SoFi stock falls after announcing $1.5B public offering of common stock

Compass Minerals International Inc (NYSE:CMP) released its fiscal second-quarter 2025 results on May 7, 2025, showing significant improvement in its Salt segment driven by normalized winter weather patterns, while continuing to execute on its inventory rationalization strategy. The stock responded positively, jumping 7.17% in premarket trading to $15.25.

Quarterly Performance Highlights

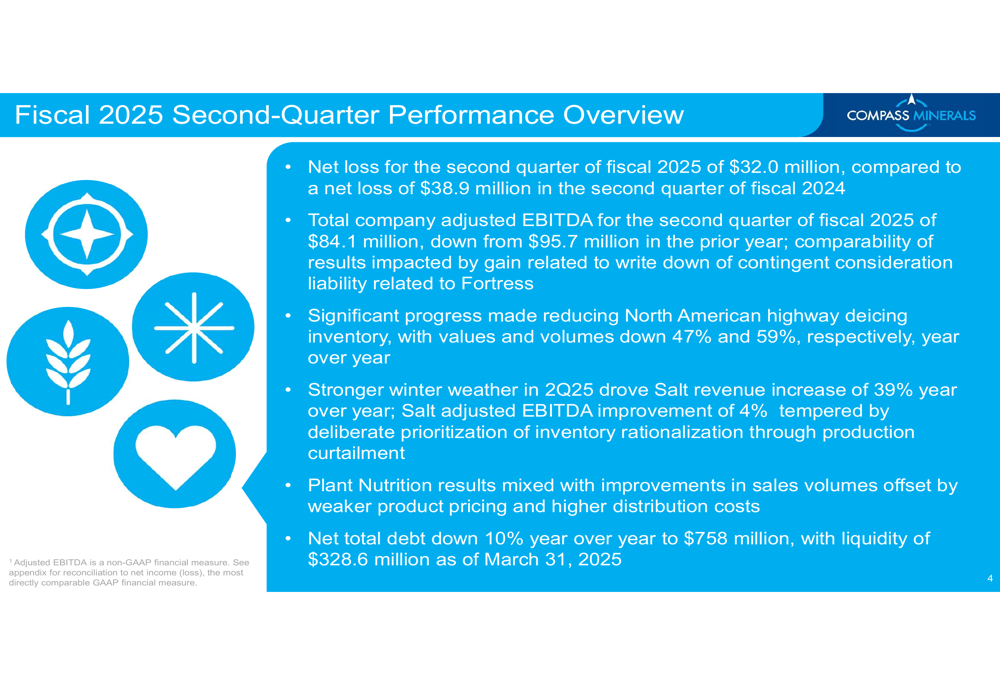

Compass Minerals reported a net loss of $32.0 million for the second quarter of fiscal 2025, an improvement from the $38.9 million loss recorded in the same period last year. Total (EPA:TTEF) company adjusted EBITDA was $84.1 million, down from $95.7 million in the prior year, though this comparison was impacted by a $7.9 million non-cash gain related to the write-down of a contingent consideration liability for Fortress.

As shown in the following overview of the company’s quarterly performance:

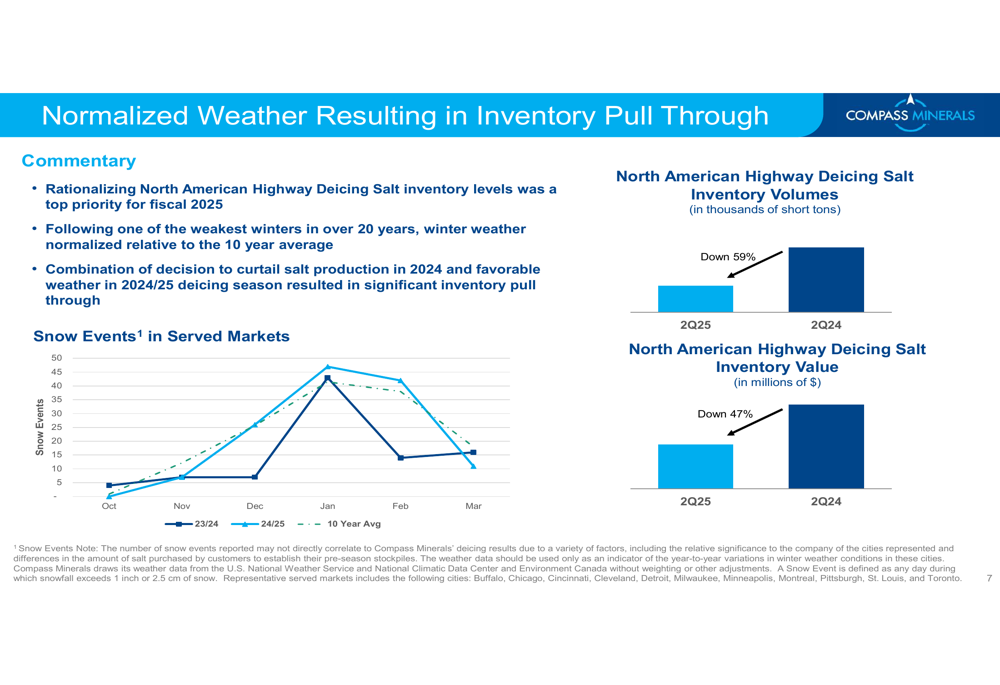

The company made significant progress in reducing its North American highway deicing inventory, with values and volumes down 47% and 59%, respectively, year over year. This inventory reduction was a key strategic priority for fiscal 2025 following one of the weakest winters in over 20 years.

Salt Segment Analysis

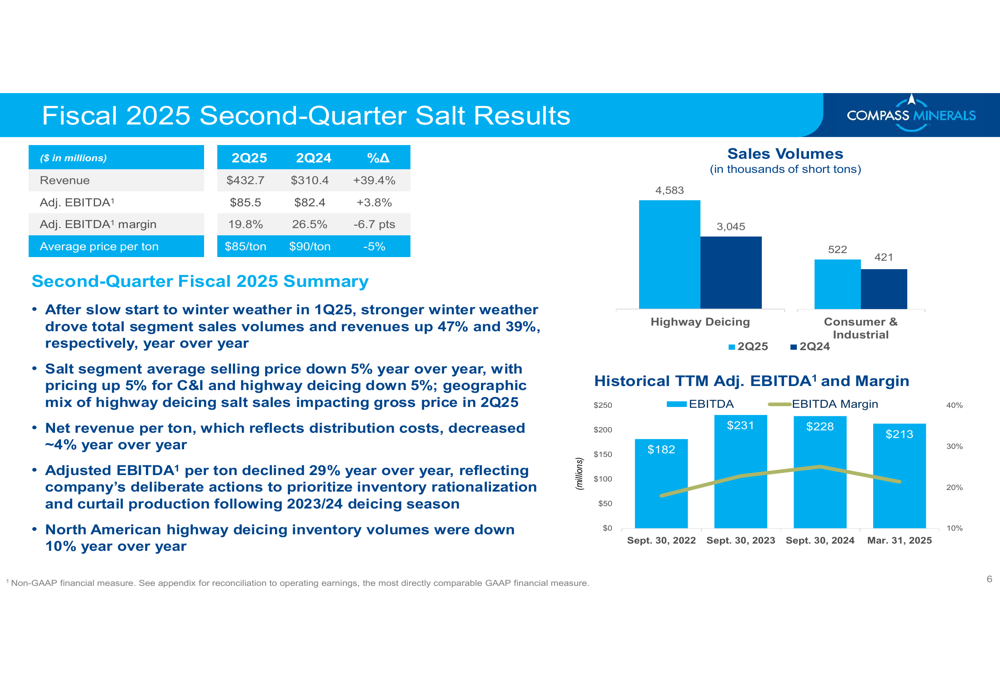

The Salt segment delivered strong results with revenue increasing 39.4% year over year to $432.7 million, driven by stronger winter weather conditions. Sales volumes rose significantly, with highway deicing volumes up 50.5% to 4.58 million tons and consumer and industrial volumes up 24% to 522,000 tons.

