Fed’s Waller emerges as top candidate for Fed chair - report

Introduction & Market Context

Crocs Inc. (NASDAQ:CROX) shares plummeted 16.38% in premarket trading on August 7, 2025, despite reporting a 3% year-over-year revenue increase in its second quarter investor presentation. The sharp decline follows the company’s concerning Q3 guidance and significant impairment charges totaling $737 million, overshadowing what management described as a "solid second quarter with contributions from both Crocs and HEYDUDE brands."

The footwear maker reported its "highest ever gross profit quarter" while simultaneously revealing substantial impairments to its HEYDUDE-related assets, creating a mixed picture for investors already concerned about potential tariff impacts and shifting consumer sentiment.

Quarterly Performance Highlights

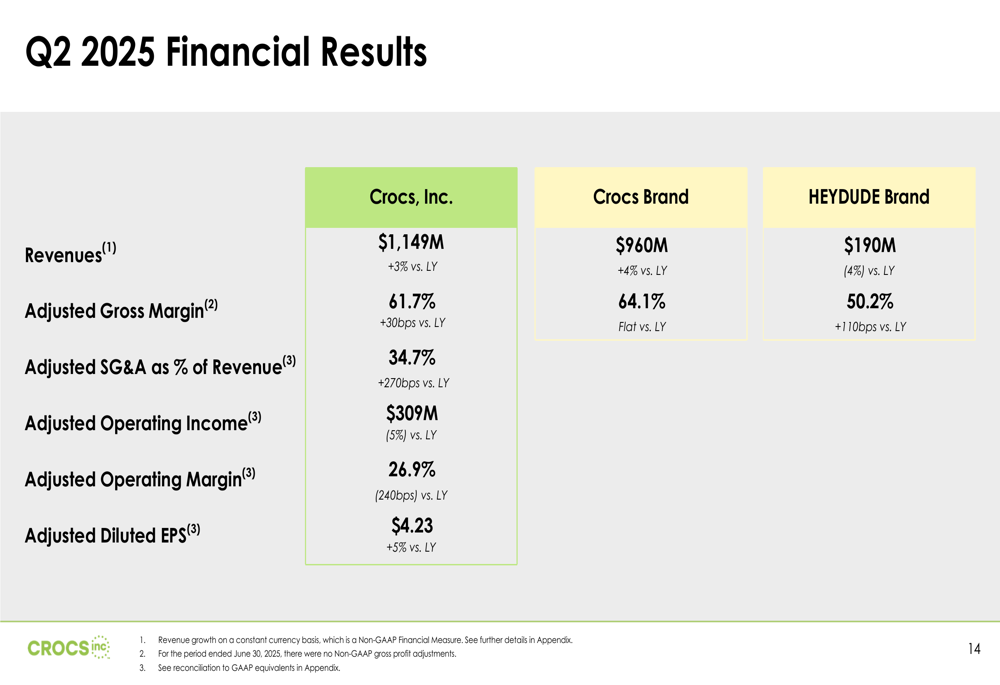

Crocs delivered Q2 2025 revenue of $1.15 billion, representing 3% growth compared to the same period last year. The company’s adjusted earnings per share reached $4.23, a 5% increase year-over-year, while adjusted operating income declined 5% to $309 million.

As shown in the following comprehensive financial results:

