Berkshire Hathaway reveals $4.3 billion stake in Alphabet, cuts Apple

Introduction & Market Context

Compass Minerals International Inc (NYSE:CMP) released its third-quarter fiscal 2025 results on August 11, 2025, showing improved performance with reduced losses and volume growth across its core business segments. The company’s stock closed at $21.44 on the day of the announcement, with a modest 0.28% gain during regular trading hours, followed by a 1.07% increase in after-hours trading.

The results come during a period of strategic focus for Compass Minerals, which has been implementing its "back-to-basics" strategy to strengthen its core salt and plant nutrition businesses while improving its financial position through debt reduction and refinancing activities.

Quarterly Performance Highlights

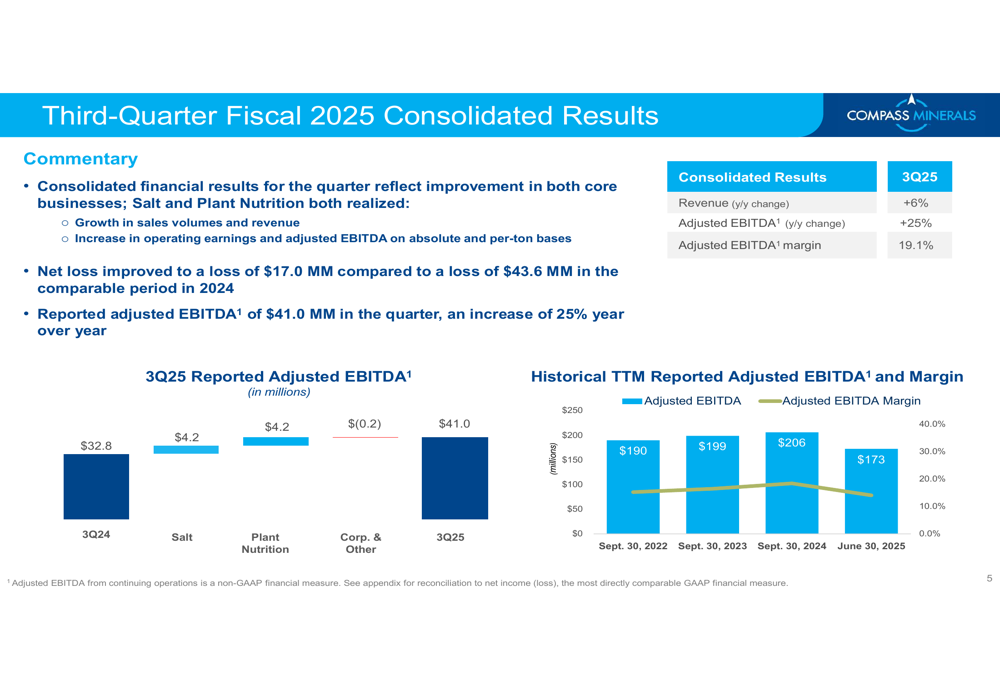

Compass Minerals reported a net loss of $17.0 million for the third quarter of fiscal 2025, a significant improvement from the $43.6 million loss recorded in the same period of fiscal 2024. Total (EPA:TTEF) company adjusted EBITDA reached $41.0 million, representing a 25% increase from $32.8 million in the prior year.

As shown in the following consolidated results chart, the company’s adjusted EBITDA margin improved to 19.1%, with both core businesses contributing to the positive momentum:

The improved performance was driven by volume growth in both the Salt and Plant Nutrition segments, with Salt sales volumes up 4% and Plant Nutrition volumes increasing by an impressive 21% year over year. These volume gains helped offset some pricing pressure, particularly in the Plant Nutrition segment where average selling prices declined by 4.7% compared to the prior year.

