September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

Central Pacific Financial Corp (NYSE:CPF), the parent company of Central Pacific Bank, released its second quarter 2025 earnings presentation on July 25, highlighting improved profitability metrics across its core business. The Hawaii-based bank, which was founded in 1954 by Japanese-American veterans of World War II, operates as the fourth largest financial institution in Hawaii with 27 branches and 55 ATMs.

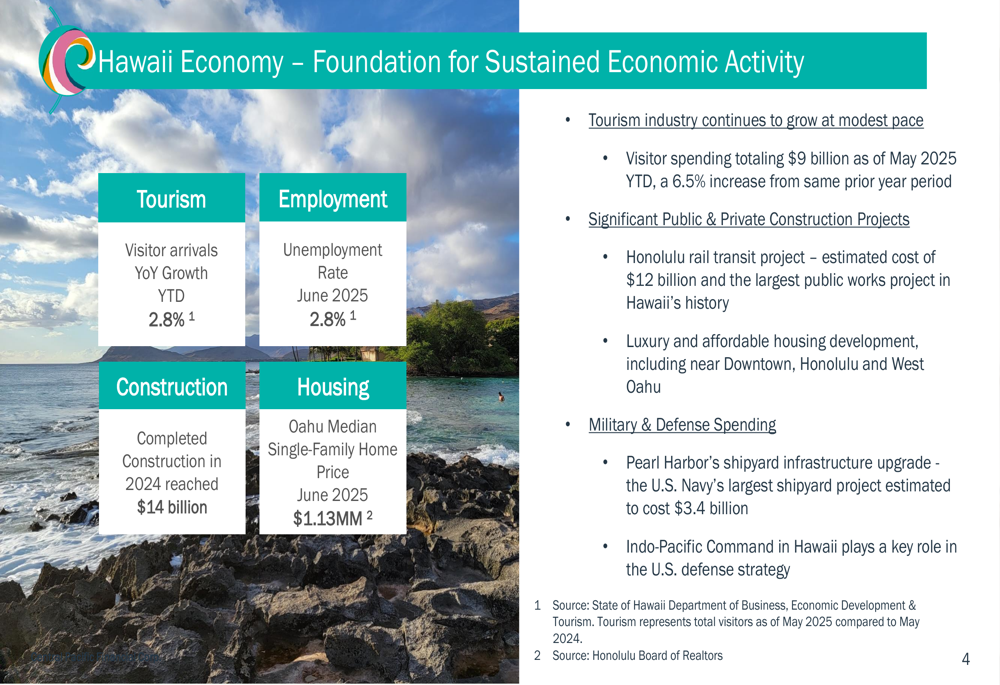

The company’s performance is supported by Hawaii’s stable economic environment, which features a low unemployment rate of 2.8% and continued growth in tourism, with visitor arrivals increasing 2.8% year-over-year year-to-date. The real estate market remains robust with the median single-family home price on Oahu reaching $1.13 million in June 2025.

As shown in the following chart of Hawaii’s economic indicators, the state’s economy provides a solid foundation for sustained banking activity:

Quarterly Performance Highlights

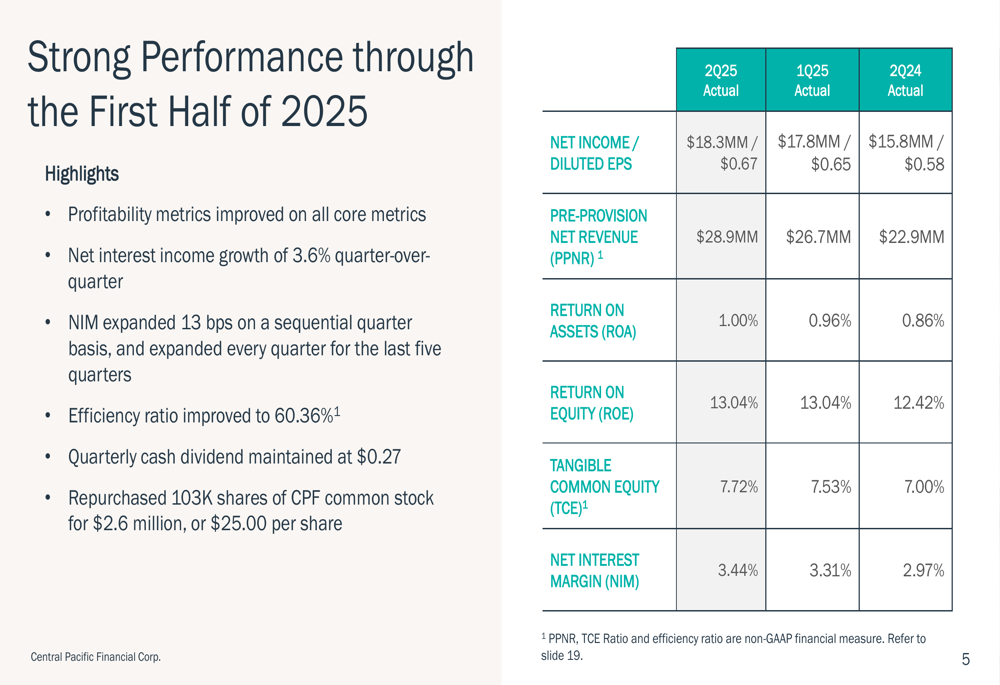

Central Pacific Financial reported net income of $18.3 million or $0.67 per diluted share for Q2 2025, an improvement from $17.8 million or $0.65 per diluted share in the previous quarter. This performance was driven by a 3.6% quarter-over-quarter increase in net interest income and continued expansion of the net interest margin (NIM) to 3.44%, up 13 basis points sequentially.

The company’s efficiency ratio improved to 60.36% from 61.16% in the previous quarter, reflecting effective expense management. CPF maintained its quarterly cash dividend of $0.27 per share and repurchased 103,000 shares of common stock for $2.6 million at an average price of $25.00 per share.

The following table illustrates CPF’s strong financial performance through the first half of 2025:

Loan and Deposit Portfolio Analysis

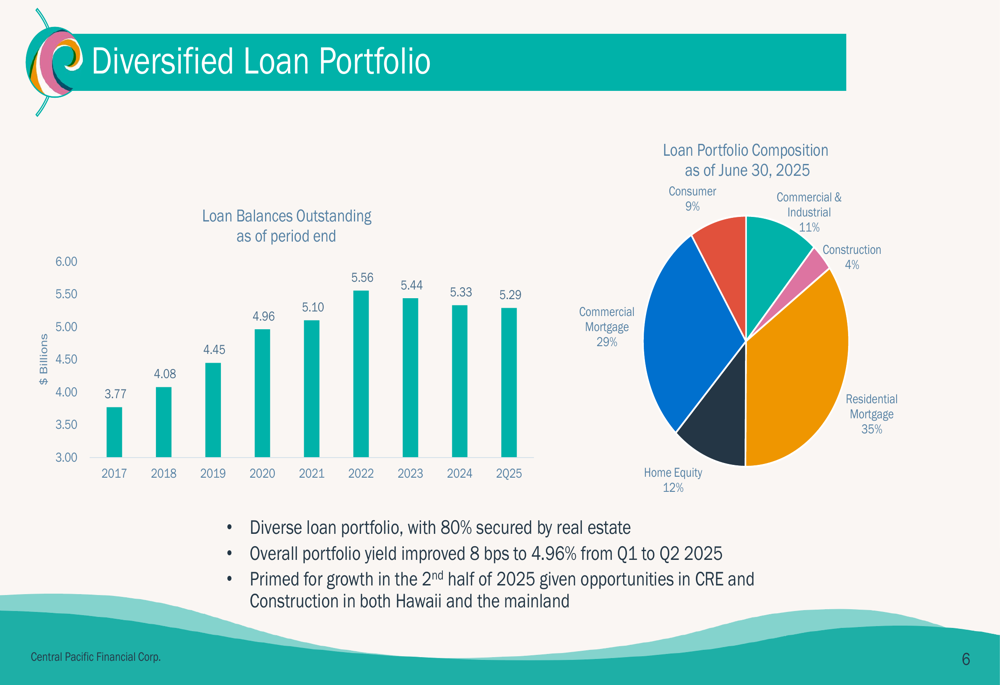

As of June 30, 2025, CPF’s loan portfolio stood at $5.29 billion, with 80% secured by real estate. The portfolio is well-diversified across commercial mortgage (29%), residential mortgage (35%), home equity (12%), commercial and industrial (11%), consumer (9%), and construction (4%) segments. The overall portfolio yield improved 8 basis points to 4.96% from Q1 to Q2 2025.

