Texas Roadhouse earnings missed by $0.05, revenue topped estimates

Introduction & Market Context

Cerence Inc (NASDAQ:CRNC), a leader in AI-powered automotive assistants, reported its third-quarter fiscal 2025 results on August 6, 2025, exceeding guidance across all key metrics despite year-over-year revenue declines. The company’s shares closed at $8.55, up 0.35% for the day, with a modest 1.05% gain in after-hours trading, suggesting a measured market response to the results.

Following a strong second quarter that saw revenue of $78 million and triggered a 5.64% stock price increase, Cerence’s Q3 performance reflects a sequential revenue decline but demonstrates operational improvements and strong cash generation that may signal stabilization in the company’s business model.

Quarterly Performance Highlights

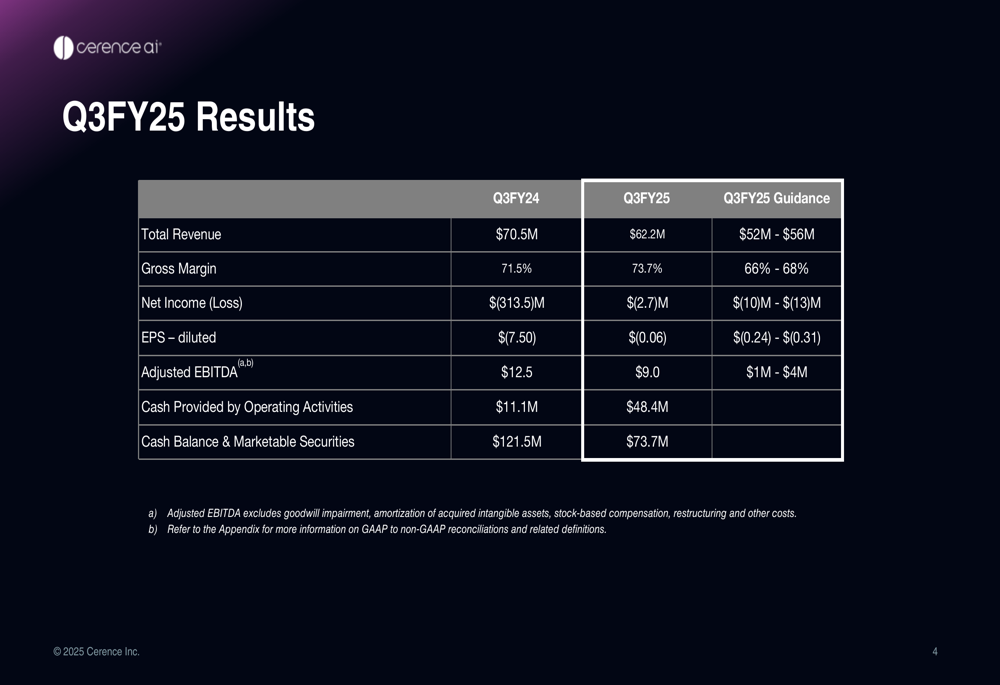

Cerence reported Q3 FY25 revenue of $62.2 million, down from $70.5 million in the same period last year but significantly exceeding the company’s guidance range of $52-56 million. Net loss narrowed dramatically to $2.7 million compared to a $313.5 million loss in Q3 FY24, translating to a diluted EPS of $(0.06) versus $(7.50) in the prior year.

As shown in the following quarterly results comparison:

Notably, gross margin improved to 73.7% from 71.5% in the prior year, exceeding guidance of 66-68%. Adjusted EBITDA reached $9.0 million, down from $12.5 million year-over-year but substantially above the guided range of $1-4 million. Perhaps most impressive was the company’s cash provided by operating activities, which surged to $48.4 million compared to $11.1 million in Q3 FY24.

