Hedge funds are buying these two big tech stocks while selling two rivals

Introduction & Market Context

ConocoPhillips (NYSE:COP) delivered a mixed financial performance in its third quarter of 2025, according to the company's earnings presentation released on November 6. The oil and gas major reported adjusted earnings per share (EPS) of $1.61, exceeding analyst expectations of $1.45, despite revenue falling short of forecasts at $14.55 billion versus the anticipated $14.78 billion.

The company's presentation comes amid a challenging price environment for energy producers, with Brent crude averaging $69.07 per barrel and WTI at $64.93 during the quarter – significantly below year-ago levels. Natural gas prices also remained under pressure, with Henry Hub averaging $3.07/MMBTU. Despite these headwinds, ConocoPhillips managed to deliver solid operational results while advancing key strategic projects.

Quarterly Performance Highlights

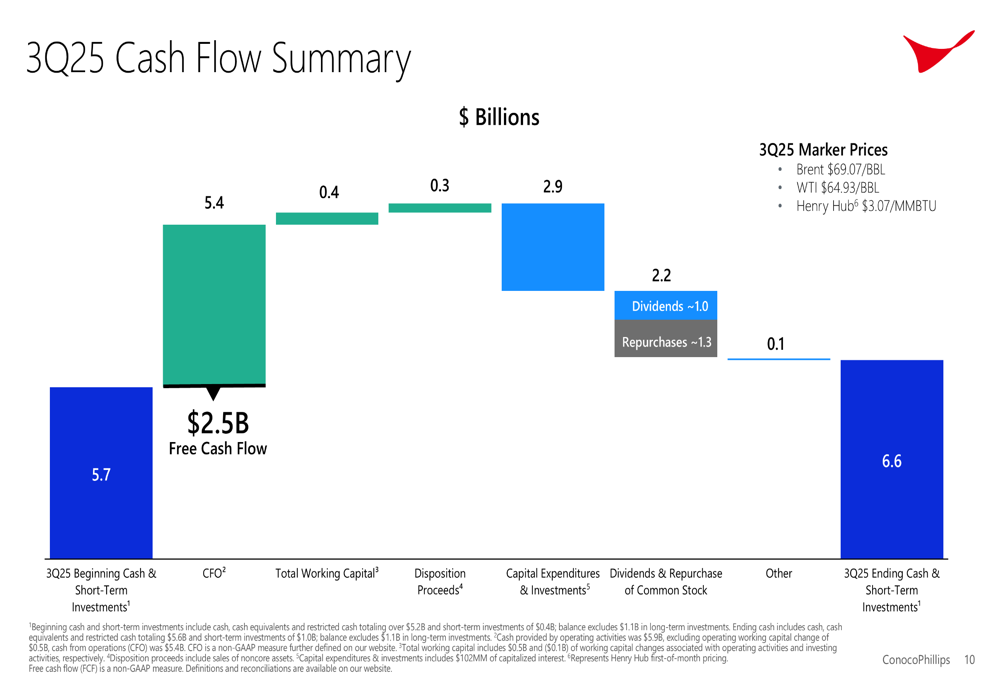

ConocoPhillips reported third-quarter production exceeding the high end of guidance at 2,330-2,370 thousand barrels of oil equivalent per day (MBOED). The company generated $5.4 billion in cash from operations and $2.5 billion in free cash flow, ending the quarter with $6.6 billion in cash on hand.

As shown in the following quarterly earnings summary:

Adjusted earnings reached $2,007 million ($1.61 per share), up from $1,793 million ($1.42 per share) in Q2 2025, though down from $2,081 million ($1.78 per share) in Q3 2024. The sequential improvement was driven by lower operating costs, increased prices, and higher volumes, partially offset by a higher effective tax rate. Year-over-year, lower prices were offset by production gains from the Marathon Oil acquisition.

The company's cash flow performance remained robust throughout the quarter:

ConocoPhillips returned $2.2 billion to shareholders during Q3, including approximately $1.3 billion in share repurchases and $1 billion in dividends. The company also announced an 8% increase in its quarterly dividend to 84 cents per share. Additionally, ConocoPhillips closed the Anadarko acquisition and signed $0.5 billion in noncore dispositions, exceeding its $3 billion asset sales target for 2025.

