Tesla could be a $10,000 stock in a decade, says longtime bull Ron Baron

Custom Truck One Source (NYSE:CTOS) presented its third-quarter 2025 results on October 28, revealing strong year-over-year growth across key metrics despite missing analyst expectations. The specialty equipment provider saw its shares tumble 14.76% following the earnings announcement, as investors reacted to the company’s slight miss on both revenue and earnings per share.

Quarterly Performance Highlights

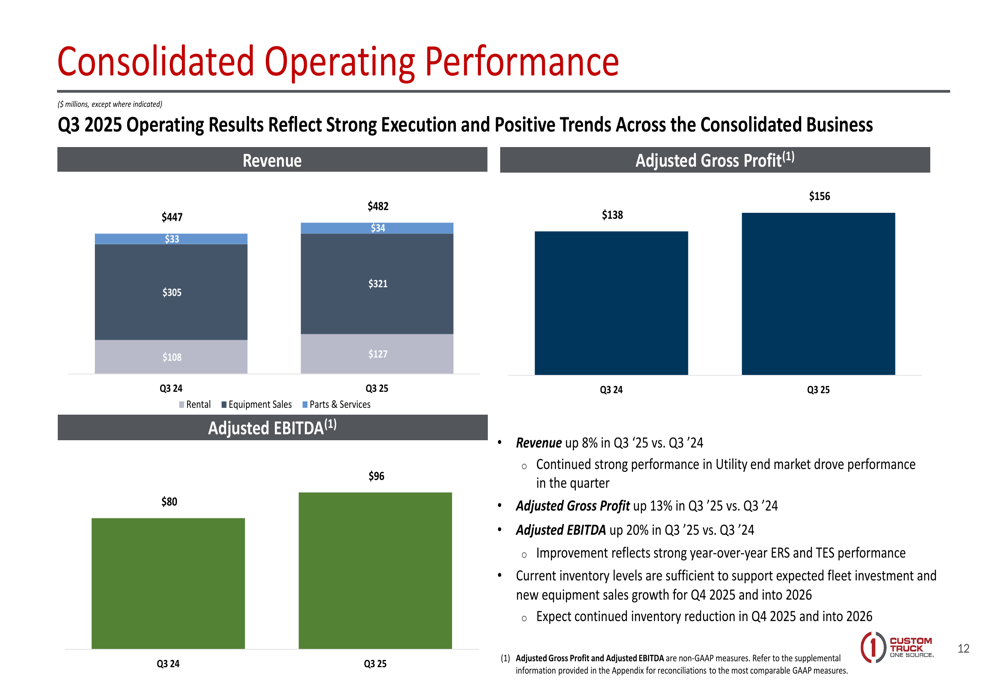

Custom Truck One Source reported Q3 2025 revenue of $482 million, representing an 8% increase compared to the same period last year. However, this figure fell short of analyst expectations of $492.38 million. The company posted an adjusted EBITDA of $96 million, up 20% year-over-year, and adjusted gross profit of $156 million, a 13% improvement from Q3 2024.

"We’re seeing really good demand in the utility sector and transmission and distribution," said CEO Ryan McMonagle during the earnings call, highlighting the company’s positive momentum despite the earnings miss.

