Berkshire Hathaway reveals $4.3 billion stake in Alphabet, cuts Apple

Introduction & Market Context

Corpay Inc (CPAY) presented its third quarter 2025 earnings results on November 5, revealing strong financial performance across key metrics. The payment solutions provider reported 14% year-over-year growth in both revenue and earnings per share, slightly exceeding analyst expectations. Following the announcement, Corpay’s stock saw a modest 0.2% increase in after-hours trading, with shares closing at $261.17, well within its 52-week range of $252.84 to $400.81.

The company’s performance comes amid an evolving payments landscape, where strategic acquisitions and technological innovation are increasingly important competitive differentiators. Corpay’s focus on corporate payments and emerging technologies like stablecoins positions it to capitalize on shifting industry dynamics.

Quarterly Performance Highlights

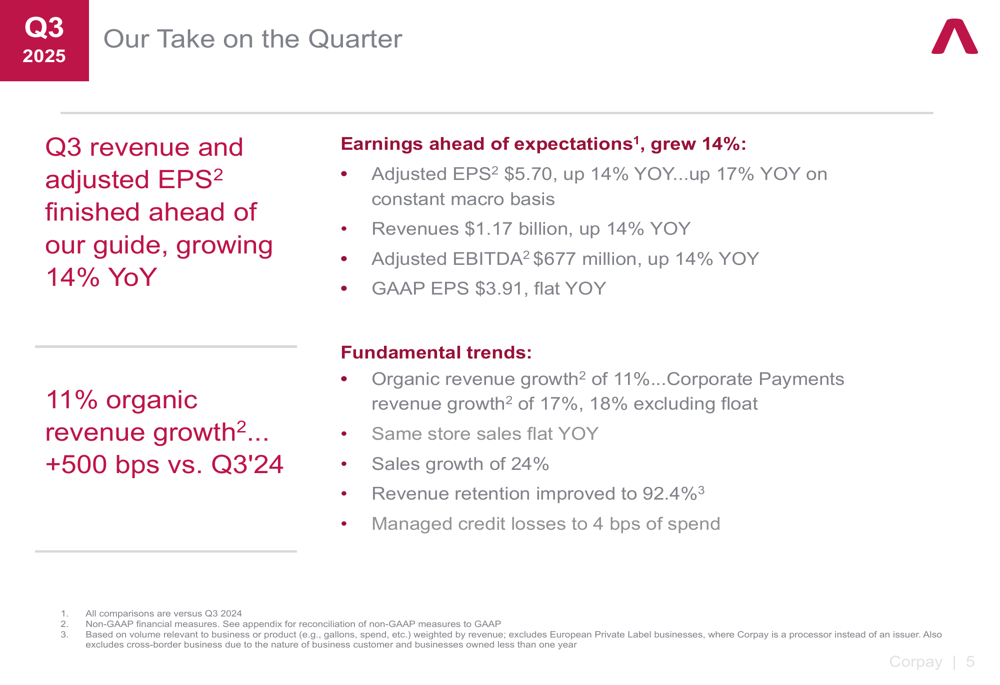

Corpay reported adjusted earnings per share of $5.70 in Q3 2025, up 14% year-over-year, on revenues of $1.17 billion, which also increased 14% compared to the same period last year. Adjusted EBITDA reached $677 million, maintaining the 14% growth trend across key financial metrics.

As shown in the following performance highlights chart:

The company achieved 11% organic revenue growth, representing a 500 basis point improvement compared to Q3 2024. This growth was primarily driven by the Corporate Payments segment, which grew 17% organically. Other notable metrics include sales growth of 24% and improved revenue retention at 92.4%, while credit losses were managed to just 4 basis points of spend.

