Asia FX moves little with focus on US-China trade, dollar steadies ahead of CPI

Introduction & Market Context

Custom Truck One Source, Inc. (NYSE:CTOS) released its first quarter 2025 investor presentation on April 30, showing modest revenue growth amid mixed segment performance. The specialty equipment provider reported a 2.7% year-over-year revenue increase to $422 million, while adjusted EBITDA declined slightly to $73 million from $77 million in the prior-year period.

The company’s stock closed at $4.23 on April 30, down 4.73% for the day, and continued declining in after-hours trading, falling an additional 4.96% to $3.83. This performance comes after a significant 29.85% surge following the company’s Q4 2024 earnings beat in February.

Custom Truck One Source operates as an integrated provider of specialty equipment serving infrastructure, transmission and distribution (T&D), rail, and telecom markets across North America with over 10,000 fleet units and 40 locations.

Quarterly Performance Highlights

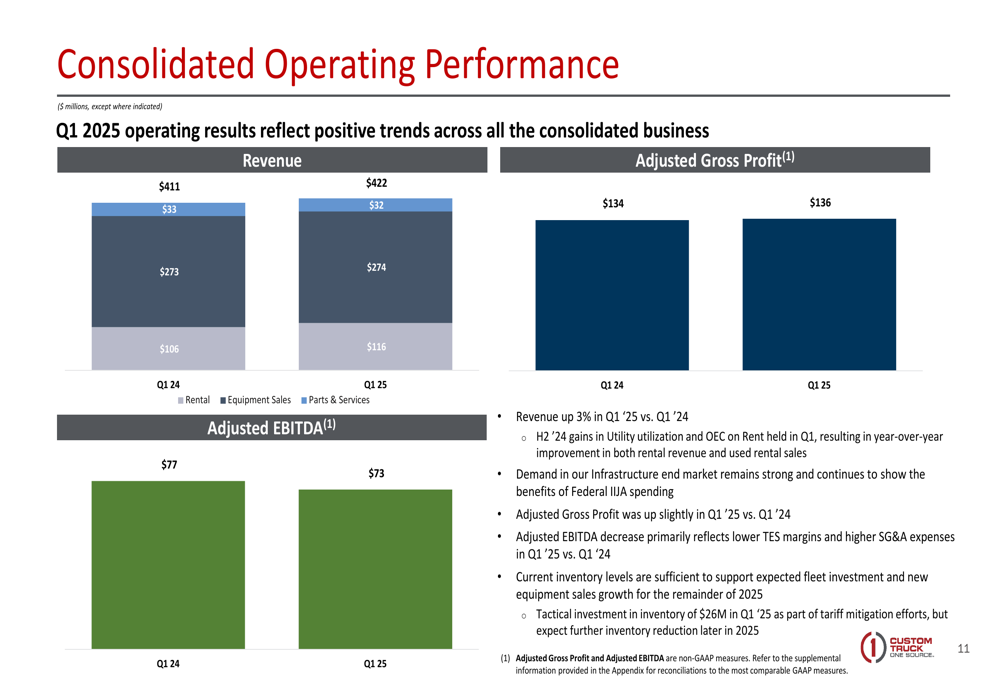

Custom Truck One Source reported Q1 2025 revenue of $422 million, up from $411 million in Q1 2024. However, adjusted EBITDA declined to $73 million from $77 million in the prior-year period. Adjusted gross profit showed a modest improvement, reaching $136 million compared to $134 million a year earlier.

The company highlighted strong fundamentals across all end markets and product categories, with particularly robust performance in its Equipment Rental Solutions (ERS) segment. Management emphasized the company’s strategic inventory investment to support demand for new equipment sales and serve as a catalyst for further investment in the ERS fleet.

As shown in the following consolidated operating performance chart:

The company’s revenue mix for Q1 2025 consisted of $32 million from rental, $274 million from equipment sales, and $116 million from parts and services. While rental revenue decreased slightly year-over-year, parts and services revenue showed healthy growth.

Segment Performance Analysis

Custom Truck One Source operates through three main segments: Equipment Rental Solutions (ERS), Truck & Equipment Sales (TES), and Aftermarket Parts & Service (APS).