The detailed breakdown of the Salt segment’s performance shows both the volume growth and pricing dynamics:

Despite the revenue increase, the Salt segment’s adjusted EBITDA margin contracted to 19.8% from 26.5% in the prior year. This margin compression reflects the company’s deliberate actions to prioritize inventory rationalization and curtail production following the 2023/24 deicing season.

The normalized weather patterns played a crucial role in helping Compass Minerals achieve its inventory reduction goals:

"After a slow start to winter weather in the first quarter, stronger winter weather drove total segment sales volumes and revenues up 47% and 39%, respectively, year over year," the company noted in its presentation.

Plant Nutrition Segment Results

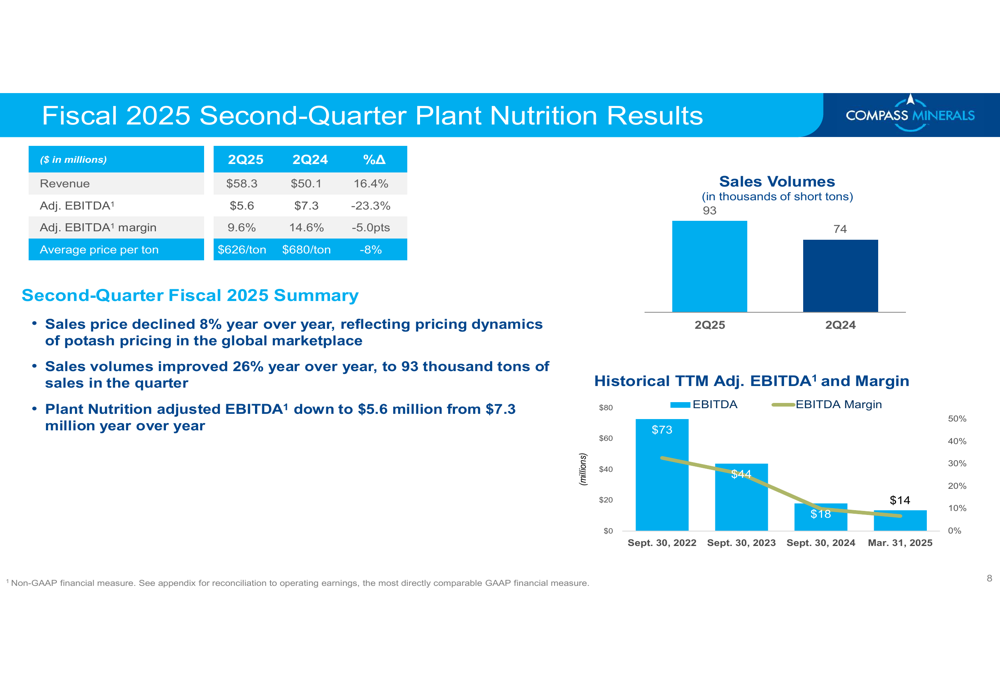

The Plant Nutrition segment delivered mixed results with revenue increasing 16.4% to $58.3 million, primarily driven by a 26% increase in sales volumes to 93,000 tons. However, average selling prices declined 8% year over year to $626 per ton, reflecting global potash pricing dynamics.

The following chart illustrates the Plant Nutrition segment’s performance:

As a result of the pricing pressure, Plant Nutrition adjusted EBITDA decreased 23.3% to $5.6 million, with the adjusted EBITDA margin contracting to 9.6% from 14.6% in the prior year.