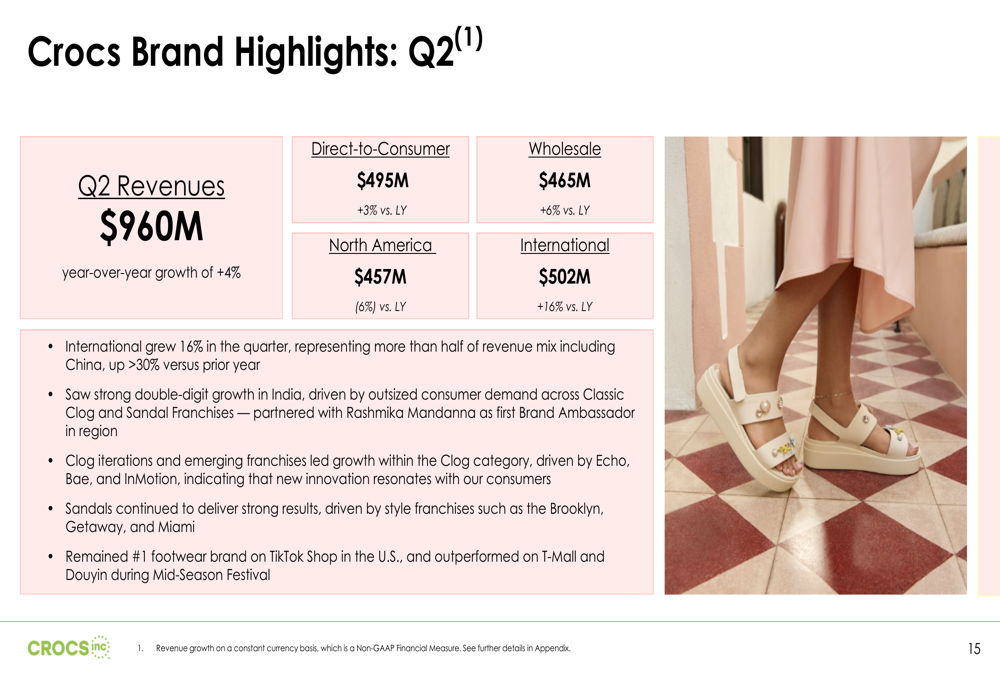

The Crocs brand continued to show strength with 4% revenue growth to $960 million, while HEYDUDE revenue declined 4% to $190 million. The company’s adjusted gross margin improved by 30 basis points to 61.7%, though adjusted operating margin contracted by 240 basis points to 26.9%.

The company’s geographic revenue mix continued to shift, with international markets now representing more than half of Crocs brand revenue. International sales grew 16% in the quarter, with China up over 30% and strong double-digit growth in India. Meanwhile, North America revenue declined 6% year-over-year.

Detailed Financial Analysis

Behind the headline numbers, Crocs’ financial statements revealed significant non-cash impairments, including a $430 million impairment of indefinite-lived trademark and a $307 million impairment of goodwill, both related to the HEYDUDE brand. These impairments dramatically affected GAAP results, with the company reporting a GAAP operating margin of -37.2% compared to 29.3% in the prior year period.

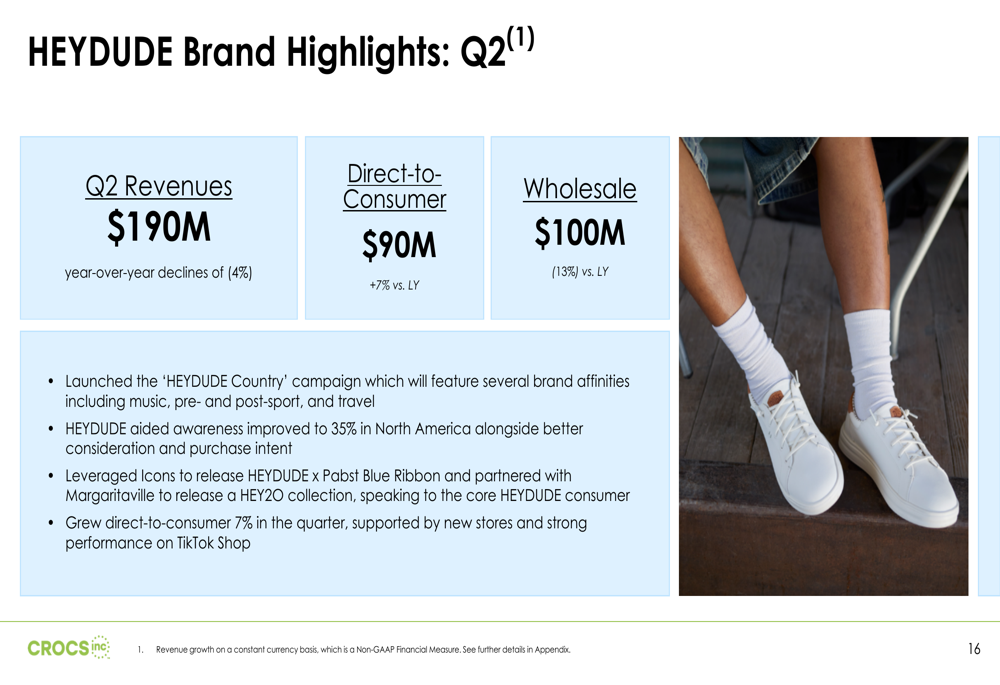

HEYDUDE’s performance showed a divergence between channels, with direct-to-consumer revenue growing 7% while wholesale declined 13%. The brand’s adjusted gross margin improved 110 basis points to 50.2%.