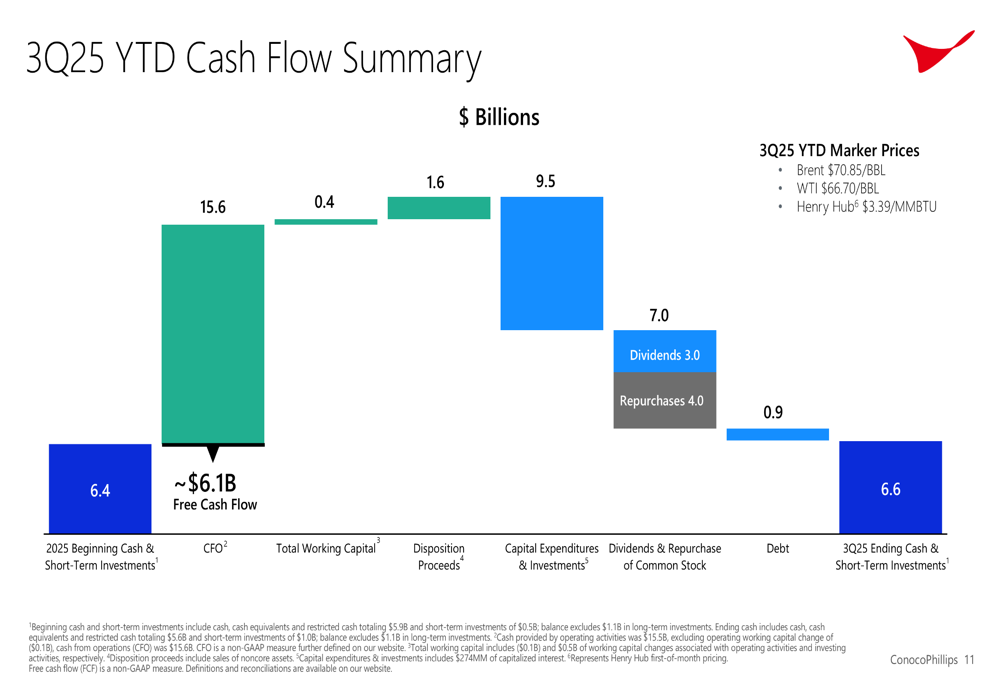

Year-to-date cash flow performance further demonstrates the company's financial strength:

Strategic Initiatives

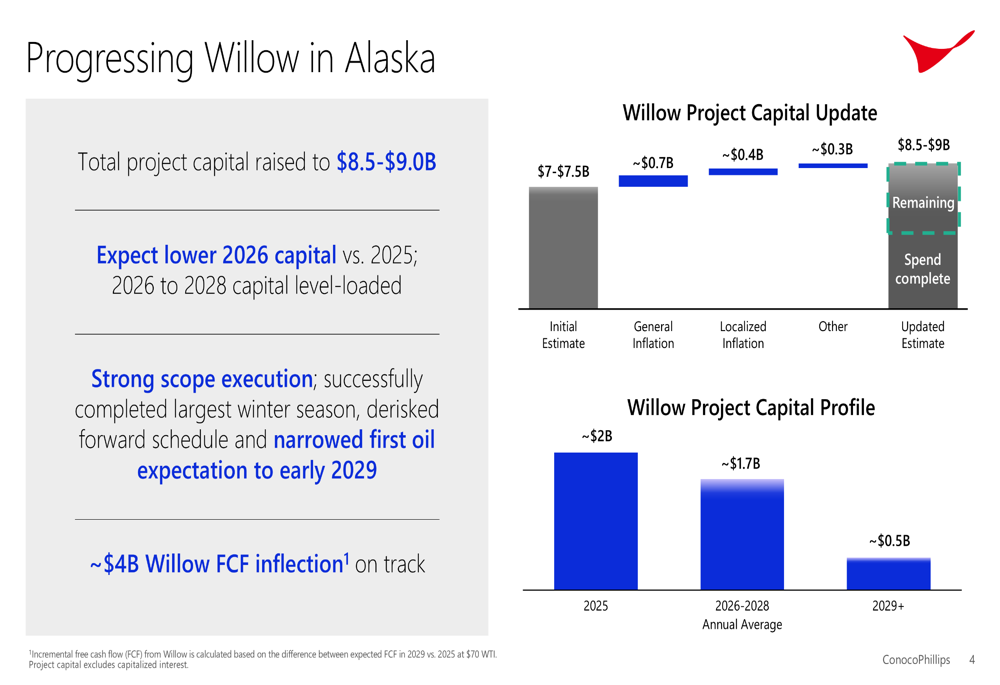

The Willow project in Alaska represents one of ConocoPhillips' most significant growth initiatives, though the company has updated its capital requirements:

Total project capital for Willow has increased to $8.5-$9.0 billion, up from the initial estimate of $7-$7.5 billion. This increase includes approximately $0.7 billion for general inflation, $0.4 billion for localized inflation, and $0.3 billion for other factors. Despite the cost increases, ConocoPhillips has narrowed its first oil expectation to early 2029 and anticipates a $4 billion free cash flow inflection once the project is online.