Detailed Financial Analysis

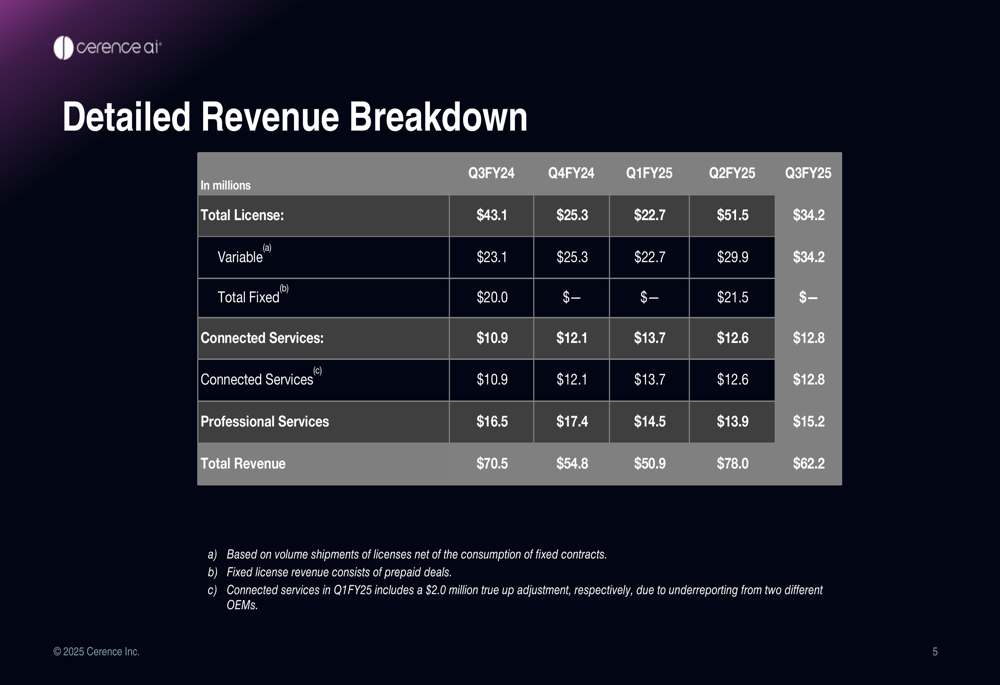

A deeper examination of Cerence’s revenue streams reveals shifting dynamics across its business segments. Variable license revenue has shown consistent sequential growth, reaching $34.2 million in Q3 FY25, while fixed license revenue has become more sporadic.

The following revenue breakdown illustrates these trends across recent quarters:

Connected services revenue remained relatively stable at $12.8 million, while professional services revenue showed modest sequential growth to $15.2 million. The company’s total revenue of $62.2 million represents a sequential decline from Q2’s $78.0 million, which had benefited from a significant fixed license component of $21.5 million.

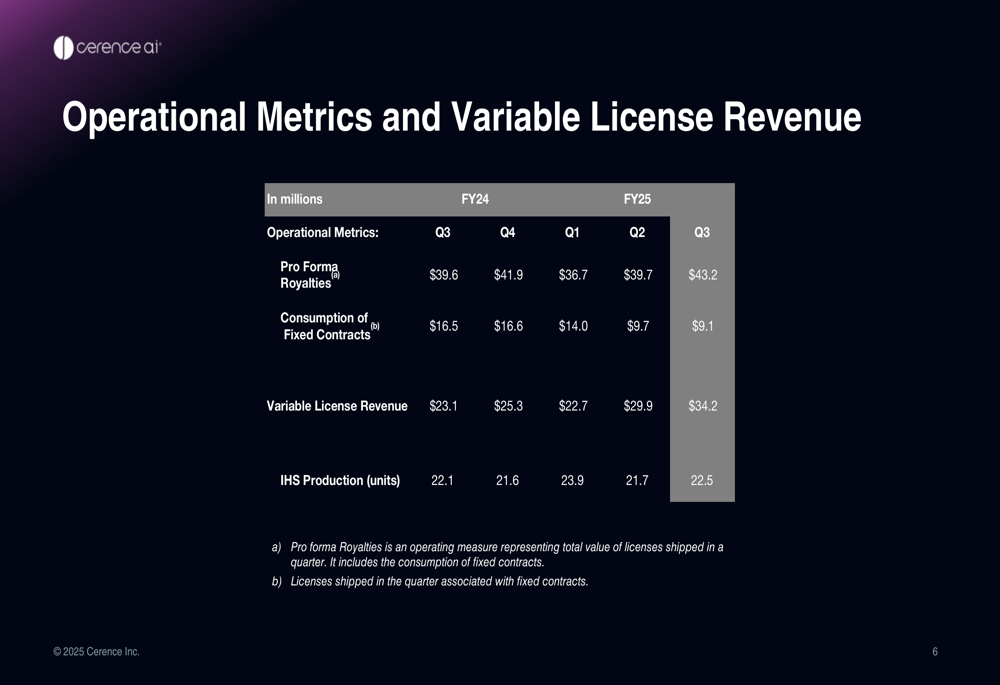

Operational metrics reveal positive underlying trends despite the revenue fluctuations:

Pro forma royalties increased to $43.2 million in Q3 FY25, showing sequential growth from $39.7 million in Q2 and year-over-year growth from $39.6 million in Q3 FY24. This metric, which represents the theoretical royalty value if all vehicles were on variable contracts, suggests strengthening fundamentals in Cerence’s core business.