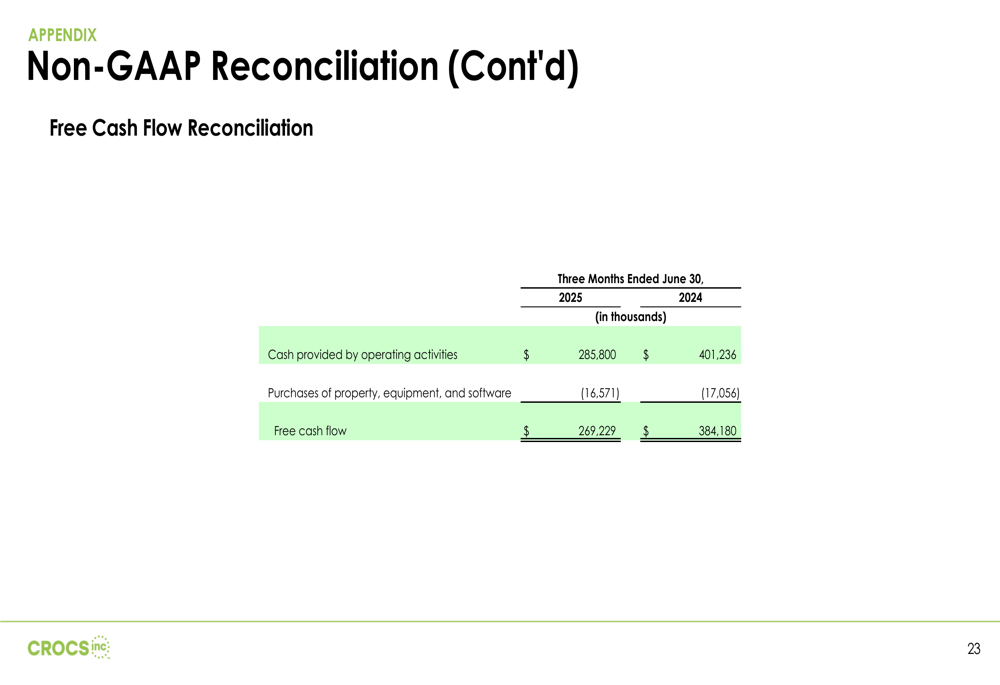

The company’s free cash flow generation declined to $269 million from $384 million in the same quarter last year. Despite this reduction, Crocs continued to focus on shareholder returns, repurchasing $133 million in shares and paying down $105 million in debt during the quarter.

Strategic Initiatives

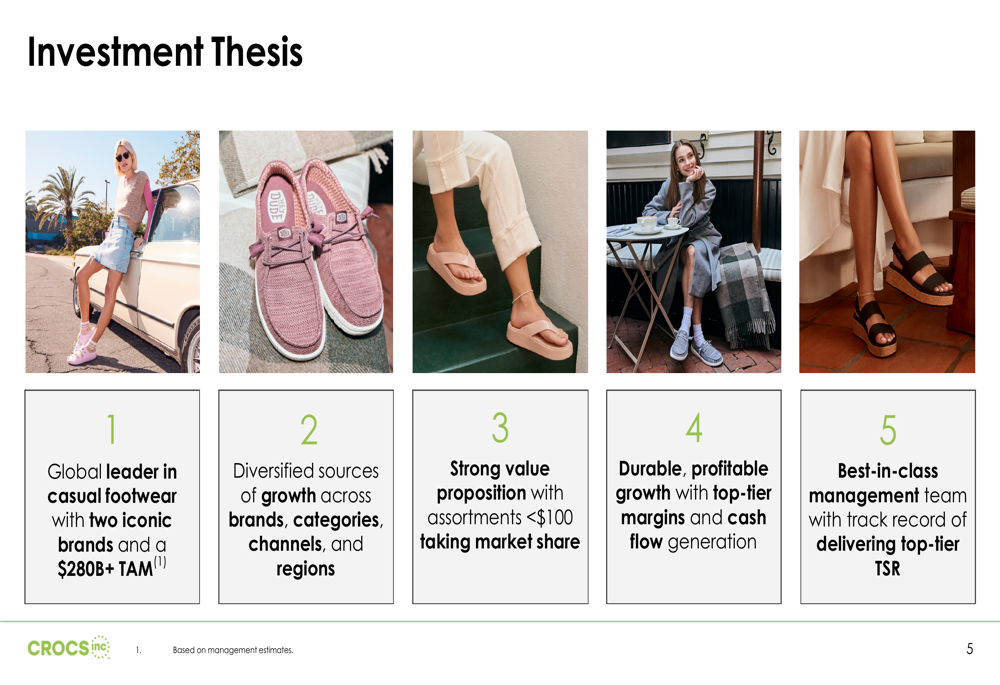

Crocs outlined its investment thesis and growth priorities, emphasizing its position as a global leader in casual footwear with a total addressable market exceeding $280 billion. The company highlighted its diversified growth platform across brands, channels, and regions.

