Diamyd Medical’s phase 3 diabetes trial passes final safety review

Introduction & Market Context

Cisco Systems Inc. (NASDAQ:CSCO) reported strong financial results for its fourth quarter of fiscal year 2025, exceeding analyst expectations despite challenging market conditions. The networking giant posted revenue of $14.7 billion, up 8% year-over-year, and non-GAAP earnings per share of $0.99, representing a 14% increase compared to the same period last year.

Despite beating expectations, Cisco’s stock experienced a slight decline of 1.37% to $71.38 during regular trading hours on August 13, 2025, though it recovered slightly in after-hours trading, gaining 0.56% to reach $71.78. The stock has been trading near its 52-week high of $72.55, having delivered a 59.13% total return to investors over the past year.

Quarterly Performance Highlights

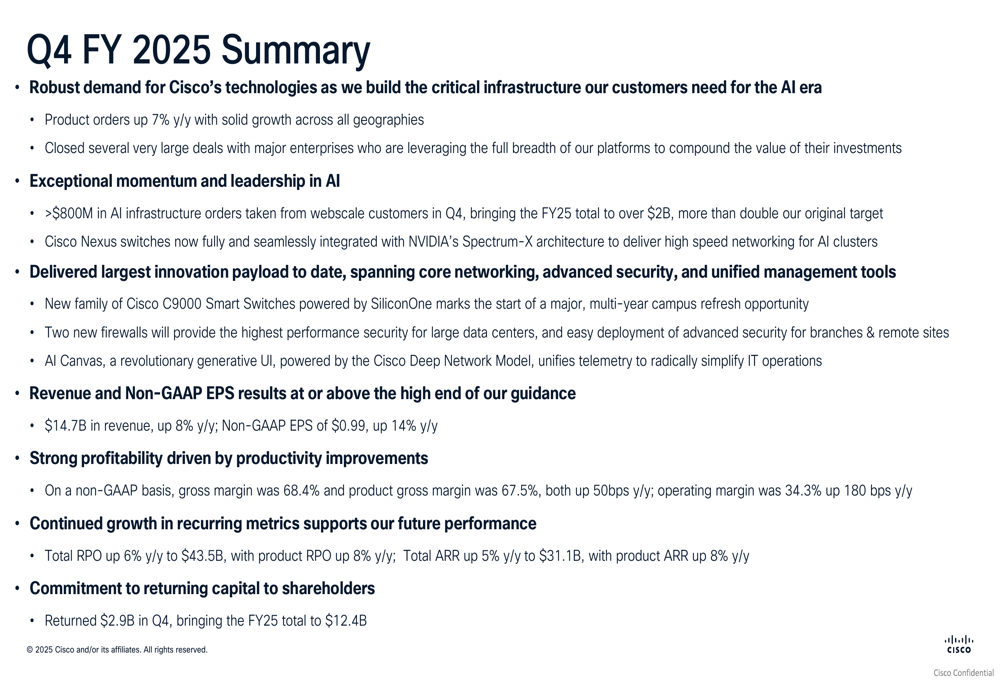

Cisco’s Q4 FY 2025 results demonstrated solid growth across key metrics, with particular strength in its AI-related business segments. The company reported robust demand for its technologies as customers build critical infrastructure for the AI era.