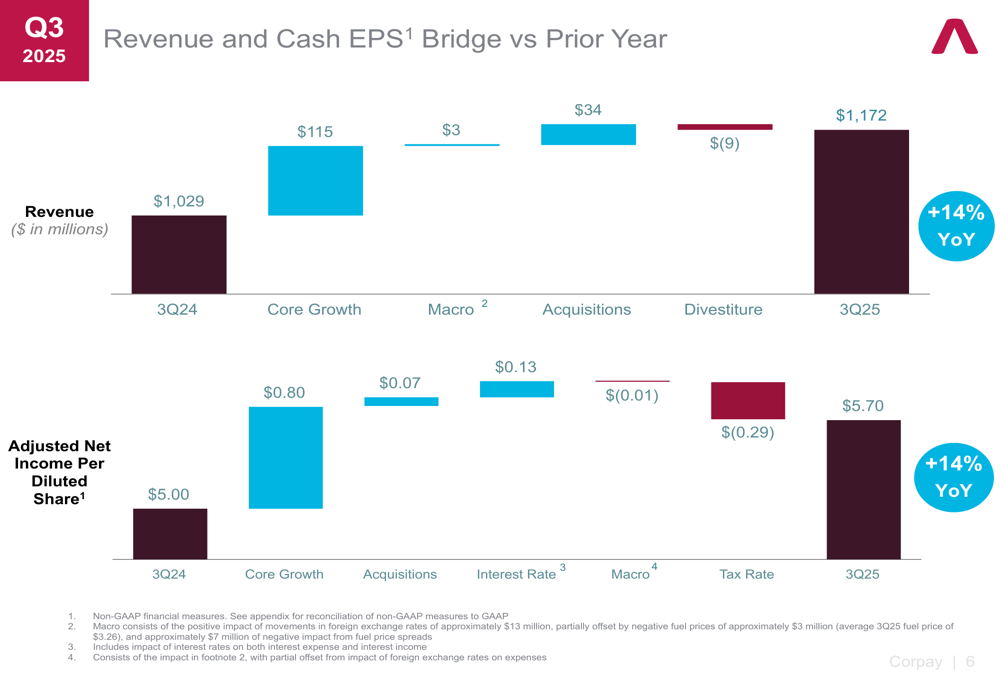

A detailed bridge analysis reveals the key factors contributing to Corpay’s year-over-year growth in both revenue and earnings per share:

Core growth was the primary driver for both revenue and EPS improvement, contributing $115 million to revenue and $0.80 to EPS. Acquisitions added $34 million to revenue and $0.07 to EPS, while interest rate impacts provided a $0.13 boost to EPS. These positive factors were partially offset by tax rate changes, which reduced EPS by $0.29.

