EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

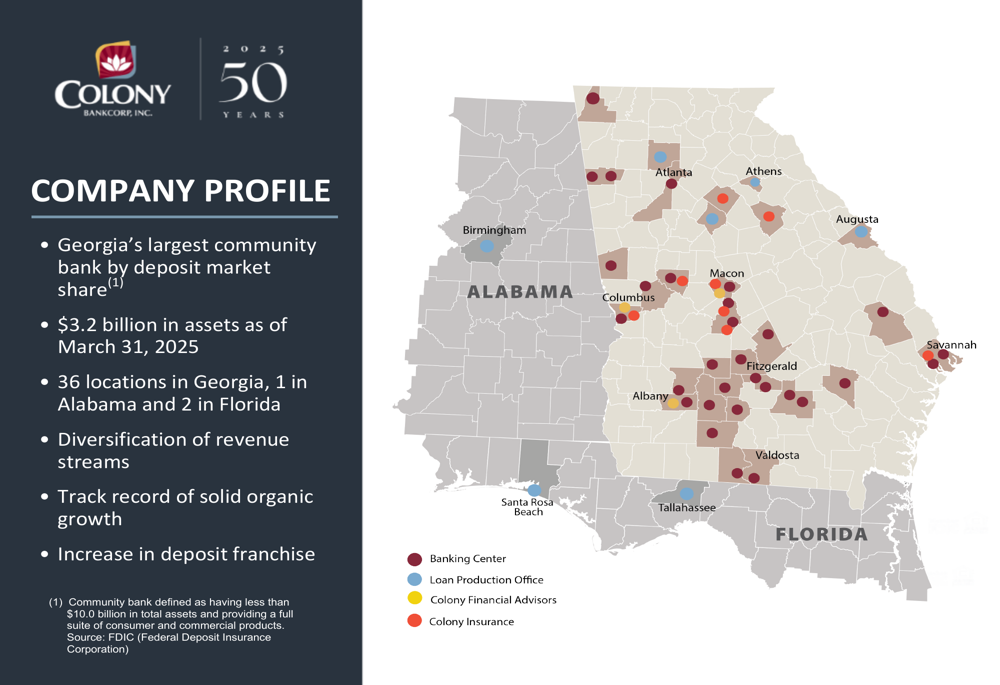

Colony Bankcorp, Inc. (NASDAQ:CBAN) released its first quarter 2025 investor presentation, highlighting its position as Georgia’s largest community bank by deposit market share with $3.2 billion in assets. The presentation, which comes after the bank’s strong Q4 2024 performance that saw earnings per share of $0.44 against a forecast of $0.33, outlines the company’s strategic initiatives and financial position.

Colony’s stock has shown positive momentum, trading at $15.90 in premarket activity on April 24, 2025, up 2.85% from its previous close of $15.46. This follows a 12.1% jump in aftermarket trading following the Q4 2024 earnings release, reflecting investor confidence in the bank’s performance and strategy.

As shown in the following geographical footprint map, Colony Bank operates 36 locations in Georgia, along with one in Alabama and two in Florida, positioning it in both high-growth metropolitan markets and stable rural communities:

Strategic Initiatives & Growth Strategy

Colony Bank’s presentation outlines a dual growth strategy focused on both organic expansion and strategic acquisitions. The bank aims to return to an 8-12% organic growth run rate by the end of 2025, leveraging its presence in dynamic growth markets including Atlanta, Augusta, Birmingham, North Florida, and Savannah.

CEO Heath Fountain, who joined the bank six years ago, is leading a strategic focus on innovation and efficiency. The bank has implemented several technology initiatives including a new digital banking platform, Salesforce (NYSE:CRM) CRM system, and nCino loan origination software to enhance customer experience and operational efficiency.