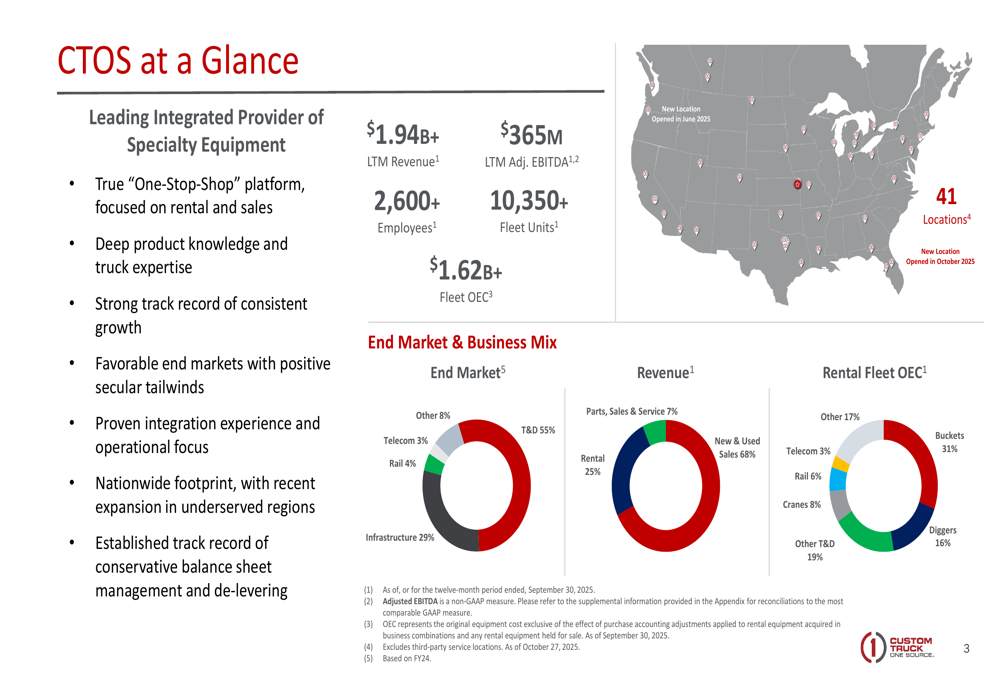

The company’s performance metrics reflect its diverse business model across multiple segments and end markets, as illustrated in this comprehensive overview:

Segment Performance Analysis

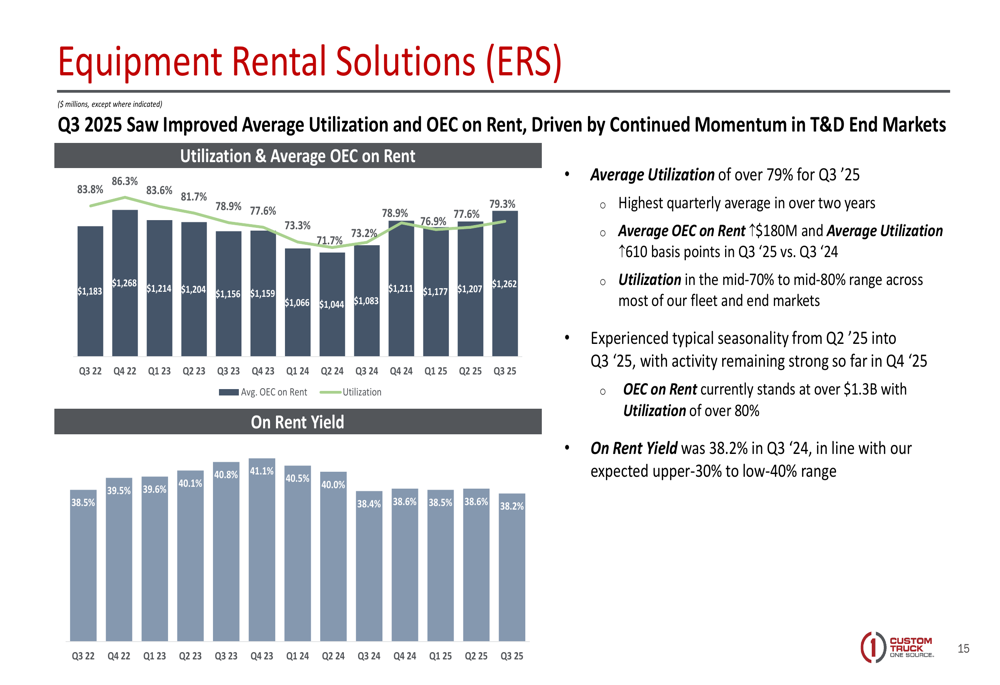

The Equipment Rental Solutions (ERS) segment demonstrated particularly strong performance, with revenue increasing by $18 million or 12% compared to Q3 2024. Rental revenue alone grew by 18%, while adjusted gross profit for the segment increased by 19%. The company achieved an adjusted gross margin of 62%, representing a 370 basis point improvement year-over-year.

Fleet utilization metrics show continued operational efficiency, with average utilization exceeding 79% for Q3 2025, a 610 basis point improvement compared to the same period last year:

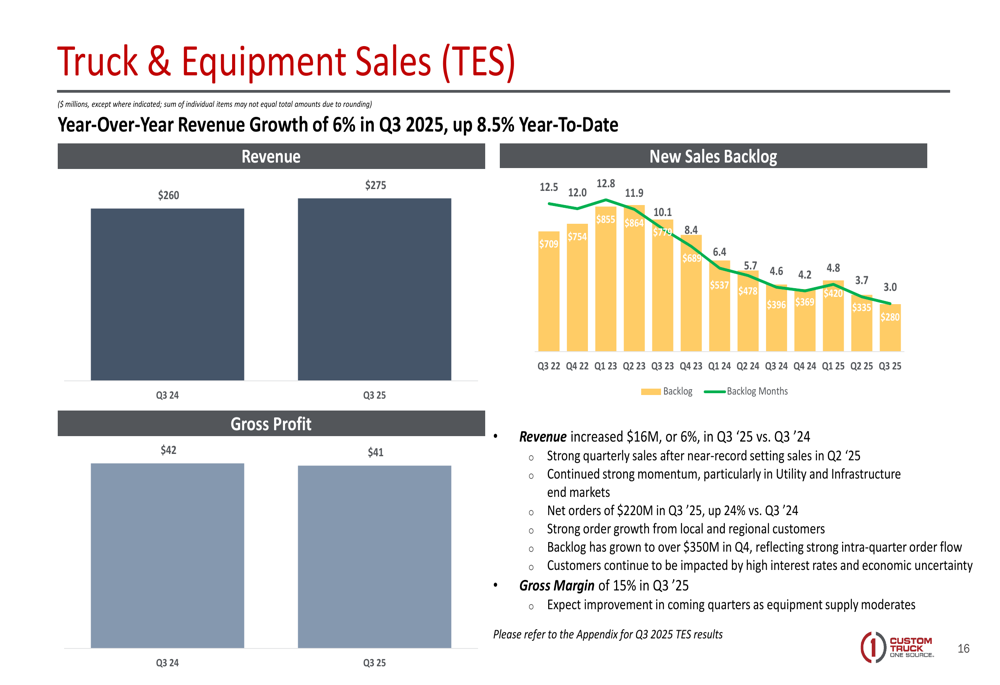

The Truck & Equipment Sales (TES) segment also contributed to growth, with revenue increasing by $16 million or 6% compared to Q3 2024. This segment maintained a gross margin of 15% during the quarter:

The Aftermarket Parts & Service (APS) segment showed modest growth with revenue up 3% year-over-year and improved profitability, achieving an adjusted gross margin of 26% compared to 23% in Q3 2024.

Overall, the company’s consolidated operating performance demonstrates consistent growth across key financial metrics:

Strategic Business Model & Market Position

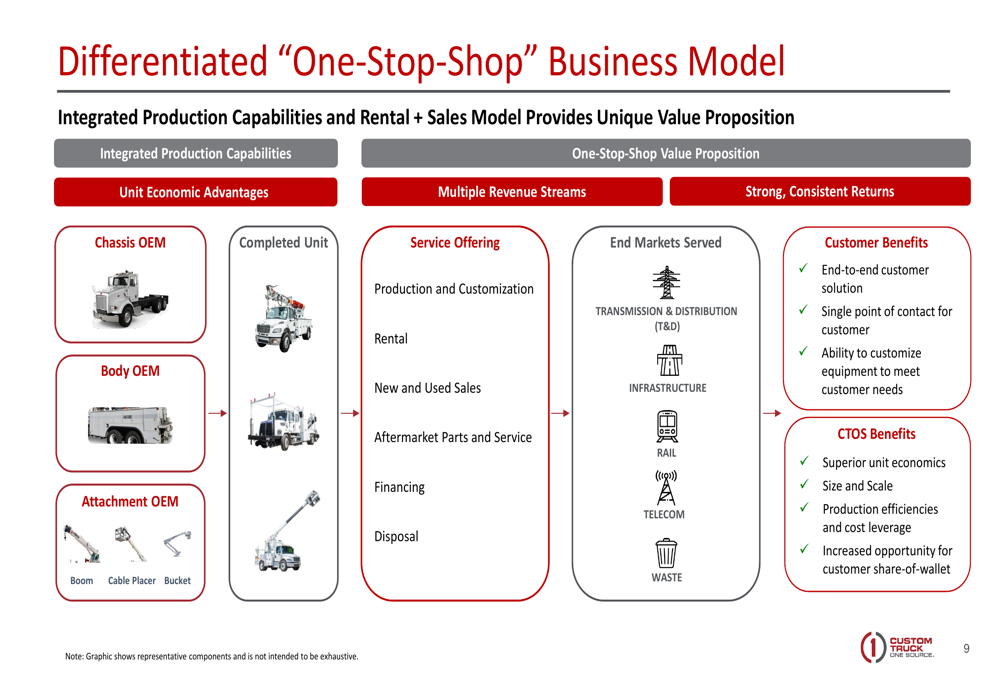

Custom Truck One Source continues to leverage its differentiated "One-Stop-Shop" business model, which integrates multiple revenue streams and provides comprehensive solutions for customers. This integrated approach enables the company to capture value across the equipment lifecycle while delivering superior unit economics.