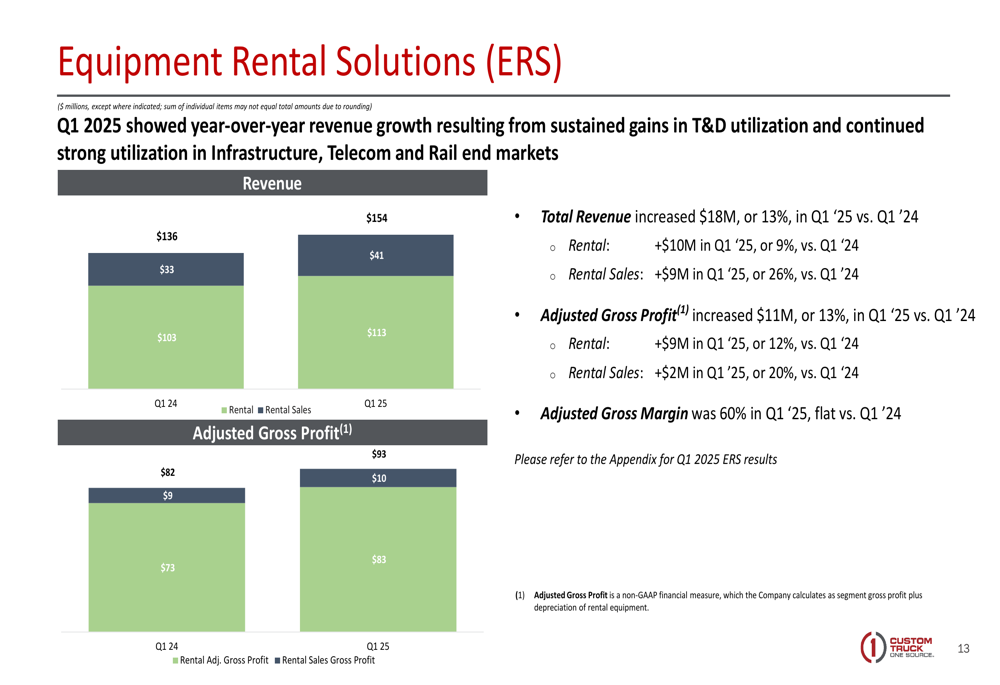

The ERS segment was a standout performer in Q1 2025, with total revenue increasing 13% year-over-year to $154 million. Rental revenue grew 9% while rental sales jumped 26% compared to Q1 2024. The segment’s adjusted gross profit increased 13% to $93 million, maintaining a strong 60% adjusted gross margin.

The following chart illustrates the ERS segment’s performance:

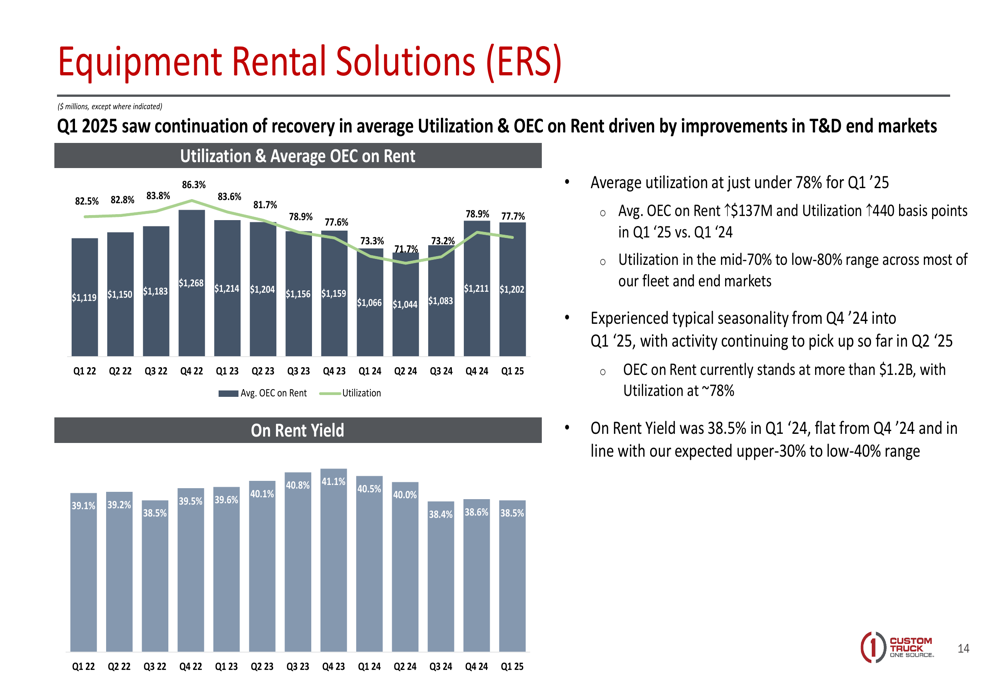

Fleet utilization metrics also showed improvement, with average utilization reaching nearly 78% in Q1 2025, up 440 basis points from Q1 2024. Average OEC (Original Equipment Cost) on rent increased by $137 million year-over-year, while on-rent yield remained steady at 38.5%.

