Broadcom named strategic vendor for Walmart virtualization solutions

Introduction & Market Context

CNX Resources Corp (NYSE:CNX) presented its Q2 2025 results on July 24, 2025, highlighting continued free cash flow generation despite challenging market conditions. The natural gas producer, operating primarily in the Appalachian Basin, reported significant progress in its share repurchase program and maintained its full-year guidance. The presentation comes after a disappointing Q1 that saw the company miss earnings expectations with an EPS of -1.34 against a forecast of 0.61, though CNX’s stock has shown signs of recovery since then, closing at $33.13 on July 23.

Quarterly Performance Highlights

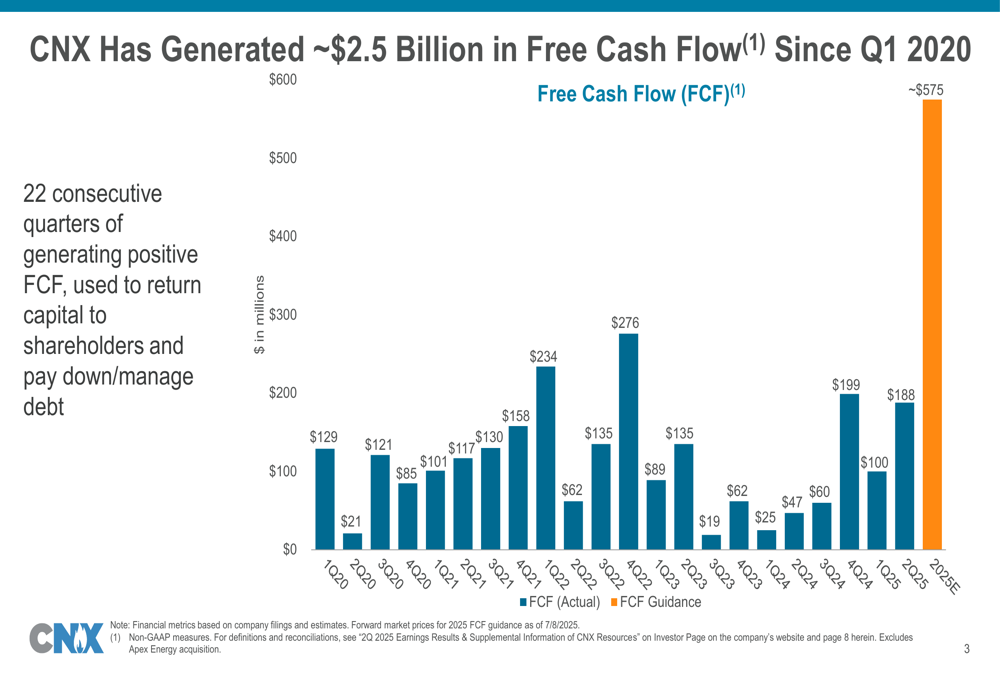

CNX reported $188 million in free cash flow for Q2 2025, marking its 22nd consecutive quarter of positive FCF generation. The company maintained strong operational efficiency with a 65% cash operating margin and fully burdened cash costs of $1.05 per Mcfe before DD&A.

As shown in the following chart of quarterly free cash flow generation, CNX has consistently delivered positive results since Q1 2020, accumulating approximately $2.5 billion in total free cash flow:

The company’s Q2 performance represents a significant improvement from Q1 2025’s $100 million FCF and demonstrates a recovery trajectory following lower results throughout 2023. Management reaffirmed its 2025 FCF guidance of approximately $575 million, suggesting confidence in maintaining this momentum through year-end.

