CCH Holdings prices IPO at $4 per share on NASDAQ

Introduction & Market Context

CPI Card Group Inc (NASDAQ:PMTS) presented its first quarter 2025 results on May 7, revealing a mixed financial performance characterized by strong revenue growth but compressed margins. The payment solutions provider’s stock fell 4.7% in premarket trading to $24.15, reflecting investor concerns about profitability despite the company’s strategic expansion efforts.

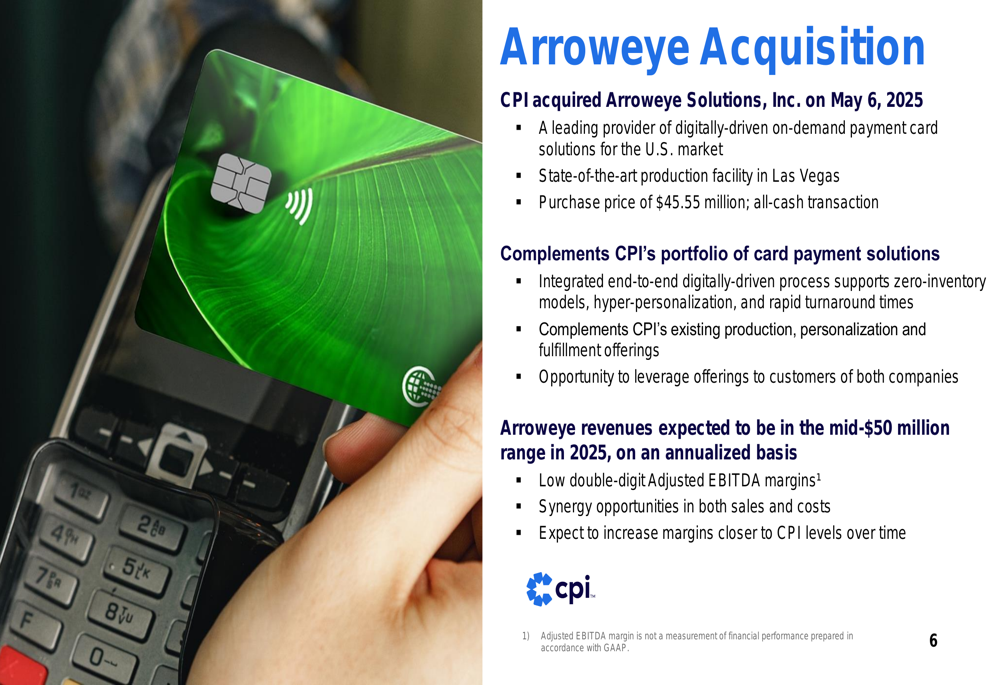

The quarter was marked by the significant acquisition of Arroweye Solutions for $45.55 million, announced just one day prior to the earnings presentation. This all-cash transaction represents a strategic move to enhance CPI’s on-demand payment card capabilities and expand its addressable market.

