Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Curtiss-Wright Corporation (NYSE:CW) presented its second quarter 2025 earnings results on August 7, 2025, showcasing robust performance across both defense and commercial markets. The company reported significant growth in revenue, operating income, and earnings per share, building on the momentum established in the first quarter.

Trading at $509.32 as of August 6, 2025, Curtiss-Wright’s stock has shown strong performance over the past year, despite a slight 0.45% decrease from its previous close. The company’s Q2 results reflect its strategic positioning in high-growth defense sectors and the resurgent commercial nuclear market.

Quarterly Performance Highlights

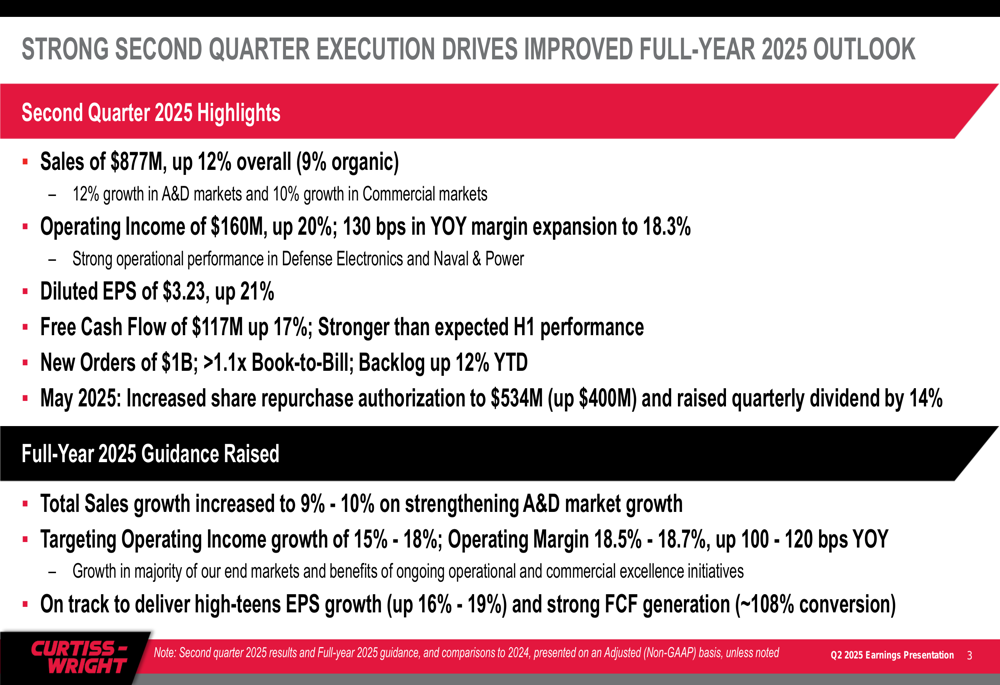

Curtiss-Wright delivered impressive second-quarter results, with sales reaching $877 million, representing a 12% increase overall (9% organic) compared to the same period last year. The company’s operating income surged 20% to $160 million, with operating margins expanding by 130 basis points to 18.3%. Diluted earnings per share grew 21% to $3.23.

As shown in the following quarterly highlights slide:

Free cash flow performance was particularly strong at $117 million, up 17% year-over-year, with the company noting stronger than expected first-half performance. New orders totaled $1 billion, resulting in a book-to-bill ratio exceeding 1.1x, while backlog increased 12% year-to-date.

The company also enhanced shareholder returns by increasing its share repurchase authorization to $534 million (up $400 million) and raising its quarterly dividend by 14% in May 2025.