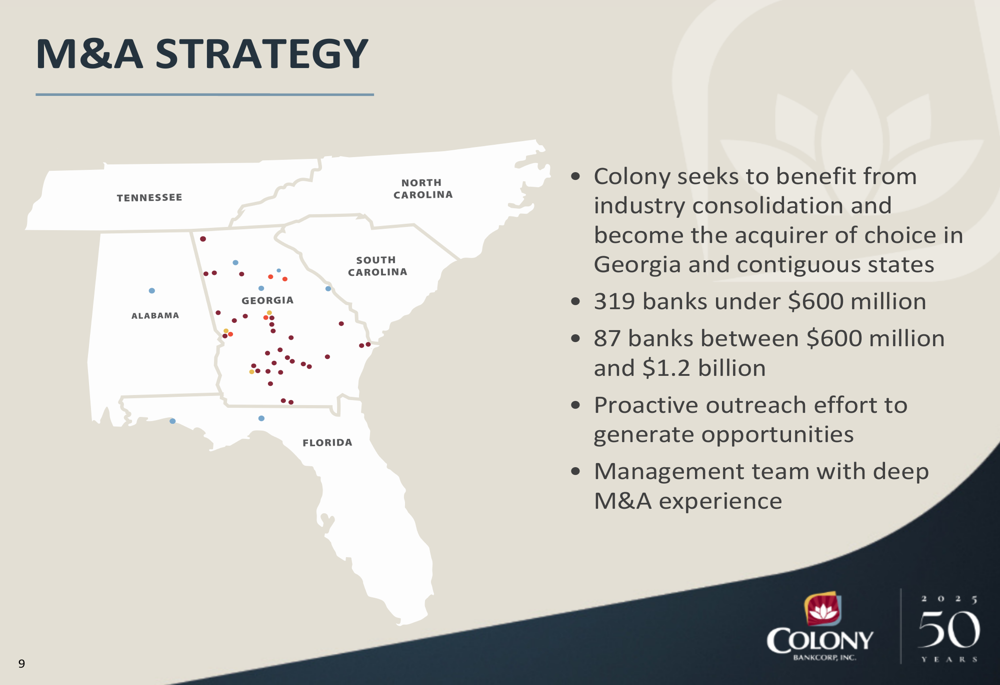

The bank’s M&A strategy aims to capitalize on industry consolidation, targeting 319 banks under $600 million and 87 banks between $600 million and $1.2 billion in assets across Georgia and contiguous states:

A recent example of this strategy is the acquisition of the Ellerbee Agency, which expands Colony Insurance into additional markets of Monroe, Greensboro, and Lake Oconee. The $3.5 million acquisition is expected to be immediately accretive to earnings per share by approximately $0.02 in the first full year, with the agency having achieved approximately $15 million in annual premiums and $2 million in annual gross revenue in 2024.

Financial Performance Highlights

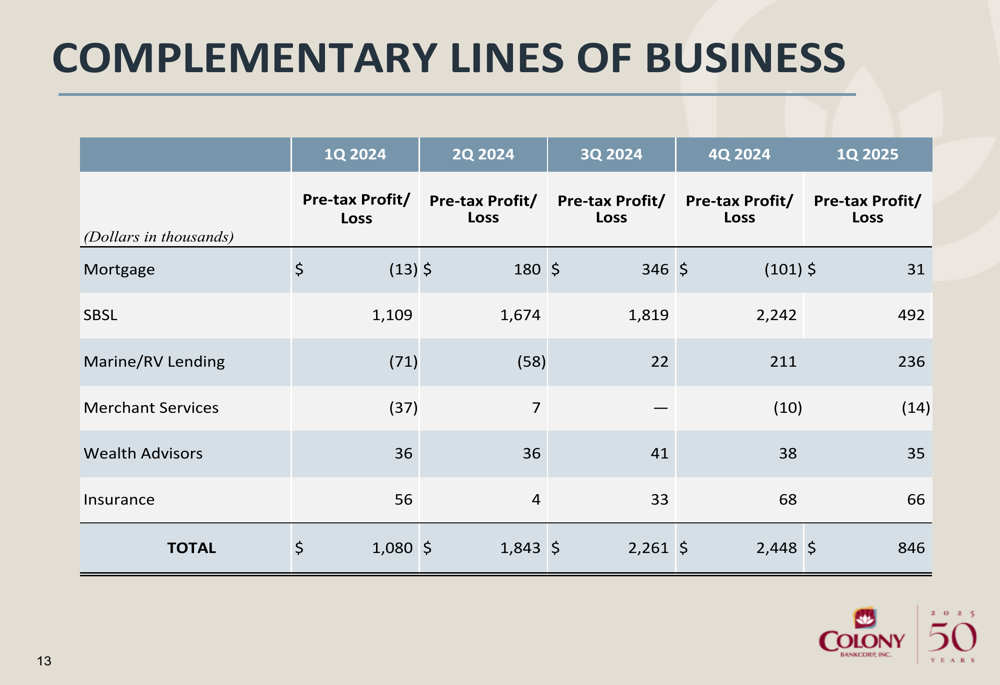

Colony’s complementary lines of business show mixed performance but contribute significantly to the bank’s diversified revenue streams. As illustrated in the following chart, while Small Business Specialty Lending (SBSL) remains the largest contributor, other segments like Marine/RV Lending have shown consistent improvement:

