BitMine stock falls after CEO change and board appointments

Introduction & Market Context

CTI Engineering Co., Ltd. (TYO:9621), Japan’s first consulting engineer company, presented its Q2 FY2025 financial results on August 12, 2025, revealing a mixed performance characterized by strong order growth but declining profitability. The company, which ranks third in sales and first in current term income among Japanese construction consulting firms, maintained most of its full-year forecasts despite the quarterly profit decline.

CTI Engineering’s stock closed at ¥2,950 on September 9, 2025, up ¥14 (0.47%) from its previous close, trading between its 52-week range of ¥2,044 to ¥3,275.

Quarterly Performance Highlights

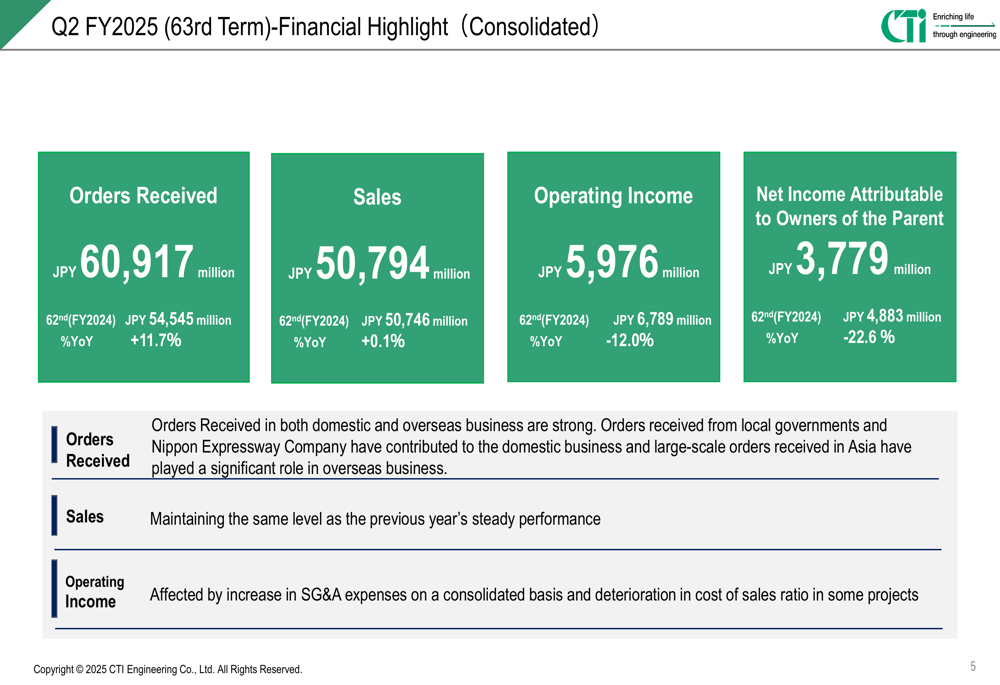

CTI Engineering reported robust order growth in Q2 FY2025, with consolidated orders received increasing 11.7% year-over-year to ¥60.9 billion. However, sales remained virtually flat at ¥50.8 billion (+0.1% YoY), while profitability metrics declined significantly.

As shown in the following consolidated financial highlights:

Operating income decreased 12.0% year-over-year to ¥6.0 billion, with operating margin contracting from 13.4% to 11.8%. Net income attributable to owners of the parent fell more sharply, declining 22.6% to ¥3.8 billion. The company attributed the profit decline to increased SG&A expenses on a consolidated basis and deteriorated cost of sales in some operations.

The quarterly results also revealed extraordinary losses related to an employee dormitory being declared dormant assets and a waiver of claims against a subsidiary, which further impacted the bottom line.