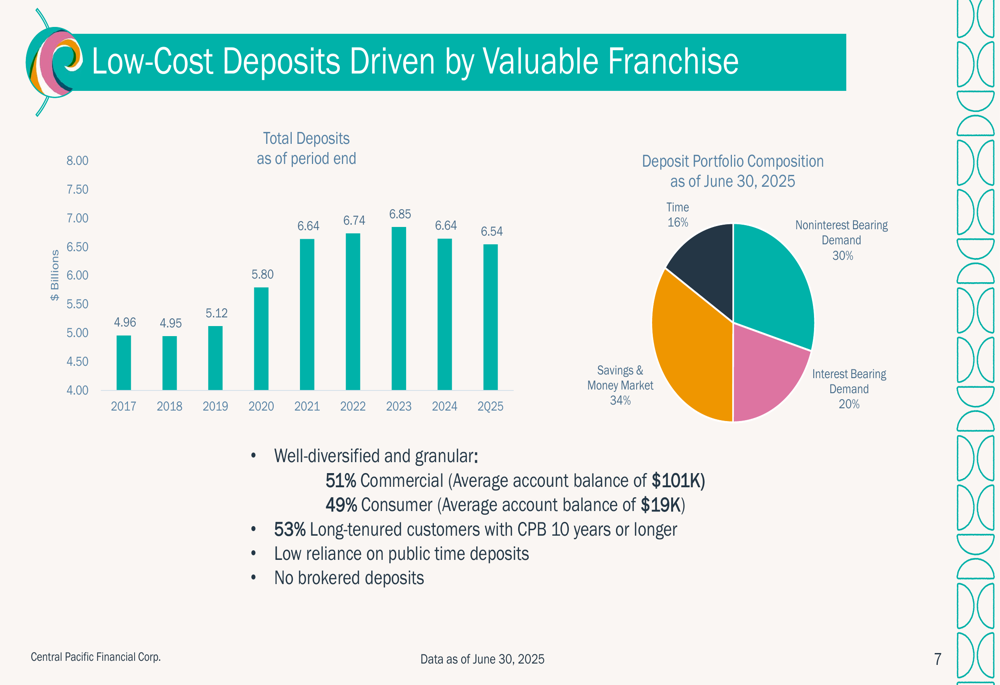

The company’s deposit base totaled $6.54 billion, with a favorable mix of 30% non-interest bearing demand deposits, 34% savings and money market accounts, 20% interest-bearing demand deposits, and 16% time deposits. The total deposit cost declined 6 basis points to 1.02% from Q1 to Q2 2025, demonstrating the bank’s ability to manage funding costs effectively.

The following charts show CPF’s diversified loan portfolio composition and deposit structure:

Central Pacific maintains a competitive advantage in deposit costs compared to both Hawaii and national peers. The company’s net interest margin of 3.44% in Q2 2025 outperformed Hawaii peers (2.69% as of Q1 2025) while approaching the level of national peers (3.41% as of Q1 2025). This advantage is partly due to CPF’s strong non-interest bearing deposit base, which represents 29.6% of total deposits.

Credit Quality and Capital Position

While overall performance was strong, the company’s credit quality metrics showed some signs of pressure. Criticized loans increased to 1.80% of total loans in Q2 2025, up from 0.82% in the previous quarter. Non-performing assets to total loans rose slightly to 0.28% from 0.21%, and annualized net charge-offs increased to 0.35% from 0.20% in Q1 2025.

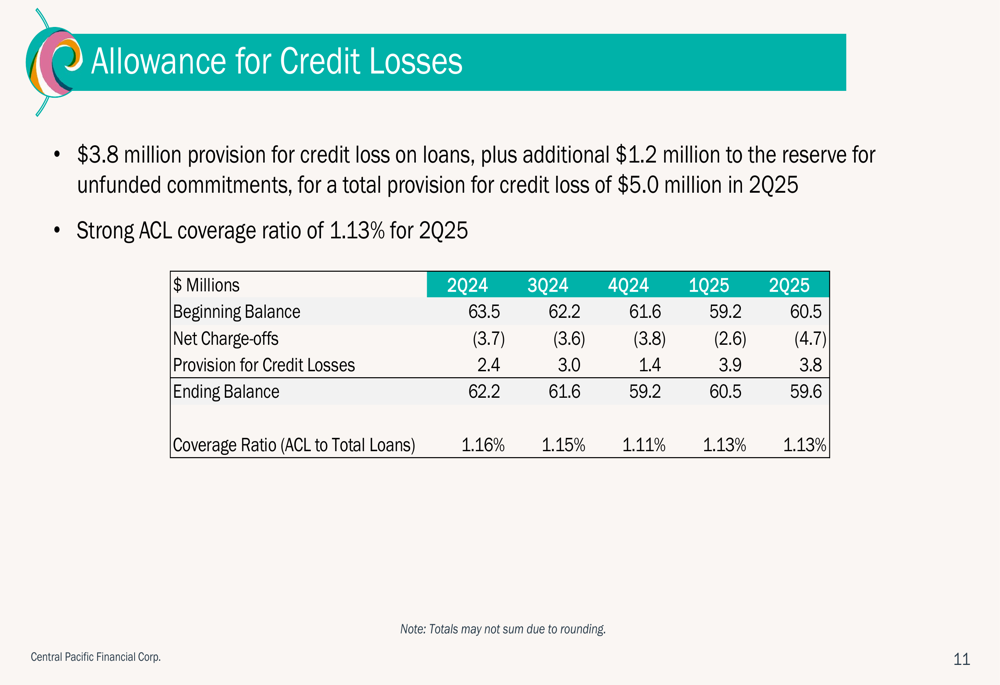

In response to these trends, CPF recorded a $3.8 million provision for credit losses on loans plus an additional $1.2 million to the reserve for unfunded commitments, for a total provision of $5.0 million in Q2 2025. The allowance for credit losses maintained a solid coverage ratio of 1.13%.

