Gold prices tick higher on fresh U.S. tariff threats, Fed rate cut hopes

Introduction & Market Context

Cricut Inc. (NASDAQ:CRCT) presented its Q2 2025 financial results on August 5, 2025, showcasing a return to growth after previous quarters of revenue challenges. The company’s stock closed at $4.72, up 0.53% on the day, as investors digested the improved performance metrics and strategic initiatives outlined in the presentation.

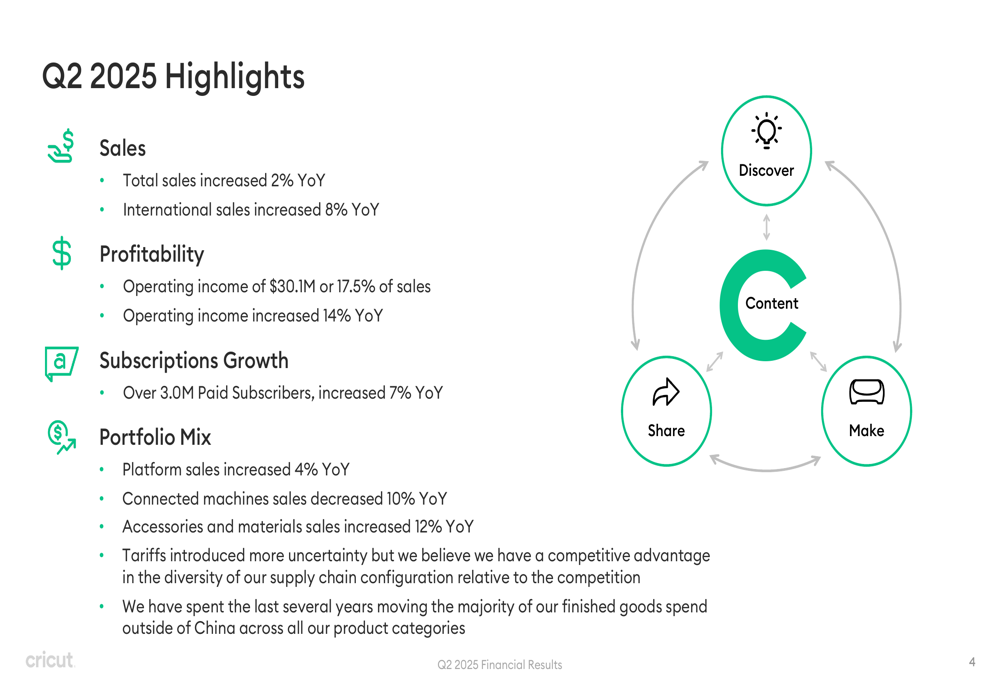

The crafting technology company reported a 2% year-over-year revenue increase, marking a turnaround from the 3% decline reported in Q1 2025. More impressively, Cricut delivered substantial profitability improvements, with operating income rising 14% and net income jumping 24% compared to the same period last year.

