Microsoft shares jump after fourth-quarter earnings beat on AI-fueled cloud growth

Introduction & Market Context

Dana Incorporated (NYSE:DAN) presented its first-quarter 2025 earnings results on April 30, showing lower sales across all segments but maintaining its full-year guidance as the company accelerates cost-saving initiatives to offset volume declines. The automotive and industrial parts supplier reported that its results were "largely in line with expectations" despite challenging market conditions.

The company’s stock, which closed at $12.99 on April 29, showed positive momentum in premarket trading with a 3.93% increase to $13.50, suggesting investors were encouraged by Dana’s maintained outlook and cost management efforts despite the sales decline.

Quarterly Performance Highlights

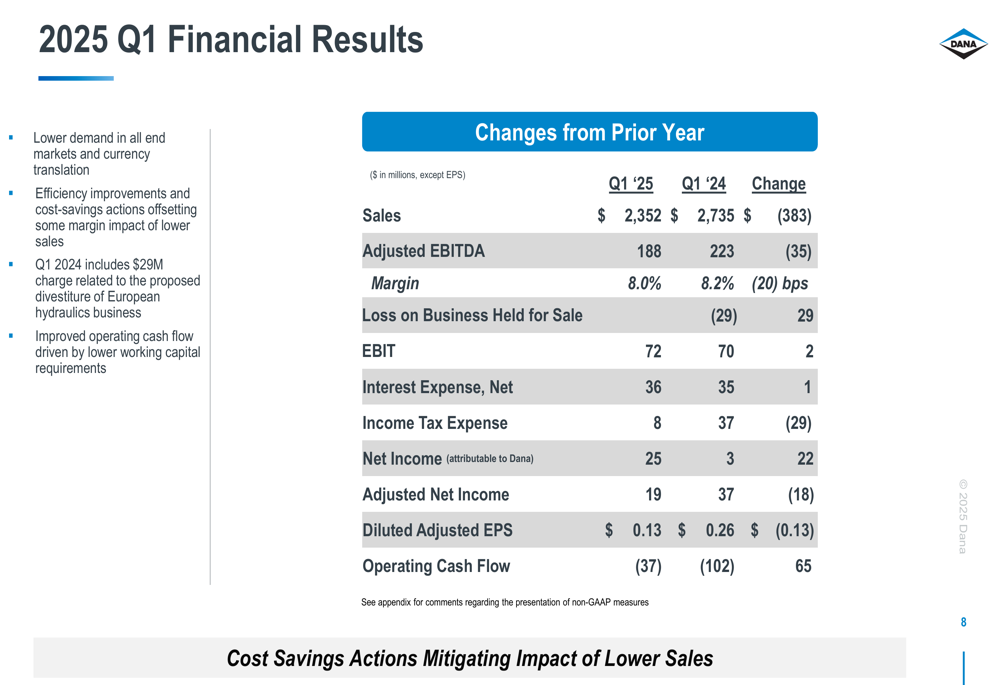

Dana reported first-quarter 2025 sales of $2,352 million, down 14% from $2,735 million in the same period last year. The decline was primarily attributed to lower demand across all end markets and negative currency translation effects.

Despite the sales drop, the company’s adjusted EBITDA margin remained relatively stable at 8.0%, compared to 8.2% in Q1 2024, as efficiency improvements and cost-saving actions helped offset the impact of lower volumes.

As shown in the following comprehensive financial results:

The company’s net income improved to $25 million from $3 million in the prior-year quarter, though adjusted net income decreased to $19 million from $37 million. Diluted adjusted EPS fell to $0.13 from $0.26 in Q1 2024.

Dana’s operating cash flow improved significantly to negative $37 million from negative $102 million in the prior-year period, driven by lower working capital requirements. This resulted in a $67 million improvement in adjusted free cash flow year-over-year.