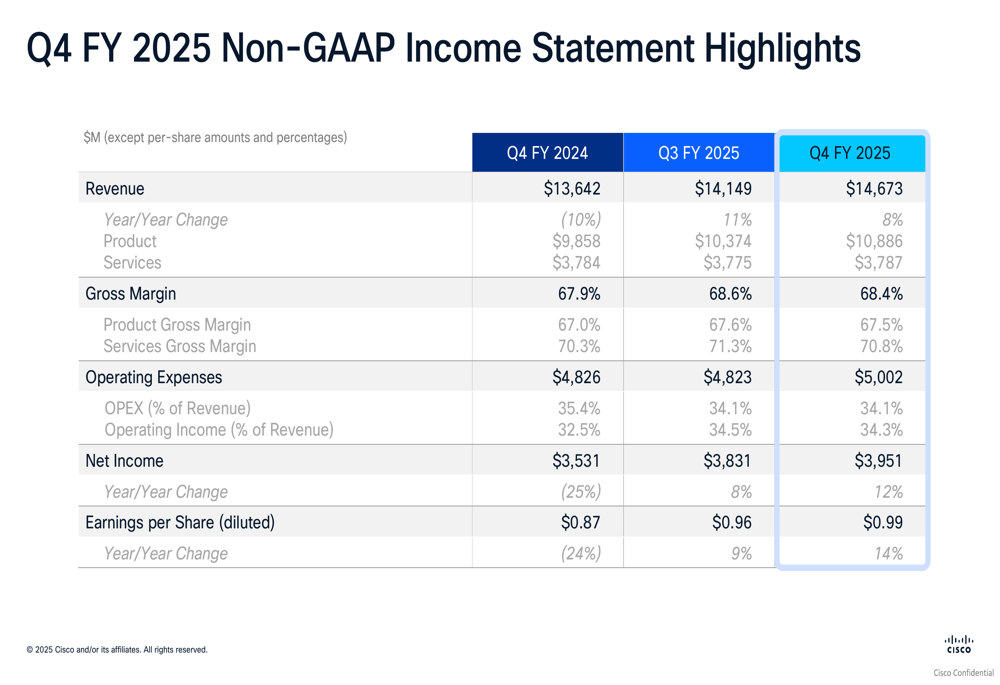

As shown in the following comprehensive summary of Cisco’s quarterly performance:

Product orders grew 7% year-over-year with solid growth across all geographies. The company closed several large deals with major enterprises leveraging Cisco’s full platform portfolio. Revenue and non-GAAP EPS results were at or above the high end of guidance, with non-GAAP gross margin at 68.4% and product gross margin at 67.5%, both up 50 basis points year-over-year.

The company’s profitability metrics showed significant improvement, with non-GAAP operating margin increasing to 34.3%, up 180 basis points year-over-year. This profitability enhancement was driven by productivity improvements across the organization.

AI Strategy and Growth

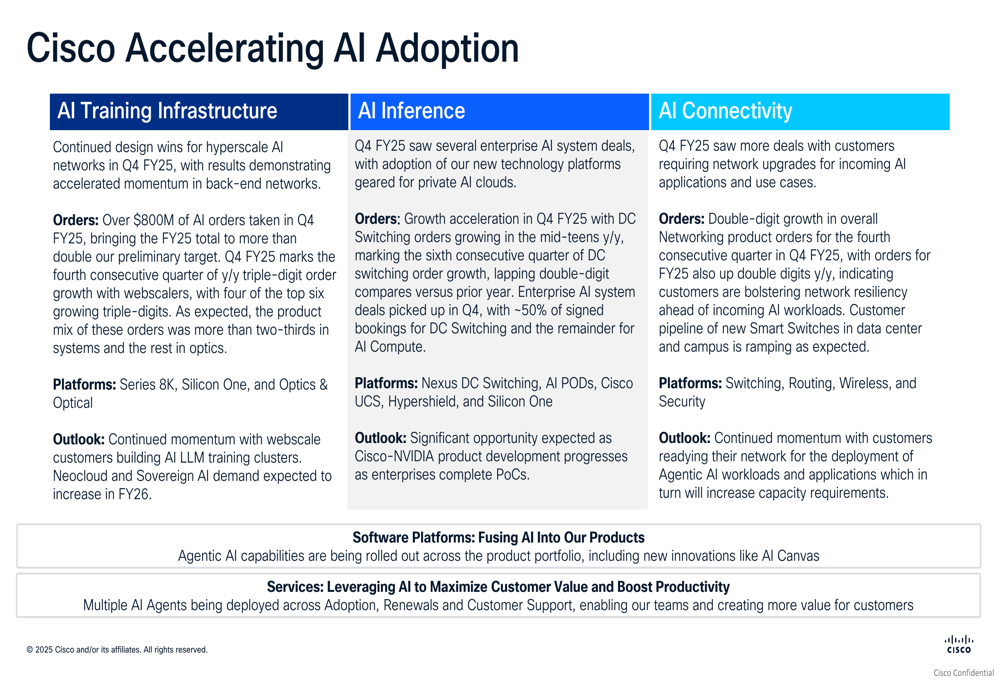

A standout element of Cisco’s quarterly results was its exceptional momentum in AI infrastructure. The company reported over $800 million in AI infrastructure orders from webscale customers in Q4 alone, bringing the fiscal year 2025 total to over $2 billion – more than double its original target.