Capital Allocation Strategy

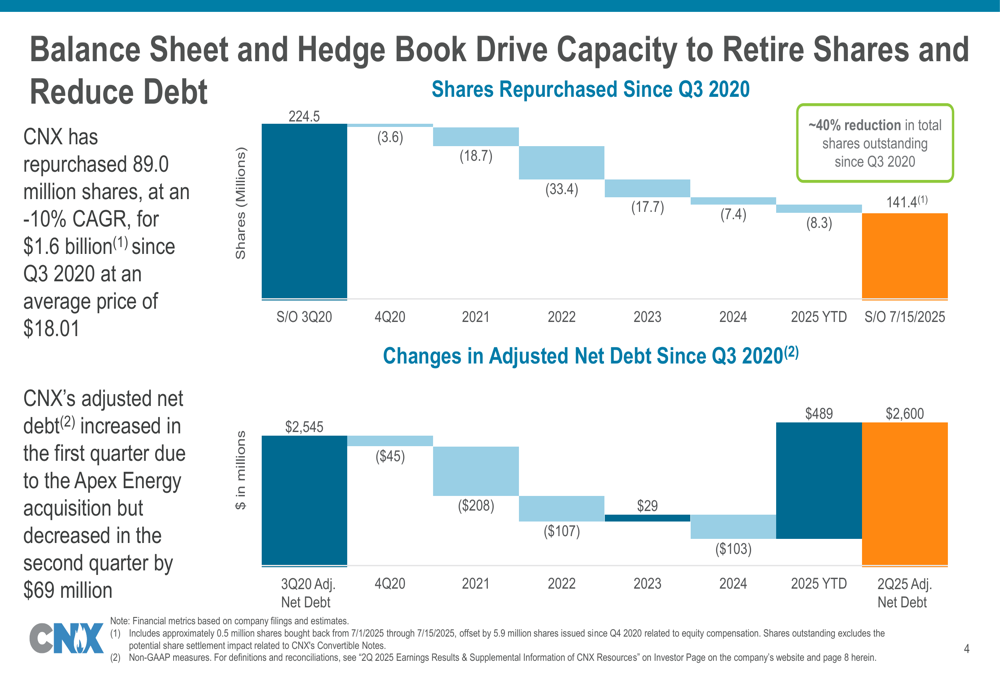

Share repurchases remain a cornerstone of CNX’s capital allocation strategy. During Q2 2025, the company repurchased 3.7 million shares on the open market at an average price of $31.24 per share, totaling $114 million. This continues an aggressive buyback program that has reduced outstanding shares by approximately 40% since Q3 2020.

The following chart illustrates CNX’s share repurchase progress and debt management since Q3 2020:

Since initiating the program, CNX has repurchased 89.0 million shares for $1.6 billion at an average price of $18.01 per share, representing significant value creation for remaining shareholders. The company’s shares outstanding have decreased from 224.5 million in Q3 2020 to 141.4 million as of July 15, 2025.

While the adjusted net debt increased in Q1 2025 due to the Apex Energy acquisition, it decreased by $69 million in Q2, demonstrating the company’s commitment to maintaining financial discipline even while pursuing strategic acquisitions.

