Nuscale Power earnings missed by $0.02, revenue fell short of estimates

Cummins Inc (NYSE:CMI) shares jumped nearly 5% in premarket trading after the engine manufacturer’s second quarter presentation revealed significant profitability improvements despite a slight revenue decline. The company’s Q2 2025 earnings teleconference, held on August 5, 2025, showcased how Cummins is navigating shifting market demands across its diverse business segments.

Quarterly Performance Highlights

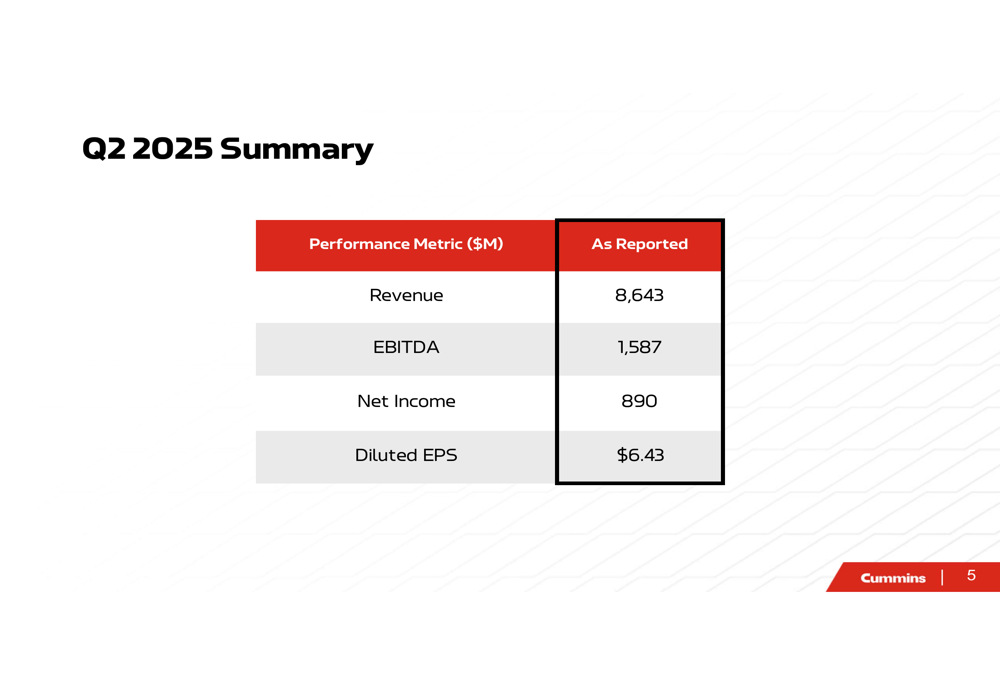

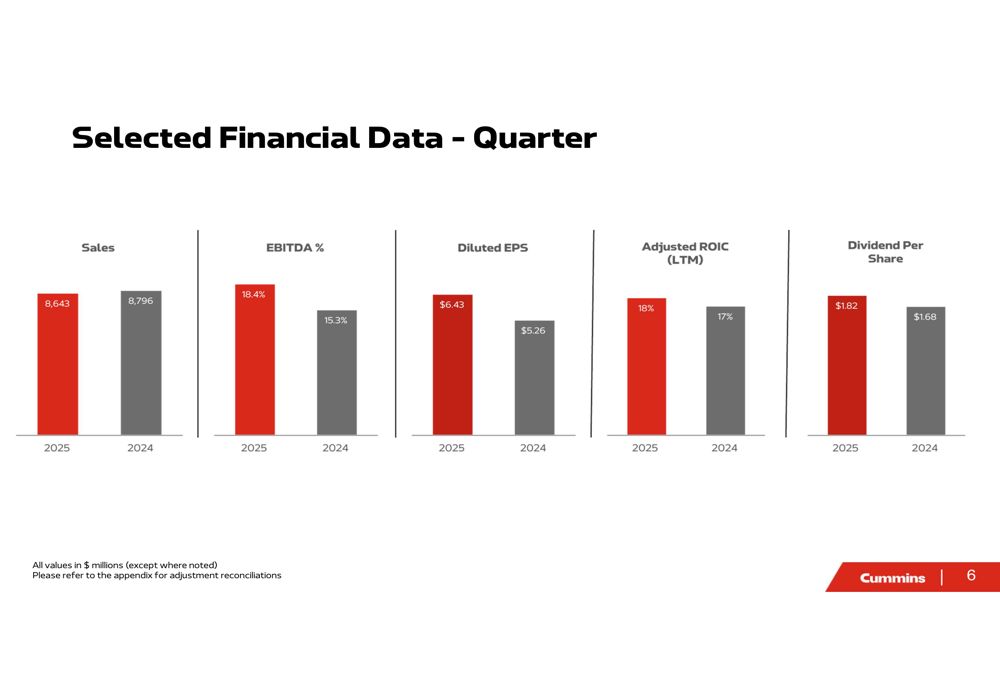

Cummins reported second quarter revenue of $8.64 billion, representing a 2% decrease compared to the same period last year. However, the company significantly improved its profitability metrics, with EBITDA reaching $1.59 billion (18.4% of sales) compared to $1.35 billion (15.3%) in Q2 2024. Net income rose to $890 million, with diluted earnings per share increasing to $6.43 from $5.26 a year earlier.

