Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

CrossAmerica Partners LP (NYSE:CAPL) presented its second quarter 2025 earnings results on August 7, 2025, revealing a mixed financial performance with significant net income growth contrasted by operational challenges across its business segments. The company’s stock closed at $20.26, up 0.87% following the presentation, as investors digested the complex earnings picture.

The second quarter results represent a substantial recovery from the company’s disappointing first quarter, when CrossAmerica reported a net loss of $7.1 million and missed EPS expectations. However, the current quarter’s strong bottom-line performance appears largely driven by non-operational gains rather than fundamental business improvements.

Quarterly Performance Highlights

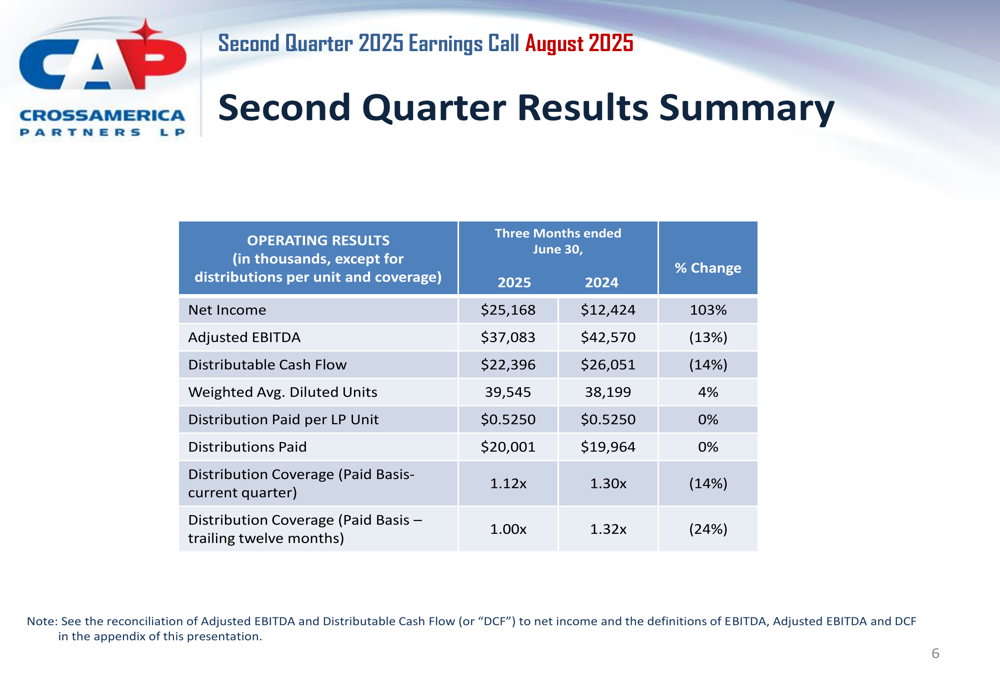

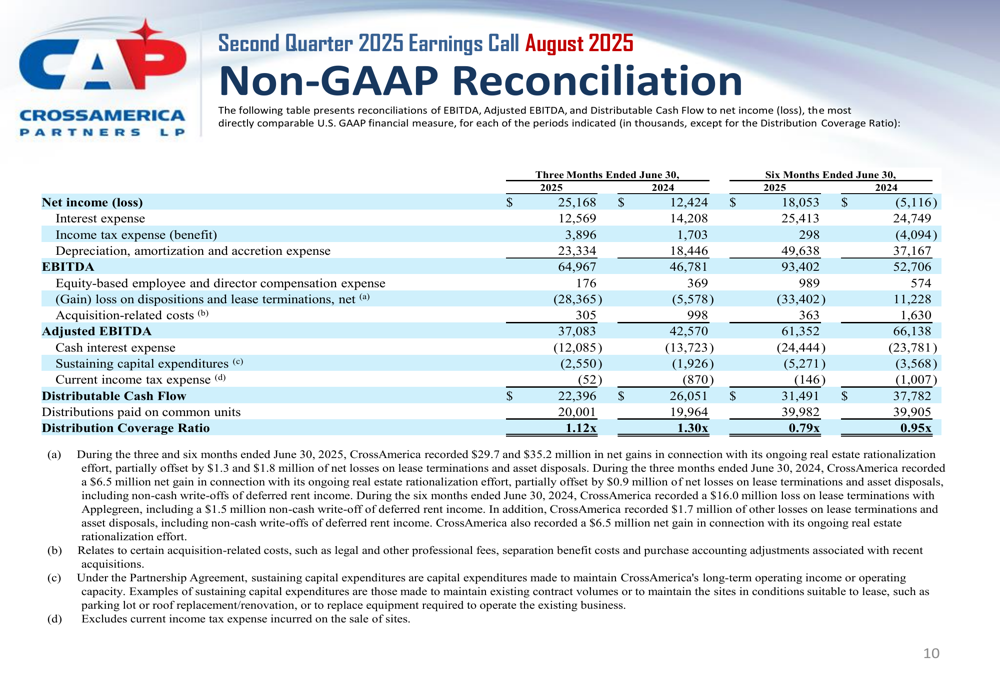

CrossAmerica reported net income of $25.2 million for Q2 2025, a remarkable 103% increase from $12.4 million in the same period last year. However, this headline figure masks underlying operational challenges, as Adjusted EBITDA declined 13% year-over-year to $37.1 million, and Distributable Cash Flow (DCF) fell 14% to $22.4 million.