Segment Performance Analysis

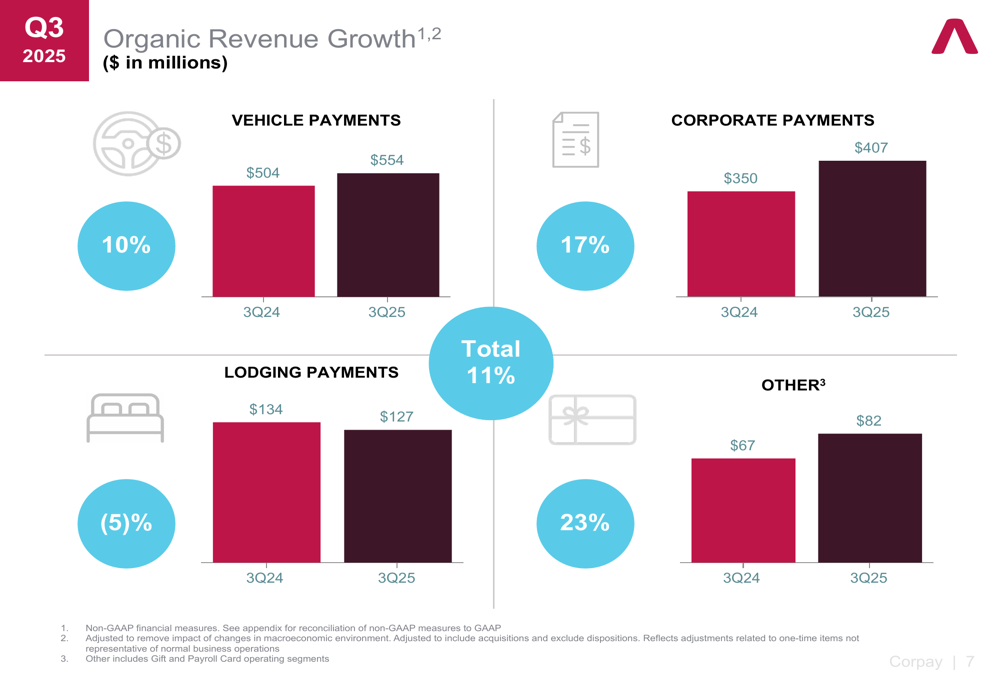

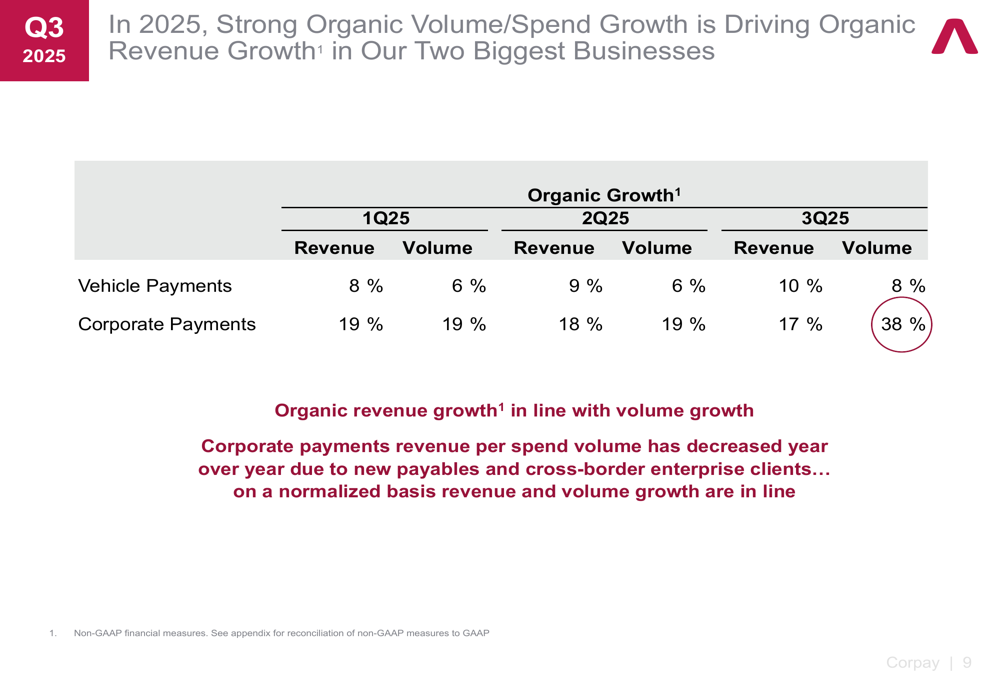

Corpay’s business segments showed varied performance, with Corporate Payments emerging as the standout performer. The segment breakdown reveals the following organic revenue growth rates:

Vehicle Payments, the company’s largest segment, delivered 10% organic revenue growth, reaching $554 million in Q3 2025 compared to $504 million in Q3 2024. Corporate Payments demonstrated the strongest performance with 17% growth, increasing from $350 million to $407 million. The Lodging Payments segment was the only one to contract, declining 5% from $134 million to $127 million.