Balance Sheet and Liquidity

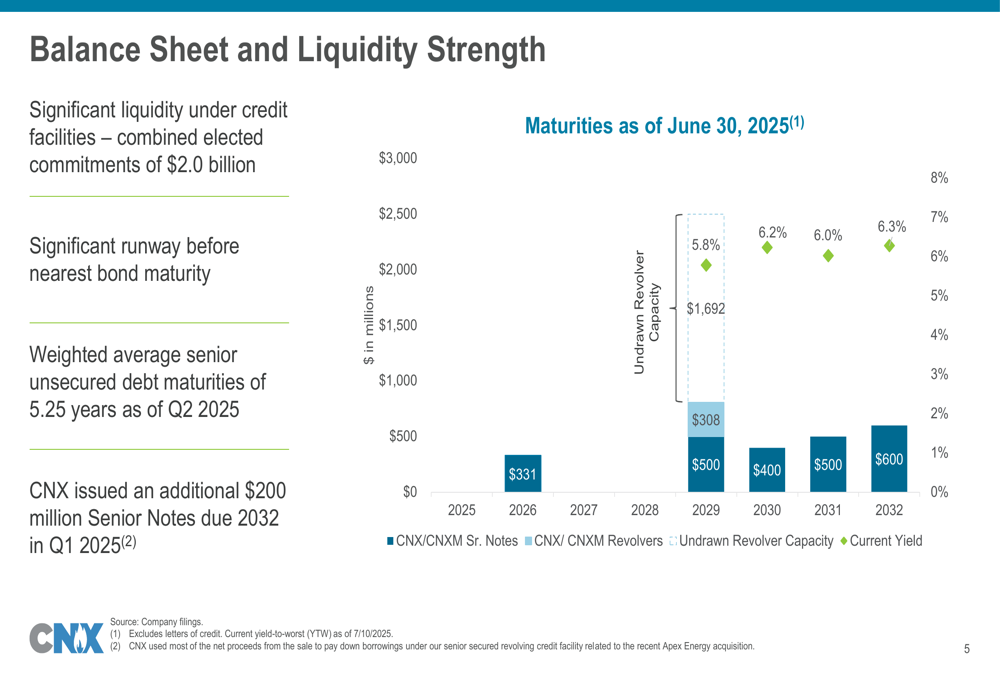

CNX maintains a strong liquidity position with $1.692 billion in undrawn revolver capacity and a well-structured debt maturity profile. The weighted average senior unsecured debt maturities extend 5.25 years, providing significant financial flexibility.

The company’s debt maturity schedule is illustrated in the following chart:

In Q1 2025, CNX issued an additional $200 million in Senior Notes due 2032, further extending its maturity profile. The company’s TTM leverage ratio stands at 2.2x, with projections to improve to 1.9x by year-end 2025, reflecting management’s focus on maintaining balance sheet strength while returning capital to shareholders.

Operational Guidance

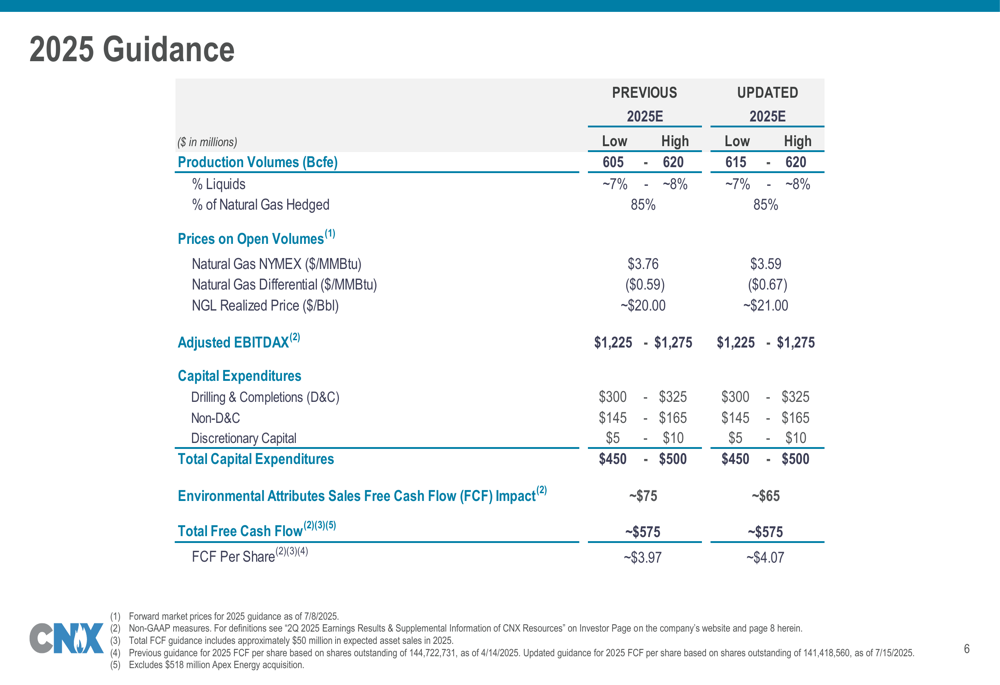

CNX slightly raised the lower end of its 2025 production guidance to 615-620 Bcfe from the previous 605-620 Bcfe, suggesting operational confidence despite the production lull anticipated in Q3 (mentioned in the Q1 earnings call). The company maintains its hedging strategy with 85% of natural gas production hedged for 2025.