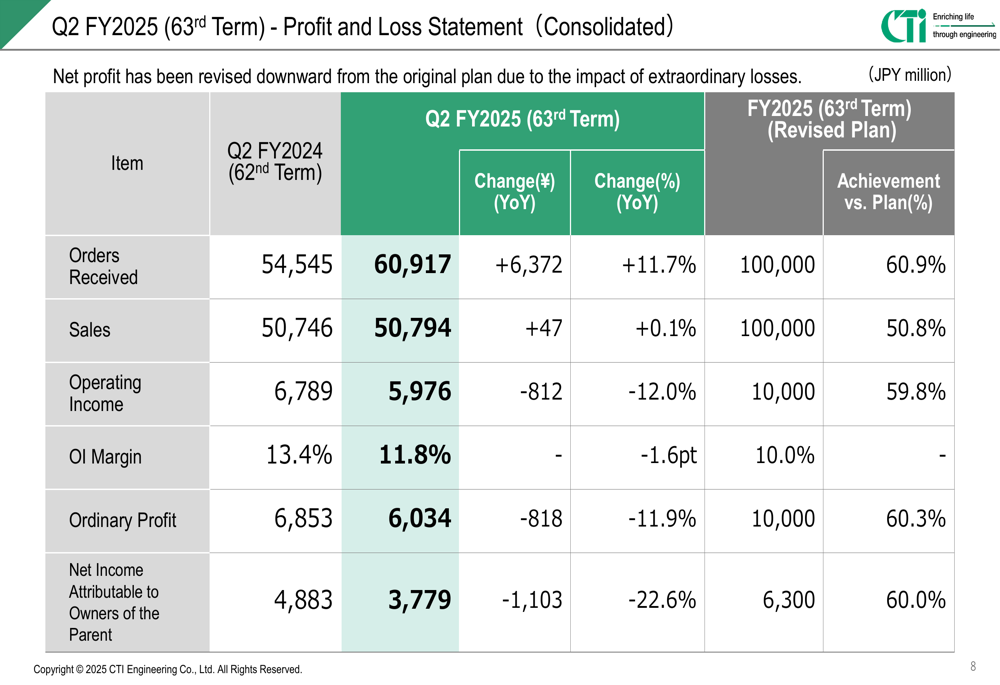

The following profit and loss statement provides a detailed breakdown of the company’s financial performance:

Despite the quarterly profit decline, CTI Engineering’s performance against its full-year forecast remains on track, with orders received achieving a 60.9% progress ratio and sales reaching 50.8% of the annual target by the midpoint of the fiscal year.

Segment Performance

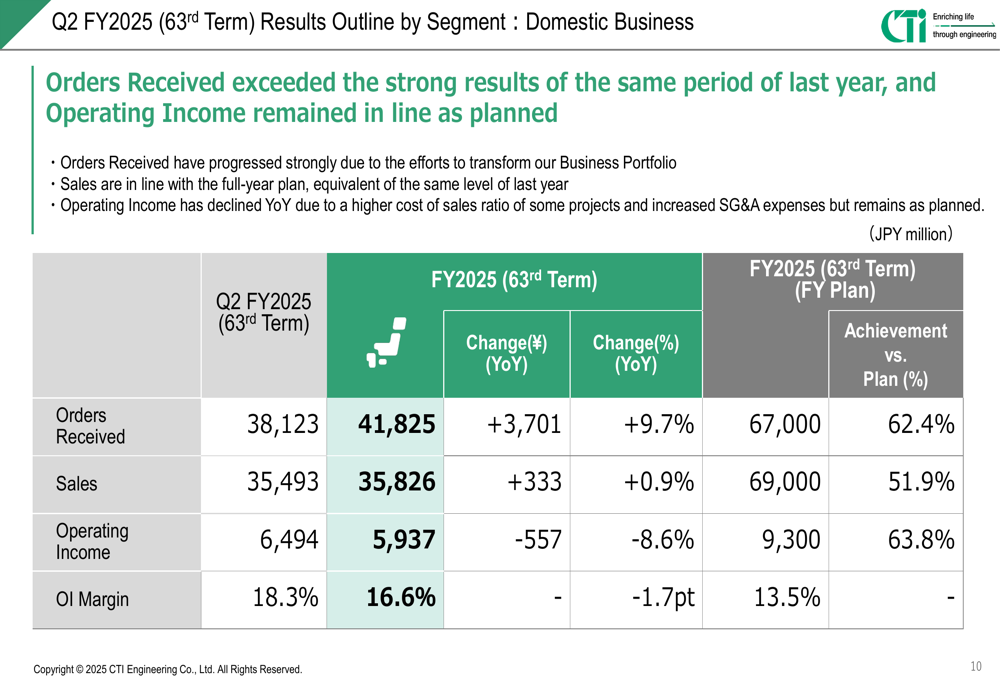

CTI Engineering’s domestic business continued to demonstrate strength, with orders received increasing 9.7% year-over-year to ¥41.8 billion. Sales in this segment grew modestly by 0.9% to ¥35.8 billion, while operating income decreased 8.6% to ¥5.9 billion. The operating margin for domestic operations remained healthy at 16.6%, though down from 18.3% in the same period last year.