The following slide illustrates Cisco’s comprehensive approach to accelerating AI adoption across different segments:

Cisco’s AI strategy spans three key areas: AI training infrastructure, AI inference, and AI connectivity. The company has seen triple-digit order growth with webscalers for four consecutive quarters in AI training infrastructure. In AI inference, data center switching orders grew in the mid-teens year-over-year, marking the sixth consecutive quarter of growth in this segment.

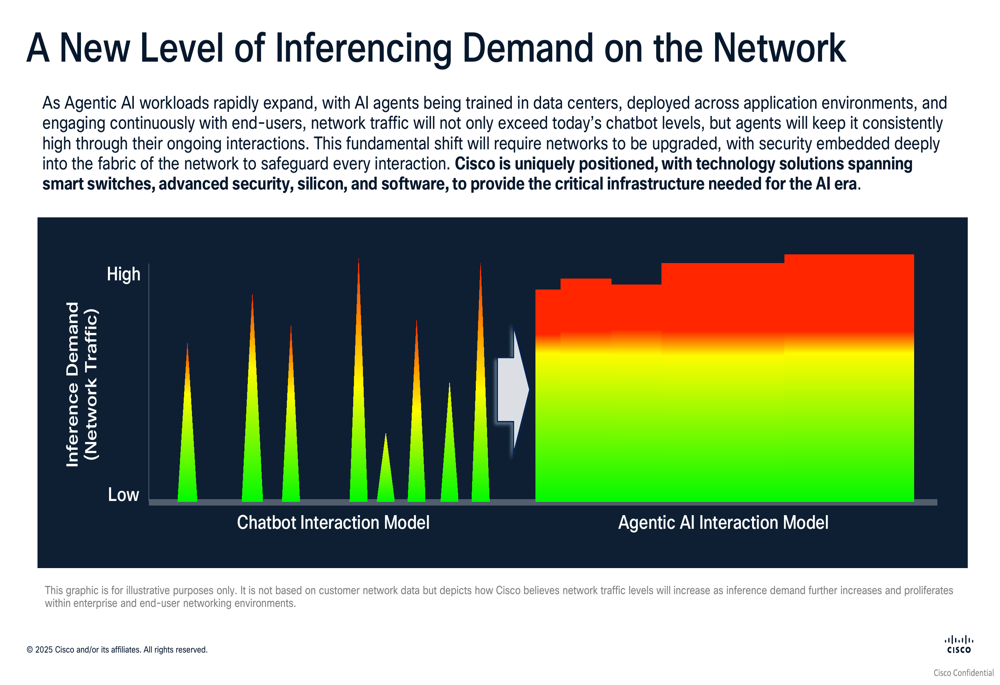

The company is also focusing on the increasing network demands created by agentic AI workloads, as illustrated in this network traffic comparison:

CEO Chuck Robbins emphasized this point during the earnings call, stating: "As we move into the next phase of AI with agents autonomously conducting tasks alongside humans, the capacity requirements of the network will be compounded." This trend is expected to drive further demand for Cisco’s networking solutions.

