Nvidia’s results, Indian tariffs, French markets - what’s moving markets

Introduction & Market Context

Clear Channel Outdoor Holdings Inc (NYSE:CCO) presented its first quarter 2025 financial results on May 1, showing modest revenue growth but declining profitability metrics as the company continues its strategic shift toward U.S. operations. The out-of-home advertising company’s stock has been under pressure, trading at $0.99 in after-market trading following the presentation, near its 52-week low of $0.811.

The company’s presentation comes after a challenging fourth quarter of 2024, when Clear Channel missed earnings expectations with an EPS of -$0.0365 against a forecast of $0.02. The Q1 2025 results indicate continued challenges in improving bottom-line performance despite top-line growth.

Quarterly Performance Highlights

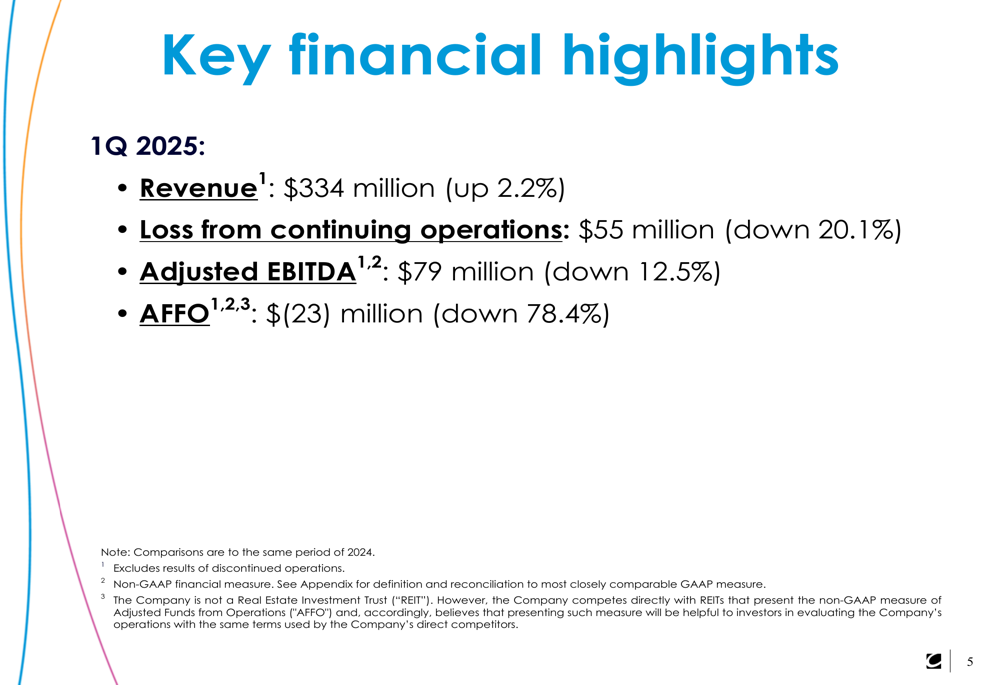

Clear Channel reported Q1 2025 revenue of $334 million, representing a 2.2% increase compared to the same period in 2024. However, profitability metrics showed significant declines, with Adjusted EBITDA falling 12.5% to $79 million and Adjusted Funds From Operations (AFFO) declining 78.4% to -$23 million. Loss from continuing operations improved by 20.1% to $55 million.

As shown in the key financial highlights from the presentation:

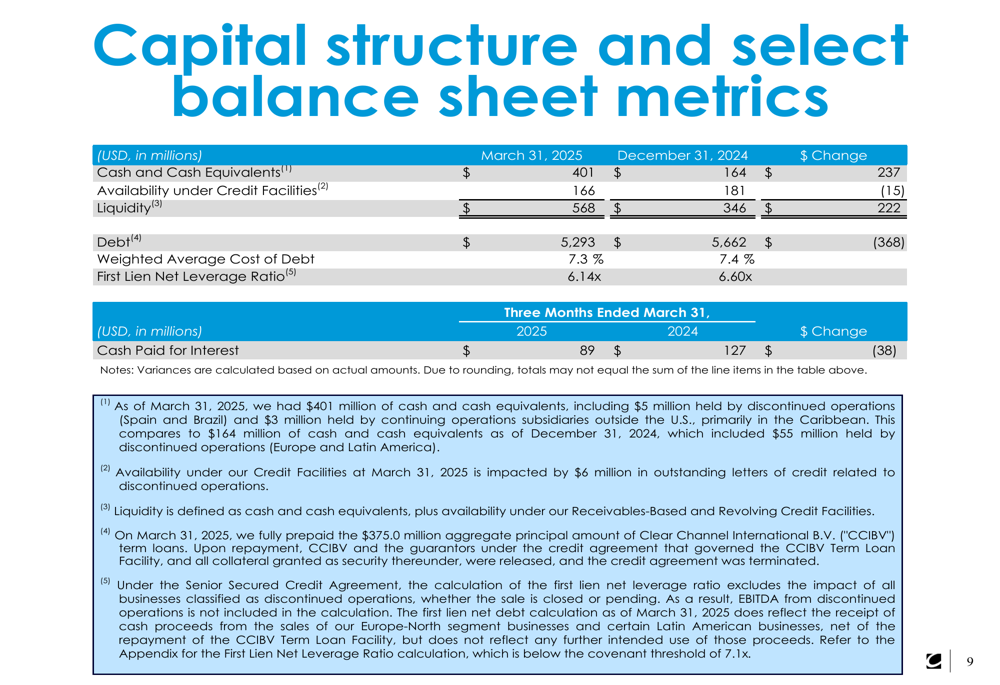

The company’s capital structure remains heavily leveraged, with total debt of $5,293 million as of March 31, 2025. The weighted average cost of debt stands at 7.3%, and the first lien net leverage ratio is 6.14x. Clear Channel reported cash and cash equivalents of $401 million, providing total liquidity of $568 million when combined with availability under credit facilities.

Segment Analysis

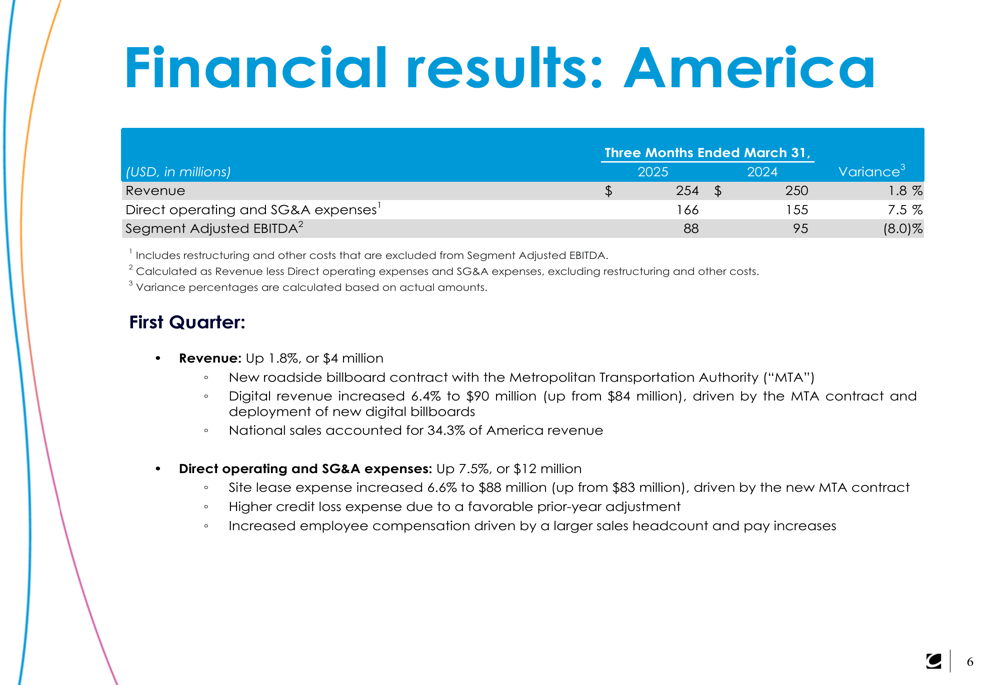

The America segment, which represents the company’s largest business unit, delivered revenue of $254 million, up 1.8% year-over-year. Digital revenue within this segment increased by 6.4%, driven by the new roadside billboard contract with the Metropolitan Transportation Authority (MTA) and deployment of new digital billboards. National sales accounted for 34.3% of America revenue. However, direct operating and SG&A expenses increased by 7.5%, primarily due to higher site lease expense from the MTA contract and increased employee compensation, resulting in an 8.0% decline in Segment Adjusted EBITDA to $88 million.