Quarterly Performance Highlights

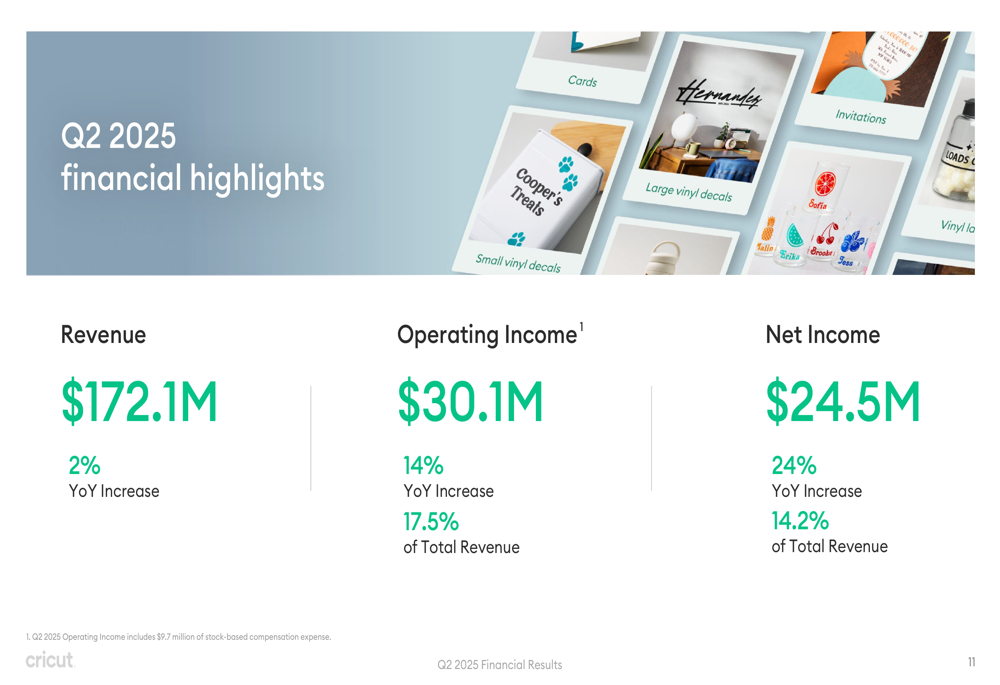

Cricut reported total revenue of $172.1 million for Q2 2025, representing a 2% increase year-over-year. The company’s operating income reached $30.1 million (17.5% of revenue), up 14% from the prior year, while net income grew to $24.5 million (14.2% of revenue), a 24% increase compared to Q2 2024.

As shown in the following financial highlights from the presentation:

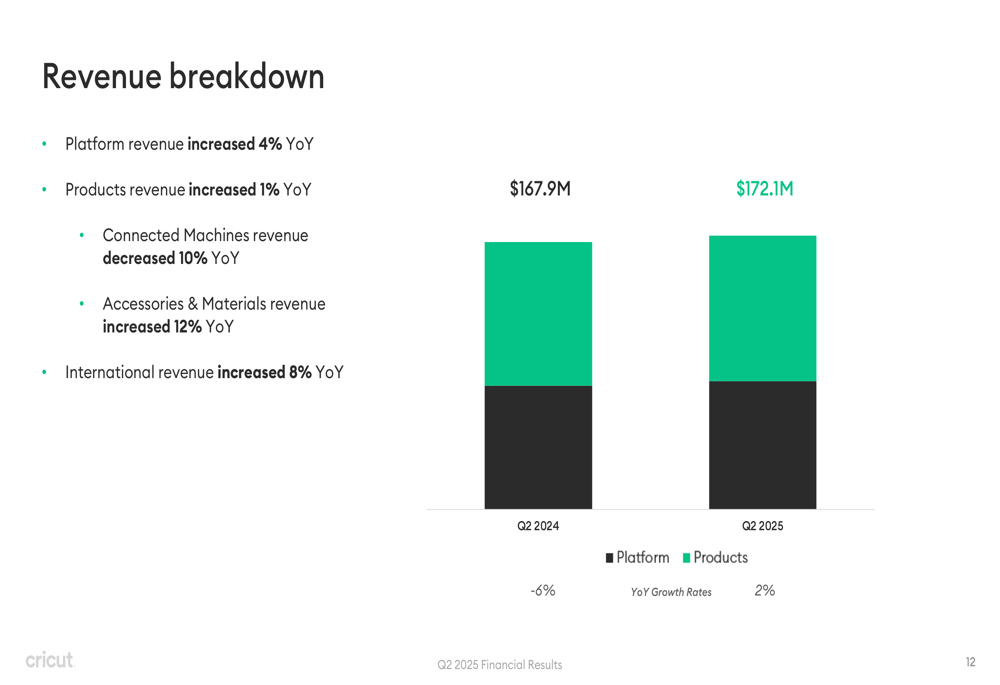

The revenue growth was driven primarily by the company’s platform business and accessories & materials segment, which offset weakness in connected machine sales. Platform revenue increased 4% year-over-year, while accessories & materials revenue grew by an impressive 12%. However, connected machine revenue declined by 10% compared to the same period last year.

The following revenue breakdown illustrates these trends:

International markets performed particularly well, with international revenue increasing 8% year-over-year, outpacing the company’s overall growth rate. This suggests Cricut’s global expansion strategy is gaining traction despite macroeconomic challenges.