Segment Analysis

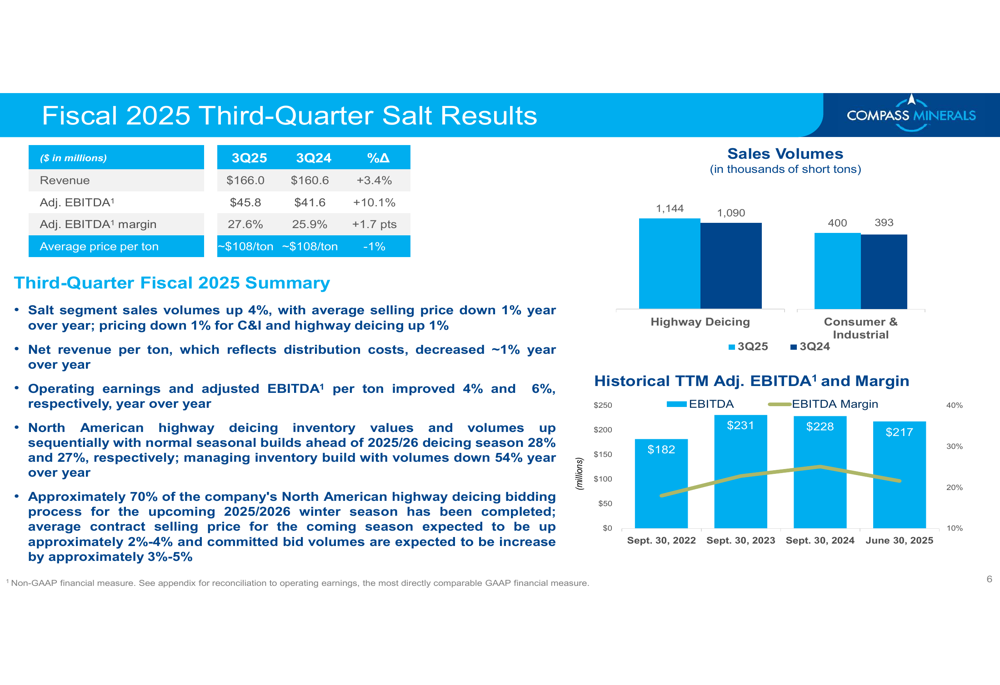

The Salt segment, which includes highway deicing and consumer & industrial products, delivered solid results with a 3.4% increase in revenue to $166.0 million and a 10.1% improvement in adjusted EBITDA to $45.8 million. The segment’s adjusted EBITDA margin expanded by 1.7 percentage points to 27.6%.

The following chart details the Salt segment’s performance metrics:

Highway deicing volumes increased to 1,144 thousand tons from 1,090 thousand tons in the prior year, while consumer & industrial volumes rose slightly to 400 thousand tons from 393 thousand tons. Despite a 1% decline in average selling price, the segment’s improved operational efficiency contributed to higher per-ton operating earnings and adjusted EBITDA.

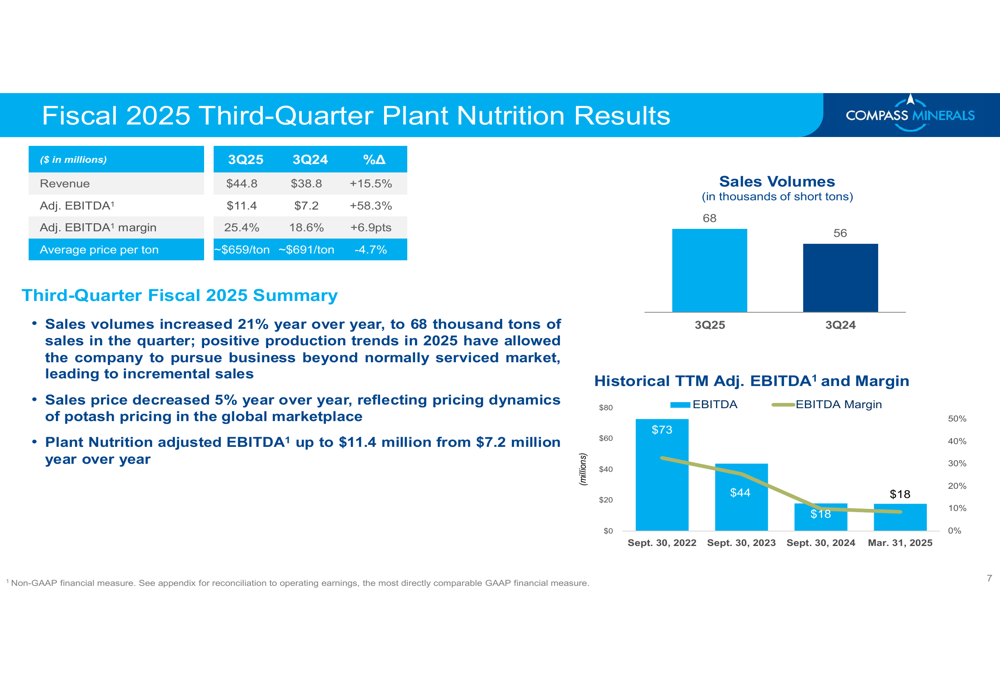

The Plant Nutrition segment showed even stronger growth, with revenue increasing by 15.5% to $44.8 million and adjusted EBITDA surging by 58.3% to $11.4 million. The segment’s adjusted EBITDA margin expanded significantly by 6.9 percentage points to 25.4%.

