Broadcom named strategic vendor for Walmart virtualization solutions

Introduction & Market Context

Curbline Properties Corp (NYSE:CURB) released its first quarter 2025 earnings presentation on April 24, showcasing strong portfolio growth and leasing performance amid its continued focus on convenience retail properties in affluent submarkets. The company’s stock closed at $23.40 prior to the earnings release, with premarket trading indicating a 4.62% jump to $24.48, suggesting positive investor reception to the results.

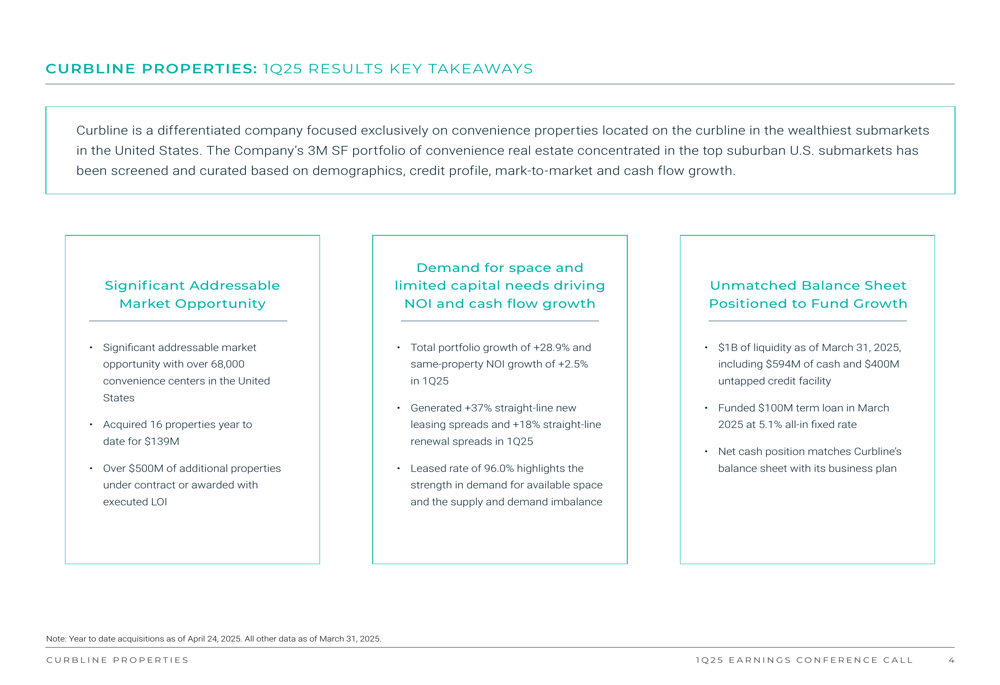

The convenience retail-focused REIT highlighted its substantial addressable market opportunity, with over 68,000 convenience centers across the United States, providing a robust pipeline for its acquisition-driven growth strategy.