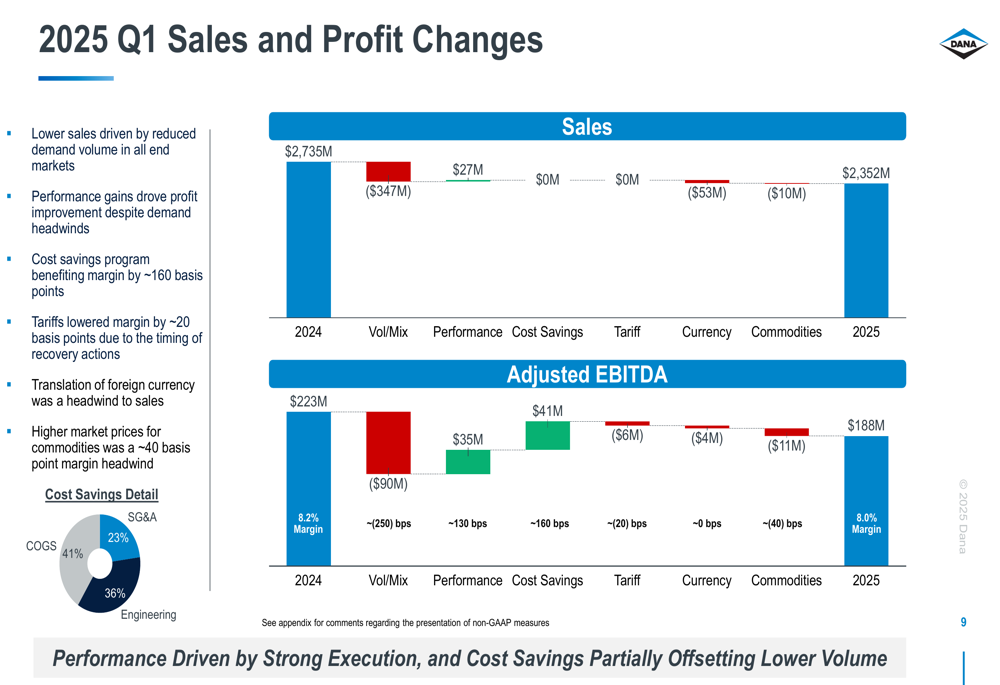

The following waterfall chart illustrates the key factors affecting Dana’s sales and profit performance:

Segment Performance

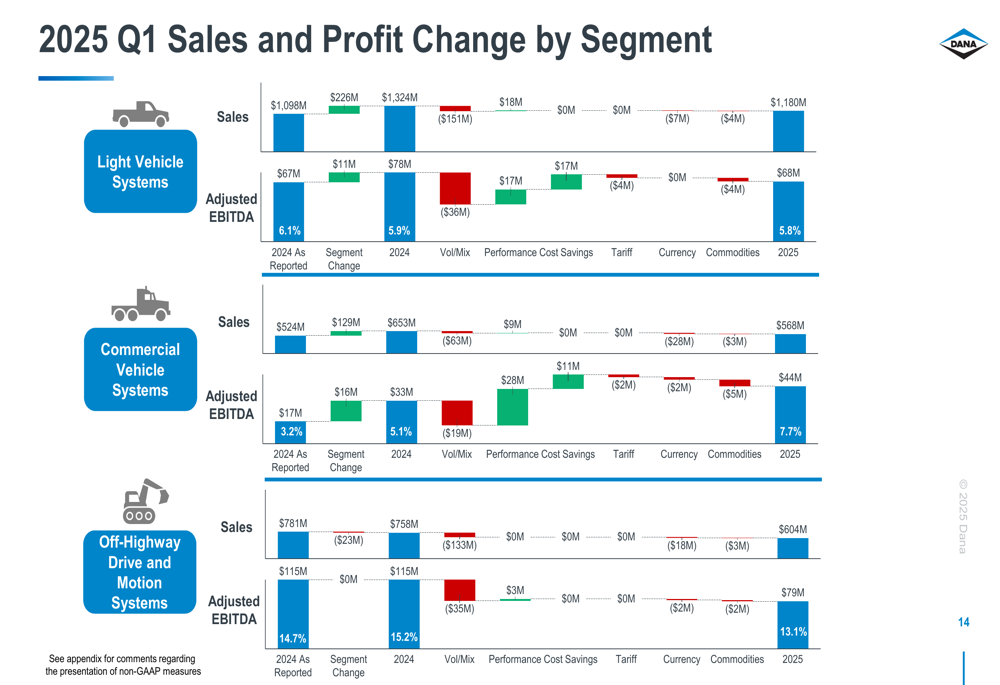

Dana’s performance varied across its business segments in Q1 2025. The Light Vehicle segment reported sales of $1,180 million, down from $1,324 million in Q1 2024, with adjusted EBITDA of $68 million compared to $78 million. The Commercial Vehicle segment showed improved profitability despite lower sales, with adjusted EBITDA increasing to $44 million from $33 million on sales of $568 million, down from $653 million. The Off-Highway segment experienced the most significant decline, with adjusted EBITDA falling to $79 million from $115 million on sales of $604 million, down from $758 million.

The segment breakdown shows how each business unit contributed to the overall results:

Strategic Initiatives

A key focus of Dana’s presentation was the acceleration of its cost-savings plan. The company announced it is increasing its 2025 cost-savings target from $175 million to $225 million as part of its broader $300 million cost-reduction initiative. In Q1 alone, cost savings contributed $41 million to adjusted EBITDA, helping to offset the $90 million negative impact from lower volumes and mix.

"Accelerating realization of $300 million cost-savings plan, increasing 2025 cost savings from $175 million to $225 million," the company stated in its presentation. The cost savings are distributed across SG&A (23%), COGS (41%), and Engineering (36%).