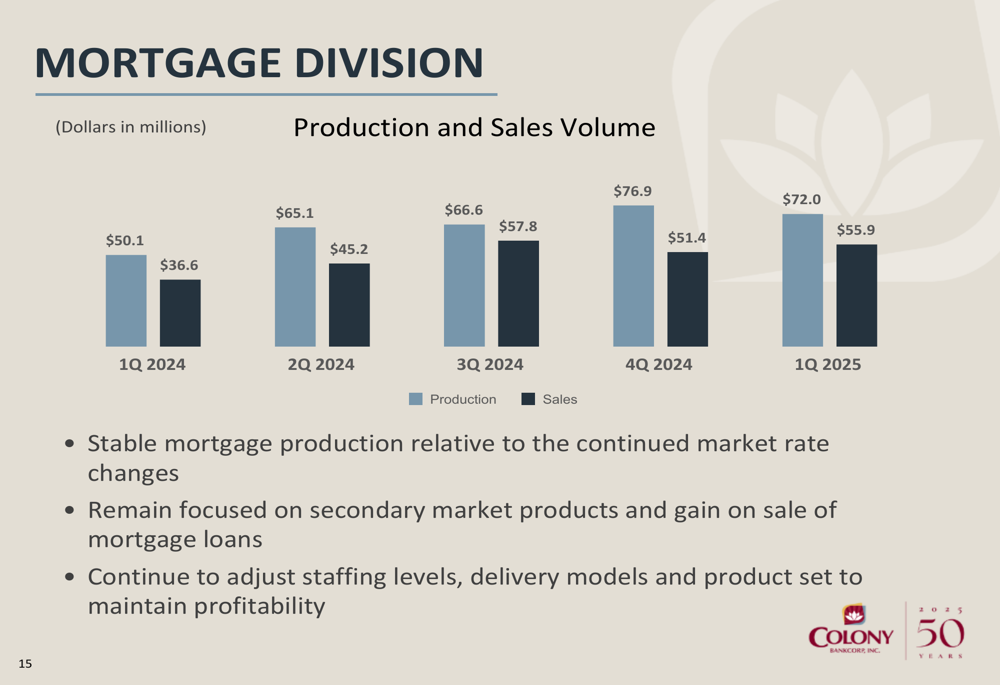

The bank’s mortgage division has maintained strong production volumes despite the challenging interest rate environment. In Q1 2025, mortgage production reached $72.0 million with sales of $55.9 million, demonstrating resilience in this business segment:

