US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

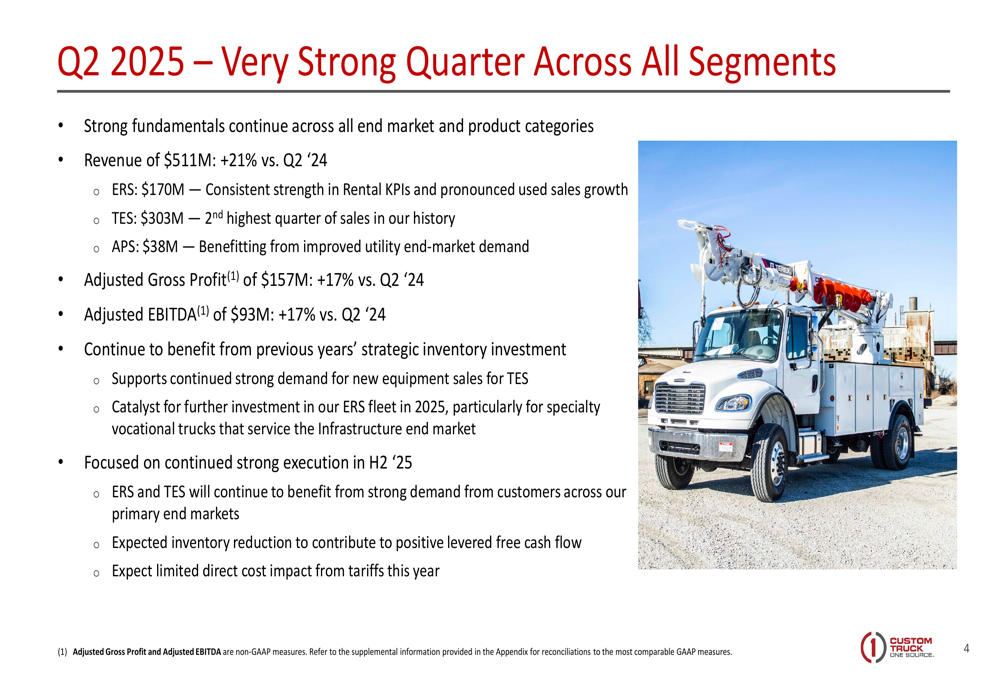

Custom Truck One Source (NYSE:CTOS), a leading provider of specialty equipment rental and sales solutions, presented its second-quarter 2025 results on July 30, showcasing a significant rebound from its disappointing first-quarter performance. The company reported substantial growth across all business segments, with particularly strong performance in its rental and equipment sales divisions.