The comprehensive 2025 guidance update is detailed in the following chart:

The company maintained its Adjusted EBITDAX guidance of $1,225-$1,275 million and total free cash flow projection of approximately $575 million. Notably, CNX increased its FCF per share guidance to approximately $4.07 from $3.97, reflecting the impact of continued share repurchases. Capital expenditures remain unchanged at $450-$500 million, with $300-$325 million allocated to drilling and completions.

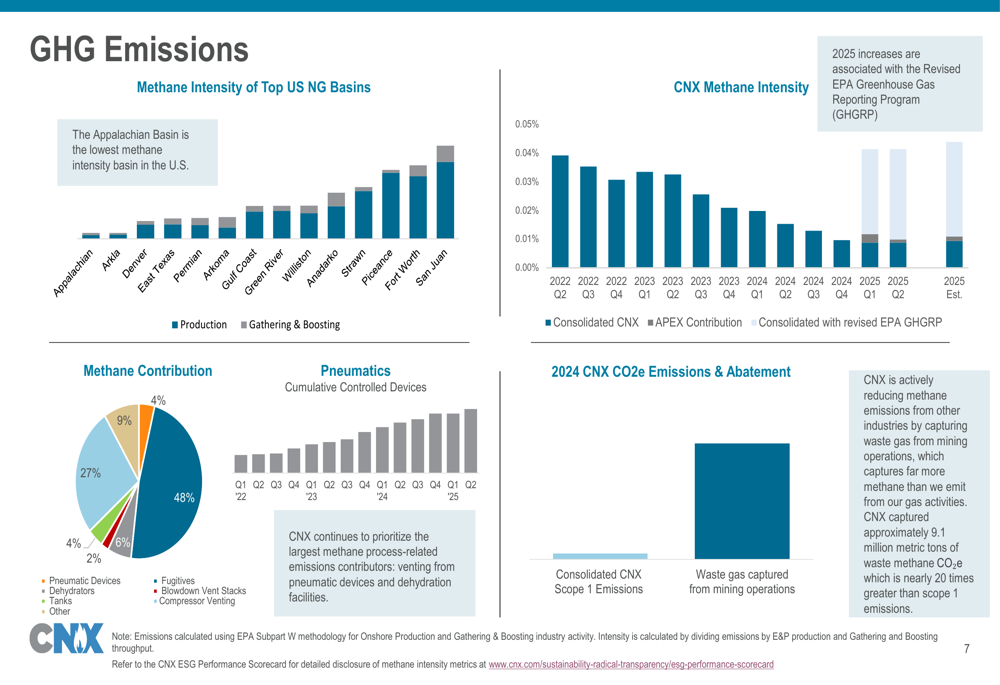

Environmental Initiatives

CNX continues to prioritize environmental performance, particularly focusing on methane emissions reduction. The company operates in the Appalachian Basin, which has the lowest methane intensity among major U.S. natural gas basins.

The following chart details CNX’s emissions profile and reduction efforts:

The company has targeted pneumatic devices, which contribute 48% of its methane emissions, as a primary focus area for reduction efforts. CNX reports capturing approximately 9.1 million metric tons of waste methane CO₂e, nearly 20 times greater than its scope 1 emissions, demonstrating its commitment to environmental stewardship alongside financial performance.

Forward-Looking Statements

Despite the significant Q1 2025 earnings miss, CNX’s Q2 presentation emphasizes continued operational execution and financial discipline. The company’s maintained guidance suggests management confidence in meeting full-year targets despite quarterly fluctuations.

The focus on per-share metrics, particularly the increased FCF per share guidance, aligns with statements from the Q1 earnings call where CFO Alan Shepherd emphasized, "We’re solving for free cash flow per share as opposed to any particular production level target."

The performance of the Apex Energy acquisition wells, which COO Nav Bell noted were "producing better than we expected" during the Q1 call, appears to be contributing positively to the company’s operational results, though specific production figures from these wells were not detailed in the Q2 presentation.

With CNX shares trading at $33.13 as of July 23, 2025, and showing slight premarket weakness (-0.45%) on the day of the presentation, investors appear cautiously optimistic about the company’s trajectory following the Q2 results, which demonstrate recovery from the challenging first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.