Quarterly Performance Highlights

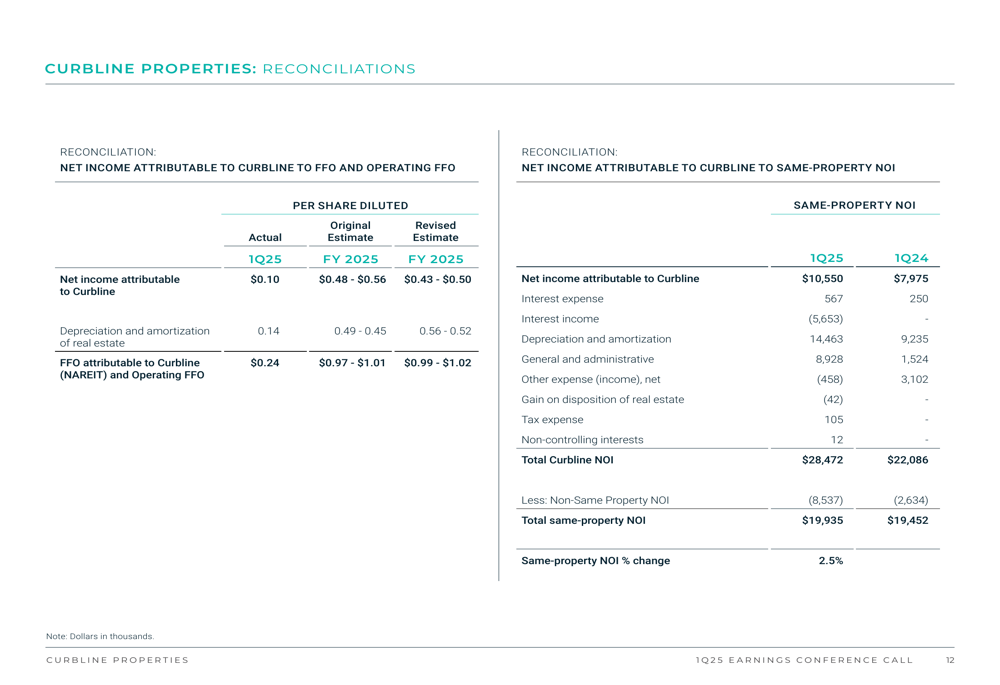

Curbline reported earnings per share of $0.10 for the first quarter, with Operating Funds From Operations (OFFO) per share reaching $0.24. The company achieved same-property net operating income (NOI) growth of 2.5% year-over-year, demonstrating solid performance from its existing portfolio.

As shown in the following summary of key financial metrics:

Particularly notable was Curbline’s leasing performance, with new cash lease spreads of 20.8% and blended cash lease spreads of 11.8% during the quarter. The company maintained a strong occupancy position with a 96.0% leased rate, which management attributed to the supply-demand imbalance for high-quality convenience real estate.

The following operations overview highlights the strength of Curbline’s tenant relationships and leasing momentum:

The company’s tenant roster includes national credit tenants such as Burger King, Einstein Bros Bagels, The UPS Store, Sherwin Williams, and T-Mobile, providing stability to its income stream. Management emphasized that the company’s properties benefit from superior access and visibility in desirable suburban locations, driving tenant demand and supporting higher rents.

Acquisition Strategy & Recent Deals

Curbline’s growth strategy remained firmly focused on acquisitions, with the company reporting $124 million in investment volume during Q1 2025 alone. Year-to-date, the REIT has acquired 16 properties for $139 million, with an additional pipeline of over $500 million in properties under contract or with executed letters of intent.

The following key takeaways slide illustrates Curbline’s strategic focus and acquisition momentum:

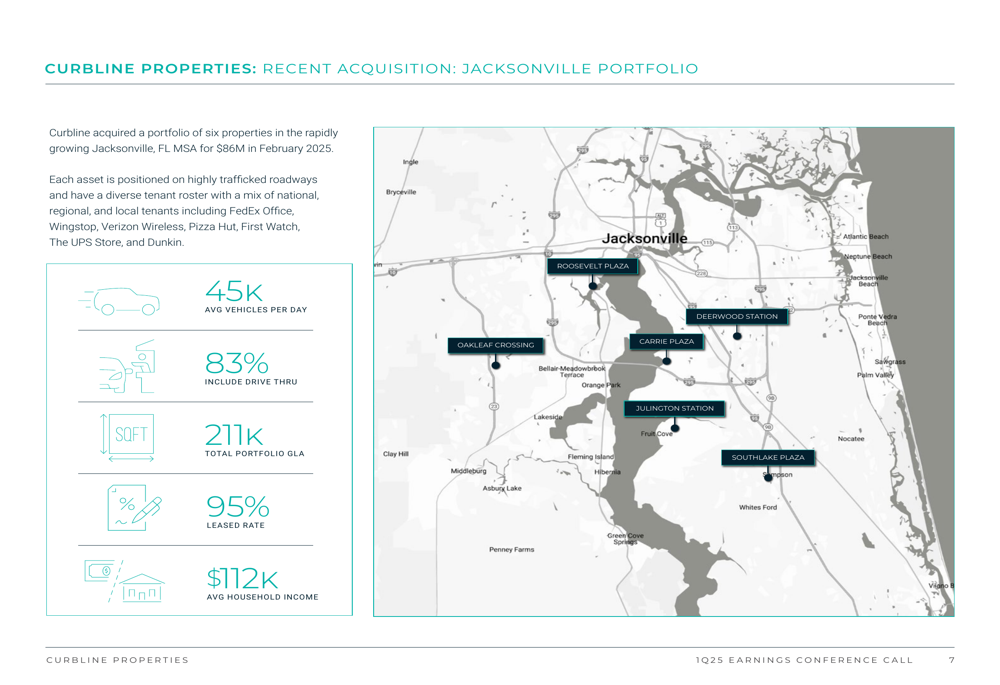

A highlight of the company’s recent acquisition activity was a six-property portfolio in the Jacksonville, Florida metropolitan area, purchased for $86 million in February 2025. These properties feature strong demographics with average household incomes of $112,000 in the surrounding areas and high traffic counts averaging 45,000 vehicles per day.

The Jacksonville acquisition is detailed in the following slide, showing the strategic clustering of properties:

Management noted that 83% of the acquired Jacksonville properties include drive-thru capabilities, an increasingly valuable feature in convenience retail. The portfolio spans 211,000 square feet of gross leasable area and was 95% leased at acquisition.

Balance Sheet Strength

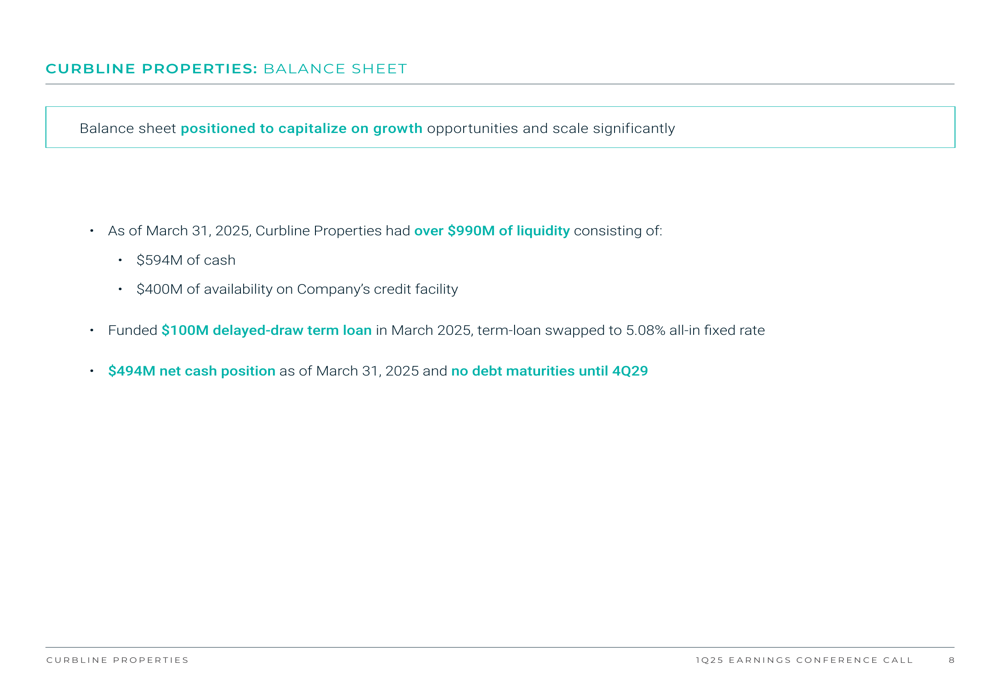

Curbline emphasized its strong financial position, with over $990 million in liquidity as of March 31, 2025. This includes $594 million in cash and $400 million available on the company’s credit facility, providing substantial dry powder for continued acquisitions.