Detailed Financial Analysis

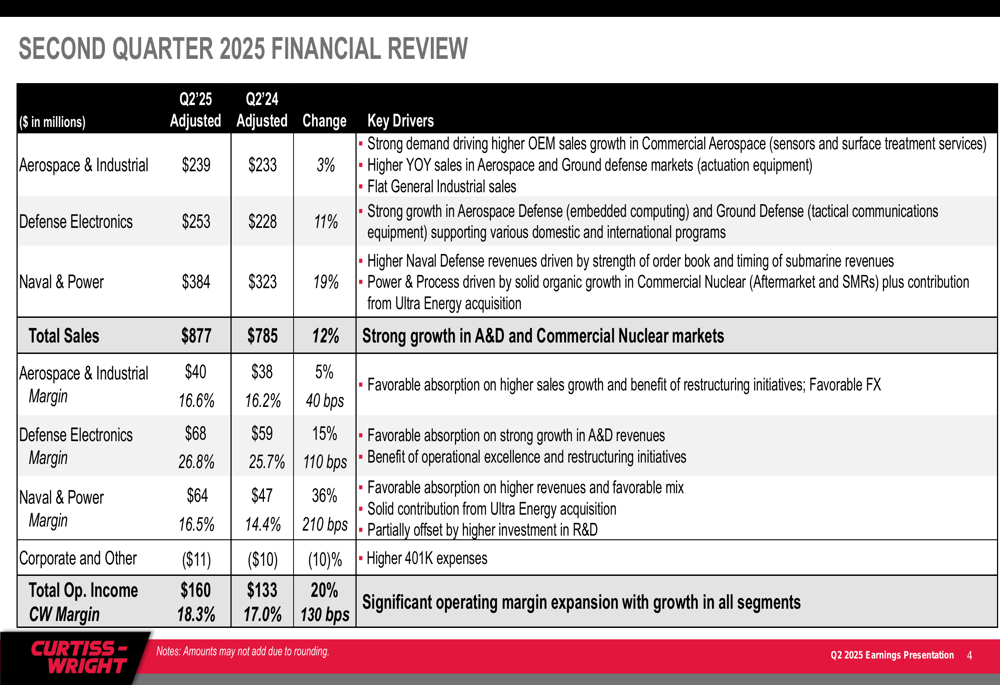

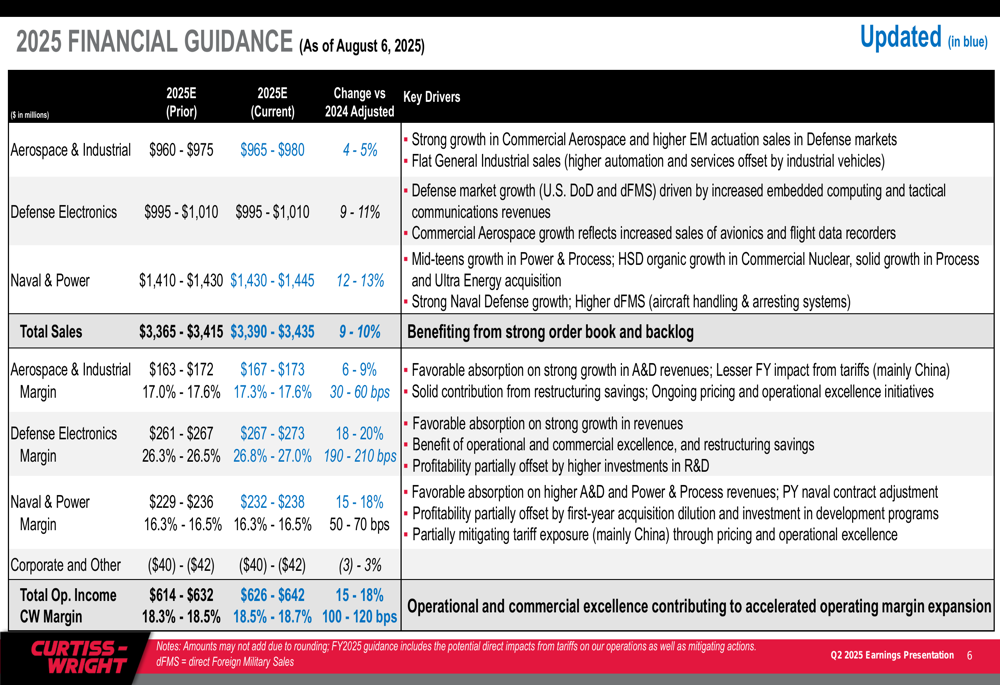

Curtiss-Wright’s performance was strong across all three business segments, with particularly notable results in the Naval & Power segment, which saw a 19% increase in sales and a 210 basis point improvement in operating margin.