The company maintained its quarterly distribution at $0.5250 per limited partner unit, unchanged from the previous year. However, the distribution coverage ratio declined to 1.12x from 1.30x in Q2 2024, raising potential concerns about distribution sustainability. On a trailing twelve-month basis, the coverage ratio has fallen to 1.00x from 1.32x a year ago, leaving little margin for error.

A closer examination of the financial reconciliation reveals that the substantial net income growth was largely attributable to a $28.4 million gain on dispositions and lease terminations, compared to a $5.6 million gain in the prior-year period. This non-operational gain effectively masked the operational declines in the business.

Segment Performance Analysis

Both of CrossAmerica’s primary business segments experienced year-over-year declines in operating income during the second quarter. The Retail segment reported operating income of $25.3 million, down 10% from $28.0 million in Q2 2024. The Wholesale segment saw a steeper 15% decline to $17.7 million from $20.9 million a year earlier.

In the Retail segment, motor fuel gross profit decreased 1% to $38.8 million, while merchandise gross profit increased 2% to $30.5 million. Same-store sales excluding cigarettes showed healthy growth of 4%, indicating some resilience in the company’s convenience store operations despite broader challenges.

The Wholesale segment faced more significant headwinds, with gross profit declining 12% to $24.9 million. Motor fuel gross profit in this segment fell 9% to $15.2 million, while the volume of gallons distributed decreased 7% to 179.2 million. The wholesale margin per gallon also contracted slightly to $0.085 from $0.087 in the prior year.

Capital Allocation and Balance Sheet

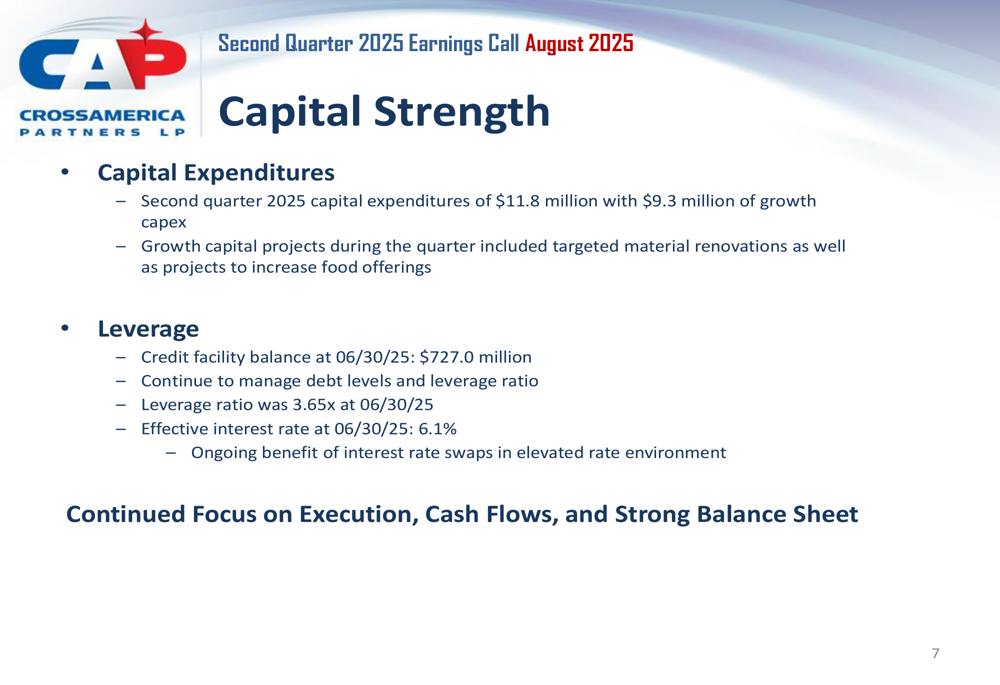

CrossAmerica reported capital expenditures of $11.8 million for the second quarter, with $9.3 million allocated to growth initiatives. These growth capital projects focused on renovations and expanding food offerings, aligning with the company’s strategic priorities.

The company’s credit facility balance stood at $727.0 million as of June 30, 2025, with a leverage ratio of 3.65x. Management highlighted that CrossAmerica is benefiting from interest rate swaps in the current elevated rate environment, with an effective interest rate of 6.1%.

Forward Outlook

While CrossAmerica did not provide specific numerical guidance for future quarters, management emphasized its continued focus on execution, cash flows, and maintaining a strong balance sheet. The company’s strategic initiatives around site renovations and expanded food offerings suggest a long-term focus on enhancing the retail experience to drive growth.

The declining distribution coverage ratio presents a potential challenge, particularly given the company’s high dividend yield that has historically attracted income-focused investors. With the trailing twelve-month coverage ratio now at 1.00x, exactly matching distributions paid, CrossAmerica has limited flexibility should operational performance continue to decline.

Looking ahead, investors will likely focus on whether CrossAmerica can reverse the operational declines in both its Retail and Wholesale segments, or whether it will continue to rely on asset sales and dispositions to support bottom-line results. The company’s ability to maintain its distribution while improving coverage will be a key metric to watch in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.