As shown in the following summary of Q2 2025 performance metrics:

The quarter’s results continue the momentum seen in Q1 2025, when Cummins exceeded EPS expectations by 18.7% with earnings of $5.96 per share. The Q2 EPS of $6.43 represents further sequential improvement, demonstrating the company’s ability to enhance profitability despite revenue challenges.

A comparison of key financial metrics between Q2 2025 and Q2 2024 reveals significant improvements across most performance indicators:

Detailed Financial Analysis

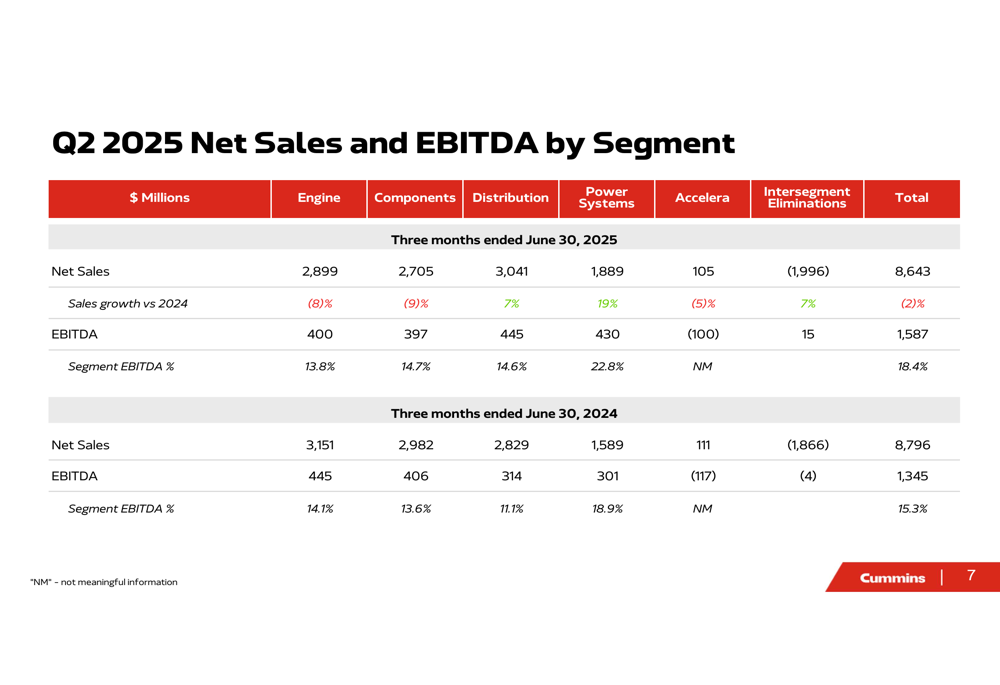

Cummins’ performance varied significantly across its business segments, reflecting shifting market dynamics. The company’s traditional Engine and Components segments faced headwinds, while Power Systems and Distribution segments delivered strong growth.

The following breakdown shows net sales and EBITDA performance by segment:

The Engine Segment, which represents 28% of Cummins’ revenue, experienced an 8% decrease in sales to $2.9 billion, with EBITDA margin slightly declining to 13.8%. This decline was primarily attributed to lower On-Highway demand in North America, though the company noted that favorable pricing in light-duty markets, operational efficiencies, and higher joint venture income helped partially offset the volume impact.

Similarly, the Components Segment saw a 9% revenue decline to $2.7 billion, but improved its EBITDA margin to 14.7% from 13.6% in the prior year. According to the presentation, this margin improvement was "driven primarily by reduced Product Coverage expense and operational efficiencies."

In contrast, the Distribution Segment delivered 7% revenue growth to $3.0 billion, with a substantial EBITDA margin improvement to 14.6% from 11.1%. The company attributed this growth to "increased demand for power generation products in North America" and operational efficiencies.

