Veeco launches Lumina+ MOCVD system, receives Rocket Lab order

Introduction & Market Context

CGI Inc. (NYSE:GIB) reported strong revenue growth but faced margin pressure in its third quarter fiscal 2025 results, presented on July 30, 2025. The global IT and business consulting services firm achieved double-digit revenue growth while continuing to invest in artificial intelligence capabilities and potential acquisitions, as reflected in its rising debt levels.

The company’s stock has been trading near $99.91, within its 52-week range of $92.85 to $122.79, as investors weigh the company’s growth trajectory against profitability concerns.

Quarterly Performance Highlights

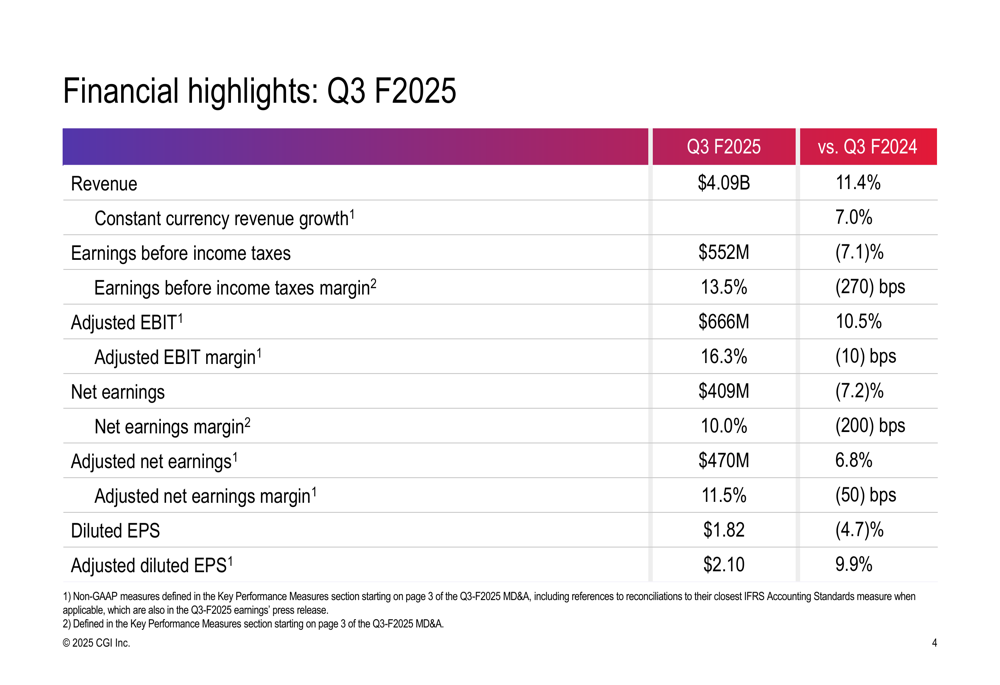

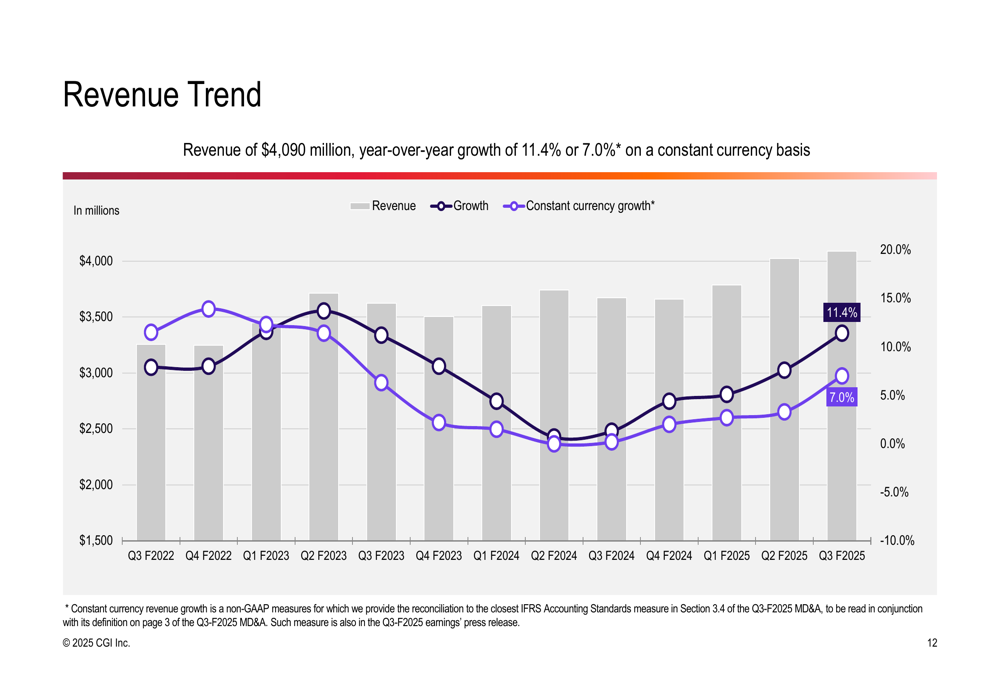