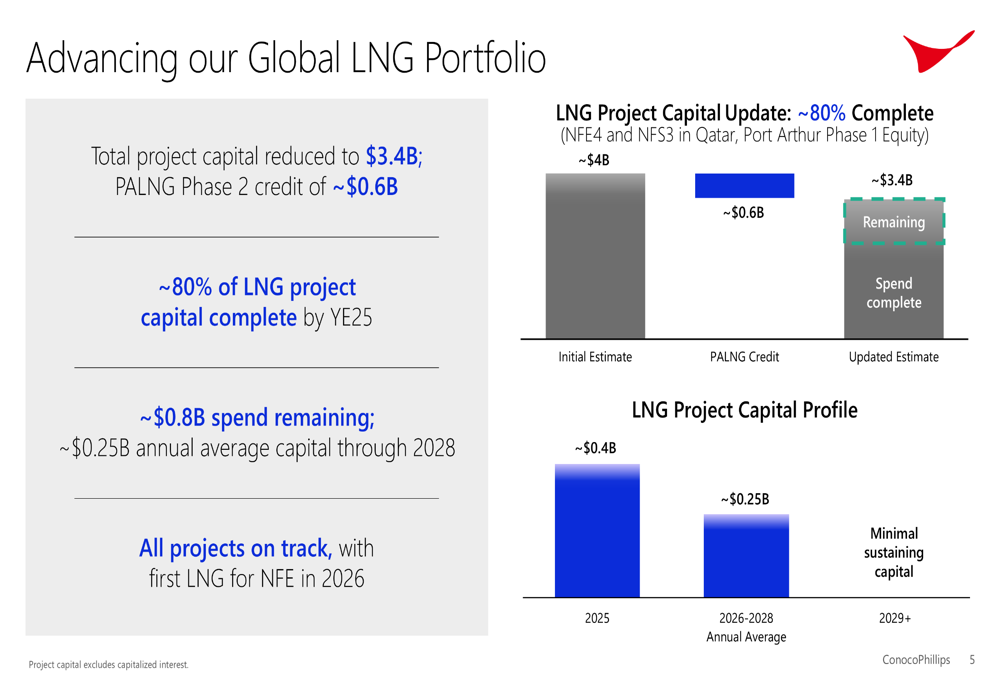

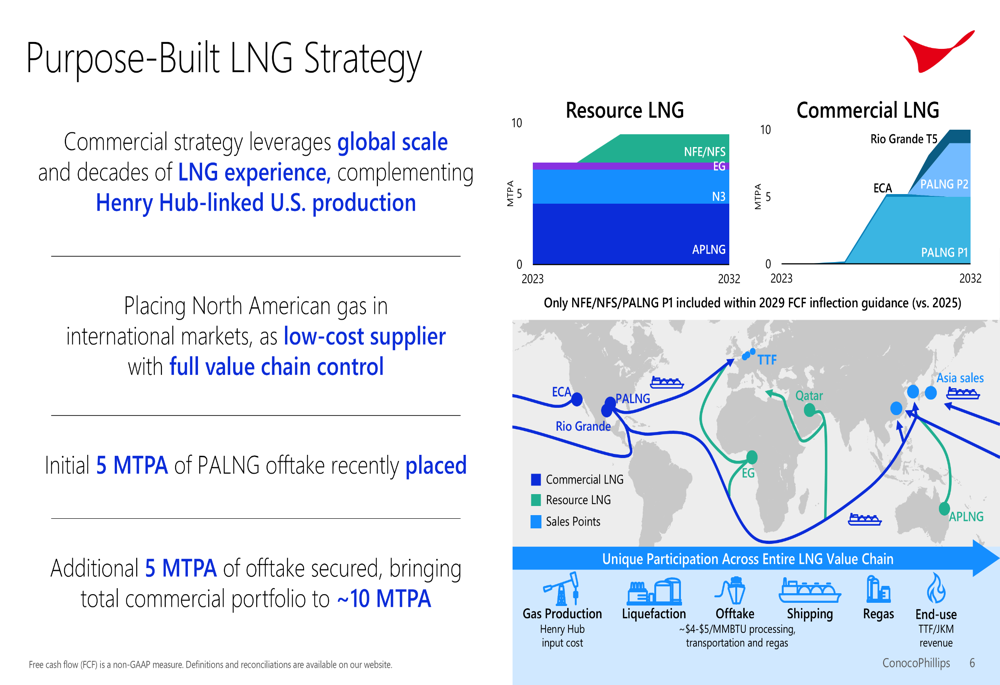

On the LNG front, ConocoPhillips is making significant progress with its global portfolio:

The company has reduced its total LNG project capital to $3.4 billion, reflecting a Port Arthur LNG Phase 2 credit of approximately $0.6 billion. By year-end 2025, about 80% of LNG project capital will be complete, with all projects on track and first LNG for New Fortress Energy expected in 2026.

ConocoPhillips has also advanced its commercial LNG strategy:

The company recently placed its initial 5 MTPA of Port Arthur LNG offtake and secured an additional 5 MTPA, bringing its total commercial portfolio to approximately 10 MTPA. This strategy leverages ConocoPhillips' global scale and decades of LNG experience to place North American gas in international markets as a low-cost supplier with full value chain control.

Forward-Looking Statements

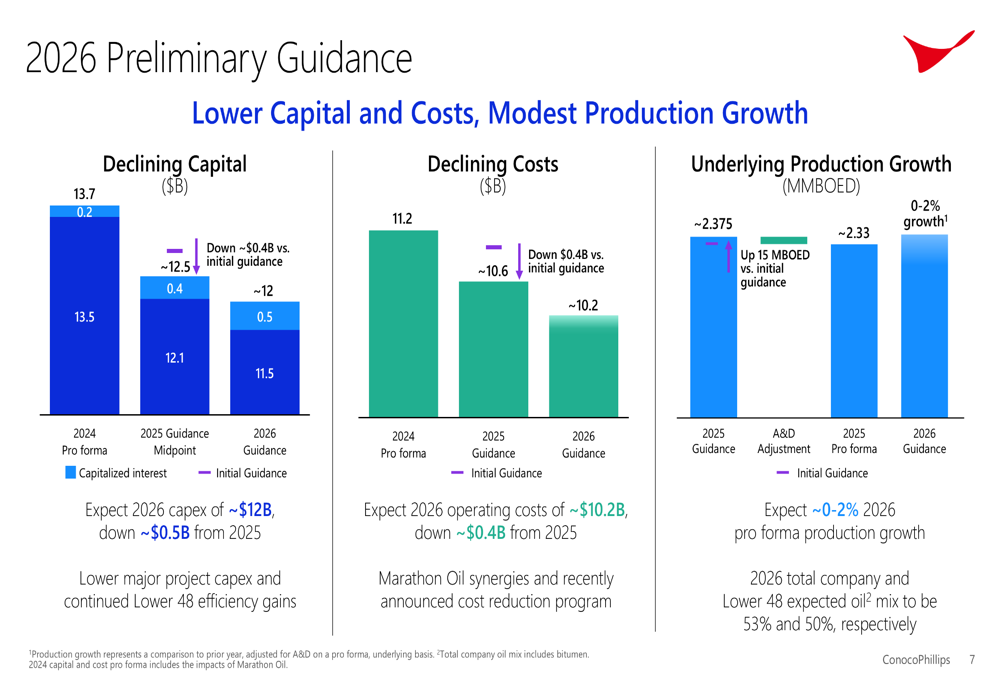

Looking ahead to 2026, ConocoPhillips provided preliminary guidance showing continued operational discipline:

The company expects capital expenditures of approximately $12 billion in 2026, down about $0.5 billion from 2025 levels. Operating costs are also projected to decline to approximately $10.2 billion, a $0.4 billion reduction from 2025. Production growth is expected to be modest at 0-2% on a pro forma basis.