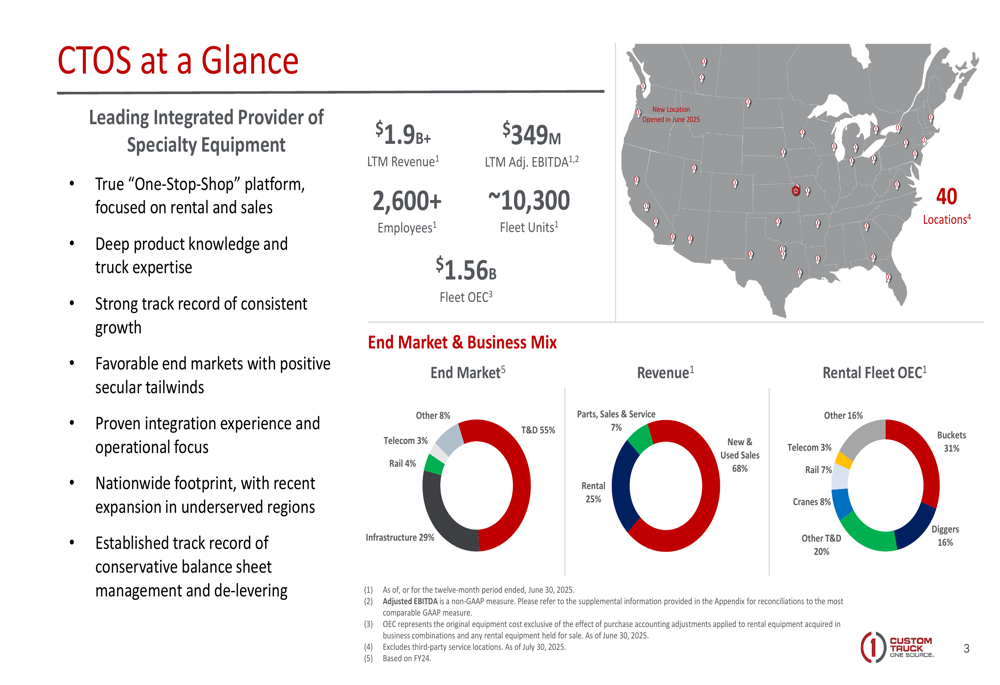

The specialty equipment provider serves diverse end markets including transmission and distribution (55%), infrastructure (29%), rail (4%), and telecom (3%), positioning it to benefit from ongoing infrastructure investment and utility modernization efforts. After missing analyst expectations in Q1 2025, when revenue came in at $422 million against projections of $434.49 million, CTOS has demonstrated a strong recovery in Q2.

As shown in the following chart detailing the company’s business profile and market position:

Quarterly Performance Highlights

Custom Truck One Source reported Q2 2025 revenue of $511 million, representing a 21% increase compared to Q2 2024. Adjusted gross profit rose 17% year-over-year to $157 million, while adjusted EBITDA also grew 17% to $93 million. This performance marks a significant improvement from the company’s Q1 results, which fell short of analyst expectations.

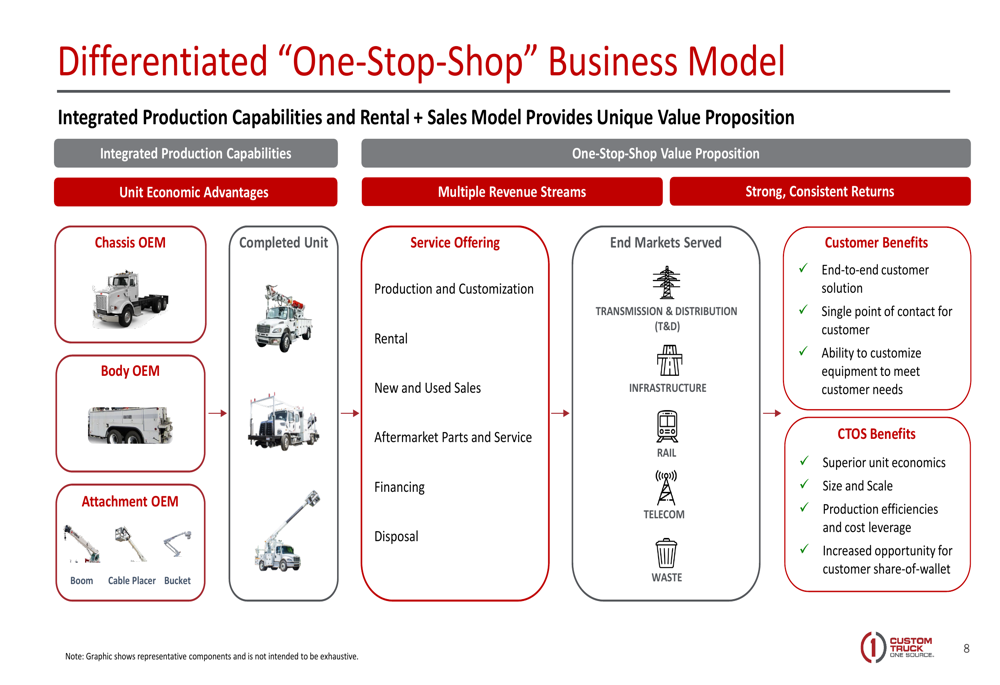

The company’s integrated "one-stop-shop" business model continues to drive its competitive advantage, offering customers end-to-end solutions from production and customization to rental, sales, aftermarket services, and financing. This comprehensive approach has helped CTOS maintain strong relationships with over 8,000 customers, with no single customer representing more than 3% of company revenue.