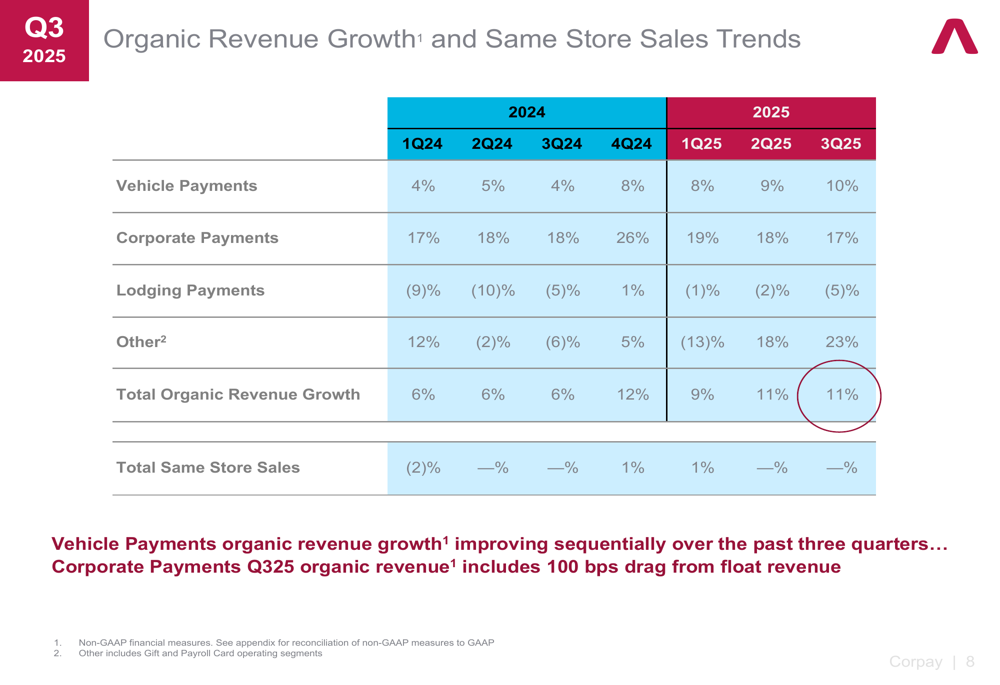

Looking at longer-term trends, Corpay has maintained consistent organic revenue growth across multiple quarters:

The company’s Vehicle Payments segment has shown sequential improvement throughout 2025, while Corporate Payments has maintained strong double-digit growth despite a 100 basis point drag from float revenue in Q3 2025.

Volume and spend metrics further illustrate the drivers behind Corpay’s revenue growth:

Corporate Payments showed particularly impressive volume growth of 38% in Q3 2025, though the company noted that revenue per spend volume has decreased year-over-year due to new payables and cross-border enterprise clients.