The following illustration demonstrates how the company’s business model creates value for both customers and shareholders:

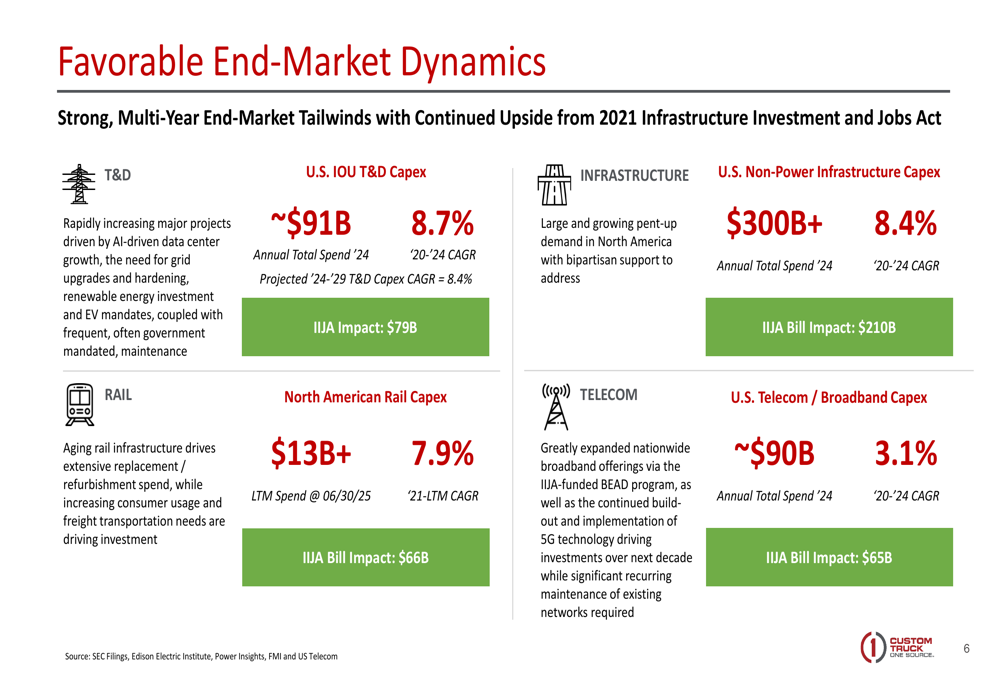

The company maintains a strong position in growing end markets, particularly in Transmission & Distribution (T&D), which represents 55% of its business. According to the presentation, T&D capital spending among U.S. Investor-Owned Utilities is projected to total almost $600 billion from 2025 to 2029, growing at an 8.4% CAGR, with transmission spending expected to grow even faster at a 15%+ CAGR.

This favorable market outlook is supported by several megatrends, including AI-related data center investment, electrification of vehicles and buildings, onshoring of manufacturing, and extreme weather events:

Forward Outlook & Financial Targets

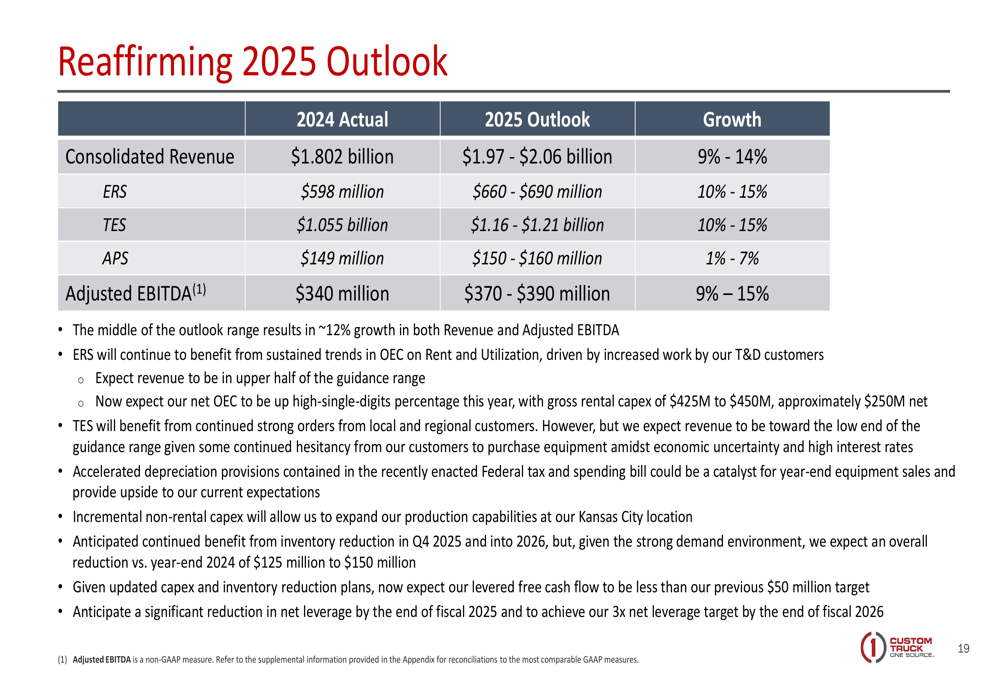

Despite the earnings miss, Custom Truck One Source reaffirmed its full-year 2025 guidance, projecting revenue between $1.97 billion and $2.06 billion (9-14% growth) and adjusted EBITDA between $370 million and $390 million (9-15% growth). The company expects continued strong demand across its primary end markets.

The detailed outlook by segment shows the company’s confidence in sustained growth across all business units:

From a balance sheet perspective, Custom Truck One Source is focusing on inventory reduction and debt management. The company aims to reduce its net leverage to below 3x by the end of fiscal 2026, down from the current 4.53x. Management indicated they expect to reduce inventory by year-end and into 2026, with free cash flow primarily directed toward debt reduction.

Market Reaction & Investor Concerns

Despite the positive year-over-year growth and reaffirmed guidance, investors reacted negatively to the earnings results. CTOS shares fell 14.76% following the announcement, with premarket trading showing an 8.16% decline to $6.19.

The market response appears to reflect concerns about the company’s earnings miss, with EPS coming in at -$0.03 compared to the forecasted -$0.02. Additionally, the revenue shortfall of approximately $10 million compared to analyst expectations may have raised questions about the company’s ability to fully capitalize on the strong end-market demand it highlights.

CFO Chris Eperjesy addressed some of these concerns during the earnings call, expressing optimism about long-term demand drivers despite macroeconomic uncertainties: "Our year-to-date results and the continued strong fundamentals of our end markets allow us to be optimistic about the long-term demand drivers in our industry."

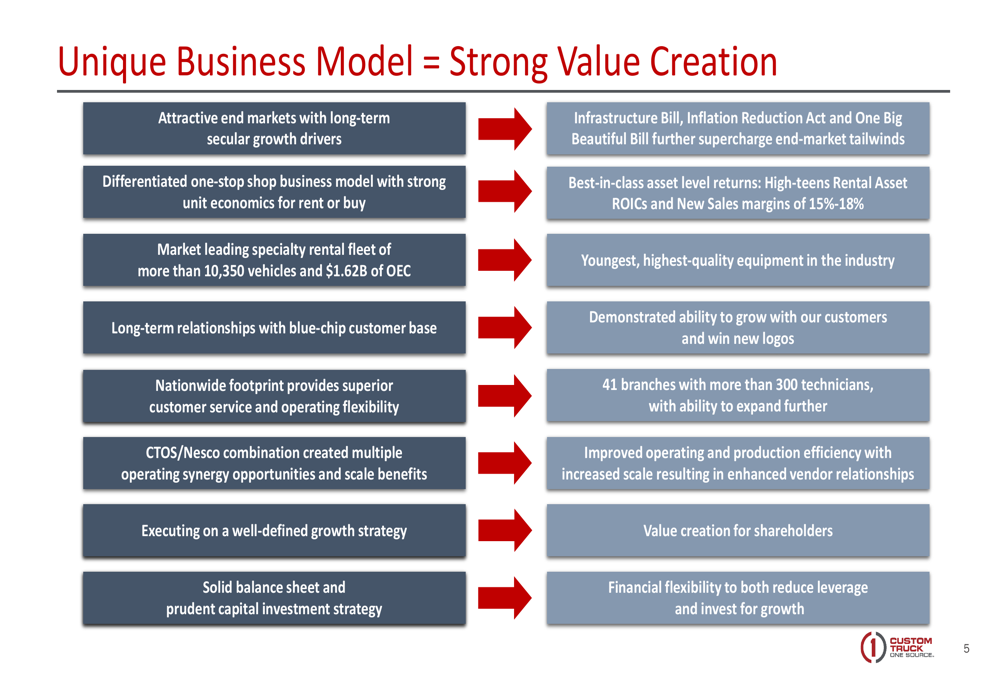

The company’s unique value proposition and business model remain core strengths, as illustrated in this strategic overview:

While Custom Truck One Source faces near-term challenges in meeting analyst expectations, its strong year-over-year growth, favorable end-market dynamics, and strategic focus on debt reduction position the company for potential long-term success. Investors will likely monitor the company’s progress in inventory reduction, debt management, and its ability to capitalize on the projected growth in its key end markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.