The standout performer was the Power Systems Segment, which posted 19% revenue growth to $1.9 billion and expanded its EBITDA margin to 22.8% from 18.9%. This impressive growth was "driven primarily by increased power generation demand, particularly for data center and mission critical applications," highlighting the impact of the ongoing data center construction boom on Cummins’ business.

Meanwhile, the Accelera Segment, which focuses on clean energy technologies, saw a slight revenue decline but reduced its EBITDA loss to $100 million from $117 million in Q2 2024. This segment continues to invest in developing electric powertrains, fuel cells, and electrolyzers.

Strategic Initiatives & Market Position

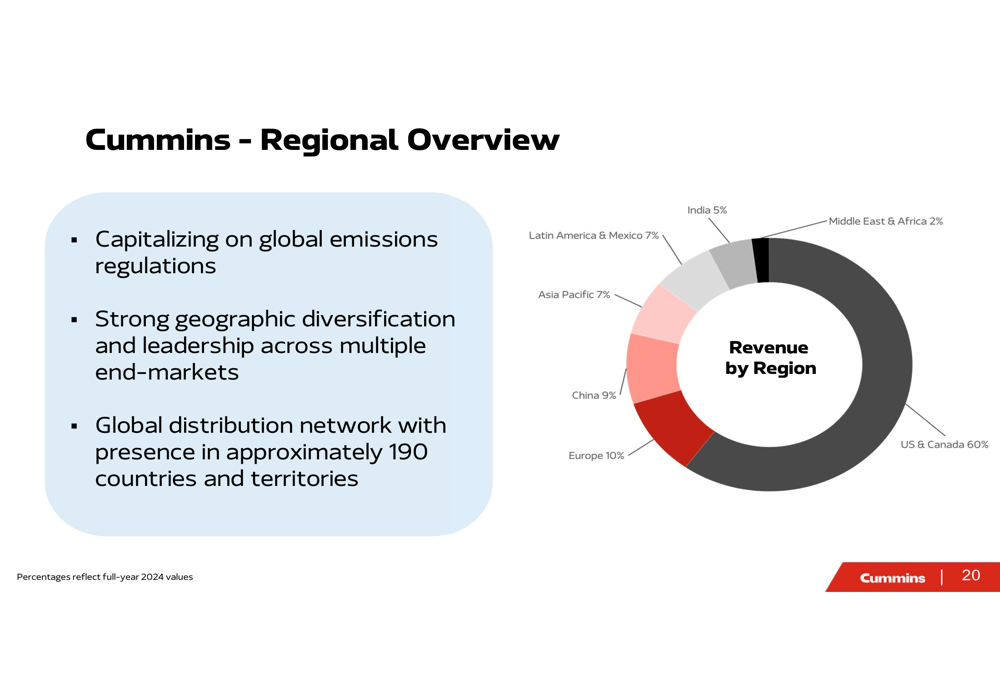

Cummins maintains a strong global presence with operations in approximately 190 countries. The company’s revenue distribution highlights its geographic diversification while maintaining a strong base in North America:

The company’s joint venture income increased to $118 million in Q2 2025 from $103 million in Q2 2024, with improvements across most segments. This performance underscores the value of Cummins’ strategic partnerships, particularly in emerging markets.