The following segment breakdown illustrates the domestic business performance:

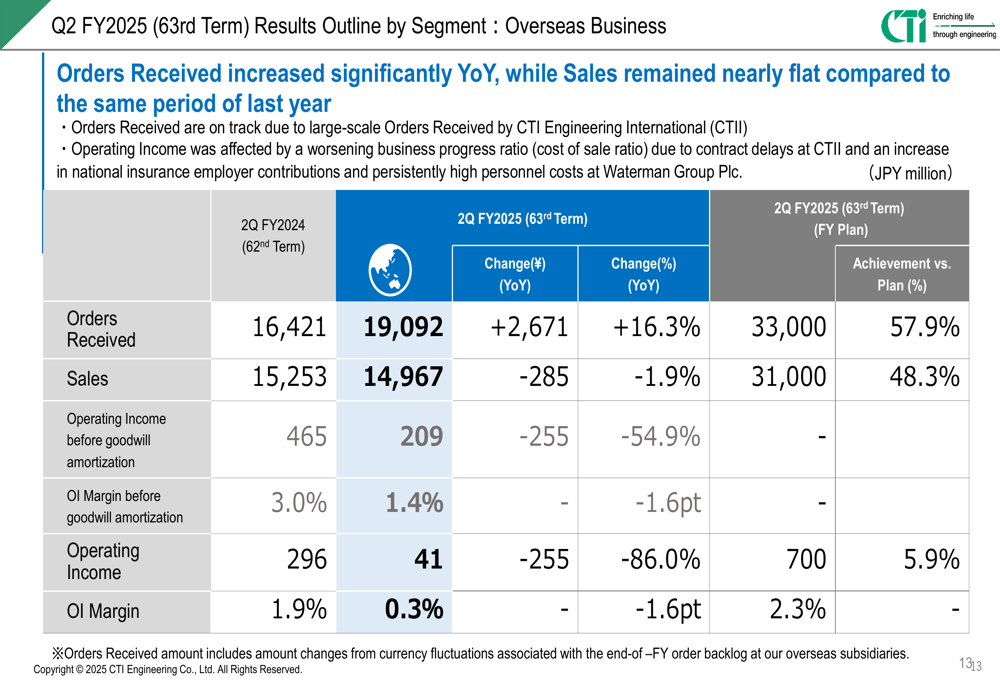

By contrast, the overseas business segment faced more significant challenges. While orders received increased 16.3% year-over-year to ¥19.1 billion, sales declined 1.9% to ¥15.0 billion. More concerning was the 86.0% drop in operating income to just ¥41 million, resulting in a razor-thin operating margin of 0.3%, down from 1.9% in Q2 FY2024.

The overseas segment results highlight the diverging performance between domestic and international operations:

Within the domestic business, the company reported particularly strong order growth in the Water & Land Sector (+14.2% YoY) and the Construction Management Sector (+31.0% YoY), while the Environment & Social Sector experienced a slight decline of 3.8%.

Revised Outlook

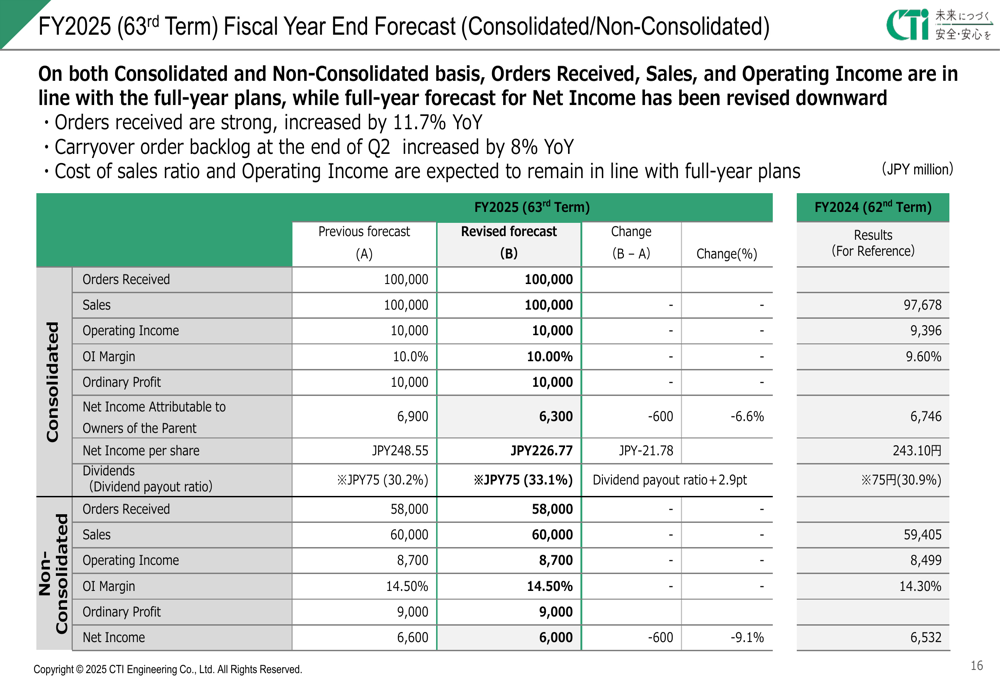

Despite the Q2 profit decline, CTI Engineering maintained its full-year forecasts for orders received, sales, and operating income at ¥100 billion, ¥100 billion, and ¥10 billion, respectively. However, the company revised its net income forecast downward from ¥6.9 billion to ¥6.3 billion, reflecting the impact of extraordinary losses.