Quarterly Performance Highlights

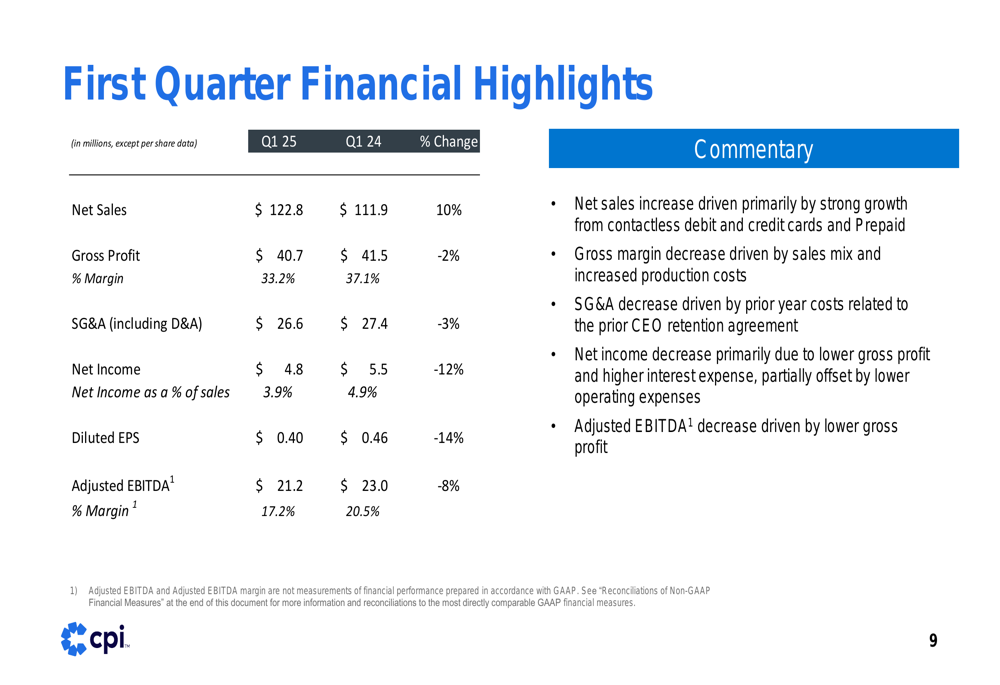

CPI Card Group reported Q1 2025 net sales of $122.8 million, a 10% increase compared to the $111.9 million recorded in the same period last year. However, this revenue growth was accompanied by margin pressure, with gross margin declining from 37.1% to 33.2% year-over-year.

The company attributed the margin compression to sales mix changes and increased production costs, which ultimately impacted bottom-line results. Net income decreased 12% to $4.8 million, with net income margin falling from 4.9% to 3.9%. Similarly, Adjusted EBITDA declined 8% to $21.2 million, with the corresponding margin decreasing from 20.5% to 17.2%.

As shown in the following comprehensive financial table comparing Q1 2025 to Q1 2024:

Both of CPI’s business segments experienced similar trends of revenue growth coupled with margin pressure. The Debit and Credit segment, which represents the bulk of the company’s business, saw net sales increase 10% to $96.5 million, while operating income decreased 5% to $21.7 million. The Prepaid Debit segment also posted a 10% revenue increase to $26.7 million, but operating income declined 9% to $8.0 million.

Strategic Initiatives

The most significant strategic development was CPI’s acquisition of Arroweye Solutions, a leading provider of digitally-driven on-demand payment card solutions for the U.S. market. Completed on May 6, 2025, this $45.55 million all-cash transaction is expected to complement CPI’s existing portfolio and create cross-selling opportunities.

The following slide details the strategic rationale and expected financial impact of the Arroweye acquisition:

According to the presentation, Arroweye is expected to generate revenues in the mid-$50 million range in 2025 on an annualized basis, with low double-digit Adjusted EBITDA margins. Management indicated they expect to increase these margins closer to CPI levels over time through synergies in both sales and costs.

In addition to the acquisition, CPI continues to invest in its new Indiana secure card production facility to expand capacity and enhance capabilities. This investment contributed to increased capital expenditures of $5.3 million in Q1 2025, compared to $1.5 million in the prior year period.

Financial Position

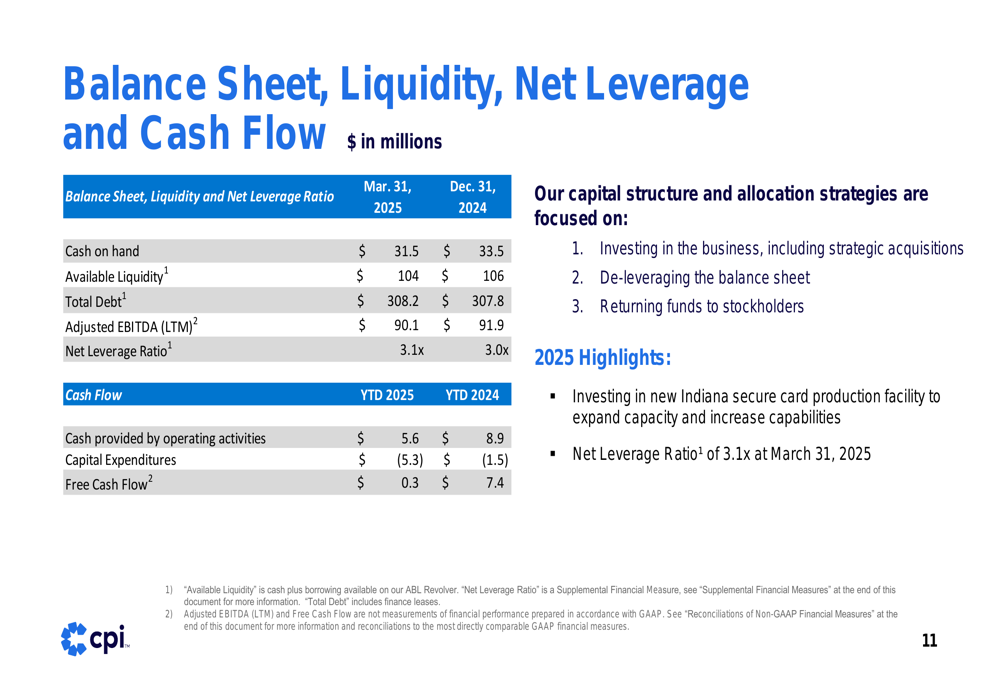

CPI’s balance sheet showed slight changes compared to the end of 2024, with cash on hand decreasing from $33.5 million to $31.5 million. The company’s net leverage ratio increased slightly from 3.0x to 3.1x, while available liquidity stood at $104 million as of March 31, 2025.