CGI delivered revenue of $4.09 billion in Q3 F2025, representing an 11.4% increase year-over-year, or 7.0% growth in constant currency. This acceleration in growth compared to the 4.4% reported in the previous fiscal year suggests the company’s strategic investments may be gaining traction.

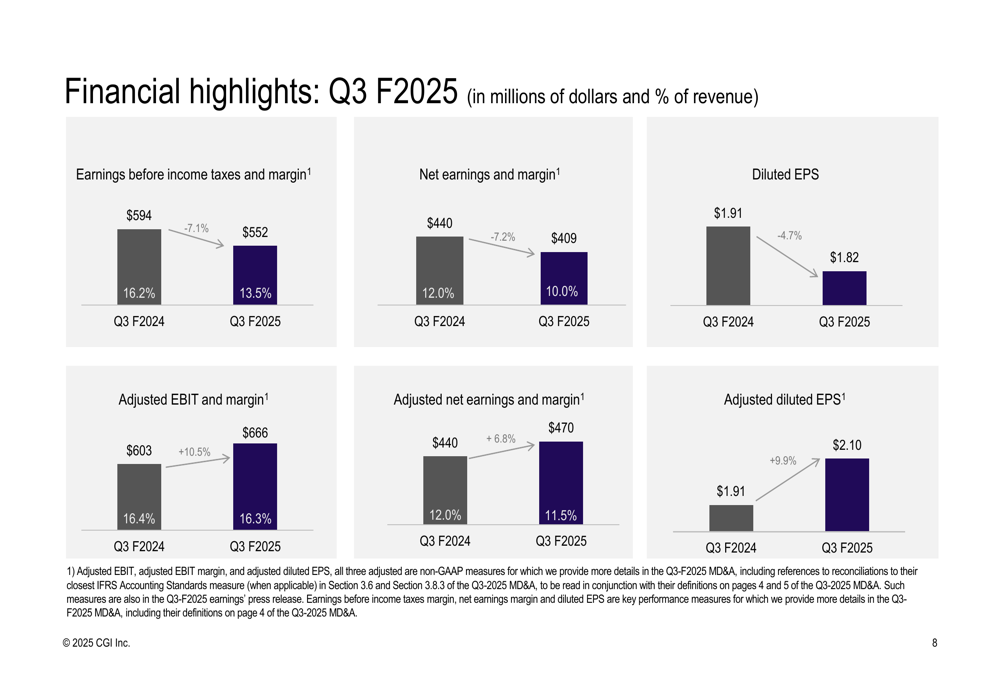

However, profitability metrics showed some pressure. Earnings before income taxes declined 7.1% to $552 million, with the corresponding margin contracting 270 basis points to 13.5%. Net earnings fell 7.2% to $409 million, resulting in a 10.0% margin, down 200 basis points from the prior year.

As shown in the following financial highlights table:

On an adjusted basis, the picture was more positive. Adjusted EBIT grew 10.5% to $666 million, with only a slight margin contraction of 10 basis points to 16.3%. Similarly, adjusted net earnings increased 6.8% to $470 million, while adjusted diluted EPS rose 9.9% to $2.10.