The following slide illustrates the company’s strong quarterly performance:

CTOS’s differentiated business model, which combines manufacturing capabilities with comprehensive service offerings, continues to be a key driver of its success:

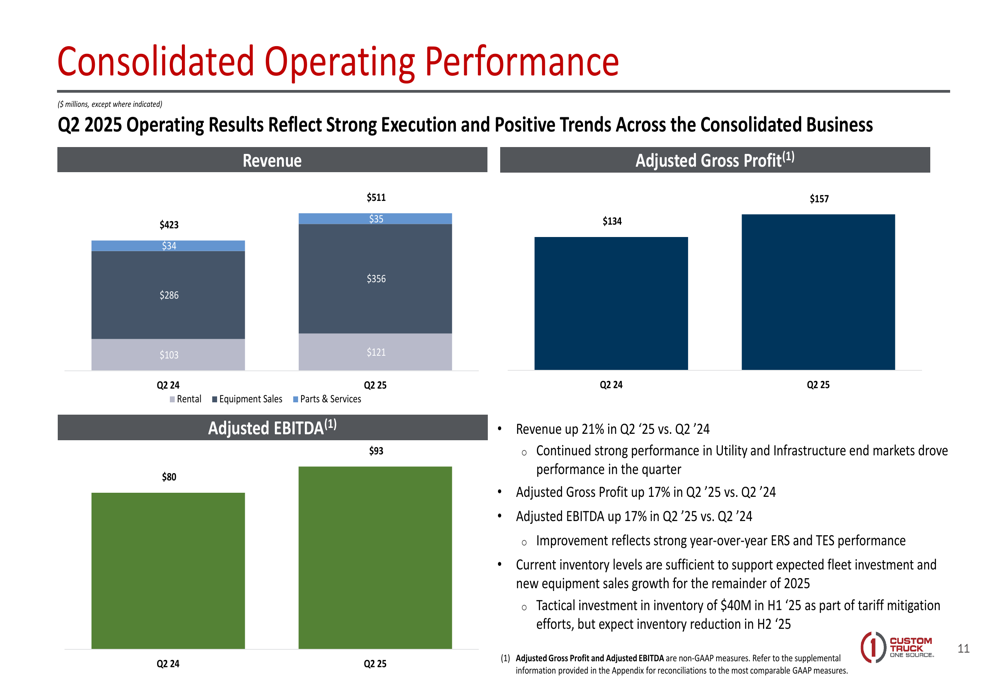

The company’s consolidated operating performance shows significant year-over-year improvements across all revenue streams:

Segment Performance Analysis

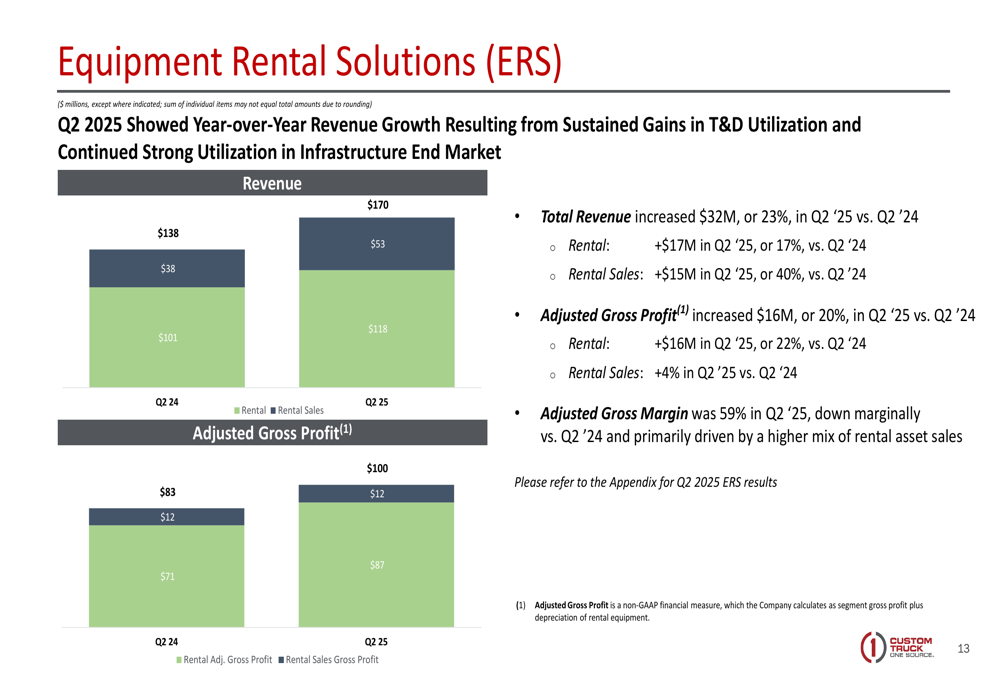

The Equipment Rental Solutions (ERS) segment delivered particularly strong results, with revenue increasing by $32 million, or 23%, compared to Q2 2024. Rental revenue grew by $17 million (17%), while rental sales increased by $15 million (40%). Adjusted gross profit for the segment rose by $16 million (20%), with an adjusted gross margin of 59% in Q2 2025.

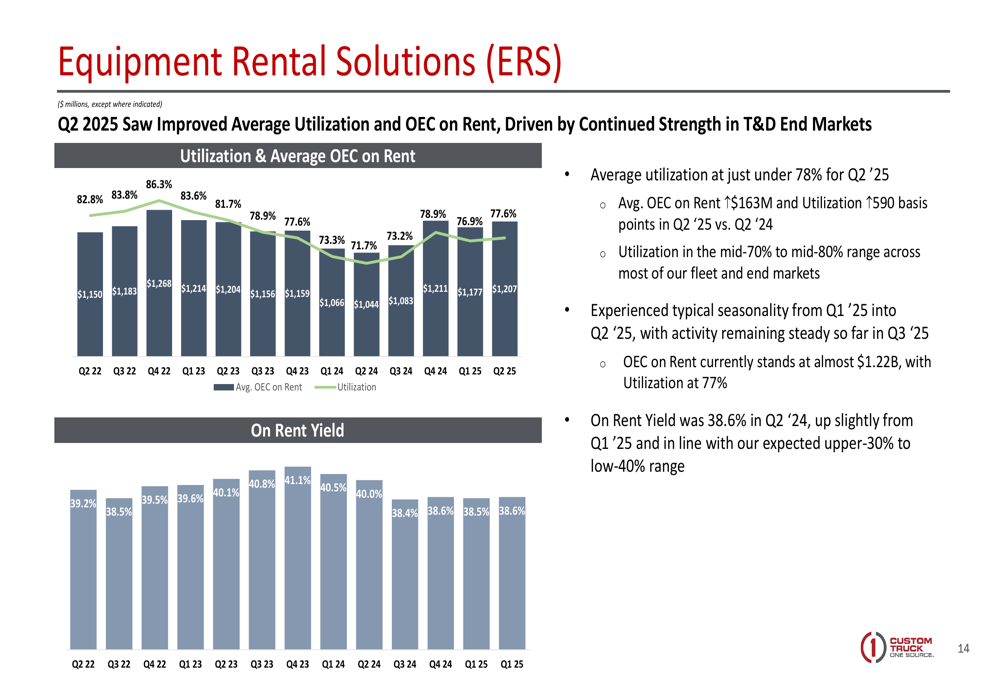

A key driver of the ERS segment’s performance was improved fleet utilization, which reached nearly 78% in Q2 2025, representing a 590 basis point increase year-over-year. Average Original Equipment Cost (OEC) on rent increased by $163 million compared to the same period last year.

The following chart details the ERS segment’s financial performance:

Fleet utilization metrics demonstrate the company’s operational efficiency improvements:

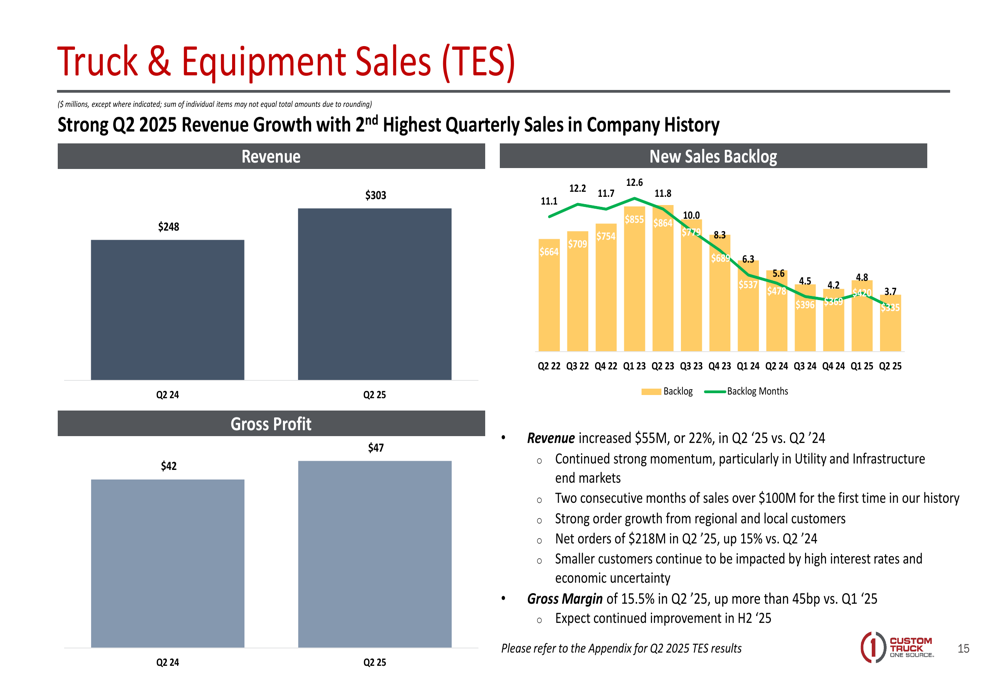

The Truck & Equipment Sales (TES) segment also showed strong growth, with revenue increasing by $55 million (22%) compared to Q2 2024. The segment maintained a gross margin of 15.5% in Q2 2025, with gross profit rising to $47 million from $42 million in the prior year period.

The following slide illustrates the TES segment’s performance:

The Aftermarket Parts & Service (APS) segment saw more modest growth, with revenue increasing by 3% year-over-year to $38 million. However, the segment improved its adjusted gross margin to 26% in Q2 2025, contributing to a 25% increase in adjusted gross profit.

Balance Sheet and Capital Strategy

Despite strong operational performance, Custom Truck One Source continues to manage a significant debt burden. The company’s leverage ratio stood at 4.66 in Q2 2025, reflecting its capital-intensive business model. Management reaffirmed its commitment to reducing net leverage to 3x by the end of fiscal 2026.