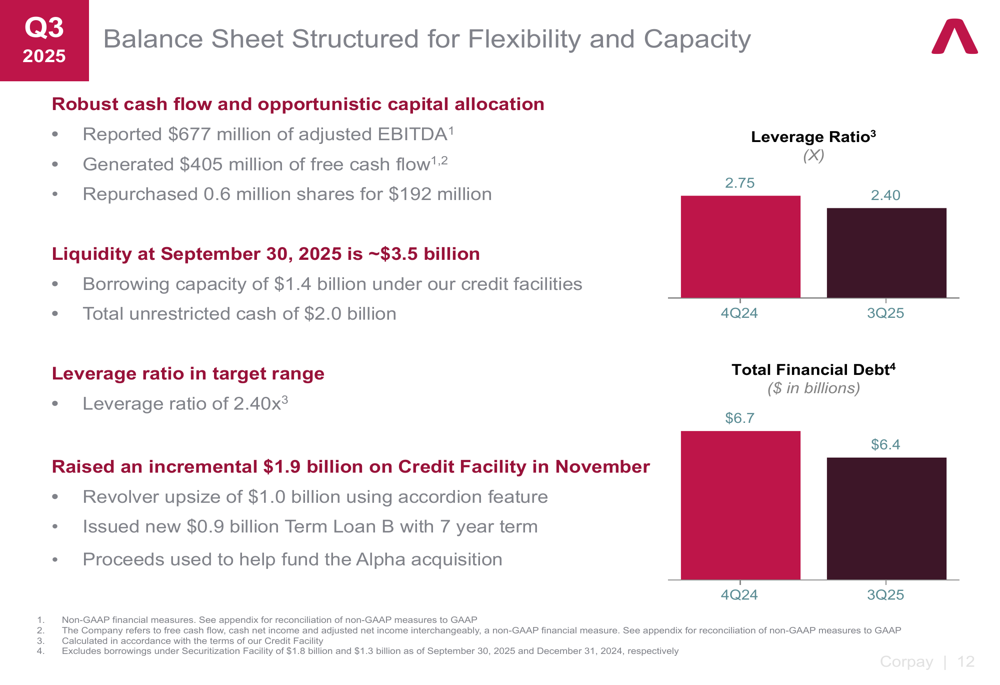

Financial Position & Balance Sheet

Corpay highlighted its strong balance sheet and financial flexibility, which provides capacity for continued strategic investments:

The company reported $677 million of adjusted EBITDA and generated $405 million of free cash flow in the quarter. Total liquidity stood at $3.5 billion as of September 30, 2025, including $1.4 billion of borrowing capacity and $2.0 billion of unrestricted cash. The leverage ratio improved to 2.40x, down from 2.75x in Q4 2024, placing it within the company’s target range.

Strategic Initiatives

Corpay outlined several strategic initiatives aimed at driving future growth, with particular emphasis on acquisitions, investments, and emerging technologies.

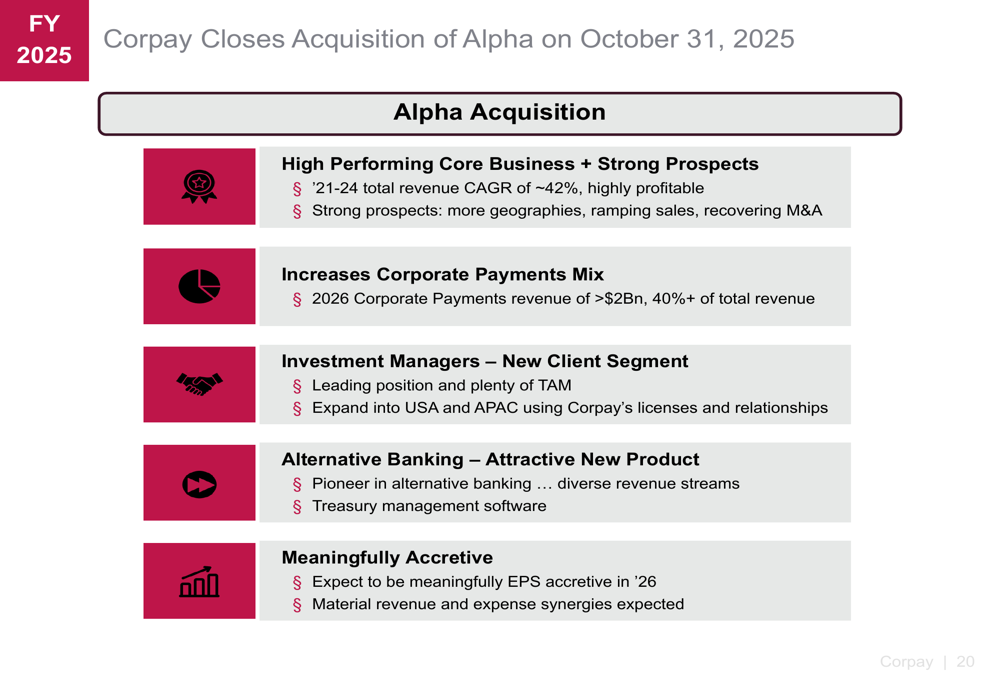

The company detailed its recent acquisition of Alpha, which is expected to enhance its corporate payments business:

The Alpha acquisition brings a high-performing core business with a 42% CAGR from 2021-2024 and increases Corpay’s corporate payments mix, with 2026 corporate payments revenue projected to exceed $2 billion, representing over 40% of total revenue. The acquisition also provides entry into the investment managers segment and adds alternative banking capabilities.