Detailed Financial Analysis

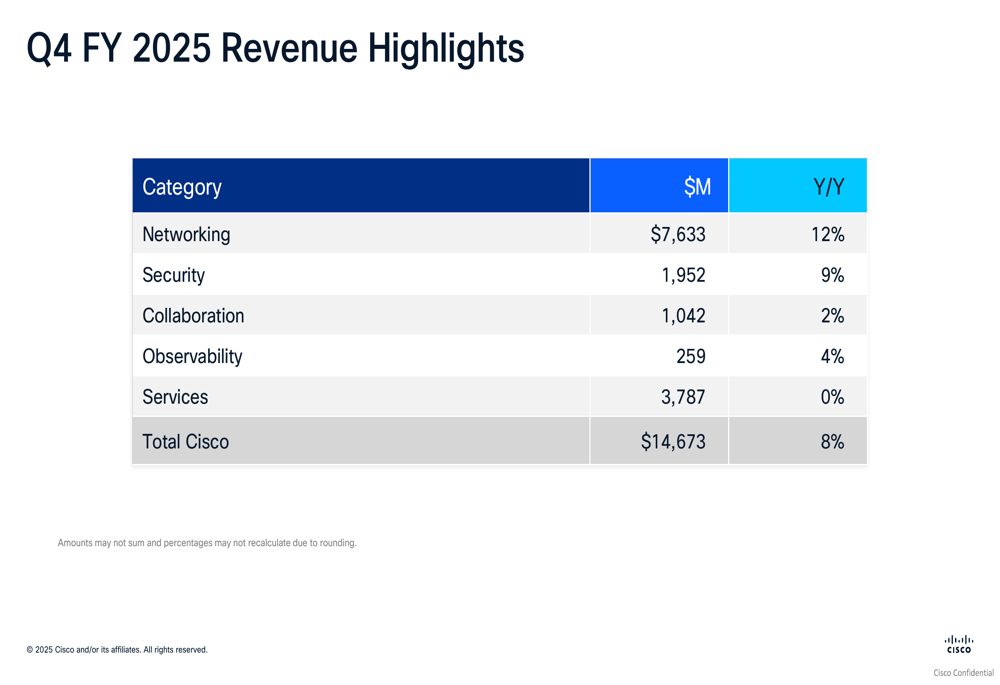

Breaking down Cisco’s Q4 FY 2025 revenue by category reveals strong performance across multiple business segments:

Networking, which represents Cisco’s largest revenue category, grew an impressive 12% year-over-year to $7.63 billion. Security solutions also showed strong growth of 9%, reaching $1.95 billion. Collaboration and Observability segments grew at more modest rates of 2% and 4%, respectively, while Services remained flat compared to the previous year.

The company’s non-GAAP income statement highlights demonstrate solid financial performance:

Revenue increased 8% year-over-year to $14.67 billion, with product revenue of $10.89 billion and services revenue of $3.79 billion. Non-GAAP gross margin was 68.4%, with product gross margin at 67.5% and services gross margin at 70.8%. Operating expenses as a percentage of revenue decreased to 34.1%, resulting in a non-GAAP operating income of 34.3%.

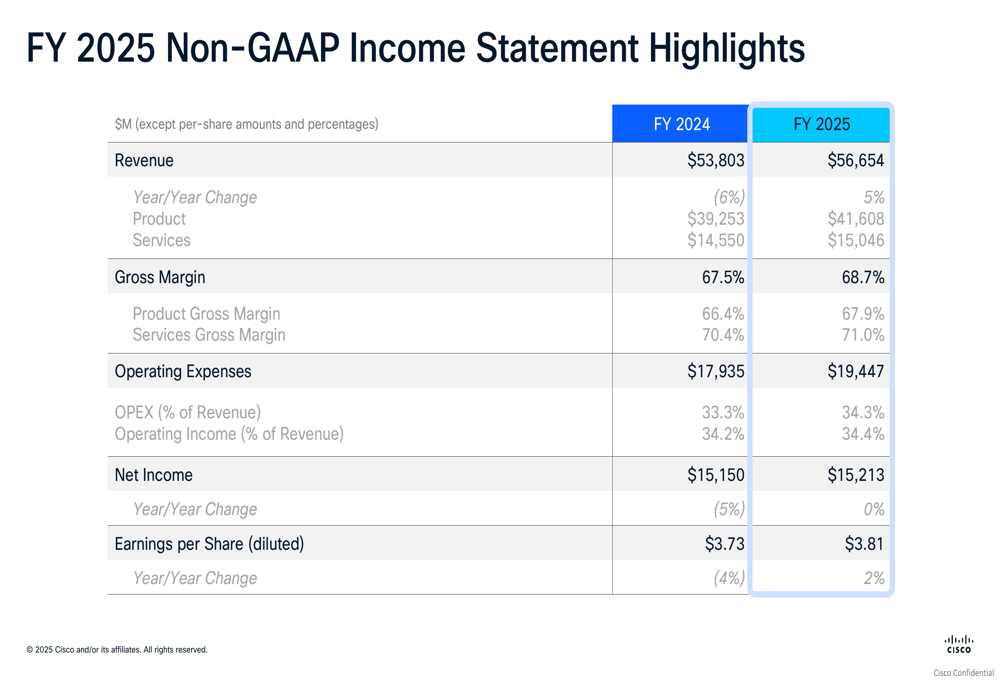

For the full fiscal year 2025, Cisco reported:

Revenue grew 5% year-over-year to $56.65 billion, with non-GAAP EPS increasing 2% to $3.81. The company maintained strong gross margins, with overall non-GAAP gross margin at 68.7% and product gross margin at 67.9%.