The visual comparison of these key metrics illustrates the mixed performance:

Geographic and Segment Analysis

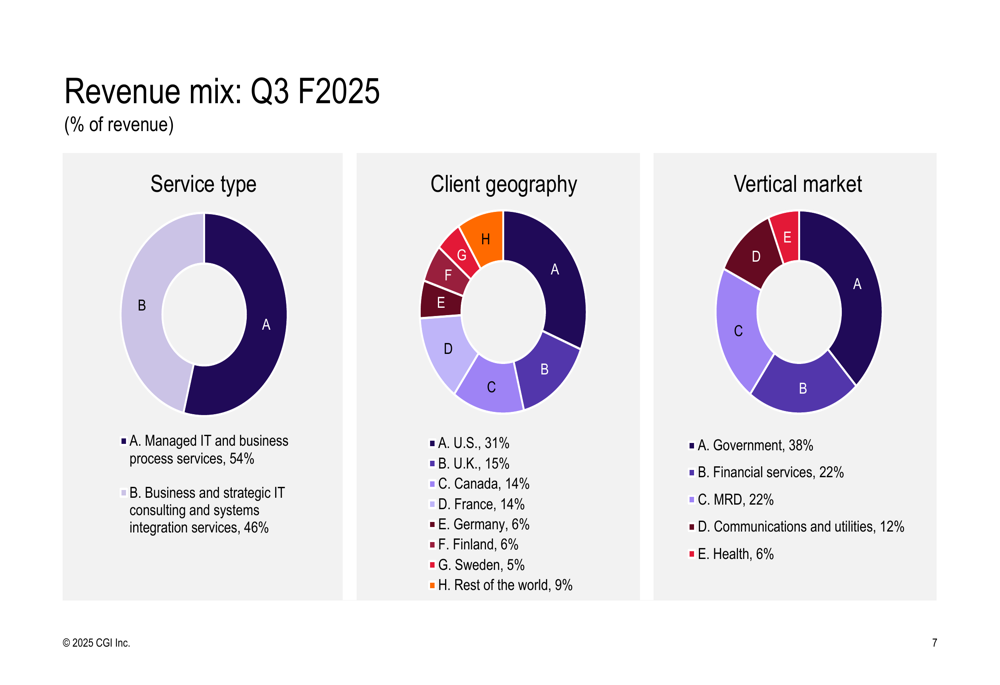

CGI’s revenue is well-diversified across geographies and industry verticals. The United States represents the largest market at 31% of revenue, followed by the United Kingdom (TADAWUL:4280) (15%), Canada (14%), and France (14%). From an industry perspective, government contracts dominate at 38% of revenue, with financial services and manufacturing, retail & distribution (MRD) each contributing 22%.

The company’s service mix is balanced between managed IT and business process services (54%) and business consulting and systems integration (46%), as illustrated in these revenue breakdowns:

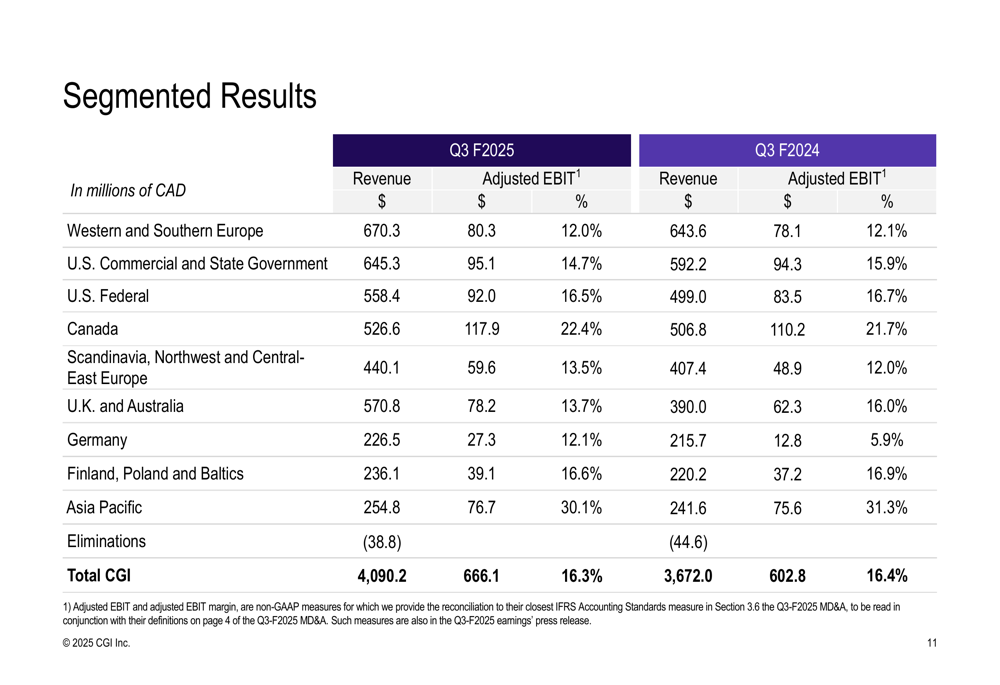

Performance varied significantly across geographic segments. The detailed segmented results show the revenue and adjusted EBIT margins for each region:

Strategic Initiatives

CGI’s CEO highlighted the company’s double-digit revenue growth and momentum in AI-related initiatives. This aligns with the company’s previously announced $1 billion investment in AI and generative AI capabilities, as mentioned in their fiscal 2024 earnings.

The company maintains a global workforce of 93,000 consultants and professionals, with 64% in client proximity roles, 13% in nearshore or onshore delivery centers, and 23% in global delivery centers including India, Philippines, and Morocco. Notably, 88% of employees are shareholders through the company’s Share Purchase Plan, which may contribute to alignment with corporate objectives.

Bookings and Future Outlook

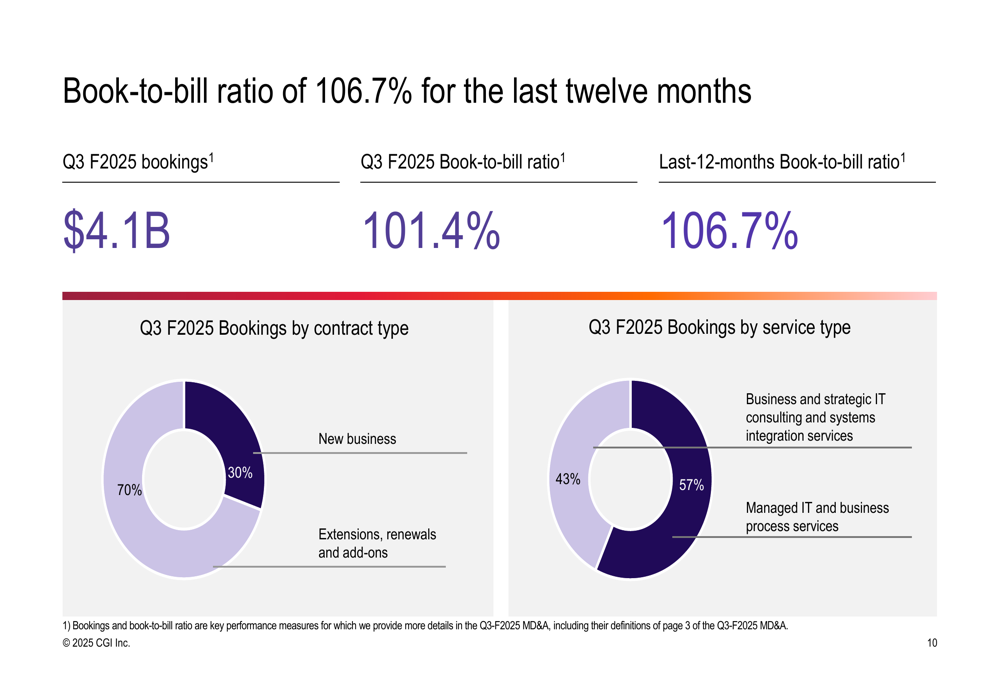

CGI’s book-to-bill ratio of 101.4% for Q3 F2025 and 106.7% for the last twelve months suggests continued growth momentum. The company secured $4.1 billion in new bookings during the quarter, with 70% coming from extensions, renewals, and add-ons, while 30% represented new business.

The breakdown of bookings by service type closely mirrors the current revenue mix, with 57% in managed services and 43% in consulting and systems integration:

The company’s revenue trend over recent quarters shows consistent growth acceleration, particularly in the most recent period:

Balance Sheet and Cash Flow

While CGI continues to generate solid cash flow, with $487 million from operations in Q3 (11.9% of revenue), the company’s debt levels have increased significantly. Long-term debt and lease liabilities reached $4.24 billion, up $1.20 billion from the same period last year.