The detailed segment breakdown reveals:

The Defense Electronics segment delivered an impressive 26.8% operating margin, up 110 basis points year-over-year, driven by strong growth in Aerospace Defense and Ground Defense markets. The Aerospace & Industrial segment showed more modest but still positive growth, with sales up 3% and margins improving by 40 basis points to 16.6%.

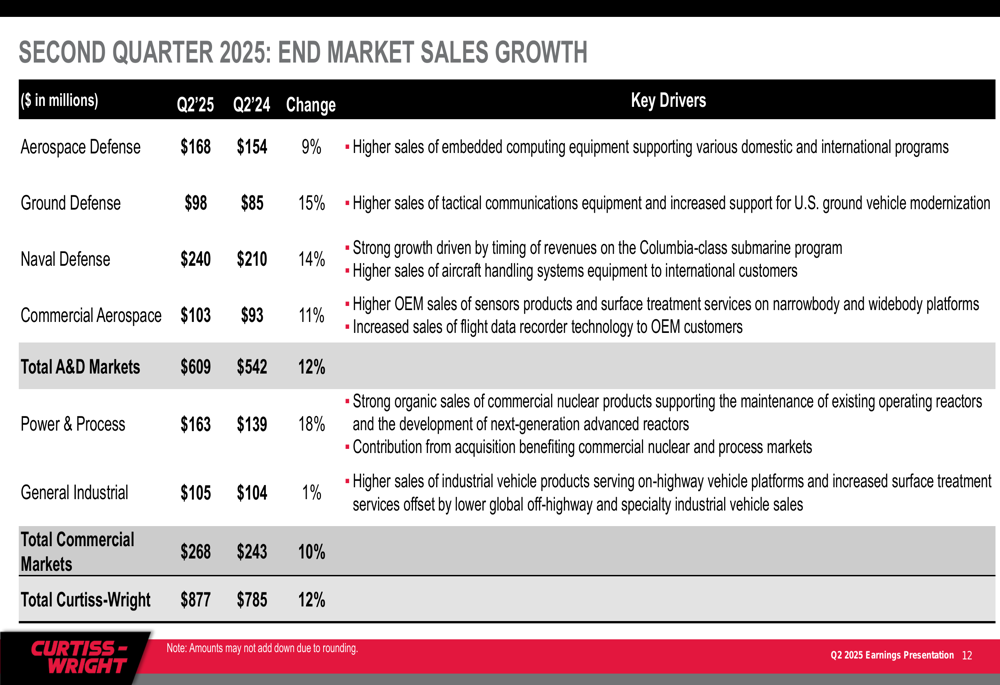

Looking at end market performance, Curtiss-Wright saw double-digit growth in most of its key markets:

The company’s defense markets showed particularly strong performance, with Ground Defense up 15%, Naval Defense up 14%, and Aerospace Defense up 9%. On the commercial side, Power & Process markets grew 18%, while Commercial Aerospace increased 11%. Only the General Industrial market showed modest growth at 1%.