Forward Guidance

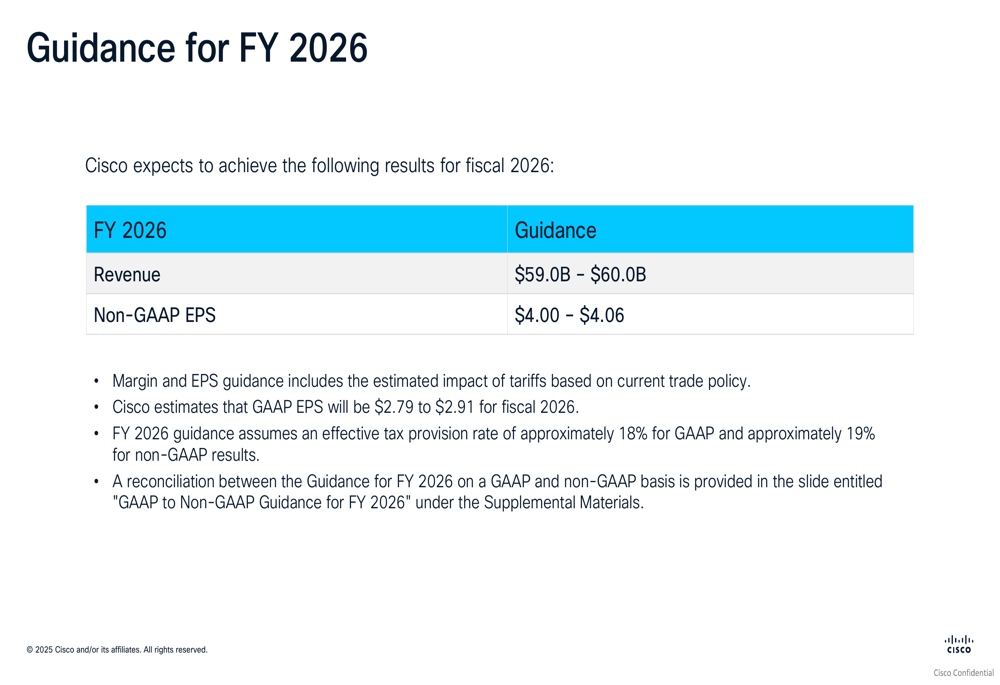

Looking ahead, Cisco provided a positive outlook for fiscal year 2026:

The company expects revenue between $59.0 billion and $60.0 billion for FY 2026, with non-GAAP EPS projected between $4.00 and $4.06. This guidance includes the estimated impact of tariffs based on current trade policy.

For the first quarter of fiscal year 2026, Cisco expects revenue between $14.65 billion and $14.85 billion, with non-GAAP EPS between $0.97 and $0.99. Non-GAAP gross margin is projected to be between 67.5% and 68.5%, with non-GAAP operating margin between 33% and 34%.

Strategic Initiatives

Cisco highlighted several strategic initiatives during its presentation, including significant product innovations. The company delivered what it described as its "largest innovation payload to date," spanning core networking, advanced security, and unified management tools.

Key product announcements included a new family of Cisco C9000 Smart Switches powered by SiliconOne, which marks the start of what the company sees as a major, multi-year campus refresh opportunity. Cisco also introduced two new firewalls designed to provide high-performance security for large data centers and simplified deployment of advanced security for branches and remote sites.

Additionally, the company launched AI Canvas, described as a "revolutionary generative UI" powered by the Cisco Deep Network Model, which unifies telemetry to simplify IT operations.

Cisco’s commitment to returning capital to shareholders remained strong, with $2.9 billion returned in Q4 through dividends and share repurchases, bringing the fiscal year 2025 total to $12.4 billion.

Despite the positive results and outlook, investors should be aware of potential risks including supply chain disruptions, increasing competition in AI and networking markets, macroeconomic conditions affecting enterprise spending, regulatory changes, and rapid technological shifts requiring continuous adaptation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.