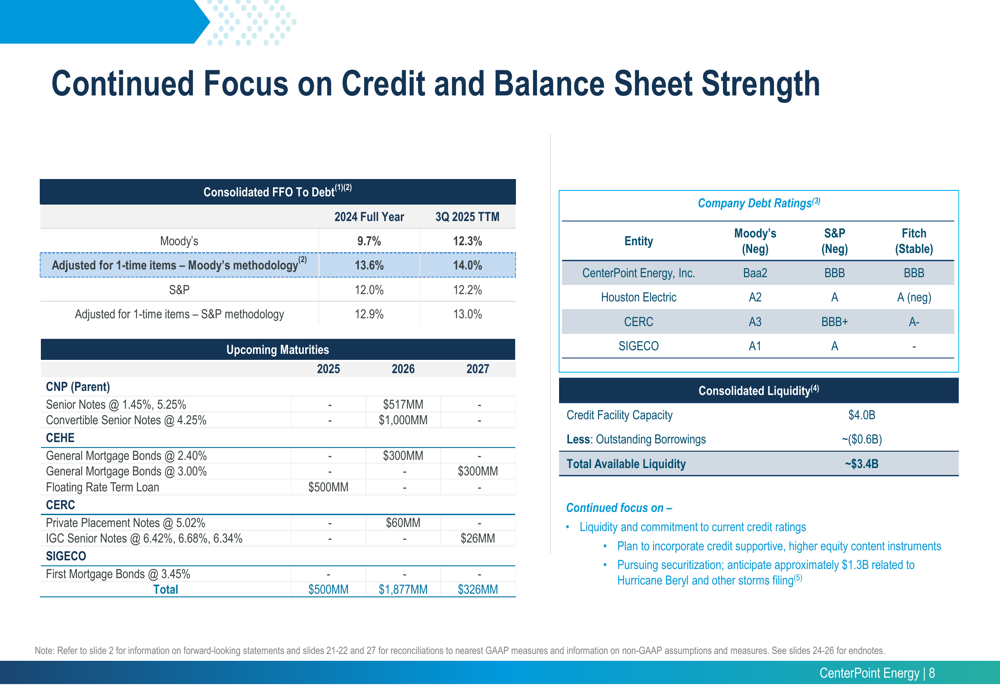

CenterPoint emphasized its commitment to maintaining balance sheet strength throughout the execution of its ambitious capital plan. The company reported a trailing twelve-month FFO to Debt ratio of 14.0% (adjusted, using Moody’s methodology) as of Q3 2025, providing a cushion above rating agency thresholds.

The company’s debt ratings remain solid across all major agencies, with investment-grade ratings from Moody’s, S&P, and Fitch:

Management plans to fund the $65 billion capital plan primarily through operating cash flow (65% of investments) and aims to efficiently finance the remainder through asset recycling, securitization proceeds, and approximately $4 billion of common equity through 2035, with about $3 billion planned for 2028-2035.

To maintain affordability for customers amid significant infrastructure investments, CenterPoint is targeting 1-2% annual O&M reductions on average through 2035, extending cost recovery mechanisms, and leveraging robust annual customer growth.

The company’s investment plan is designed to deliver three primary outcomes: supporting economic growth (~$24 billion), enhancing resiliency and reliability (~$21 billion), and improving customer experience (~$20 billion).

As illustrated in this investment allocation chart:

With its strong quarterly performance, strategic asset recycling through the Ohio Gas sale, and comprehensive long-term capital plan, CenterPoint appears well-positioned to capitalize on the significant growth in energy demand across its service territories while delivering consistent financial returns to investors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.