Detailed Financial Analysis

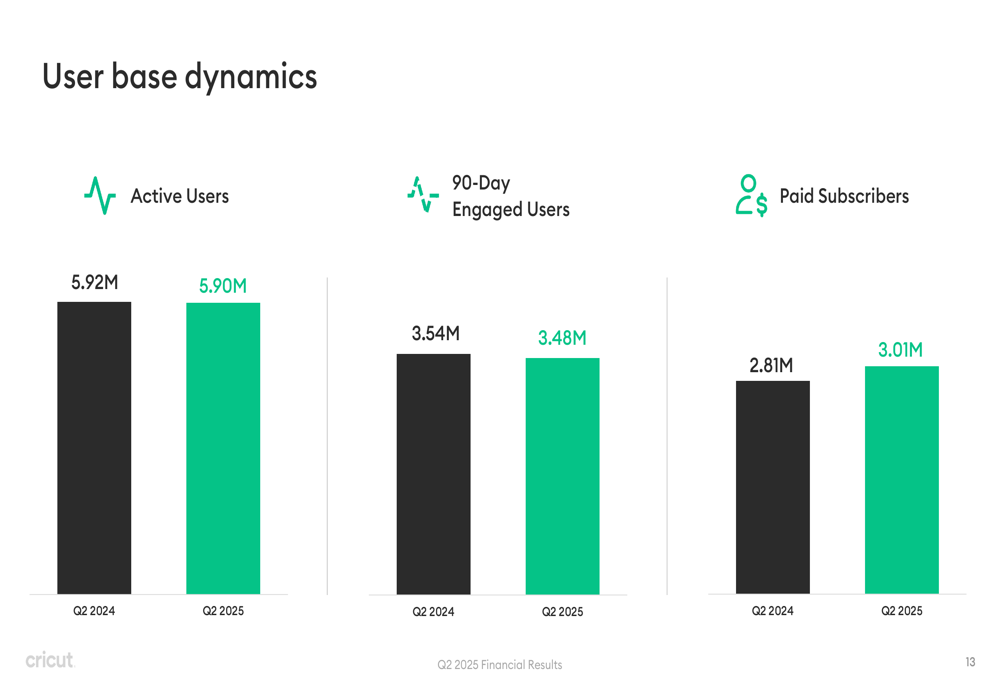

Cricut’s user metrics showed mixed results for the quarter. The company reported 3.01 million paid subscribers, up 7% year-over-year and an increase of 36,000 sequentially from Q1. However, total active users slightly declined to 5.90 million from 5.92 million in Q2 2024, and 90-day engaged users decreased to 3.48 million from 3.54 million in the prior year.

The following chart illustrates these user dynamics:

Gross margin improved significantly to 59.0% in Q2 2025, compared to 53.5% in Q2 2024. This improvement was attributed to a slight increase in platform margins due to lower amortization of software development costs, as well as product margin increases from capitalized costs associated with higher inventory and the selling of previously reserved excess and obsolete products.

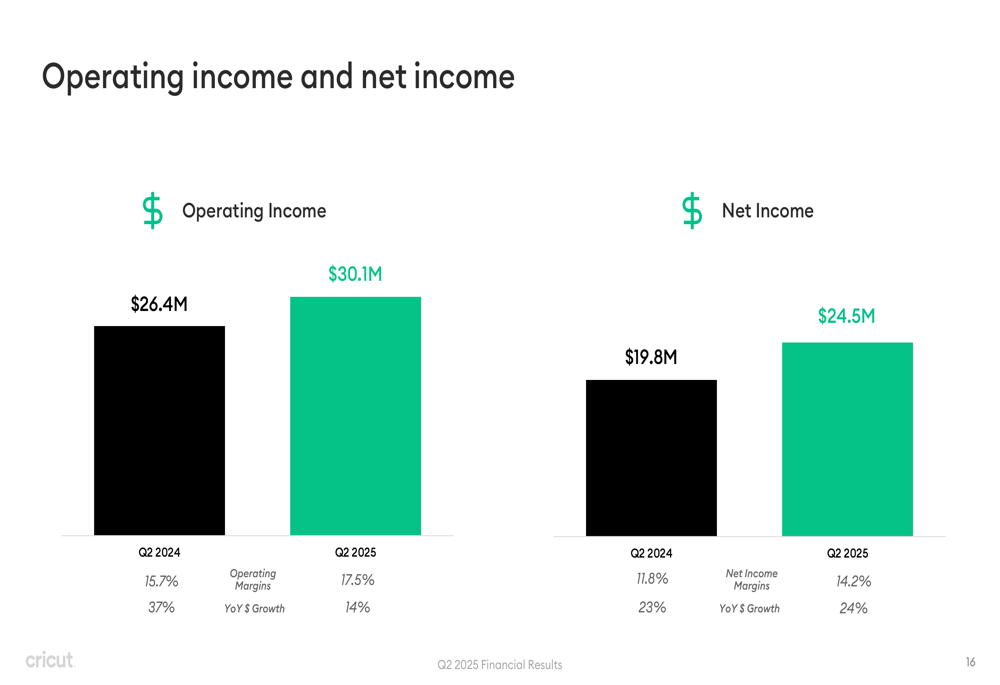

Operating income and net income both showed substantial year-over-year improvements, with operating margins expanding from 15.7% to 17.5% and net income margins increasing from 11.8% to 14.2%.