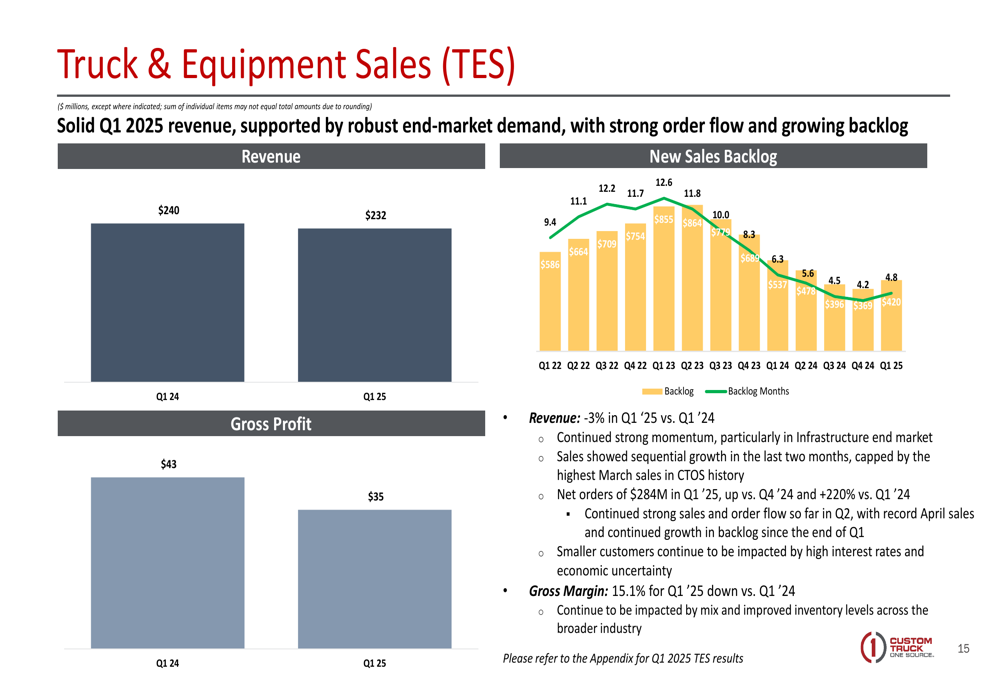

The TES segment experienced a slight 3% revenue decline in Q1 2025 compared to Q1 2024, with gross margin contracting to 15.1%. However, the segment showed promising future growth potential with net orders of $284 million in Q1 2025, representing a substantial 220% increase compared to Q1 2024.

The following chart shows the TES segment’s performance and backlog growth:

The APS segment reported flat revenue year-over-year, with adjusted gross margin declining to 22% in Q1 2025 from the prior year period.

Strategic Positioning and Growth Outlook

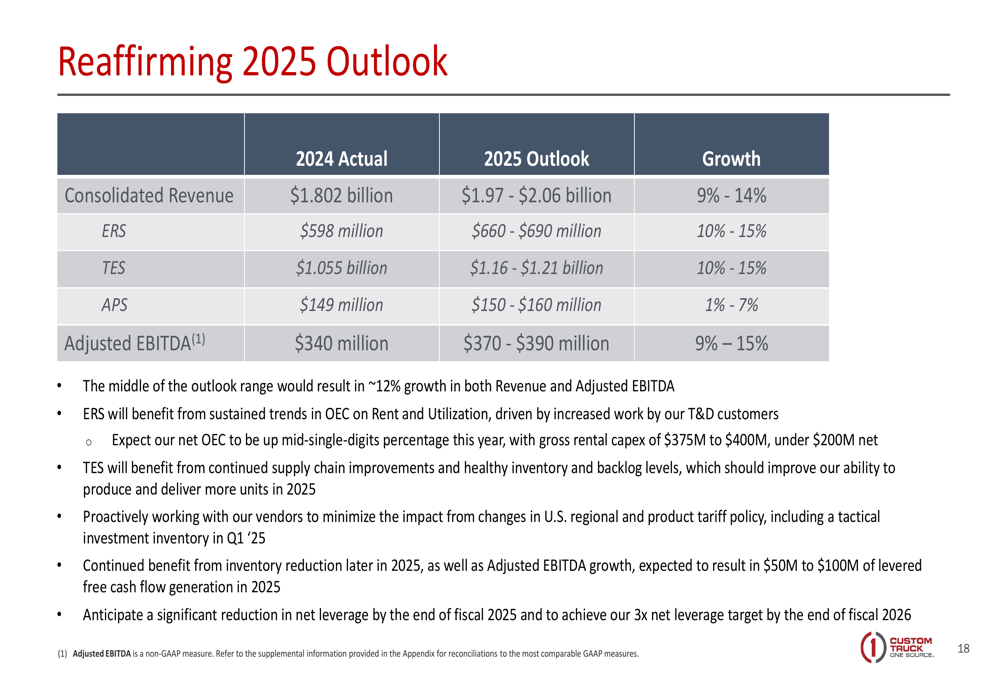

Custom Truck One Source reaffirmed its full-year 2025 outlook, projecting consolidated revenue between $1.97 billion and $2.06 billion, representing 9-14% growth. The company expects adjusted EBITDA to reach $370-390 million, reflecting 9-15% growth.