The financial results for the America segment are detailed in this slide:

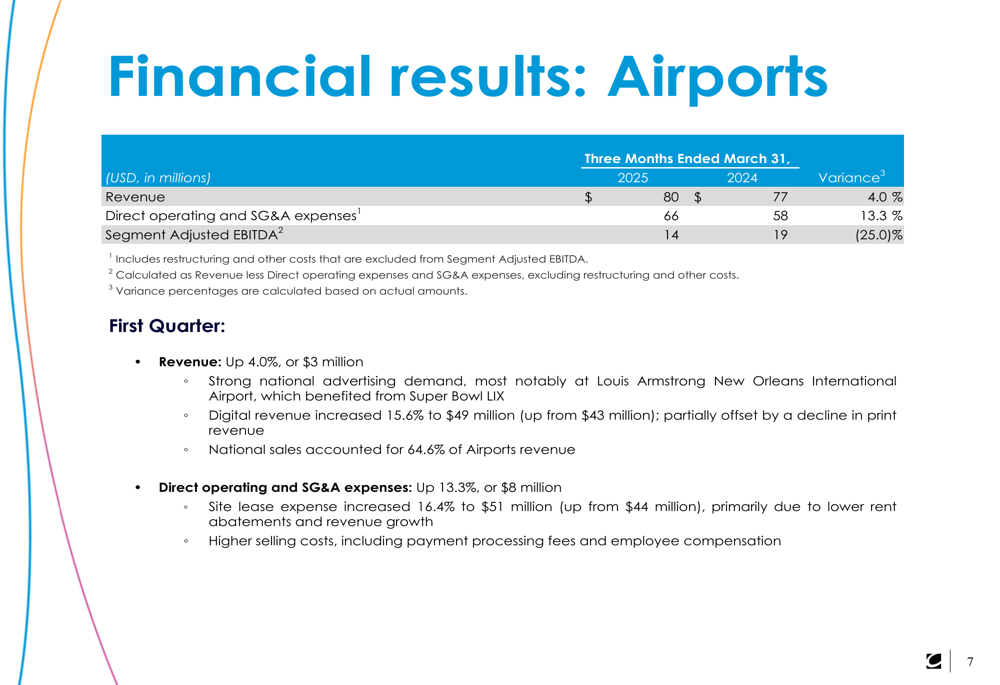

The Airports segment showed stronger revenue growth of 4.0%, reaching $80 million in Q1 2025. This growth was driven by strong national advertising demand and a 15.6% increase in digital revenue, boosted by the Louis Armstrong New Orleans International Airport Super Bowl LIX event. National sales represented 64.6% of Airports revenue. Similar to the America segment, expenses increased at a faster rate than revenue, with direct operating and SG&A expenses up 13.3%, leading to a 25.0% decline in Segment Adjusted EBITDA to $14 million.

The following slide illustrates the Airports segment performance:

Strategic Initiatives and Debt Reduction

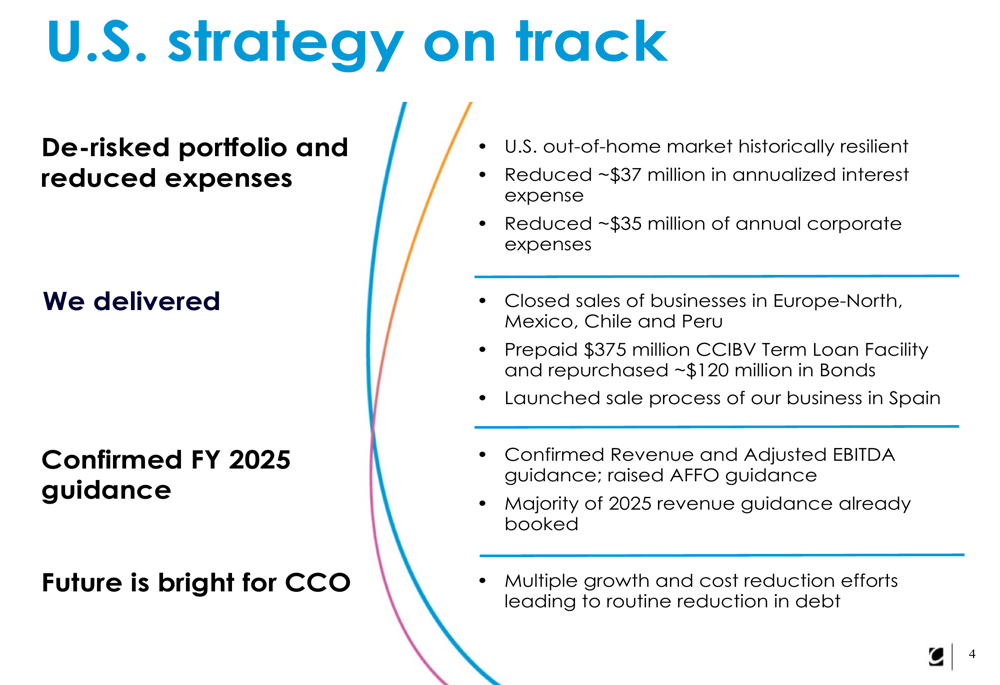

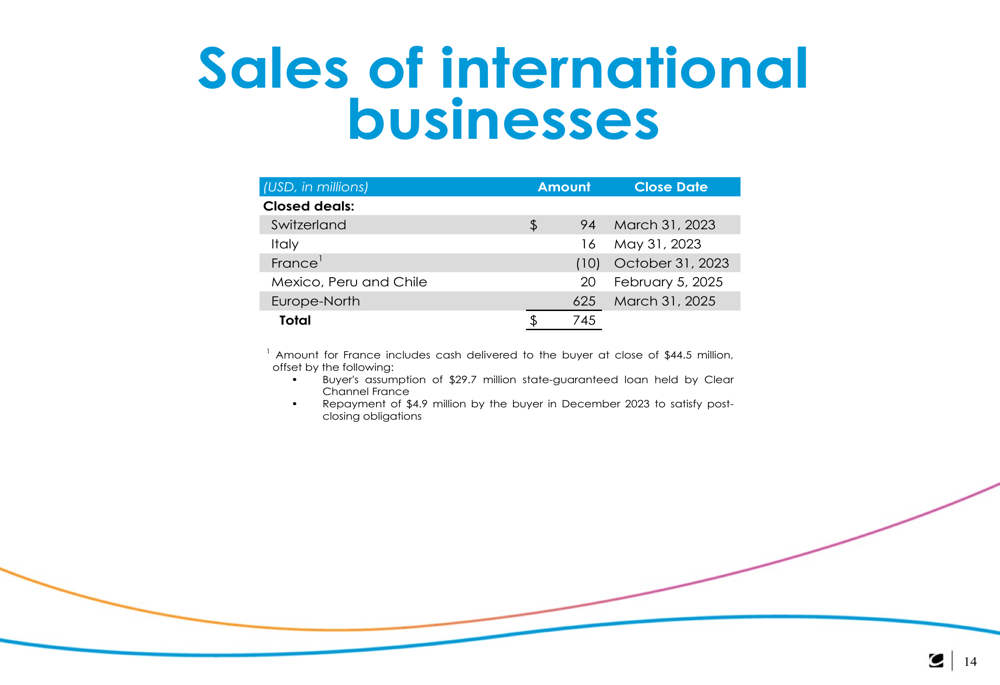

Clear Channel continues to execute its strategy of focusing on U.S. operations while divesting international businesses. The company has successfully closed sales of businesses in Europe-North, Mexico, Chile, and Peru, and has launched the sale process for its business in Spain. In total, the company has generated $745 million from international divestments.

