Procore signs multi-year strategic collaboration agreement with AWS

Introduction & Market Context

CNX Resources (NYSE:CNX) presented its Q1 2025 update on April 24, 2025, highlighting continued operational execution and financial discipline. The natural gas producer, operating primarily in the Appalachian Basin, reported its 21st consecutive quarter of positive free cash flow generation despite challenging market conditions in previous quarters.

The company’s stock has shown resilience, trading at $30.59 at the previous close, with premarket activity showing a 1.67% increase to $31.10. This positive movement comes after CNX experienced a significant earnings miss in Q4 2024, suggesting investors are focusing on the company’s consistent cash flow generation and shareholder return strategy rather than quarterly earnings volatility.

Quarterly Performance Highlights

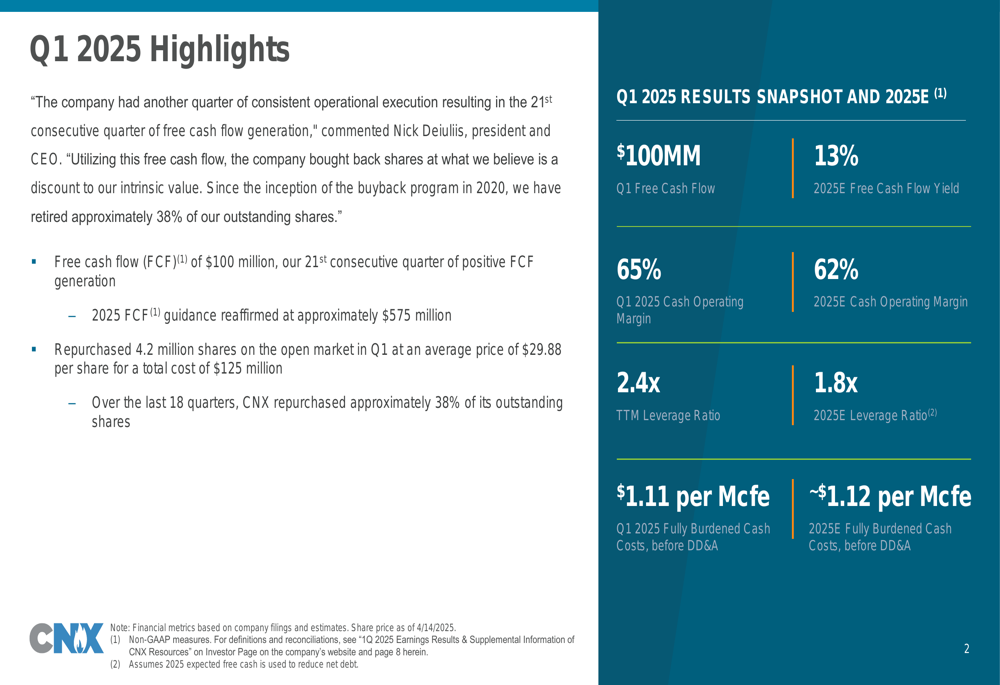

CNX delivered $100 million in free cash flow during Q1 2025, maintaining its streak of positive FCF generation. The company achieved a robust 65% cash operating margin for the quarter, demonstrating effective cost management in its operations.

CEO Nick Deiuliis emphasized the company’s consistent operational execution, which has become a hallmark of CNX’s strategy in recent years. The company’s fully burdened cash costs before DD&A remained controlled at $1.11 per Mcfe during Q1, positioning CNX as one of the more efficient operators in its peer group.

As shown in the following quarterly results snapshot:

Free Cash Flow and Capital Allocation

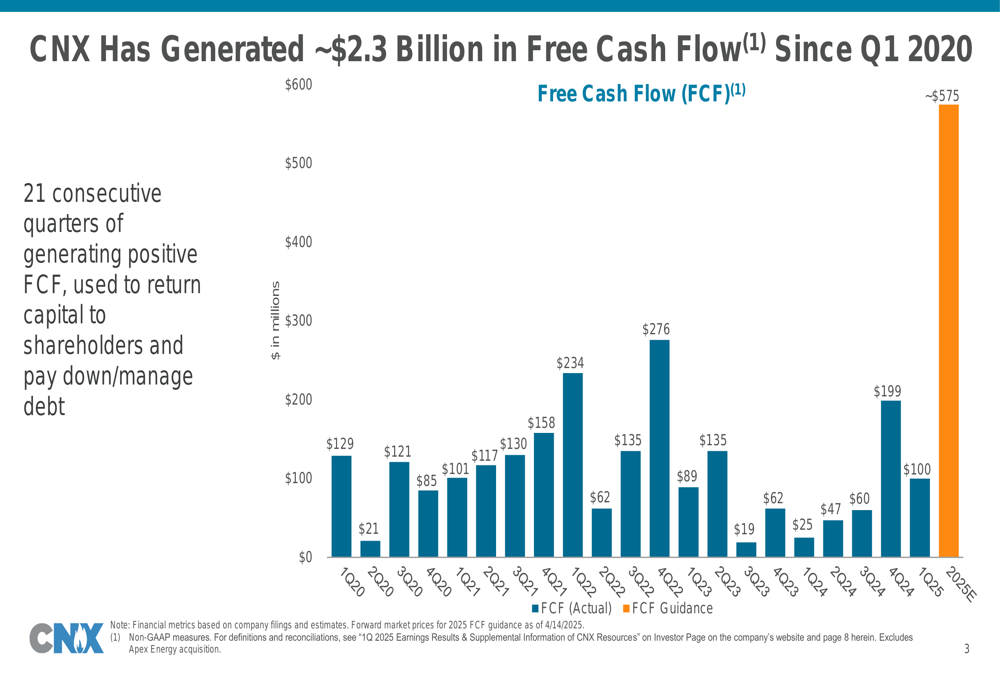

CNX has generated approximately $2.3 billion in free cash flow since Q1 2020, with no quarters of negative FCF during this period. This consistent performance has enabled the company to pursue an aggressive share repurchase program while maintaining balance sheet strength.

The company’s free cash flow trajectory is illustrated in this multi-year chart:

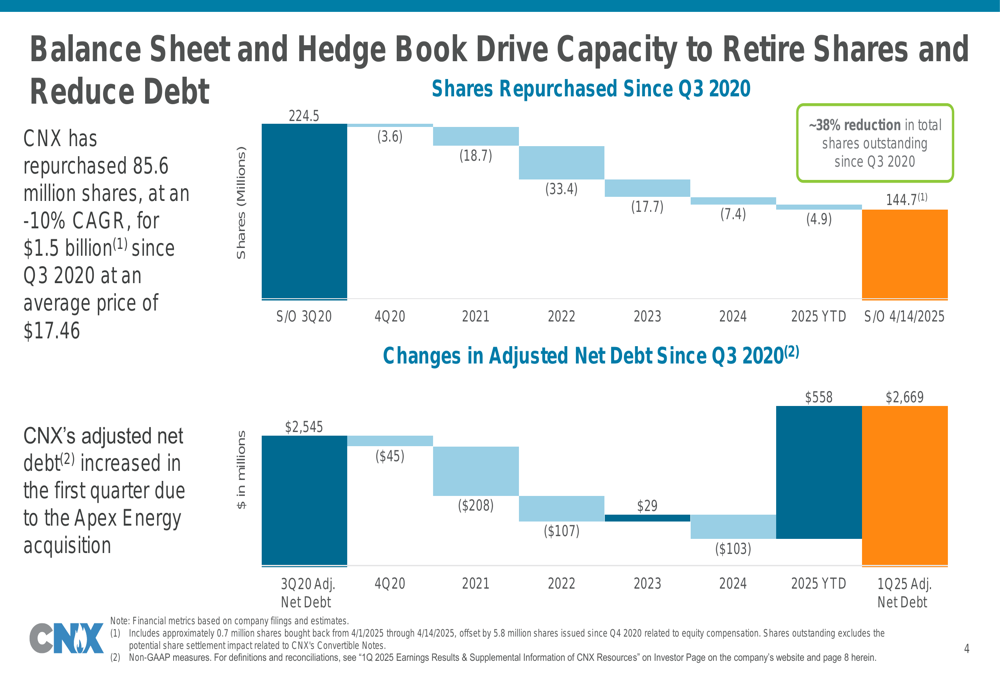

Capital allocation has heavily favored share repurchases, with CNX buying back 4.2 million shares on the open market in Q1 at an average price of $29.88 per share, totaling $125 million. Since initiating its buyback program in Q3 2020, the company has repurchased 85.6 million shares at an average price of $17.46, reducing its outstanding share count by approximately 38%.

