Williams Wesley Hastie sells $328k in Cipher Mining shares

Introduction & Market Context

Danske Bank (CPH:DANSKE) released its third-quarter 2025 earnings presentation on October 31, revealing strong financial performance that triggered a remarkable 30.56% surge in its stock price. The Nordic banking giant reported a net profit of DKK 16.7 billion for the first nine months of 2025, demonstrating resilient performance across all business segments despite lower central bank rates affecting deposit margins.

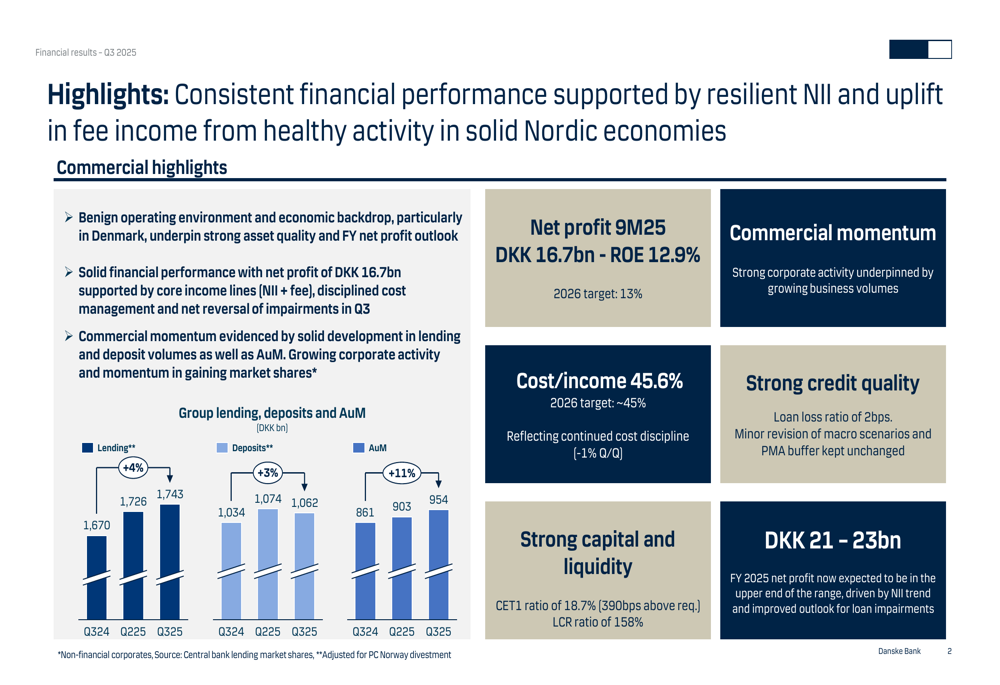

The bank’s presentation highlighted consistent financial performance supported by resilient Net Interest Income (NII) and an uplift in fee income, attributed to healthy activity levels in the solid Nordic economies. This performance comes amid what the bank described as a "benign operating environment" that has helped maintain strong credit quality.

As shown in the following comprehensive overview of key financial metrics:

Quarterly Performance Highlights

Danske Bank reported a return on equity of 12.9% for the first nine months of 2025, approaching its 2026 target of 13%. The bank’s cost/income ratio stood at 45.6%, also nearing its 2026 target of approximately 45%. These efficiency improvements reflect the bank’s continued focus on cost management and operational optimization.

The presentation revealed strong commercial momentum with solid development in lending and deposit volumes. Lending increased 4% year-over-year to DKK 1,743 billion in Q3 2025, while deposits grew 3% to DKK 1,074 billion. Assets under management showed particularly strong growth, rising 11% year-over-year to DKK 954 billion.