The following chart illustrates the Plant Nutrition segment’s performance:

The substantial 21% increase in Plant Nutrition sales volumes to 68 thousand tons offset the 4.7% decline in average selling price, resulting in overall revenue growth. This volume-driven performance reflects the company’s focus on serving high-value and chloride-sensitive crop markets in North America.

Financial Position and Debt Management

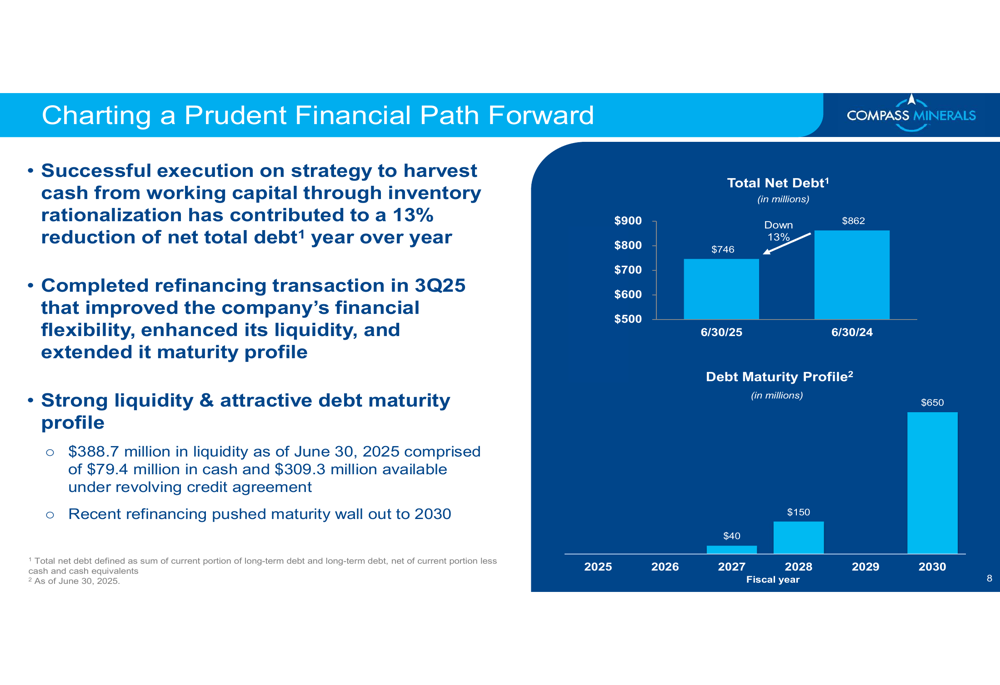

Compass Minerals continued to strengthen its financial position during the quarter, reducing its net total debt by 13% year over year to $746 million as of June 30, 2025. The company reported liquidity of $389 million, comprising $79.4 million in cash and $309.3 million available under its revolving credit agreement.

The company’s debt management strategy is illustrated in the following chart:

During the third quarter, Compass Minerals completed refinancing activities that improved its financial flexibility, enhanced liquidity, and extended its debt maturity profile. The refinancing resulted in a more balanced maturity schedule with $40 million due in 2027, $150 million in 2028, and $650 million in 2030.

The company recognized a $7.6 million loss on extinguishment of debt related to these refinancing activities, as noted in the reconciliation for adjusted EBITDA.