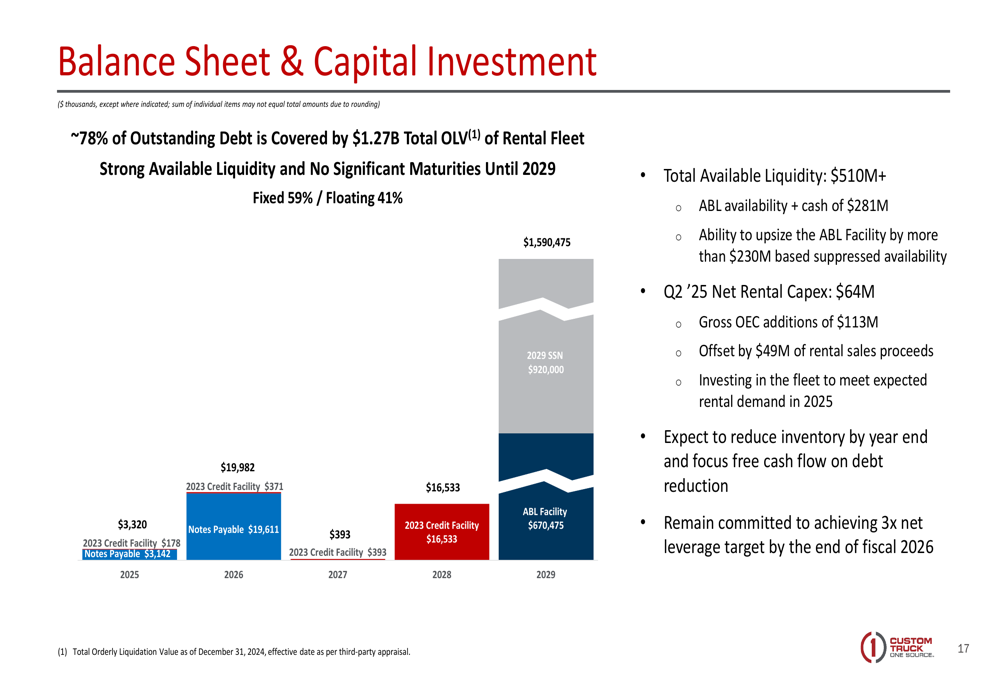

The company highlighted that approximately 78% of its outstanding debt is covered by the $1.27 billion total orderly liquidation value (OLV) of its rental fleet. CTOS maintains strong available liquidity of over $510 million, with no significant debt maturities until 2029. The company reported Q2 2025 net rental capital expenditures of $64 million as it continues to invest in fleet growth.

The following slide provides details on the company’s balance sheet and capital investment strategy:

Forward Outlook and Guidance

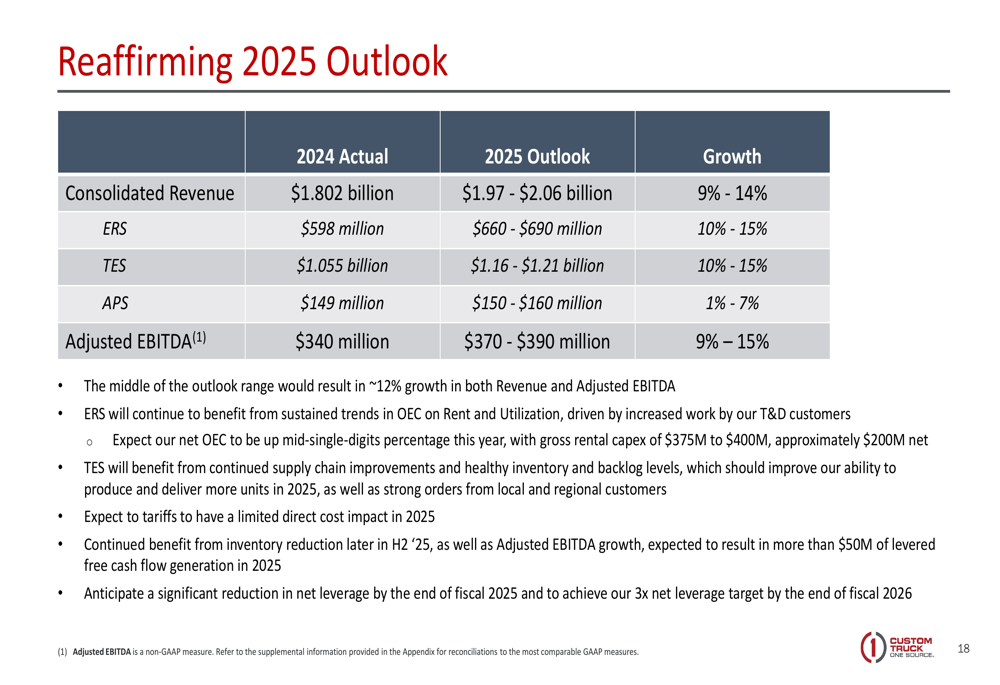

Custom Truck One Source reaffirmed its full-year 2025 guidance, projecting consolidated revenue between $1.97 billion and $2.06 billion, representing 9% to 14% growth. The company expects adjusted EBITDA to reach between $370 million and $390 million, reflecting 9% to 15% growth.

By segment, CTOS forecasts:

- ERS revenue of $660-$690 million (10-15% growth)

- TES revenue of $1.16-$1.21 billion (10-15% growth)

- APS revenue of $150-$160 million (1-7% growth)

Management noted that achieving the midpoint of the guidance range would result in approximately 12% growth in both revenue and adjusted EBITDA for the full year.

The following slide details the company’s 2025 outlook:

Custom Truck One Source continues to benefit from favorable end-market dynamics, including ongoing investments in utility infrastructure, transportation, and telecommunications. The company’s nationwide footprint of 40 locations, including recent expansions into underserved regions, positions it well to capitalize on these market opportunities while providing comprehensive support to its diverse customer base.

While the company faces challenges related to its high leverage ratio, its strong operational performance and strategic focus on high-demand market segments provide a foundation for continued growth. Investors will be watching closely to see if CTOS can maintain its growth momentum while making progress toward its leverage reduction targets in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.