Financial Position and Debt Management

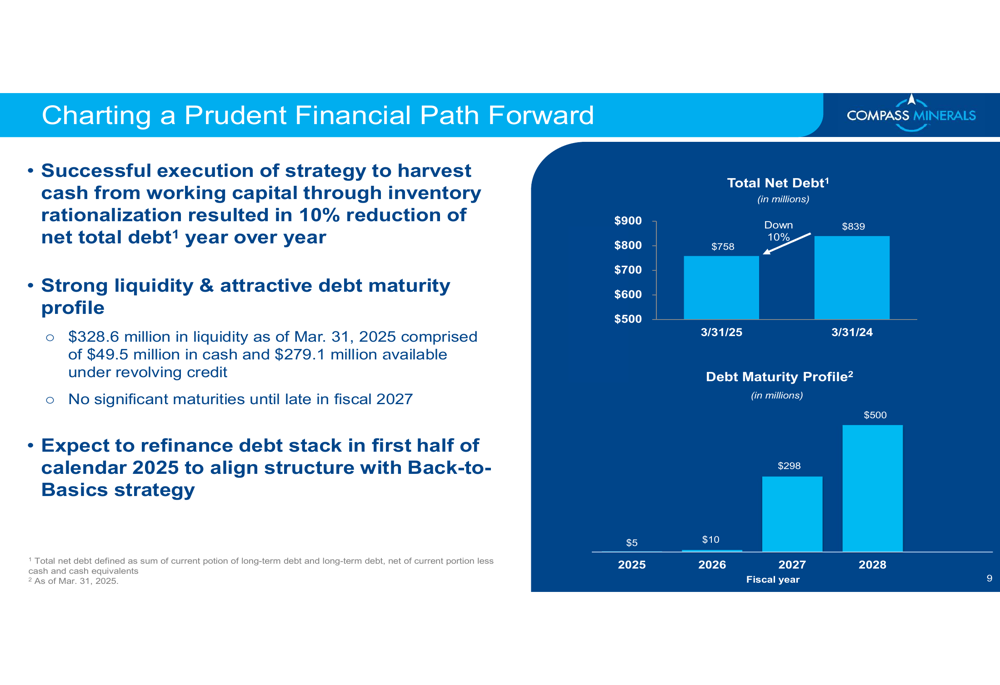

Compass Minerals has made significant progress in strengthening its financial position, with net total debt down 10% year over year to $758 million. The company reported strong liquidity of $328.6 million as of March 31, 2025, comprised of $49.5 million in cash and $279.1 million available under its revolving credit facility.

The company’s financial strategy and debt profile are illustrated below:

Management indicated plans to refinance its debt stack in the first half of calendar 2025 to better align with its "Back-to-Basics" strategy. The company has no significant debt maturities until late in fiscal 2027, providing financial flexibility in the near term.