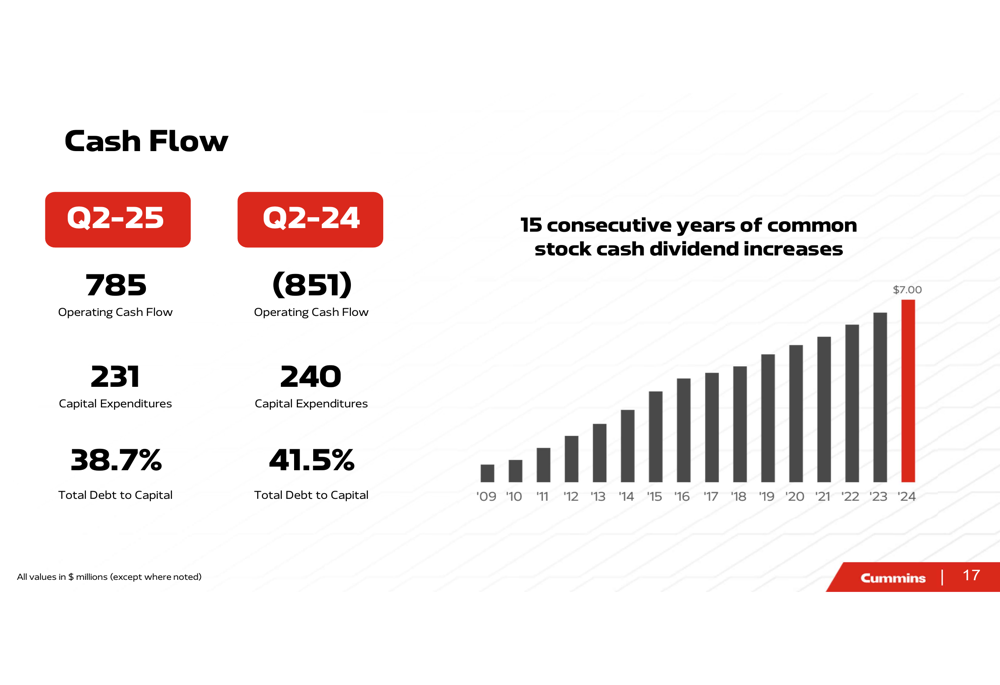

The company’s cash flow performance showed dramatic improvement, with Q2 2025 operating cash flow of $785 million compared to negative $851 million in Q2 2024. Capital expenditures remained relatively stable at $231 million, while the total debt to capital ratio improved to 38.7% from 41.5% a year earlier.

As illustrated in the cash flow summary below, Cummins has maintained 15 consecutive years of dividend increases:

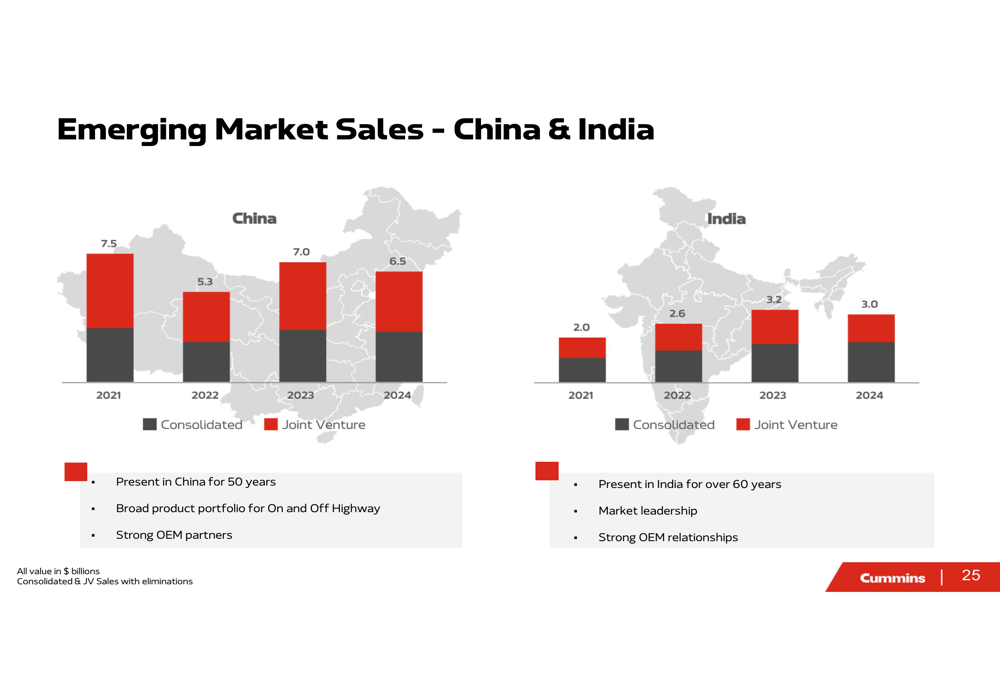

Cummins continues to focus on emerging markets, particularly China and India, where it has established operations for over 50 and 60 years, respectively. While these markets have experienced some fluctuations, they remain strategically important for the company’s long-term growth:

Forward-Looking Statements

The Q2 presentation did not specifically address the trade tariff concerns that led to the withdrawal of annual guidance during the Q1 earnings call. At that time, CEO Jennifer Rumsey had commented, "We are entering uncharted territory as the trade tariffs start to have a more significant impact," highlighting external pressures facing the company.

However, the Q2 results suggest that Cummins is successfully navigating these challenges through operational efficiencies and strategic focus on high-growth areas like data center power generation. The company’s ability to expand profit margins despite revenue headwinds in its traditional segments demonstrates effective cost management and strategic allocation of resources.

The continued growth in the Power Systems segment, particularly related to data center applications, positions Cummins to benefit from ongoing investments in digital infrastructure. Meanwhile, the improvement in the Accelera segment’s performance indicates progress in the company’s long-term strategy to develop clean energy solutions.

With the stock trading at $361.59 before the earnings release and jumping to $378.50 in premarket trading, investors appear to be responding positively to Cummins’ ability to deliver strong profitability despite mixed market conditions. The company’s consistent dividend growth and improved cash flow generation further reinforce investor confidence in its financial stability and long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.