The company’s balance sheet overview reveals its conservative financial approach:

In March 2025, Curbline funded a $100 million delayed-draw term loan, which was swapped to a 5.08% all-in fixed rate. The company highlighted its $494 million net cash position and the absence of any debt maturities until the fourth quarter of 2029, providing significant financial flexibility.

Revised Guidance & Outlook

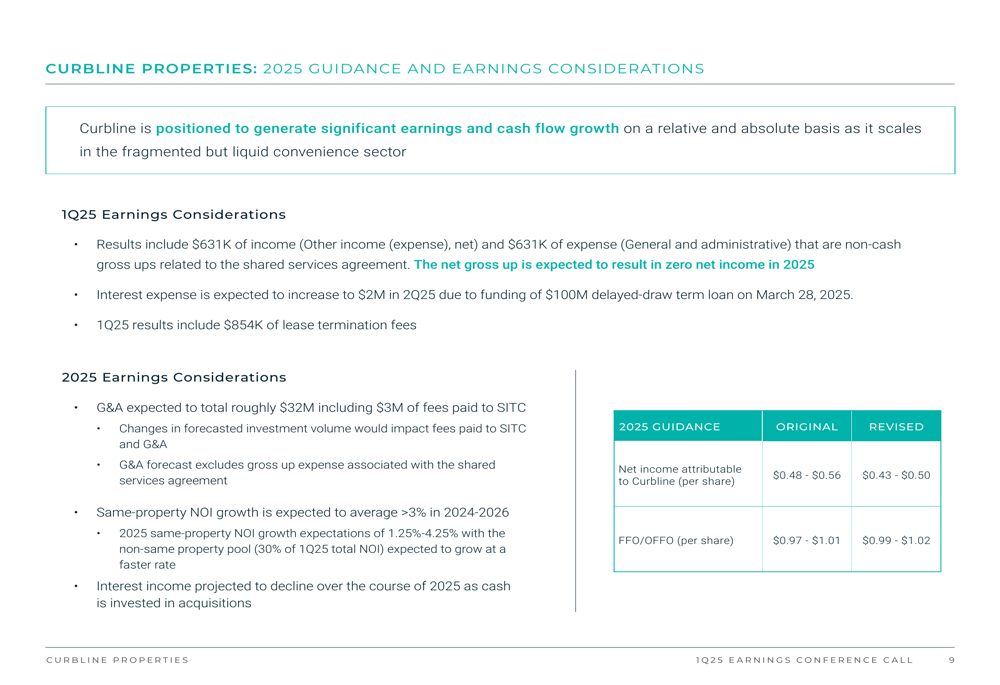

Curbline revised its full-year 2025 guidance, adjusting net income attributable to the company downward to $0.43-$0.50 per share from the original $0.48-$0.56 per share. However, the company raised its FFO/OFFO guidance to $0.99-$1.02 per share from the previous range of $0.97-$1.01 per share.

The following guidance slide details these revisions and provides additional earnings considerations:

Management noted that Q1 results included $854,000 in lease termination fees and explained that interest expense is expected to increase to $2 million in Q2 2025 due to the funding of the $100 million term loan. The company expects interest income to decline throughout the year as cash is deployed for acquisitions.

Looking ahead, Curbline projects same-property NOI growth to average greater than 3% between 2024-2026, reflecting confidence in the company’s ability to drive organic growth alongside its acquisition strategy.

The reconciliation of various financial metrics provides additional context for the company’s performance and guidance:

With its focus on convenience retail in affluent submarkets, substantial acquisition pipeline, and strong balance sheet, Curbline appears well-positioned to continue its growth trajectory through 2025, despite the slight downward adjustment to net income guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.