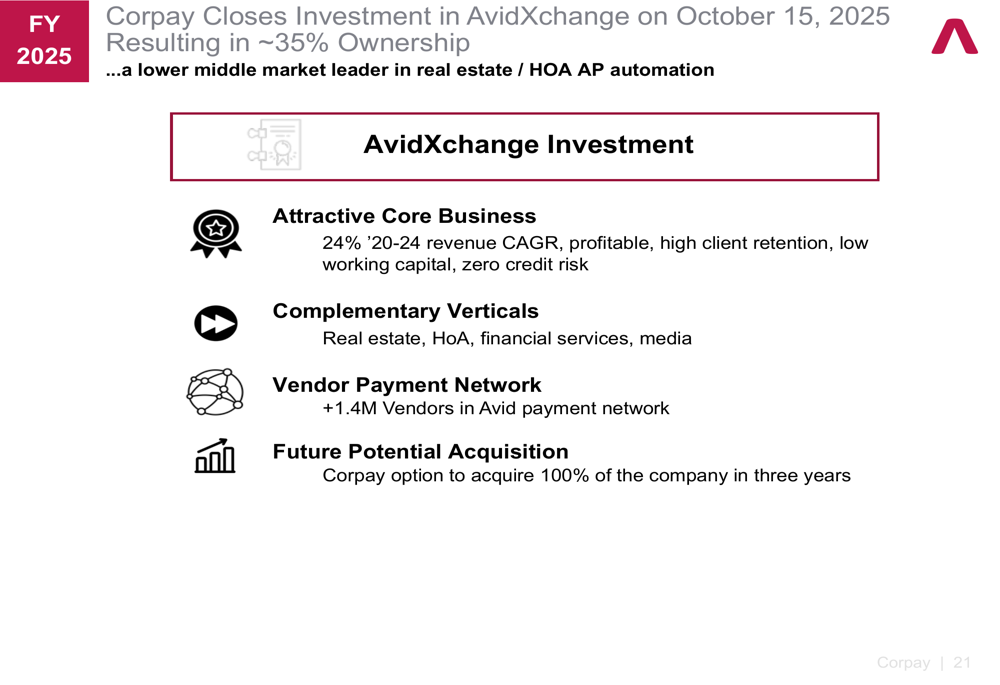

Additionally, Corpay highlighted its strategic investment in AvidXchange:

The AvidXchange investment provides access to an attractive business with 24% revenue CAGR from 2020-2024, complementary verticals, and a vendor payment network of over 1.4 million vendors. Notably, Corpay has secured an option to acquire 100% of the company in three years.