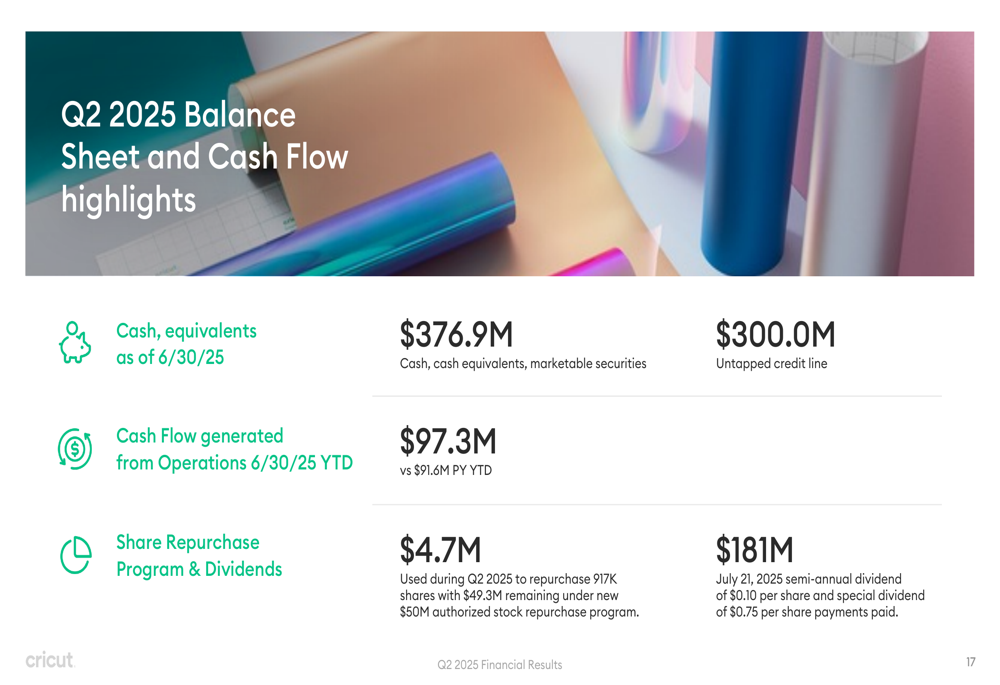

Cricut maintained a strong financial position with $376.9 million in cash and equivalents as of June 30, 2025. The company generated $97.3 million in cash flow from operations year-to-date, up from $91.6 million in the prior year period. During Q2, Cricut repurchased 917,000 shares for $4.7 million and paid $181 million in dividends, including a $0.10 per share semi-annual dividend and a substantial $0.75 per share special dividend.

Strategic Initiatives

Cricut outlined several strategic initiatives aimed at accelerating growth and improving user engagement. The company recently launched new products, including the Cricut Explore 4 and Cricut Maker 4, which have reportedly triggered excitement among both users and retailers. Management indicated that increased marketing efforts have yielded a 2x increase in views and engagement year-over-year.

To address user acquisition and retention challenges, Cricut is implementing significant improvements to the machine registration process and day-one support for new users. The company is also focusing on simplifying the overall user experience with step-by-step guidance for projects within its Design Space platform and continued improvements to AI functionality, including beta testing of a new generative AI feature called Create AI.

In the accessories and materials segment, Cricut is expanding its value-oriented product line to address affordability concerns and competitive pressures. The company launched additional Cricut Value Material SKUs in response to consumer demand and is creating products that prioritize affordability while working seamlessly with Cricut machines. Management also highlighted that a diversified manufacturing footprint positions the company as a better retail partner, particularly amid tariff uncertainties.

Forward-Looking Statements

Looking ahead, Cricut’s management expressed a relentless focus on increasing execution speed and accelerating investments in hardware product development, materials, engagement, and marketing to drive future revenue growth. The company expects platform sales to increase year-over-year on continued paid subscriber growth, though it cautioned that subscriber growth may be challenging until machine sales and new user acquisition accelerate.

Management noted that Q2 operating margin benefits are not expected to recur, and given the uncertainty surrounding tariffs, the company declined to provide specific operating margin guidance. Nevertheless, Cricut expects to remain profitable each quarter and generate significant positive cash flow during 2025.

The company also cautioned that Q2 accessories and materials product sales may have benefited from accelerated shipments motivated by tariff risks, which could impact future quarters. Additionally, management indicated that Q3 typically sees flat to declining quarter-over-quarter subscriber counts, with seasonal growth returning in Q4.

Despite these challenges, Cricut’s return to revenue growth and substantial profitability improvements suggest the company’s strategic initiatives may be gaining traction after several quarters of revenue declines. Investors will be watching closely to see if these positive trends continue in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.