The following slide provides a detailed overview of CPI’s financial position and cash flow:

Free cash flow generation decreased significantly to $0.3 million in Q1 2025 from $7.4 million in the prior year period, primarily due to lower net income and increased capital expenditures related to the new production facility. Cash provided by operating activities also declined to $5.6 million from $8.9 million year-over-year.

Market Trends & Industry Position

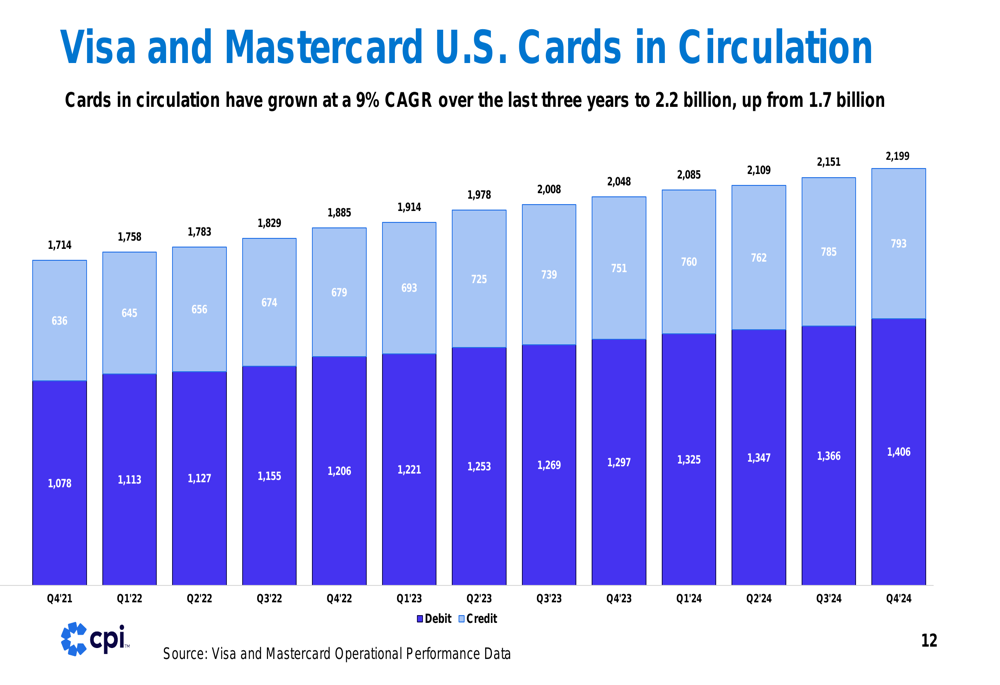

Despite the near-term margin challenges, CPI highlighted positive long-term industry trends supporting its growth strategy. According to the company’s data, Visa (NYSE:V) and Mastercard (NYSE:MA) U.S. cards in circulation have grown at a 9% CAGR over the last three years, reaching 2.2 billion cards, up from 1.7 billion.

The presentation emphasized strong customer demand for contactless debit and credit cards, as well as continued growth in the Prepaid segment. Management noted that these secular trends remain intact and position CPI well for future growth with its innovative and high-quality solutions.

The following chart illustrates the steady growth in U.S. cards in circulation:

Forward-Looking Statements

Despite the margin pressures in Q1, CPI affirmed its full-year 2025 outlook, excluding the impact of the Arroweye acquisition. The company continues to project mid-to-high single-digit increases in both net sales and Adjusted EBITDA, dependent on a stable economic and tariff environment.

Management highlighted that they have implemented cost savings activities in response to projected tariff costs and first-half sales mix pressures. They also noted that customer demand remains strong, supporting their confidence in the full-year outlook.

The following slide outlines the company’s 2025 guidance and long-term growth trends:

Summary and Outlook

CPI Card Group’s Q1 2025 results present a mixed picture of strong revenue growth coupled with margin challenges. The strategic acquisition of Arroweye Solutions represents a significant expansion of the company’s capabilities in on-demand payment card solutions, though it will take time to realize the full synergy benefits.

The company’s affirmation of its full-year guidance suggests management believes the margin pressures are temporary and manageable through cost-saving initiatives. However, the market’s negative reaction indicates investor concerns about the sustainability of profitability amid these challenges.

As summarized in the company’s presentation:

Looking ahead, CPI’s performance will likely depend on its ability to successfully integrate Arroweye, realize cost synergies, improve margins through favorable sales mix, and capitalize on the continued growth in card issuance trends. The company’s investments in expanded production capacity position it for future growth, but near-term profitability challenges may continue to weigh on investor sentiment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.