The following slide illustrates the company’s key investment thesis points:

For the core Crocs brand, management is focusing on driving brand relevance through icon iterations, gaining market share outside of clogs, fueling digital marketing, and expanding globally. For HEYDUDE, priorities include building community through "HEYDUDE Country" campaigns, scaling core products, and stabilizing North America while expanding internationally.

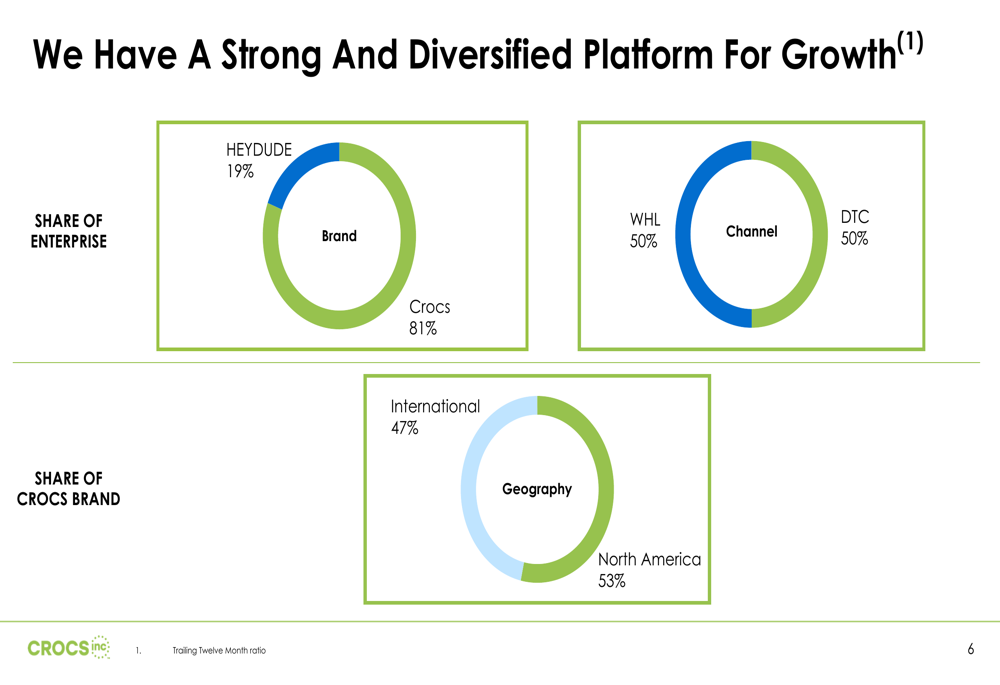

The company’s revenue diversification strategy is reflected in this breakdown:

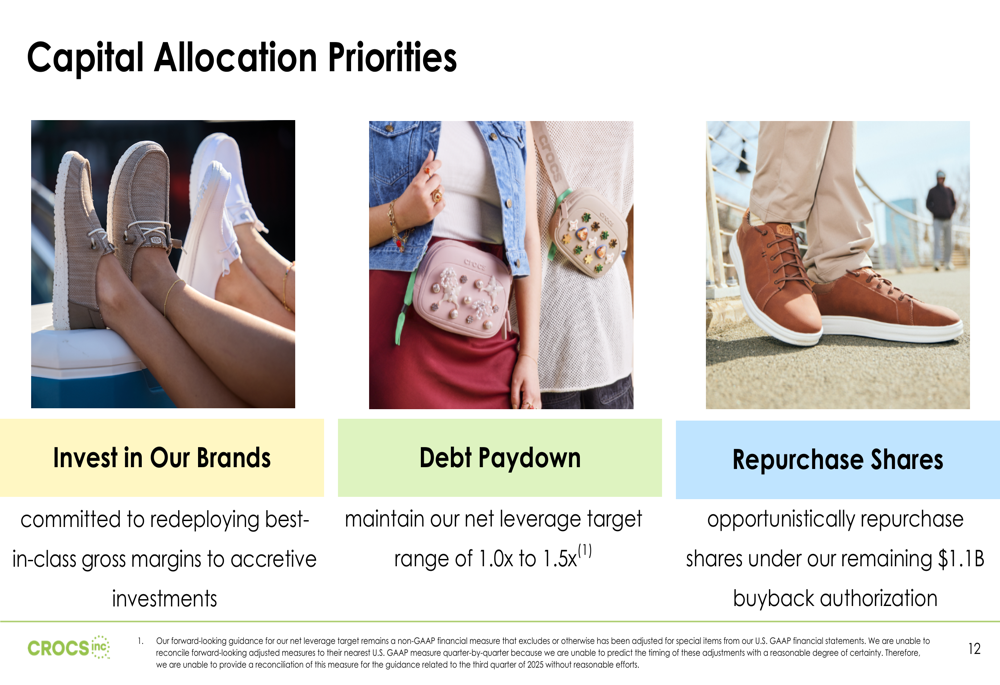

Regarding capital allocation, Crocs outlined three priorities: investing in its brands, paying down debt to maintain a net leverage target range of 1.0x to 1.5x, and opportunistically repurchasing shares under its remaining $1.1 billion buyback authorization.

Forward-Looking Statements

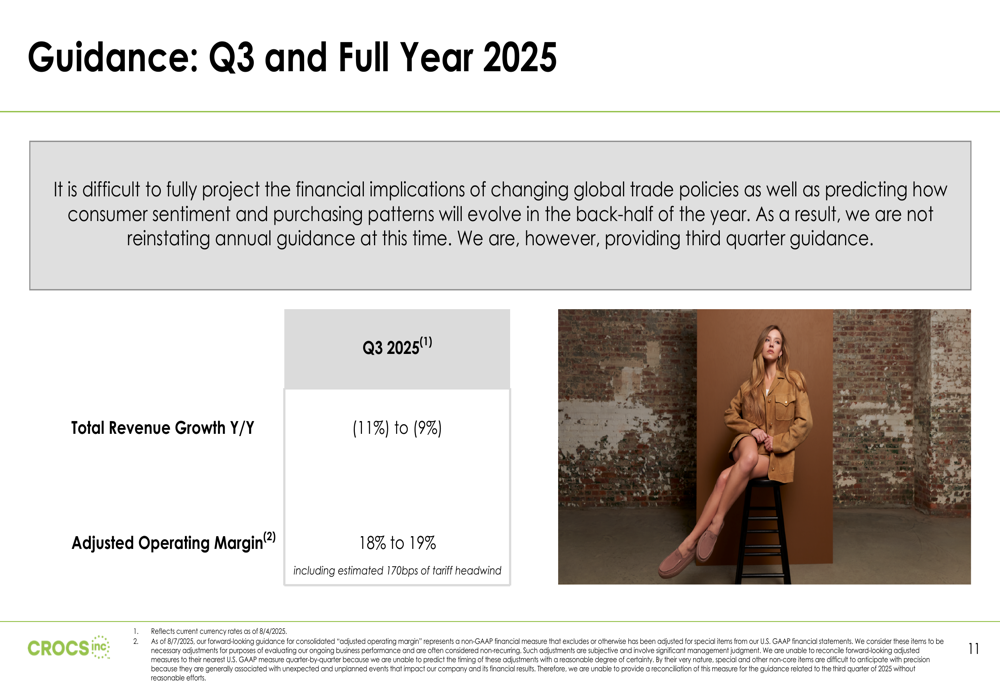

The most concerning aspect of the presentation for investors appears to be the Q3 2025 guidance, which projects a year-over-year revenue decline of 9% to 11% and adjusted operating margin of 18% to 19%, including an estimated 170 basis point headwind from tariffs.

Notably, Crocs declined to reinstate full-year guidance, citing difficulties in projecting financial implications of changing global trade policies and consumer sentiment. This uncertainty, combined with the projected Q3 revenue decline and significant impairments, likely contributed to the sharp premarket stock decline.

The company is implementing $50 million in cost savings and reducing inventory receipts while pulling back on promotional activity to protect brand health. Management emphasized its focus on managing expenses in the current environment while continuing to invest in long-term growth opportunities.

This marks a significant shift from Q1 2025, when Crocs reported earnings per share of $3.00, exceeding analysts’ expectations of $2.48, and saw its stock rise nearly 6% following the announcement. The deteriorating outlook suggests increasing headwinds for the casual footwear maker as it navigates changing consumer preferences and potential tariff impacts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.