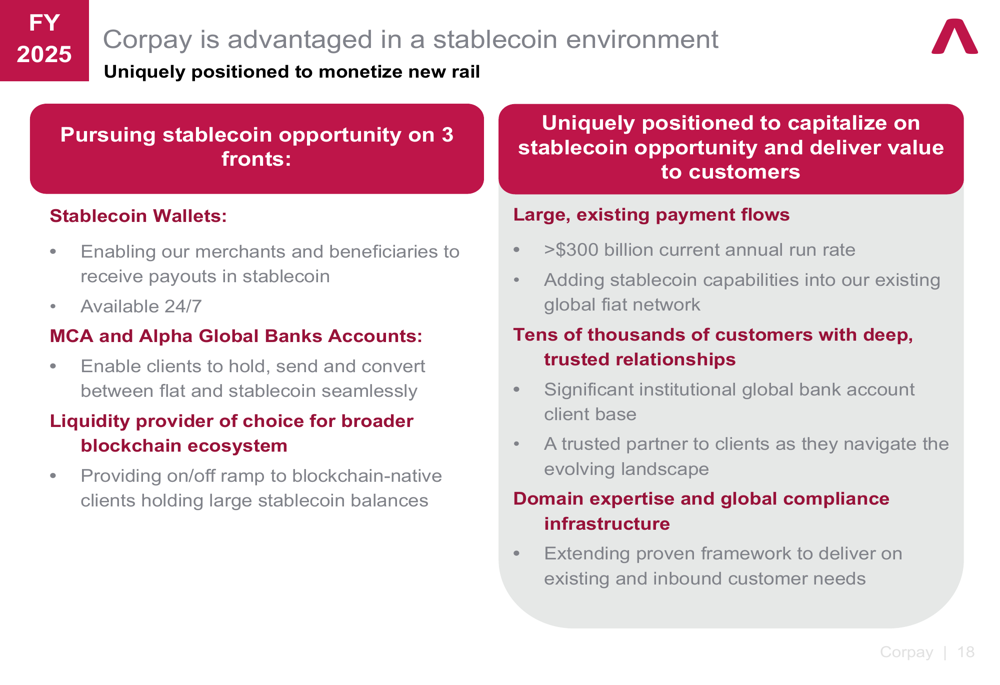

On the technology front, Corpay is pursuing opportunities in the stablecoin space:

The company’s three-pronged stablecoin strategy includes enabling stablecoin wallets for merchants and beneficiaries, integrating stablecoin capabilities into MCA and Alpha Global Banks Accounts, and positioning as a liquidity provider for the broader blockchain ecosystem. Corpay believes its existing payment flows (exceeding $300 billion annual run rate) and customer relationships provide a strong foundation for this initiative.

Forward-Looking Statements

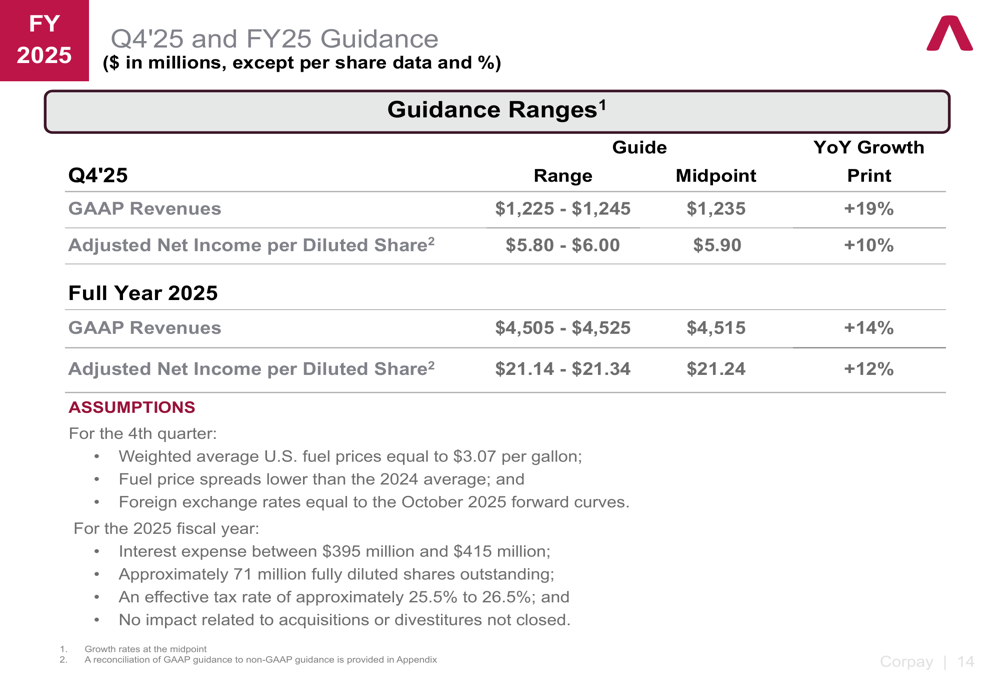

Corpay provided guidance for Q4 2025 and the full fiscal year, as well as a preliminary outlook for 2026:

For Q4 2025, the company projects GAAP revenues of $1,225-$1,245 million (19% YoY growth at midpoint) and adjusted net income per diluted share of $5.80-$6.00 (10% YoY growth at midpoint). Full-year 2025 guidance includes GAAP revenues of $4,505-$4,525 million (14% growth) and adjusted net income per diluted share of $21.14-$21.34 (12% growth).

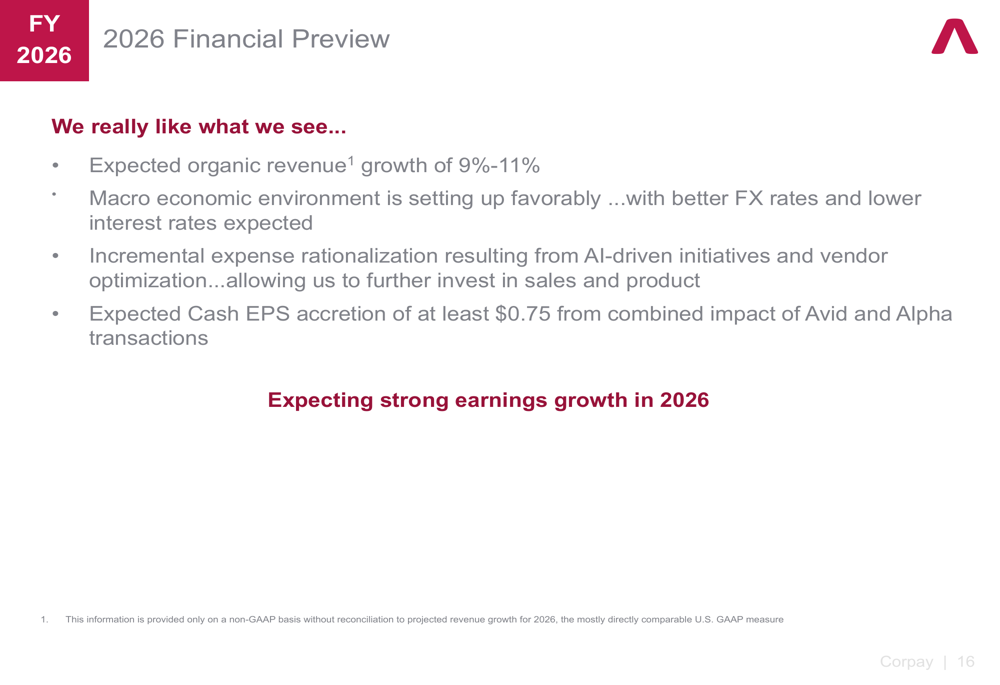

Looking ahead to 2026, Corpay provided this financial preview:

The company expects organic revenue growth of 9%-11% in 2026, supported by an improved macroeconomic environment with better FX rates and lower interest rates. Expense rationalization through AI-driven initiatives and vendor optimization is anticipated to contribute to profitability, while the combined impact of the Avid and Alpha transactions is expected to provide cash EPS accretion of at least $0.75.

Conclusion

Corpay’s Q3 2025 presentation demonstrates strong financial performance across key metrics, with particular strength in the Corporate Payments segment. The company’s strategic acquisitions and investments position it for continued growth in 2026 and beyond, while initiatives in emerging areas like stablecoins represent potential new revenue streams.

With consistent organic revenue growth, improving customer retention, and a strong balance sheet, Corpay appears well-positioned to execute its growth strategy. However, investors should monitor the integration of recent acquisitions and the company’s ability to maintain growth momentum in an increasingly competitive payments landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.