Strategic Initiatives

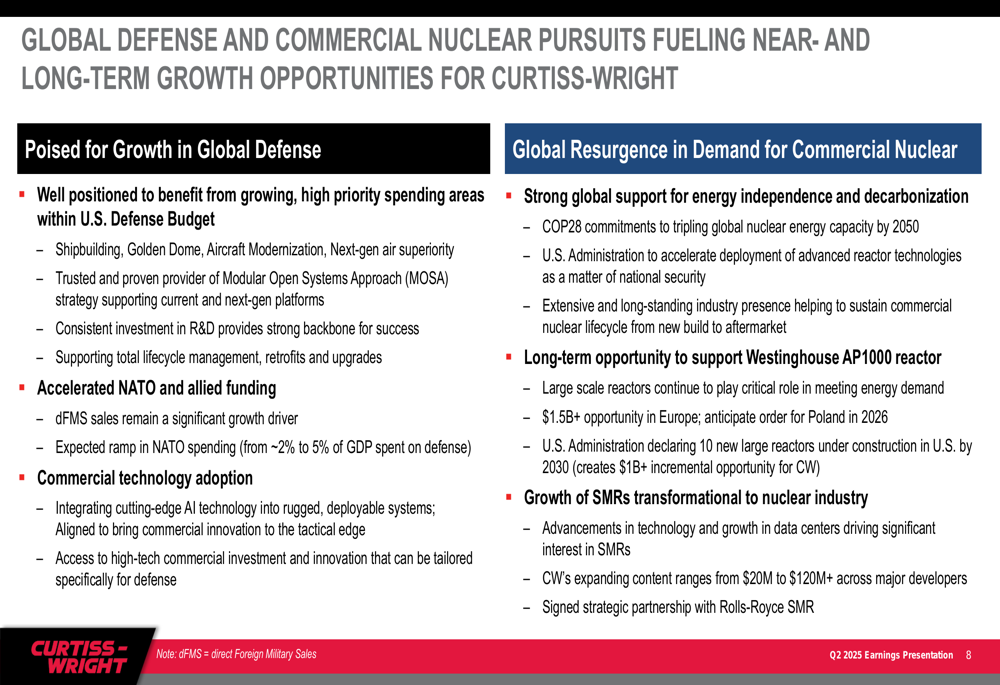

Curtiss-Wright highlighted its strategic positioning in global defense and commercial nuclear markets, which are experiencing significant growth due to increased defense spending and renewed interest in nuclear energy.

The company outlined its growth opportunities in these key markets:

In defense markets, Curtiss-Wright is benefiting from growing U.S. defense budget priorities, accelerated NATO and allied funding, and commercial technology adoption. The company’s strong presence in naval defense (26% of sales) positions it well to capitalize on submarine and surface ship programs.

The commercial nuclear market represents a significant growth opportunity, driven by global support for energy independence and decarbonization. Curtiss-Wright highlighted long-term opportunities to support the Westinghouse AP1000 reactor and the transformational growth potential of Small Modular Reactors (SMRs).

Forward-Looking Statements

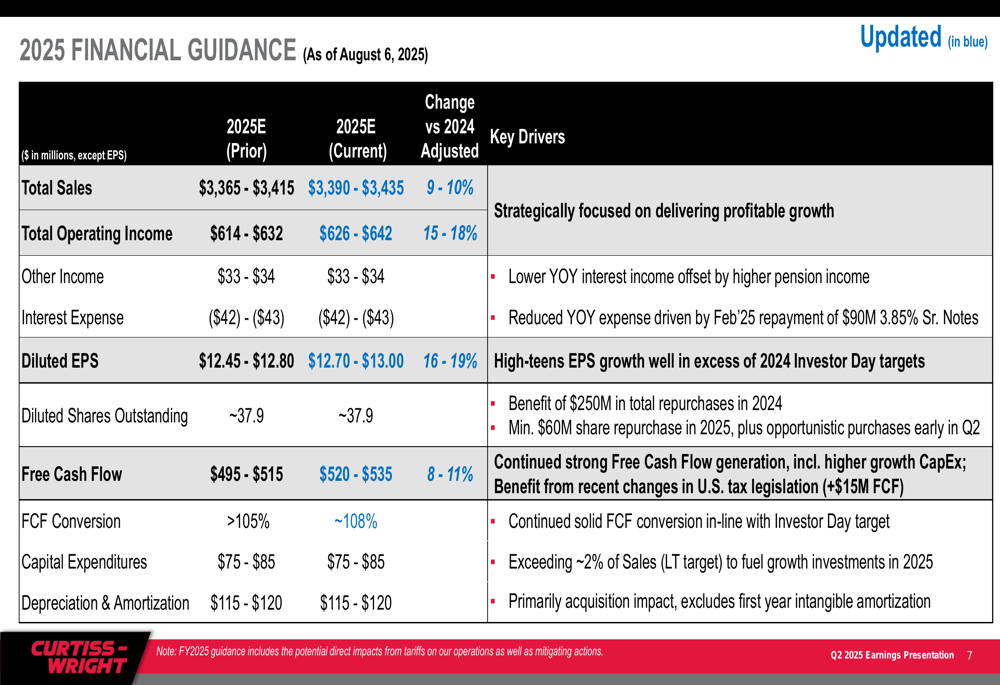

Based on its strong first-half performance, Curtiss-Wright raised its full-year 2025 guidance across all key metrics. The company now expects:

Total (EPA:TTEF) sales growth is projected at 9-10%, up from previous guidance, with the Naval & Power segment expected to lead growth at 12-13%. Operating margins are forecast to expand by 100-120 basis points to 18.5-18.7%, with the Defense Electronics segment maintaining the highest margins at 26.8-27.0%.