This aggressive share repurchase strategy has significantly reduced the company’s share count over time, as demonstrated in the following chart:

Balance Sheet and Liquidity Position

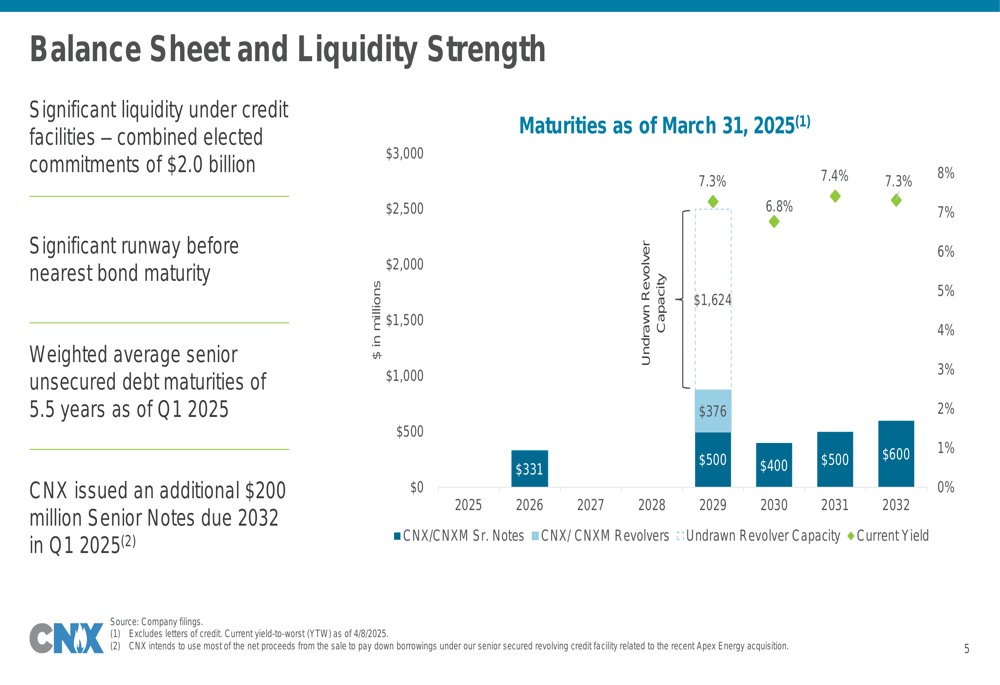

CNX maintains a strong balance sheet with substantial liquidity. The company reported a trailing twelve-month leverage ratio of 2.4x, which it expects to improve to 1.8x by the end of 2025. This deleveraging trajectory reflects management’s commitment to financial discipline.

The company has significant runway before facing major debt maturities, with a weighted average senior unsecured debt maturity of 5.5 years as of Q1 2025. CNX also maintains substantial liquidity under its credit facilities, with combined elected commitments of $2.0 billion.

The following chart illustrates CNX’s debt maturity schedule:

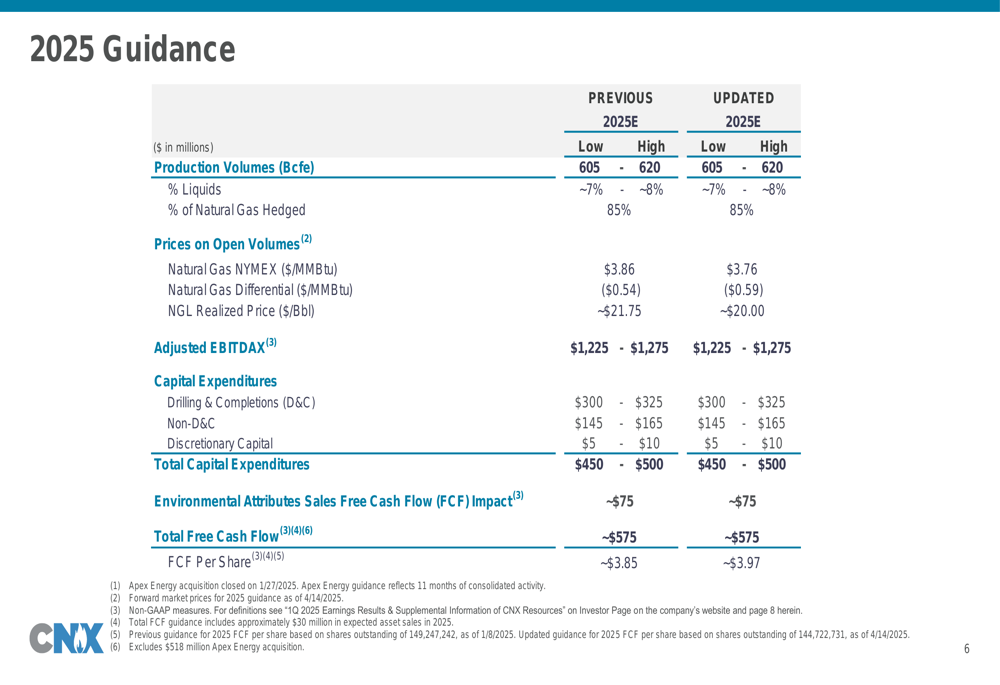

2025 Guidance and Outlook

CNX reaffirmed its 2025 guidance, projecting approximately $575 million in free cash flow for the full year, which translates to a free cash flow yield of 13% and approximately $3.97 per share. The company expects to maintain cash operating margins of around 62% for the year.

Production volumes are projected to be between 605-620 Bcfe, with liquids comprising approximately 7-8% of total production. The company has hedged approximately 85% of its natural gas production for 2025, providing significant cash flow certainty in a volatile commodity price environment.

Capital expenditures are expected to range between $450-$500 million, with the majority allocated to drilling and completions activities. The company projects adjusted EBITDAX of $1,225-$1,275 million for the full year.

The detailed 2025 guidance is presented in the following table:

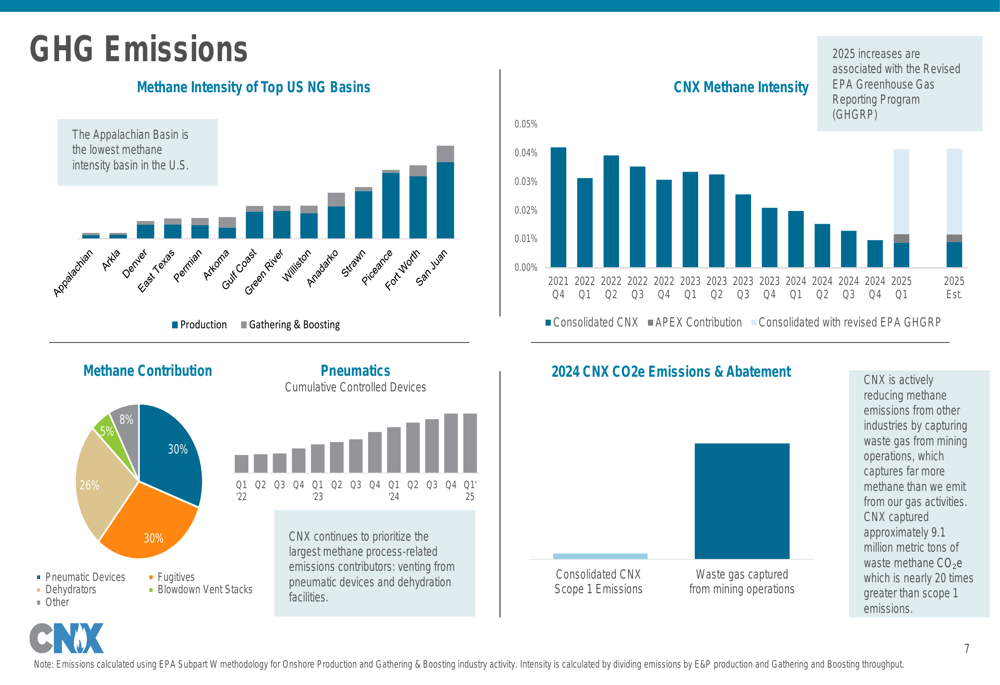

Environmental Initiatives

CNX highlighted its environmental performance, noting that it operates in the Appalachian Basin, which has the lowest methane intensity among U.S. natural gas producing regions. The company is actively working to reduce methane emissions by capturing waste gas from mining operations.

In 2024, CNX captured approximately 9.1 million metric tons of waste methane CO₂e, which is nearly 20 times greater than its Scope 1 emissions. This environmental focus positions the company favorably in an increasingly ESG-conscious market and regulatory environment.

The company’s emissions profile and abatement efforts are illustrated in the following chart:

While CNX’s Q1 2025 presentation maintains a positive tone about the company’s operational execution and financial discipline, it’s worth noting that the company experienced a significant earnings miss in the previous quarter. Q4 2024 saw an EPS of -$0.97 against a forecast of $0.43, with revenue of $136.58 million versus expectations of $424.4 million.

Despite these previous challenges, CNX’s consistent free cash flow generation and shareholder-friendly capital allocation strategy appear to be resonating with investors, as evidenced by the stock’s resilience and positive premarket movement following the Q1 update.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.