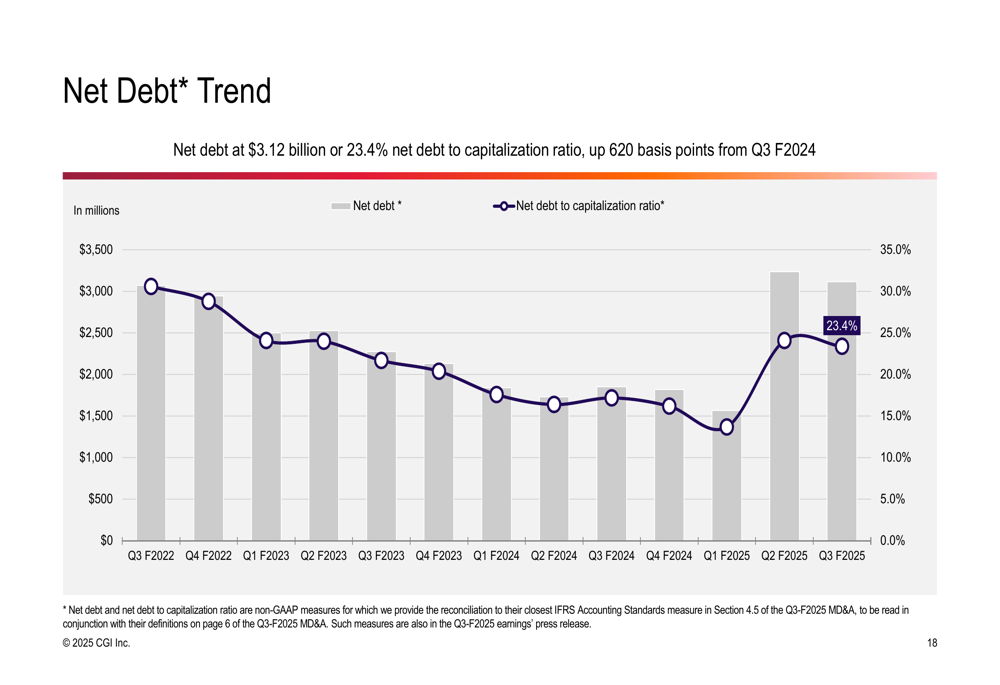

Net debt stood at $3.12 billion, resulting in a net debt to capitalization ratio of 23.4%, an increase of 620 basis points year-over-year. This rising leverage likely reflects CGI’s acquisition strategy and investments in AI capabilities.

The following chart illustrates the net debt trend:

Adjusted EBIT Performance

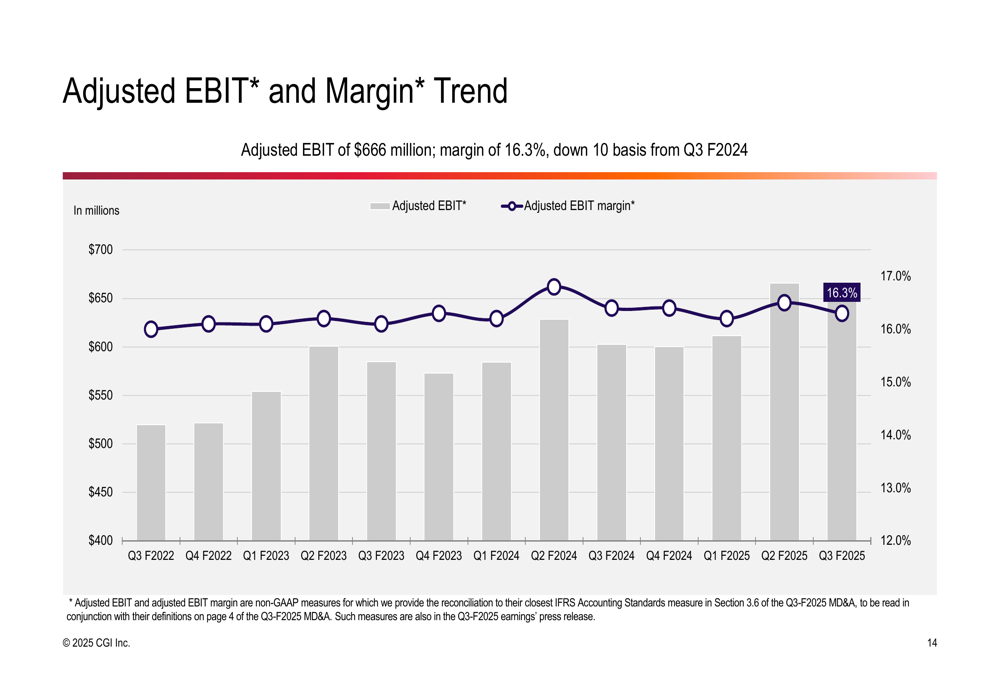

Despite margin pressures in some metrics, CGI’s adjusted EBIT showed positive growth, reaching $666 million with a 16.3% margin. While this represents a slight margin contraction of 10 basis points from Q3 F2024, the absolute growth of 10.5% demonstrates the company’s ability to scale its operations.

The trend in adjusted EBIT and margin over recent quarters is shown below:

Earnings Performance

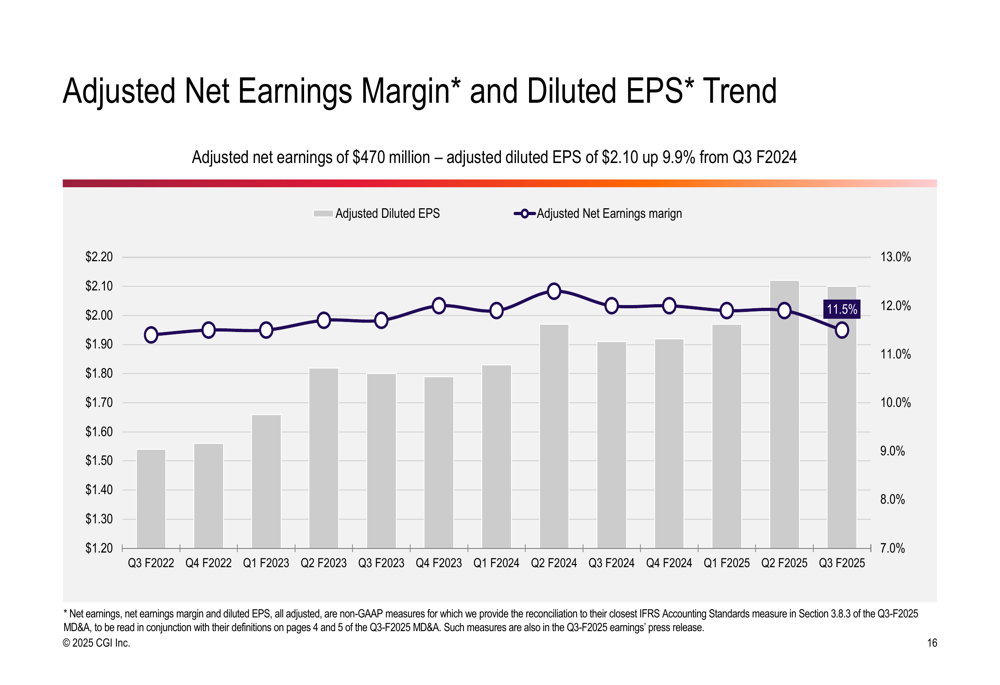

On an adjusted basis, CGI’s earnings performance was stronger than the GAAP results would suggest. Adjusted net earnings grew 6.8% to $470 million, while adjusted diluted EPS increased 9.9% to $2.10. This discrepancy between GAAP and adjusted results may reflect integration costs, acquisition expenses, or other one-time items.

The trend in adjusted net earnings and adjusted diluted EPS is illustrated here:

Forward-Looking Statements

CGI’s Q3 F2025 presentation suggests the company is in an investment phase, with strong revenue growth but some margin pressure as it expands capabilities and integrates acquisitions. The solid book-to-bill ratio indicates healthy demand for CGI’s services, particularly in AI and digital transformation.

The rising debt levels bear monitoring but appear to be part of a deliberate strategy to fund growth initiatives and acquisitions. As these investments mature, investors will likely look for margin improvement and accelerated earnings growth in coming quarters.

With a diversified geographic and industry footprint, CGI appears well-positioned to navigate varying market conditions while continuing to execute on its long-term growth strategy centered around digital transformation and AI capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.