Outlook & Guidance

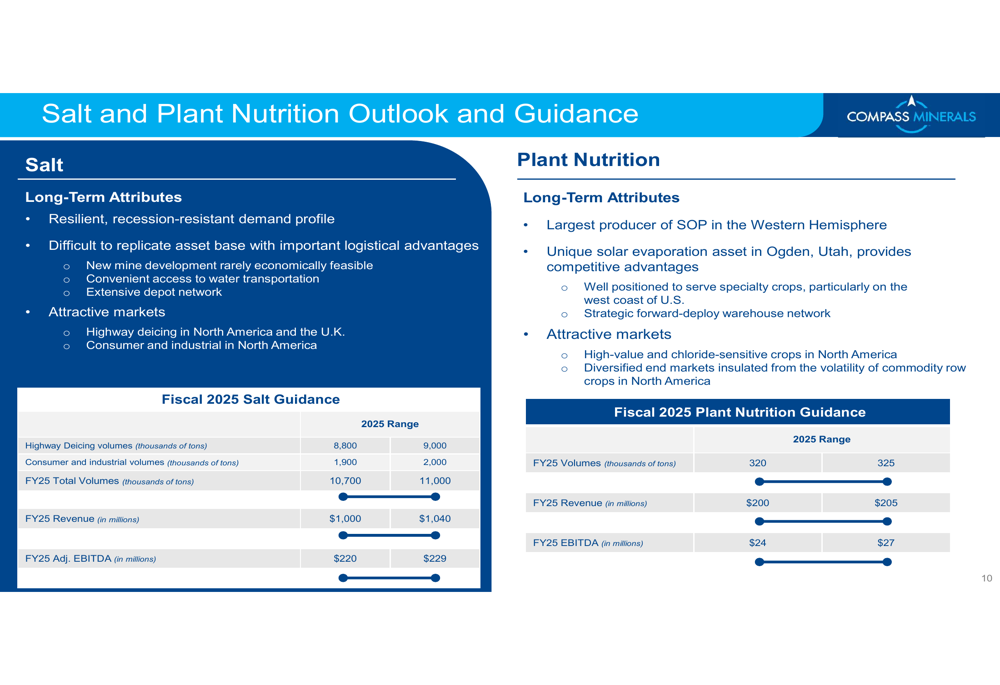

Looking ahead, Compass Minerals provided guidance for fiscal year 2025, maintaining its previous outlook for both core business segments. For the Salt segment, the company expects total volumes of 10,700-11,000 thousand tons, revenue of $1,000-1,040 million, and adjusted EBITDA of $220-229 million.

The following chart details the company’s outlook and guidance for both segments:

For the Plant Nutrition segment, Compass Minerals forecasts volumes of 320-325 thousand tons, revenue of $200-205 million, and adjusted EBITDA of $24-27 million. On a consolidated basis, the company expects total adjusted EBITDA of $185-201 million for fiscal year 2025.

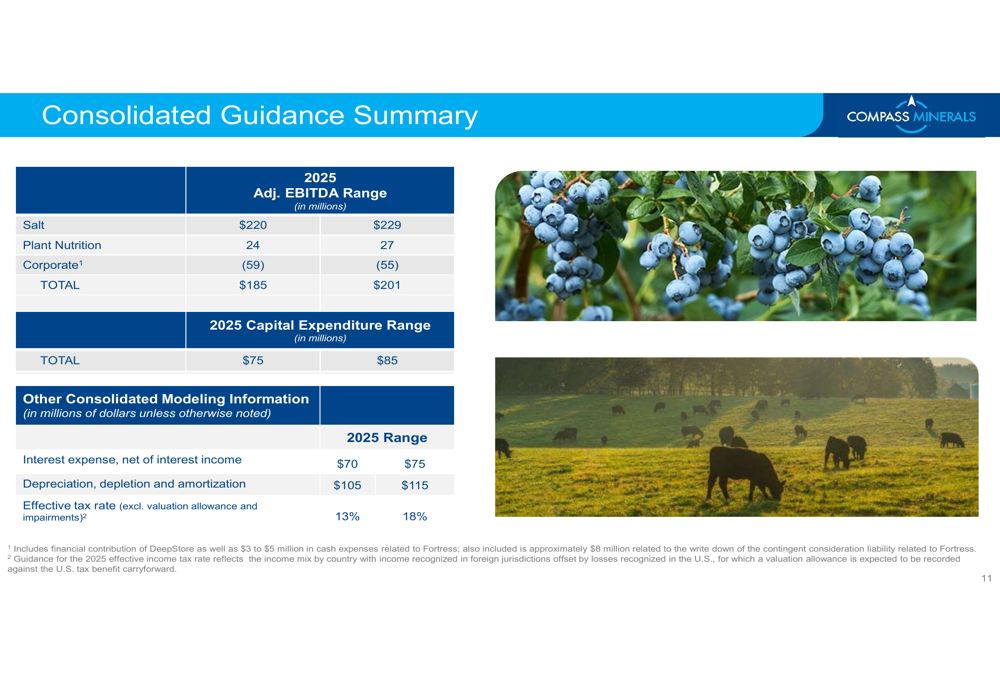

The consolidated guidance summary provides additional details on capital expenditures and other financial metrics:

Capital expenditures are projected to be $75-85 million for fiscal year 2025, while interest expense is expected to range from $70-75 million. The company anticipates an effective tax rate of 13-18% (excluding valuation allowance and impairments) and depreciation, depletion, and amortization of $105-115 million.

Compass Minerals continues to emphasize its competitive advantages, including its "difficult to replicate asset base with important logistical advantages" in the Salt segment and its position as the "largest producer of SOP in the Western Hemisphere" in the Plant Nutrition segment. These strategic assets, combined with the company’s focus on operational efficiency and debt reduction, position Compass Minerals to continue its recovery trajectory in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.