Dana also highlighted that its Off-Highway divestiture is underway with a "competitive process with multiple bidders," signaling progress in the company’s portfolio restructuring efforts. Additionally, the company identified non-core assets and investments that can be monetized, with expected pre-tax proceeds of approximately $50 million in Q2 2025.

On the innovation front, Dana announced it won its 10th Automotive News PACE Award for its Modular High-Performance Hybrid 8-Speed Dual-Clutch Transmission, developed in collaboration with Graziano and Lamborghini:

Cash Flow Management

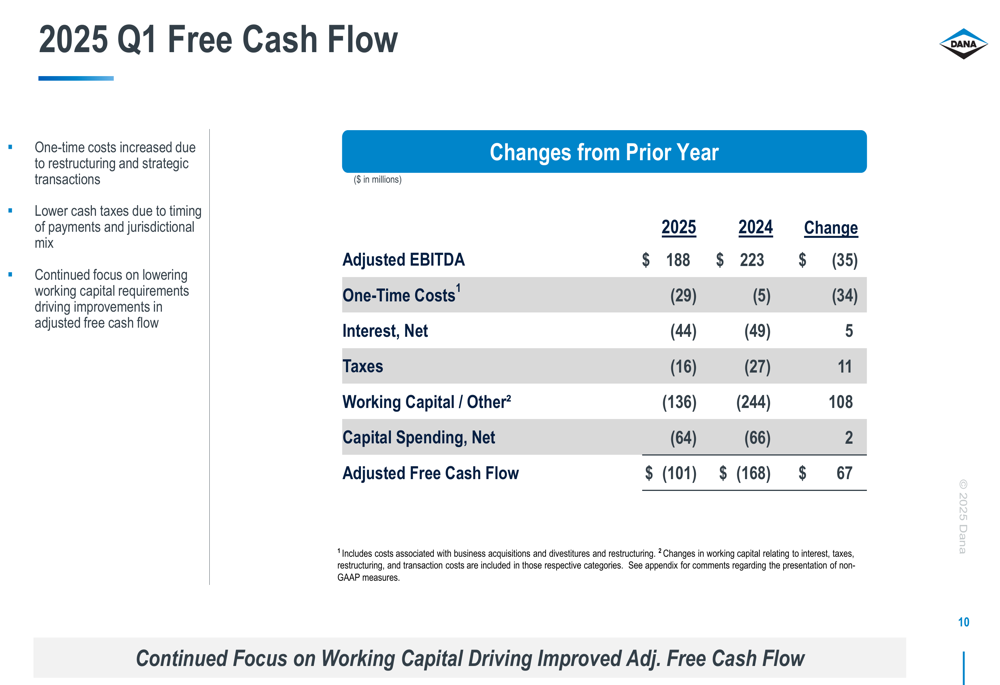

Dana placed significant emphasis on improving its cash flow performance, with the presentation highlighting a $67 million improvement in adjusted free cash flow in Q1 2025 compared to the prior year. The company attributed this improvement to better working capital management and continued focus on capital spending efficiency.

The following chart details the components of Dana’s Q1 free cash flow:

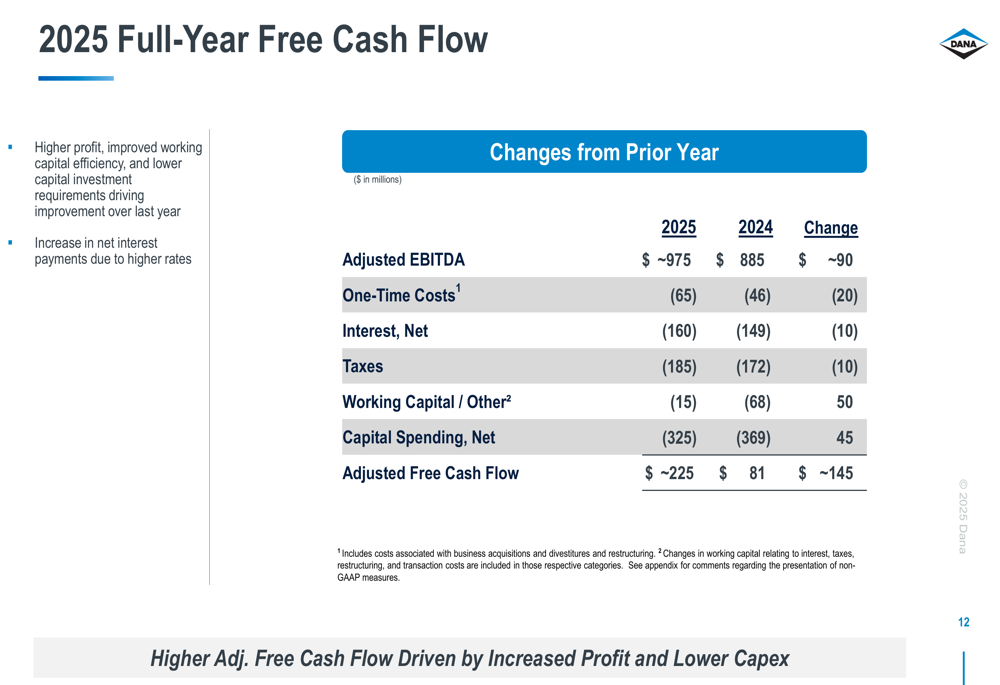

For the full year 2025, Dana is projecting adjusted free cash flow of approximately $225 million, a significant improvement from the $81 million reported in 2024. This improvement is expected to be driven by higher profit, improved working capital efficiency, and lower capital spending.

The full-year free cash flow projection is broken down as follows:

Market Challenges and Outlook

Dana acknowledged several market challenges in its presentation, including softening North American commercial vehicle demand, though this is partially offset by strength in South America and Europe. The company also noted that Off-Highway end markets are seeing some pre-buying in Q2, while light-truck production schedules remain stable in the near term but face potential demand risk later in the year due to tariff impacts on pricing.

Regarding tariffs, Dana described the situation as "manageable" with mitigation actions being completed, including steel and aluminum index movements in recovery mechanisms and customer recovery claims submitted.

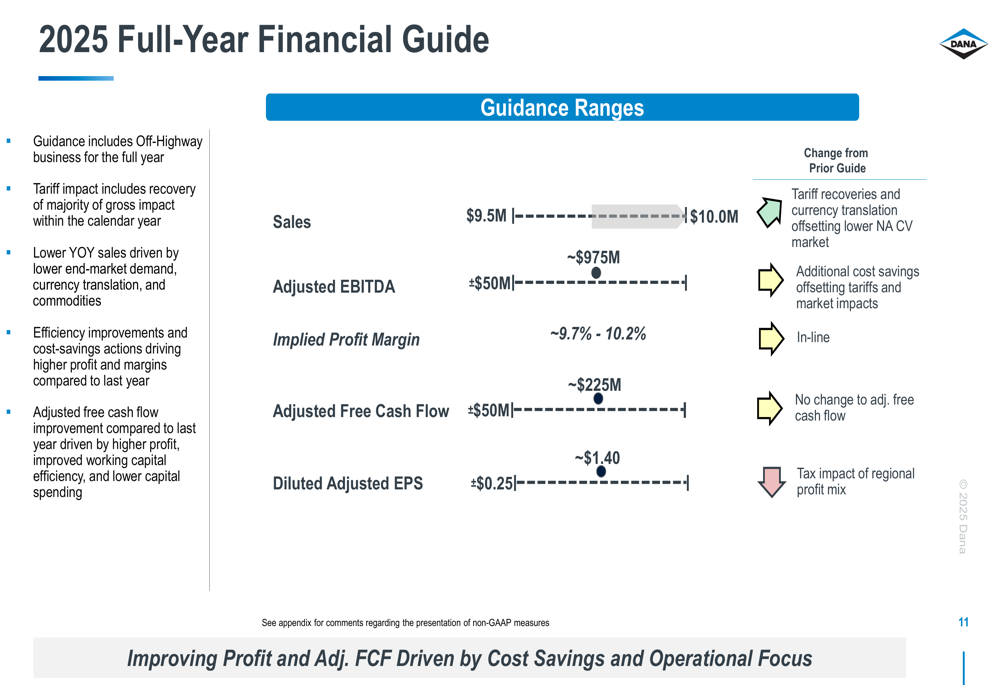

Despite these challenges, Dana maintained its full-year 2025 guidance:

The company projects sales of $9.5 billion to $10.0 billion, adjusted EBITDA of approximately $975 million (up $50 million from previous guidance), and adjusted free cash flow of approximately $225 million. The implied profit margin is expected to range from 9.7% to 10.2%, showing improvement from current levels.

Forward-Looking Statements

Looking ahead, Dana emphasized that its guidance includes the Off-Highway business for the full year, suggesting the divestiture may not be completed until late 2025 or beyond. The company expects lower year-over-year sales driven by reduced end-market demand, currency translation, and commodity factors.

However, Dana remains confident that efficiency improvements and cost-savings actions will drive higher profit and margins compared to last year. The company stated it has "the right footprint and flexible cost structure to manage through uncertainty and maintain our full-year adj EBITDA guidance."

This outlook represents a strategic shift from what was reported in Dana’s Q3 2024 earnings, where the company had adjusted its full-year sales guidance to approximately $10.3 billion. The current guidance of $9.5-10.0 billion for 2025 reflects continued market challenges but also Dana’s confidence in its ability to maintain profitability through operational efficiency and cost management.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.