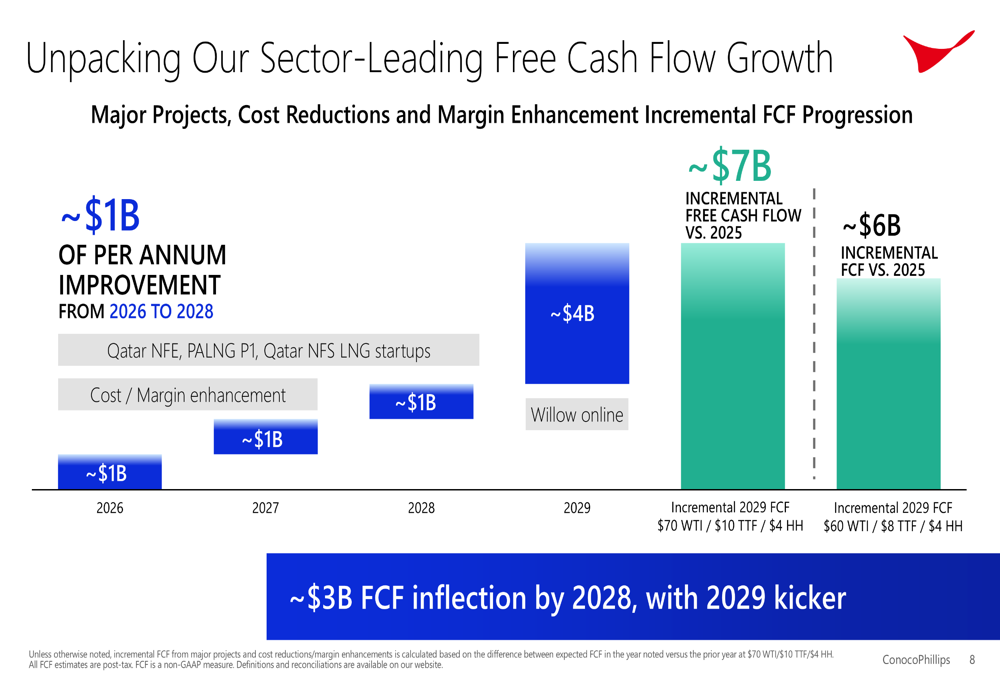

ConocoPhillips outlined its path to significant free cash flow growth over the coming years:

The company anticipates approximately $1 billion of annual free cash flow improvement from 2026 through 2028, driven by Qatar NFE, Port Arthur LNG Phase 1, Qatar NFS LNG startups, and cost/margin enhancements. By 2029, with the Willow project online, ConocoPhillips projects approximately $7 billion in incremental free cash flow compared to 2025 levels.

Market Reaction and Analyst Perspectives

Despite the earnings beat and positive long-term outlook, ConocoPhillips' stock showed a slight pre-market decline of 0.07% following the earnings release, closing at $87.64, down 1.23% from the previous close. The stock remains within its 52-week range of $79.88 to $115.38.

Market analysts have focused particularly on the cost increases for the Willow project, though management maintains that the project remains on schedule. Questions during the earnings call also addressed the company's exploration strategy and its focus on converting North American gas to international pricing.

CEO Ryan Lance emphasized the company's strategic positioning during the call, stating, "We are a resource-rich company in a resource-starved world," while CFO Andy O'Brien highlighted the company's LNG strategy as a key differentiator in the market.

As ConocoPhillips continues to execute on its major projects and cost reduction initiatives, investors will be watching closely to see if the projected free cash flow growth materializes and translates into enhanced shareholder returns in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.