Strategic Initiatives

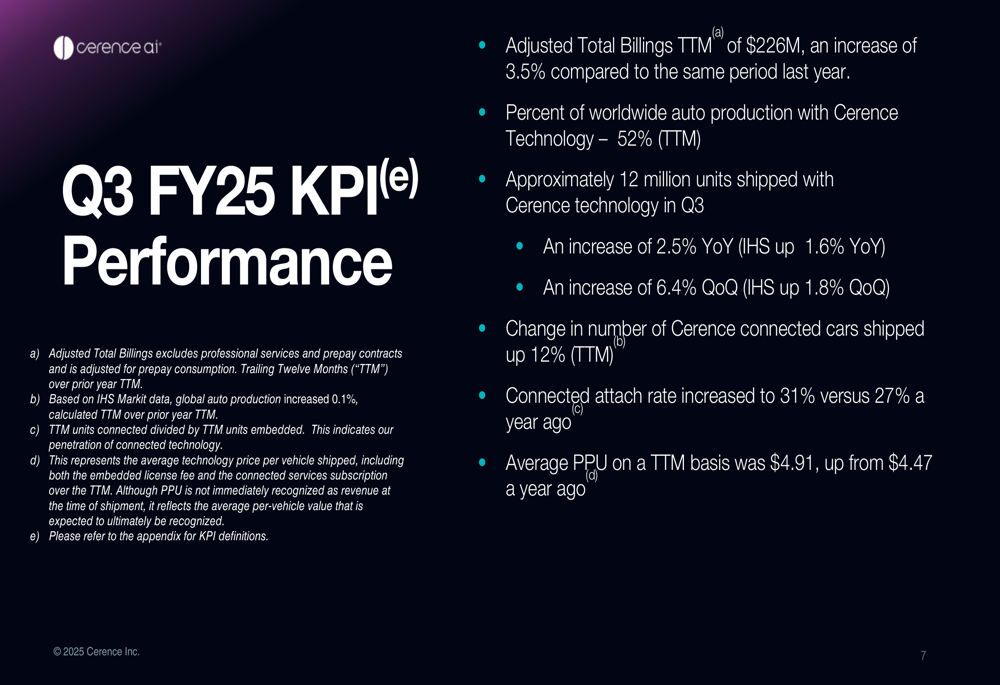

Cerence continues to expand its market penetration while increasing the value of its technology per vehicle. Key performance indicators highlight the company’s strategic progress:

The company now powers technology in 52% of worldwide auto production on a trailing twelve-month basis. Approximately 12 million vehicles shipped with Cerence technology in Q3, representing a 2.5% year-over-year increase, outpacing the broader auto industry’s 1.6% growth.

Particularly encouraging is the connected attach rate, which increased to 31% from 27% a year ago, indicating growing adoption of Cerence’s higher-value connected services. This shift is reflected in the average price per unit (PPU), which rose to $4.91 from $4.47 a year ago on a TTM basis.

These metrics align with the company’s Q2 earnings call commentary, where CEO Brian Krizanich emphasized that "AI is driving usage of voice in the vehicle across the board," highlighting the strategic importance of AI development in Cerence’s product portfolio.