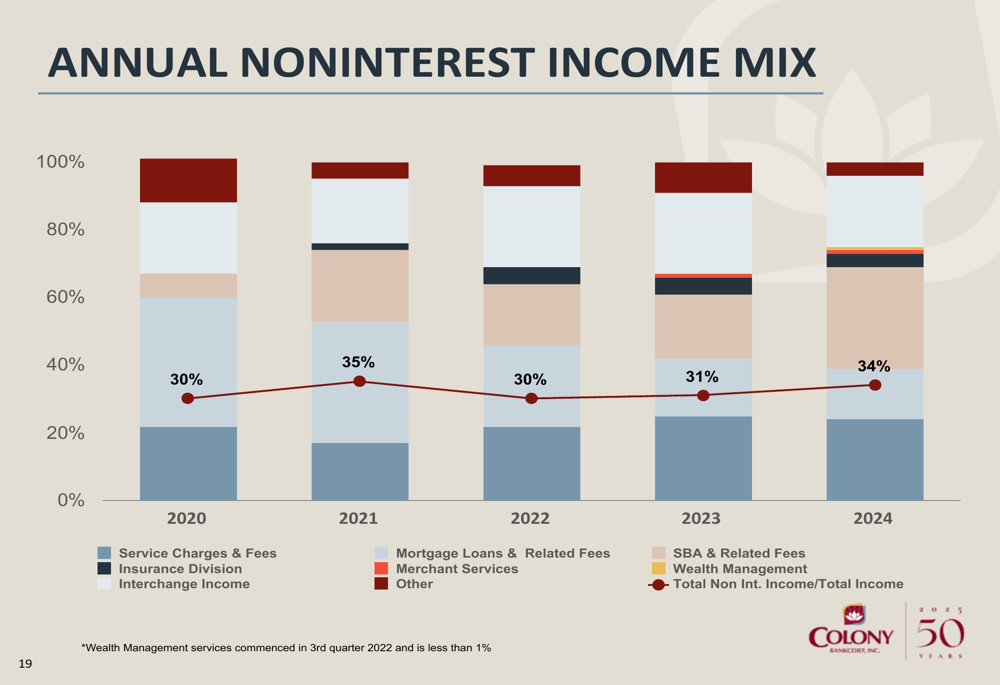

Colony’s noninterest income mix shows increasing diversification, with service charges, insurance, and interchange income representing the largest components. This diversification strategy has helped maintain stable revenue streams despite interest rate fluctuations:

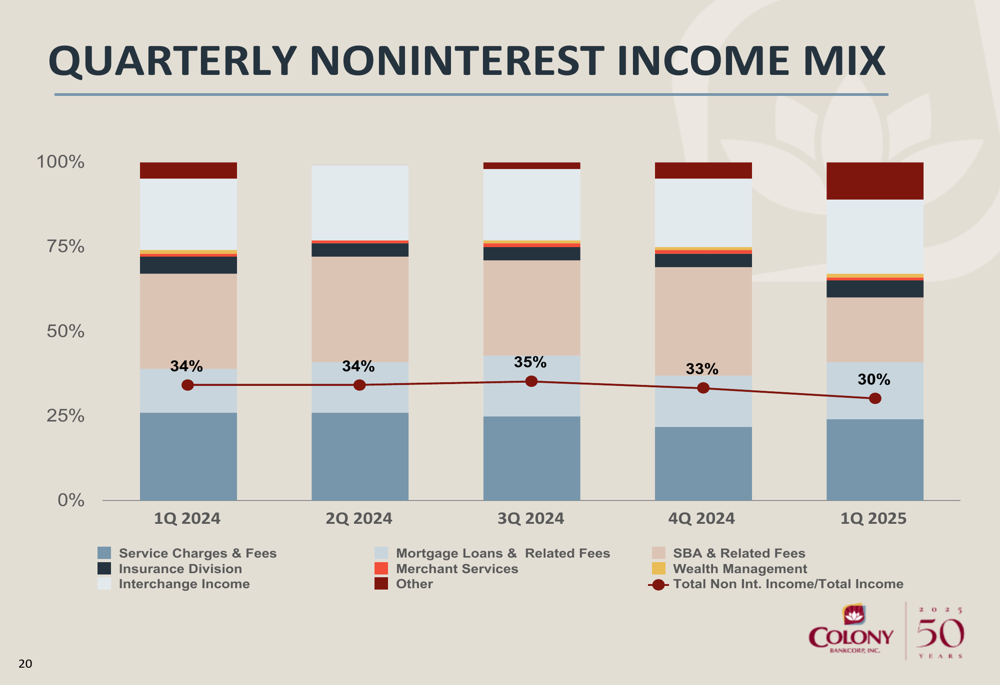

The quarterly noninterest income mix shows some seasonal fluctuation, with total noninterest income representing 30% of total income in Q1 2025, down from 34% in Q1 2024:

Capital Position & Liquidity

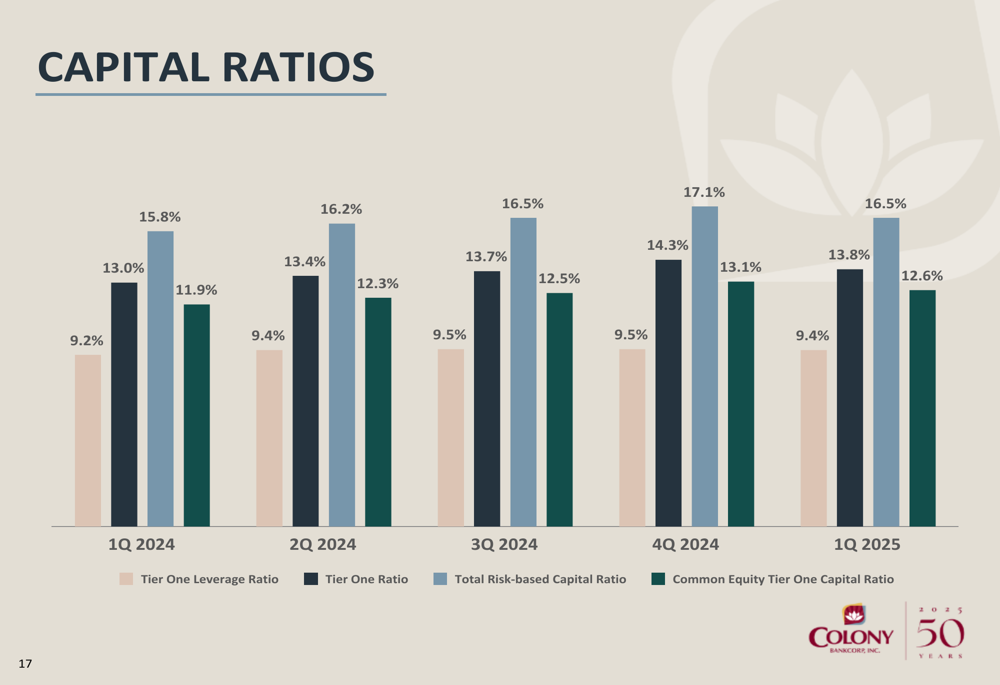

Colony maintains strong capital ratios, well above regulatory requirements. As of Q1 2025, the bank reported a Tier One Leverage Ratio of 9.4%, Tier One Ratio of 13.8%, Total (EPA:TTEF) Risk-based Capital Ratio of 16.5%, and Common Equity Tier One Capital Ratio of 12.6%:

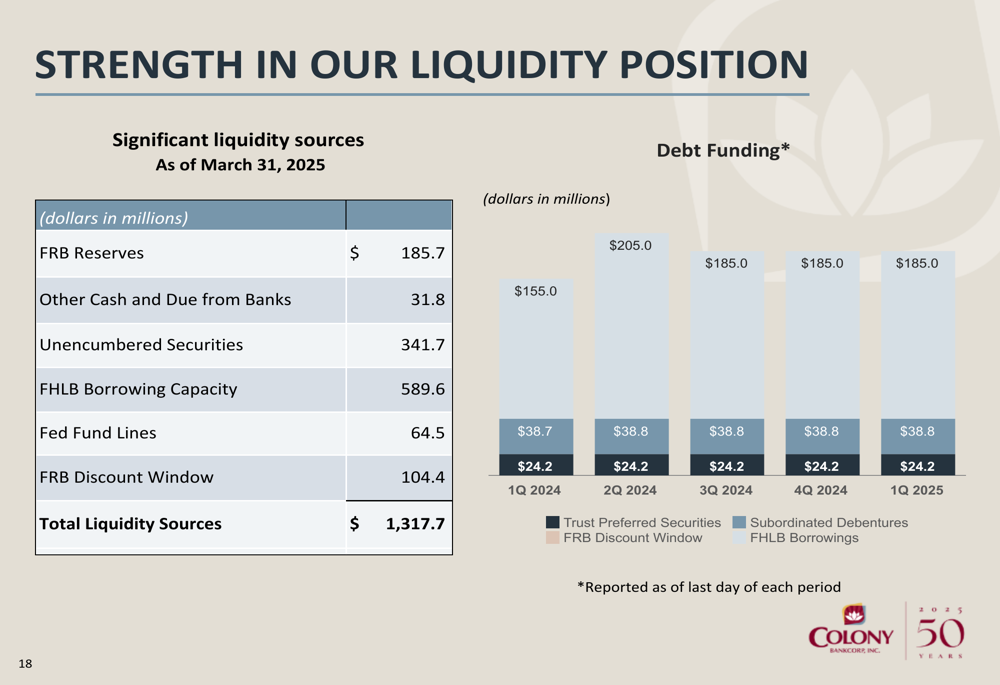

The bank’s liquidity position remains robust with total liquidity sources of $1,317.7 million as of March 31, 2025, including $185.7 million in Federal Reserve reserves, $341.7 million in unencumbered securities, and $589.6 million in FHLB borrowing capacity:

Colony has maintained a shareholder-focused dividend policy, with the quarterly dividend increasing from $0.1125 in 2024 to $0.1150 in 2025, representing an annual yield of 3.1% based on the April 19, 2025 closing stock price of $14.85.