The company provided additional financial guidance details:

Diluted EPS is now expected to grow 16-19% to $12.70-$13.00, while free cash flow is projected at $520-$535 million, representing 8-11% growth and approximately 108% conversion.

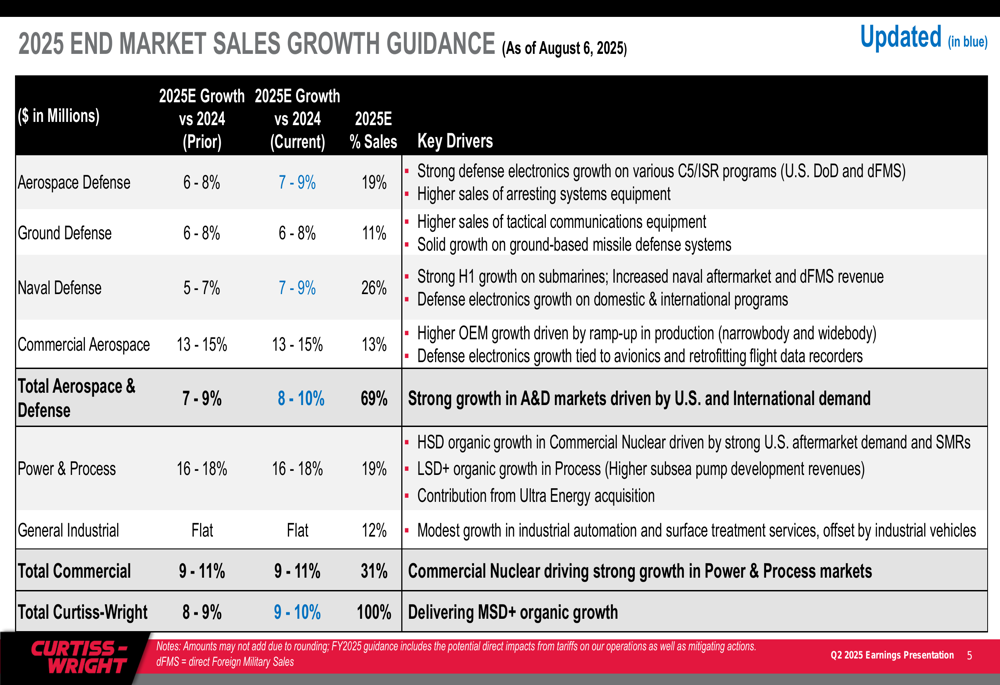

Curtiss-Wright’s end market outlook shows strong growth across most sectors:

The company projects 8-10% growth in Aerospace & Defense markets, which represent 69% of total sales, and 9-11% growth in Commercial markets, which account for 31% of sales. The Power & Process segment is expected to show the strongest growth at 16-18%, driven by high single-digit organic growth in Commercial Nuclear.

Conclusion

Curtiss-Wright’s Q2 2025 results demonstrate the company’s continued execution of its growth strategy and operational excellence initiatives. The strong performance across both defense and commercial markets, coupled with significant margin expansion, has enabled the company to raise its full-year guidance.

The company’s strategic positioning in growing defense markets and the resurgent commercial nuclear sector provides a solid foundation for continued growth. With a robust order book, improving margins, and disciplined capital allocation, Curtiss-Wright appears well-positioned to deliver on its long-term financial targets.

As CEO Lynn Bamford noted in the previous quarter’s earnings call, the company is "off to a great start in 2025," and the second-quarter results further reinforce this positive trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.