Forward-Looking Statements

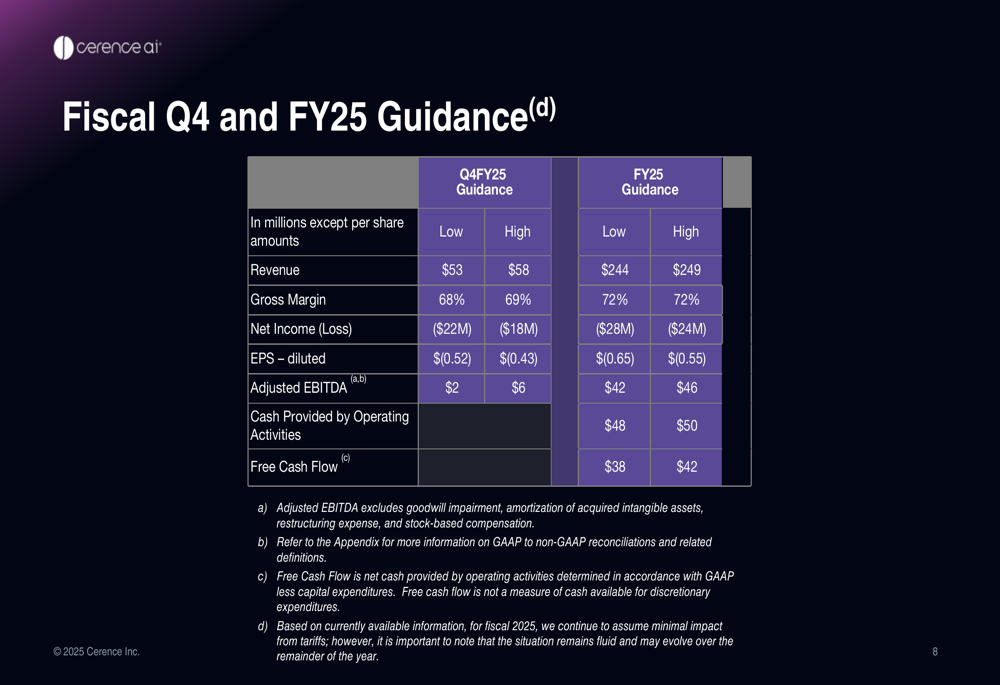

Looking ahead, Cerence provided guidance for both Q4 and the full fiscal year 2025:

For Q4 FY25, the company expects revenue between $53-58 million and adjusted EBITDA of $2-6 million. Full-year FY25 guidance projects revenue of $244-249 million and adjusted EBITDA of $42-46 million.

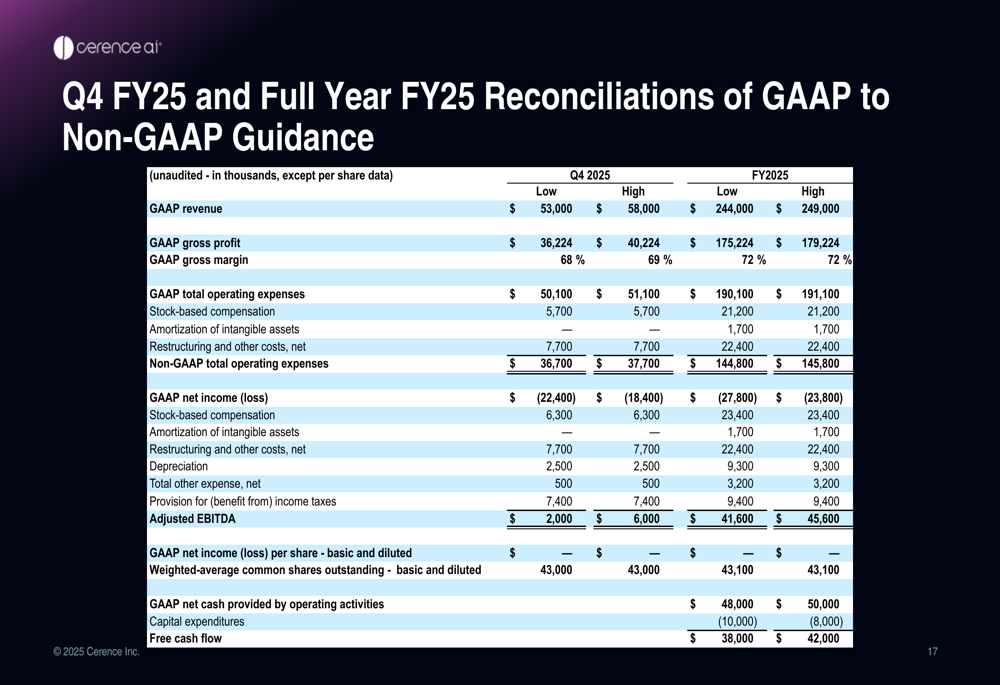

The reconciliation between GAAP and non-GAAP metrics provides additional context for understanding these projections:

Notably, Cerence expects to generate strong cash flow for the full year, with operating cash flow projected at $48-50 million and free cash flow of $38-42 million, demonstrating the company’s ability to maintain financial discipline despite revenue challenges.

Executive Summary

Cerence’s Q3 FY25 results present a mixed picture of year-over-year revenue decline but operational improvements and strong cash generation. The company continues to increase its penetration in the automotive market while shifting toward higher-value connected services, as evidenced by the growing connected attach rate and rising average price per unit.

While the stock’s modest after-hours movement suggests investors remain cautious, the company’s ability to exceed guidance across all metrics and generate substantial cash flow may indicate that Cerence is successfully navigating its business transition. The guidance for Q4 and full-year FY25 suggests continued focus on operational efficiency and cash generation as the company works to stabilize and eventually return to growth.

For investors, the key metrics to watch in coming quarters will be the continued evolution of variable license revenue, connected attach rates, and average PPU, which collectively will determine whether Cerence can translate its strong market position into sustainable financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.