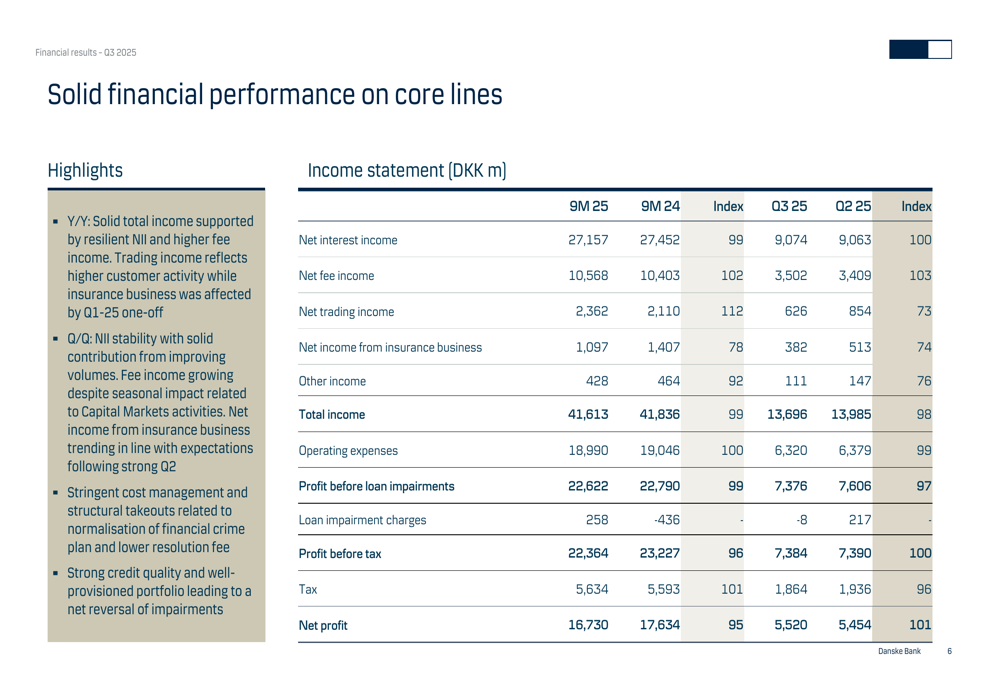

The bank’s income statement shows stable performance across key revenue streams, with net interest income of DKK 9,074 million for Q3 2025, slightly higher than the DKK 9,063 million in Q2. Fee income showed improvement, increasing to DKK 3,502 million in Q3 from DKK 3,409 million in the previous quarter.

The detailed income statement reveals the bank’s financial stability and growth:

Segment Performance Analysis

Danske Bank’s presentation provided a detailed breakdown of performance across its three main business segments, all showing resilience despite challenging market conditions.

The Personal Customers segment demonstrated stable financial performance as deposit growth and customer activity mitigated the impact of lower central bank rates. The segment achieved a return on allocated capital (ROAC) of 33% in Q3 2025, exceeding its 2026 target of approximately 29%. The cost/income ratio improved to 51%, moving closer to the 2026 target of below 50%.

As illustrated in the Personal Customers performance overview:

The Business Customers segment showed increased commercial momentum, supported by an expanding customer base and strong growth in lending volumes. Lending increased 4% year-over-year to DKK 692 billion, while the segment maintained a solid ROAC of 20% and a cost/income ratio of 38%, well below its 2026 target of less than 40%.

The Business Customers segment’s key performance metrics are displayed here:

The Large Corporates & Institutions segment delivered particularly strong results, with total income up 8% year-over-year driven by NII and sustained lending growth of 12%. The segment achieved an impressive ROAC of 25%, significantly exceeding its 2026 target of approximately 18%. The cost/income ratio of 43% remained well below the target of less than 50%.

The following chart illustrates the strong performance of the Large Corporates & Institutions segment:

Financial Details and Balance Sheet Strength

Danske Bank’s presentation emphasized the bank’s strong credit quality, with a loan loss ratio of just 2 basis points. The bank reported a net reversal of impairments of DKK 8 million in Q3 2025, reflecting the strong underlying credit quality of its loan portfolio.

The bank’s asset quality metrics demonstrate its prudent risk management approach:

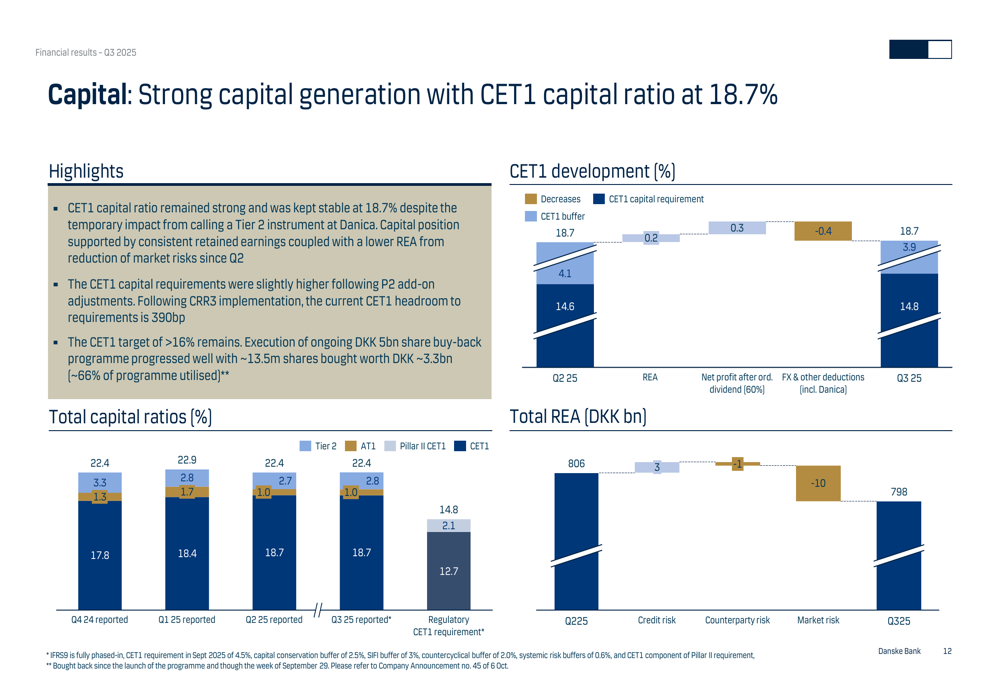

Capital generation remained strong, with the Common Equity Tier 1 (CET1) ratio at 18.7%, which is 390 basis points above regulatory requirements. This robust capital position provides the bank with significant flexibility for potential growth opportunities and shareholder returns.

The bank’s capital position is illustrated in the following chart:

Net interest income remained resilient despite the challenging interest rate environment, underpinned by volume growth and the bank’s structural hedge, which helped mitigate the impact of policy rate cuts on deposit margins. The bank’s fee income showed positive development, driven by solid customer activity across segments.

The following chart demonstrates how NII has been supported by volumes and structural hedge:

Forward-Looking Statements

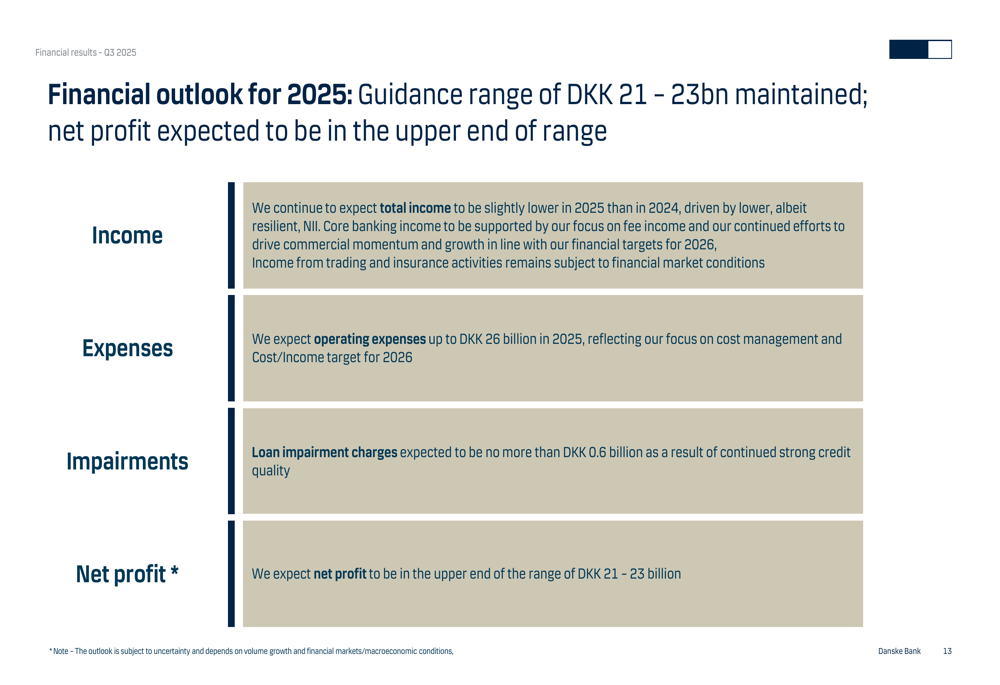

Danske Bank maintained its full-year 2025 guidance, with net profit expected to be in the upper end of the DKK 21-23 billion range. This outlook reflects the bank’s confidence in its business model and strategic direction despite ongoing macroeconomic uncertainties.

The bank expects total income to be slightly lower in 2025 compared to the previous year, with operating expenses projected to be up to DKK 26 billion. Loan impairment charges are expected to be no more than DKK 0.6 billion, down from the previous guidance of DKK 1 billion, indicating improved expectations for credit quality.

The financial outlook for 2025 is summarized in this overview:

CEO Carsten Egeriis and CFO Cecile Hillary emphasized the bank’s strong position in the Nordic banking market and its continued focus on operational efficiency and customer-centric solutions. The 30.56% stock surge following the earnings release suggests that investors share the management’s confidence in the bank’s strategic direction and financial outlook.

Danske Bank’s Q3 2025 presentation demonstrates that the bank is well-positioned to navigate the current economic environment while continuing to deliver solid returns to shareholders. With strong capital ratios, improving operational efficiency, and growing business volumes, the bank appears on track to meet or exceed its 2026 financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.