The following chart details the company’s allowance for credit losses:

Central Pacific maintains strong capital ratios well above regulatory minimums, with ample liquidity sources totaling $2.82 billion as of June 30, 2025. This includes $317 million in cash, $572 million in unpledged securities, and $1.63 billion in available FHLB borrowing capacity.

Strategic Initiatives and Recognition

CPF continues to focus on three foundational principles: supporting small businesses, promoting home ownership, and bridging Hawaii and Japan. The bank was named the #1 bank for small businesses in Hawaii and recognized as an SBA (LON:SBA) Lender of the Year. It is actively involved in 20 new home projects and has established key alliances in Japan.

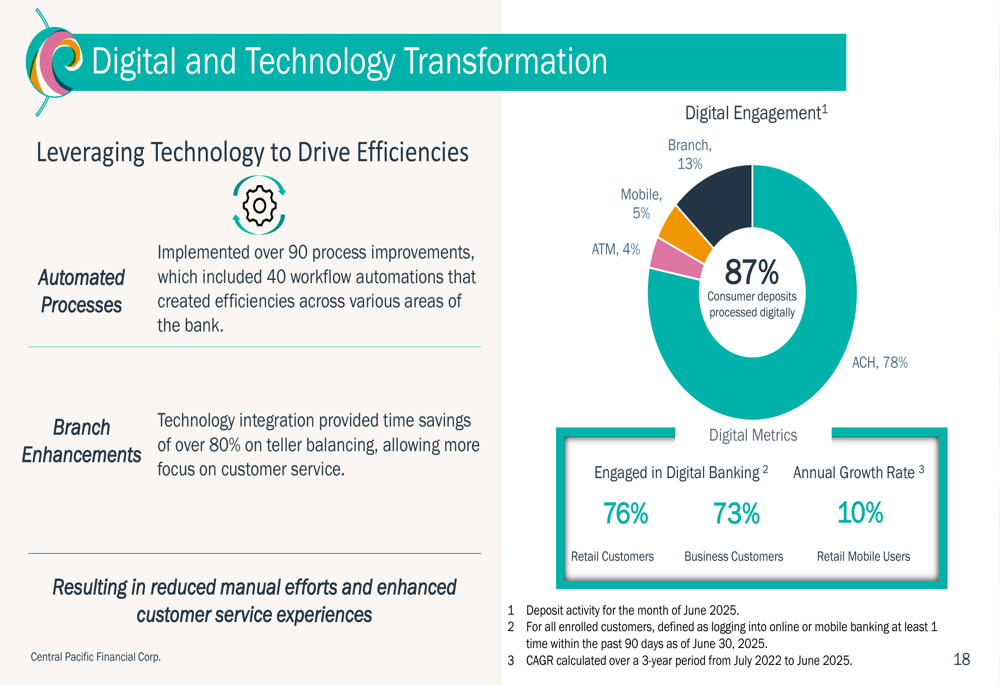

The company is also making significant progress in its digital transformation efforts, with 87% of consumer deposits processed digitally and high digital banking engagement rates of 76% for retail customers and 73% for business customers. Retail mobile users are growing at an annual rate of 10%.

As shown in the following chart of digital banking adoption:

Central Pacific Bank’s strong performance and customer service have earned it recognition as the Best Bank in Hawaii by multiple publications, including Forbes Magazine, Newsweek, and the Honolulu Star-Advertiser:

Forward-Looking Statements

Looking ahead, CPF is positioned for growth in the second half of 2025, particularly in commercial real estate and construction lending in both Hawaii and the mainland. The company’s strong capital position, ample liquidity, and efficient operations provide a solid foundation for continued expansion.

Management remains focused on managing deposit costs, growing core deposits, and optimizing the loan portfolio mix to maintain NIM expansion. While credit quality metrics bear watching, the company’s strong allowance coverage and disciplined underwriting should help mitigate potential risks.

The Hawaii economy’s stability, with its low unemployment rate and steady tourism growth, provides a favorable operating environment for Central Pacific Financial as it continues to execute its strategic initiatives focused on small business, home ownership, and Japan-Hawaii connections.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.