Forward Guidance

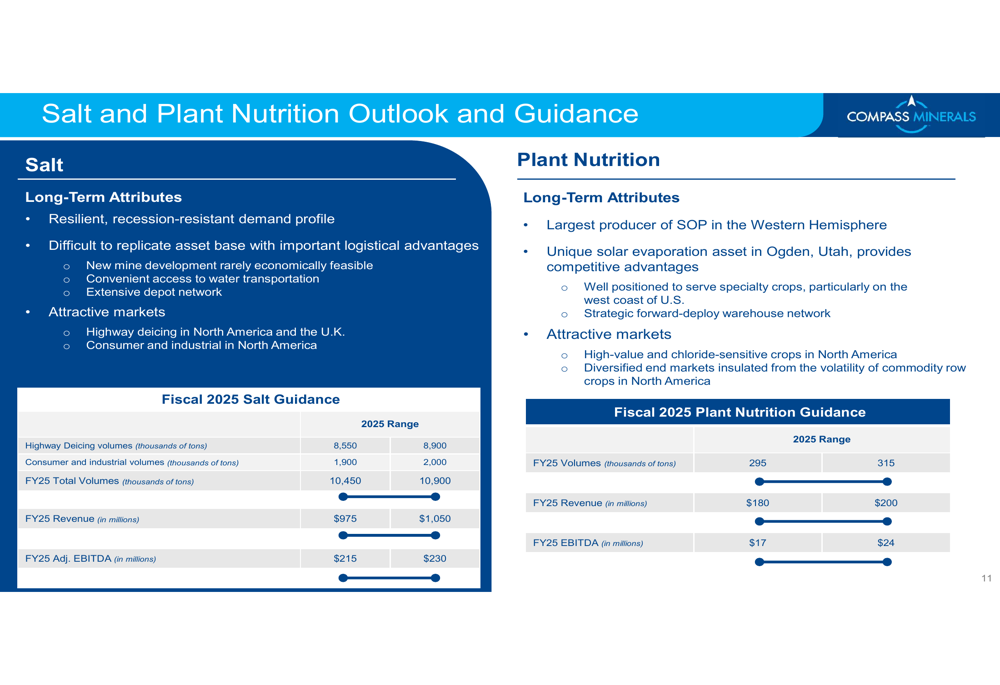

For fiscal 2025, Compass Minerals provided guidance for both its Salt and Plant Nutrition segments. The company expects Salt segment volumes to range between 10.45 million and 10.9 million tons, with revenue between $975 million and $1.05 billion and adjusted EBITDA between $215 million and $230 million.

The detailed guidance for both segments shows the company’s expectations:

For the Plant Nutrition segment, the company forecasts volumes between 295,000 and 315,000 tons, with revenue between $180 million and $200 million and adjusted EBITDA between $17 million and $24 million.

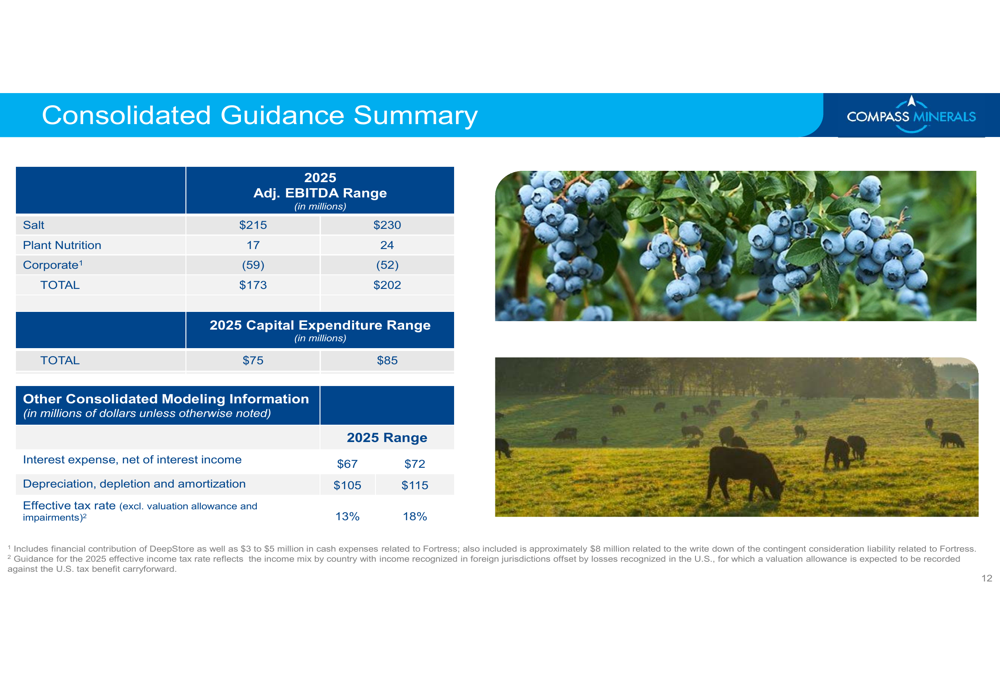

On a consolidated basis, Compass Minerals expects total adjusted EBITDA for fiscal 2025 to range between $173 million and $202 million, with capital expenditures between $75 million and $85 million.

Strategic Direction

The second-quarter results demonstrate Compass Minerals’ continued execution of the strategy outlined in its previous earnings call, where CEO Edward Dowling stated, "Our goal is to gear the company such that it generates free cash flow even in mild winters."

The successful inventory rationalization and debt reduction efforts align with this strategic focus on financial health and operational efficiency. The company continues to leverage its core strengths, including its "difficult to replicate asset base with important logistical advantages" in the Salt segment and its position as the "largest producer of SOP in the Western Hemisphere" in the Plant Nutrition segment.

With normalized winter weather patterns supporting stronger sales and continued progress on strategic initiatives, Compass Minerals appears to be navigating a path toward improved financial performance after the challenges faced in fiscal 2024.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.