The following slide shows the revised full-year forecast:

The company affirmed that its Mid-Term Management Plan 2027 remains on track, with progress in business portfolio transformation, human capital development, and digital transformation initiatives. CTI Engineering reported growth in local government contracts and information provision services, aligning with its strategic objectives.

For the remainder of the fiscal year, the company outlined several focus areas:

1. In domestic business: Maintaining profitability while increasing orders in line with business portfolio transformation

2. In overseas business: Improving profitability at CTII by utilizing local subsidiaries and at Waterman by negotiating with clients to transfer increased costs

3. In human capital and digital transformation: Securing talent through various recruitment methods and implementing systems that support diverse working styles, while promoting the use of generative AI and other technologies to improve efficiency

Competitive Industry Position

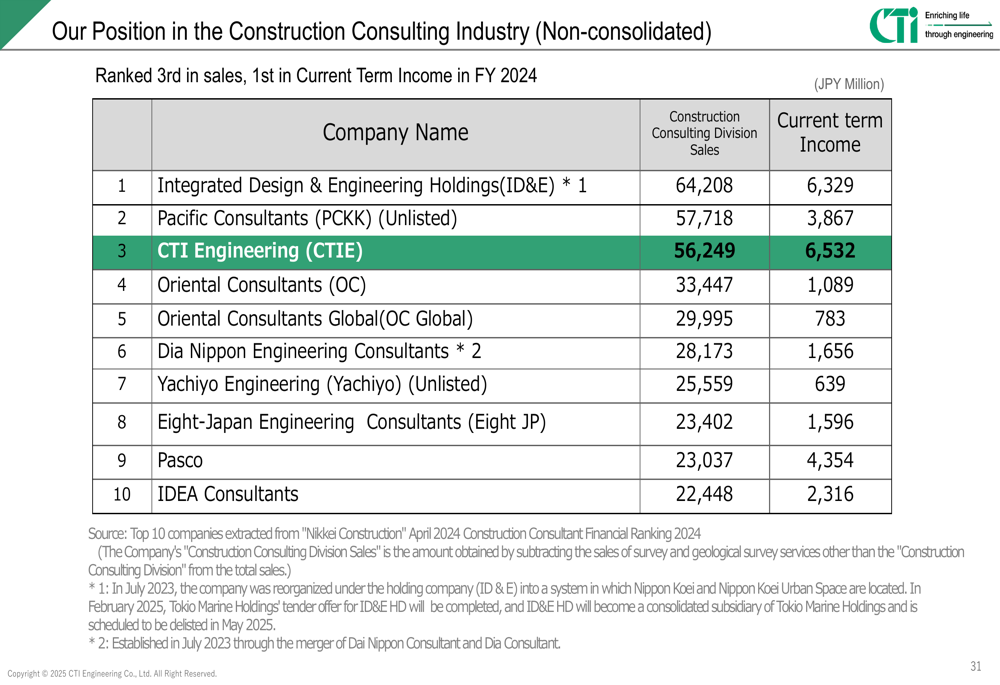

CTI Engineering highlighted its strong competitive position in Japan’s construction consulting industry, ranking third in sales and first in current term income for FY2024. The company’s presentation emphasized its technical expertise and strong relationships with government clients, with 46% of orders coming from the national government.

The following slide illustrates CTI Engineering’s position relative to key competitors:

The company’s business model benefits from a stable earnings structure, with approximately 61% of contracts won through technical competition (proposals and comprehensive evaluation) rather than price competition. This technical focus aligns with CTI Engineering’s emphasis on professional engineers and specialized expertise as core strengths.

CTI Engineering also noted progress in its business portfolio transformation, with growth in local government contracts and information provision services. The company maintained its shareholder return policy, with dividends held steady at ¥75 per share, representing a dividend payout ratio of 33.1%.

As CTI Engineering navigates the challenges in its overseas business while building on domestic strengths, investors will be watching closely to see if the company can maintain its order momentum while addressing the profitability pressures evident in this quarter’s results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.