Loan & Deposit Portfolio Composition

Colony’s loan portfolio remains heavily weighted toward real estate at 83.6%, with commercial loans representing 10.3%, consumer and other loans at 5.3%, and agriculture loans at 0.8%. Within the real estate category, nonowner occupied real estate represents 34.1% of the portfolio, followed by owner occupied real estate at 22.4% and residential real estate at 21.5%.

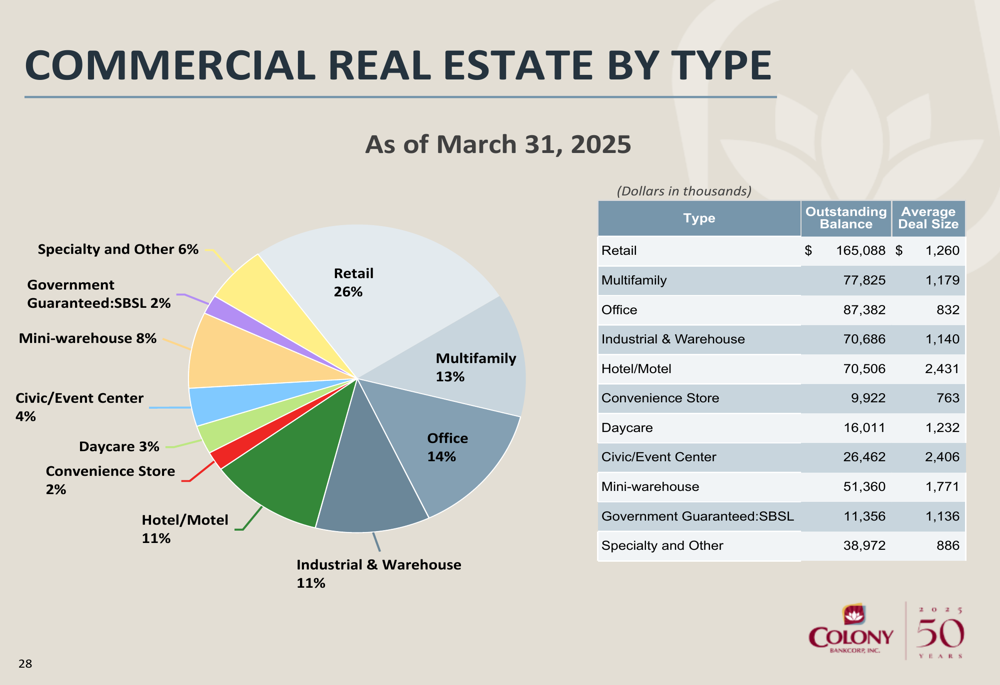

The bank’s commercial real estate portfolio is well-diversified across property types, with retail (26%), office (14%), multifamily (13%), industrial & warehouse (11%), and hotel/motel (11%) representing the largest segments:

On the deposit side, Colony has seen a gradual decrease in the cost of interest-bearing deposits from 2.36% in Q1 2024 to 2.22% in Q1 2025, reflecting the bank’s improved deposit pricing strategy as the Federal Reserve begins easing rates. This trend aligns with management’s outlook for modest margin expansion in 2025.

Forward-Looking Statements

Looking ahead, Colony Bank has outlined several short-term and long-term objectives. In the near term, the bank aims to achieve a return on assets target of 1.00%, maintain noninterest expense discipline, and focus on growing core deposits and customer relationships.

Long-term objectives include developing five complementary lines of business each generating over $1 million in net income, improving efficiency through economies of scale, achieving return on assets in the top quartile of peers, and growing the customer base by 8-12% per year.

Management expects to benefit from the Federal Reserve’s easing of rates, which should reduce pressure on deposit costs and potentially allow for restructuring of the investment portfolio to enhance returns. The bank’s focus on innovation, efficiency, and strategic acquisitions positions it well for continued growth in its core Georgia market and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.