The proceeds from these sales have been used to strengthen the balance sheet, including the prepayment of a $375 million CCIBV Term Loan Facility and repurchase of approximately $120 million in bonds. The company has reduced annualized interest expense by approximately $37 million and annual corporate expenses by approximately $35 million.

The progress on the company’s U.S. strategy is highlighted in this slide:

The details of international business sales are presented here:

Clear Channel’s billboard portfolio continues to serve major brands across the United States, as showcased in these examples:

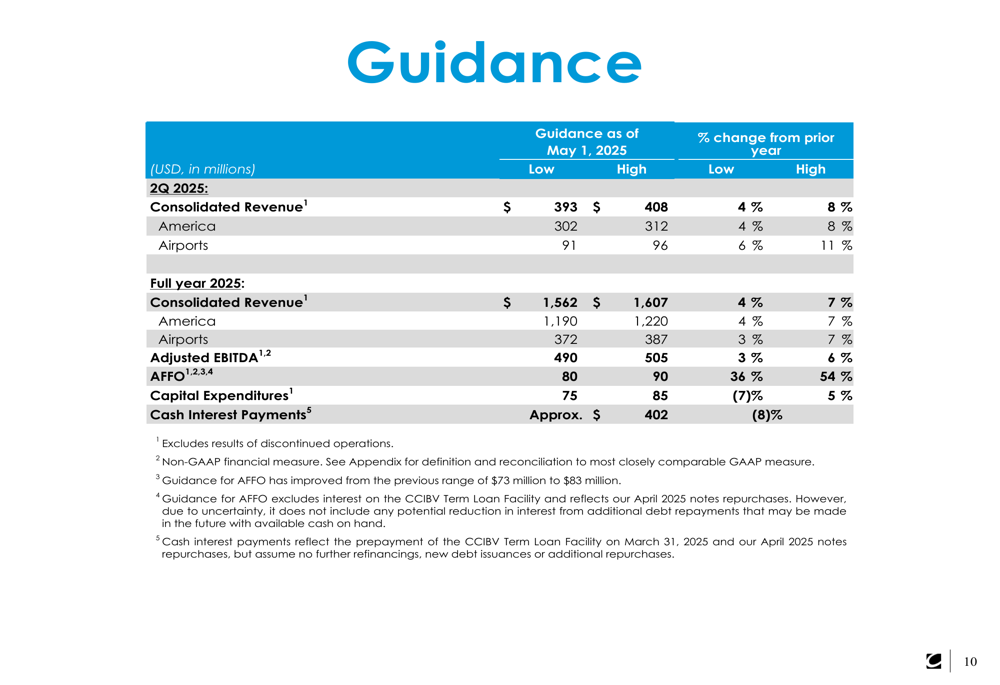

Forward Guidance and Outlook

Looking ahead, Clear Channel provided guidance for both Q2 2025 and the full year. For Q2 2025, the company expects consolidated revenue of $393-$408 million, representing 4-8% year-over-year growth. The America segment is projected to generate $302-$312 million (4-8% growth), while the Airports segment is expected to contribute $91-$96 million (6-11% growth).

For the full year 2025, Clear Channel forecasts consolidated revenue of $1,562-$1,607 million (4-7% growth), Adjusted EBITDA of $490-$505 million (3-6% growth), and AFFO of $80-$90 million (36-54% growth). The company also expects capital expenditures of $75-$85 million and cash interest payments of approximately $402 million, an 8% reduction from the previous year.

The detailed guidance is presented in this slide:

Despite the positive revenue guidance, Clear Channel faces ongoing challenges, including high debt levels and declining profitability metrics. The company’s first lien net leverage ratio of 6.14x indicates significant financial leverage, though management is focused on routine debt reduction through growth and cost-cutting initiatives.

As Clear Channel continues its strategic transformation, investors will be watching closely to see if the company can translate its modest revenue growth into improved profitability and accelerated debt reduction in the coming quarters. The guidance suggests management expects performance to improve throughout 2025, particularly in the Airports segment where Q2 revenue growth is projected to reach up to 11%.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.