The segment-level guidance shows:

- ERS: $660-690 million (10-15% growth)

- TES: $1.16-1.21 billion (10-15% growth)

- APS: $150-160 million (1-7% growth)

The following chart details the company’s 2025 outlook:

The company highlighted its unique "one-stop-shop" business model as a key competitive advantage, providing integrated production capabilities and multiple revenue streams across diverse end markets. This model delivers both customer benefits (end-to-end solutions, customization) and company advantages (superior unit economics, production efficiencies).

Custom Truck One Source serves over 8,000 customers, with the top 15 customers representing approximately 18% of revenue and no single customer accounting for more than 3% of company revenue. The company emphasized its 15+ year tenure with top customers and strong brand recognition in the industry.

The company also highlighted favorable end-market dynamics, particularly in transmission and distribution (T&D) and infrastructure, which are benefiting from the Infrastructure Investment and Jobs Act (IIJA). T&D capex is expected to reach approximately $95 billion in 2024, while infrastructure capex is projected at around $302 billion.

Balance Sheet and Capital Allocation

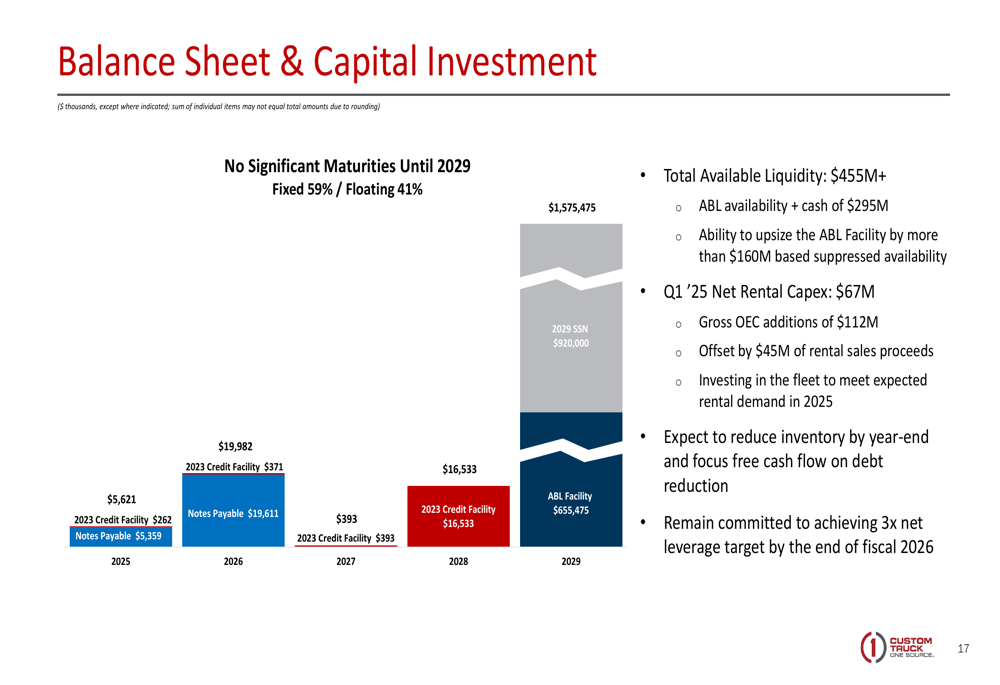

Custom Truck One Source reported total available liquidity exceeding $455 million as of Q1 2025. The company invested $67 million in net rental capex during the quarter and reiterated its commitment to reducing inventory by year-end and focusing free cash flow on debt reduction.

The following chart shows the company’s balance sheet and capital investment strategy:

Management emphasized there are no significant debt maturities until 2029 and reaffirmed its target to achieve 3x net leverage by the end of fiscal 2026. This focus on deleveraging aligns with statements made during the Q4 2024 earnings call, where the company noted its current net leverage of 4.5x and the goal to reduce it below 4x by the end of 2025.

The company’s balance sheet strategy includes reducing inventory levels while continuing strategic investments in its rental fleet, positioning Custom Truck One Source to capitalize on infrastructure spending trends while improving financial flexibility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.