Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Dave Inc (NASDAQ:DAVE) presented its second quarter 2025 earnings results on August 6, 2025, showcasing substantial growth across all key metrics and raising its full-year guidance. The fintech company, which positions itself as a lower-cost banking alternative for financially struggling Americans, reported continued momentum following its strong Q1 performance.

The company’s stock, which had already surged 28.63% following its Q1 earnings announcement, was trading at $235.01 in premarket trading, down 1.6% from its previous close of $238.83. Despite this slight pullback, Dave shares have shown remarkable strength, trading significantly above their 52-week low of $30.17.

Quarterly Performance Highlights

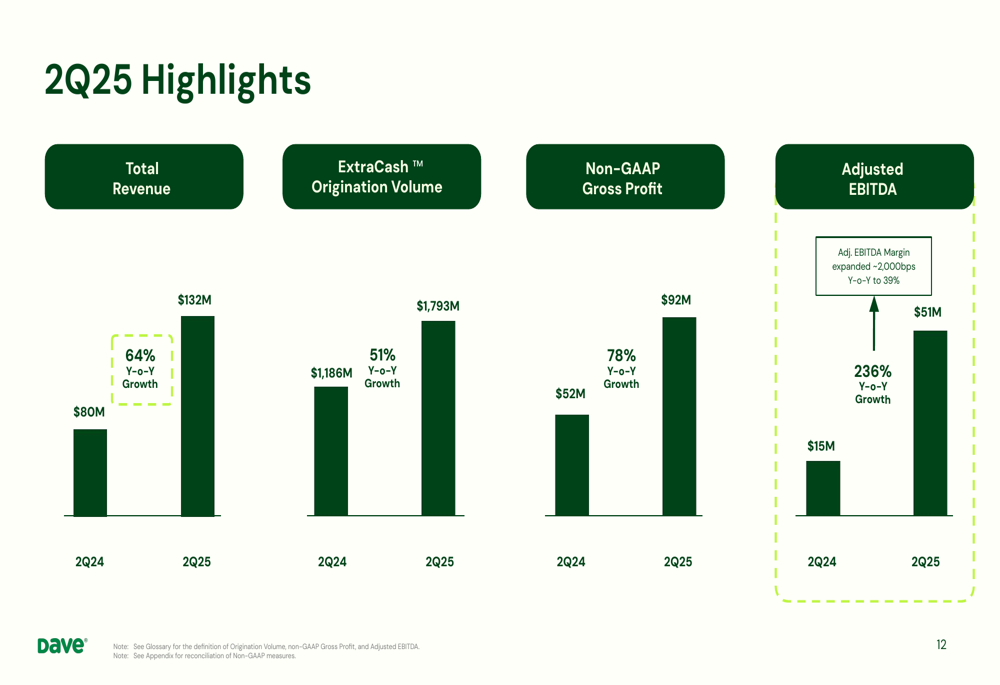

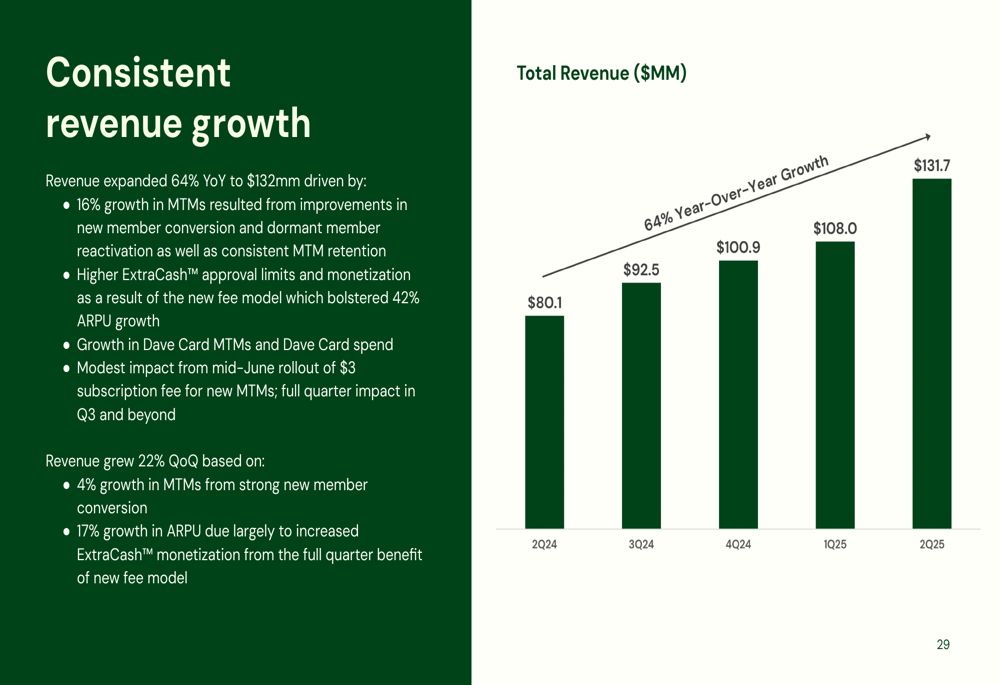

Dave reported exceptional financial results for Q2 2025, with total revenue reaching $132 million, representing a 64% year-over-year increase. This growth was driven by a 16% increase in Monthly Transacting Members (MTMs), higher ExtraCash approval limits, growth in Dave Card MTMs, and a modest impact from the mid-June rollout of a $3 subscription fee for new MTMs.

As shown in the following chart of quarterly financial highlights:

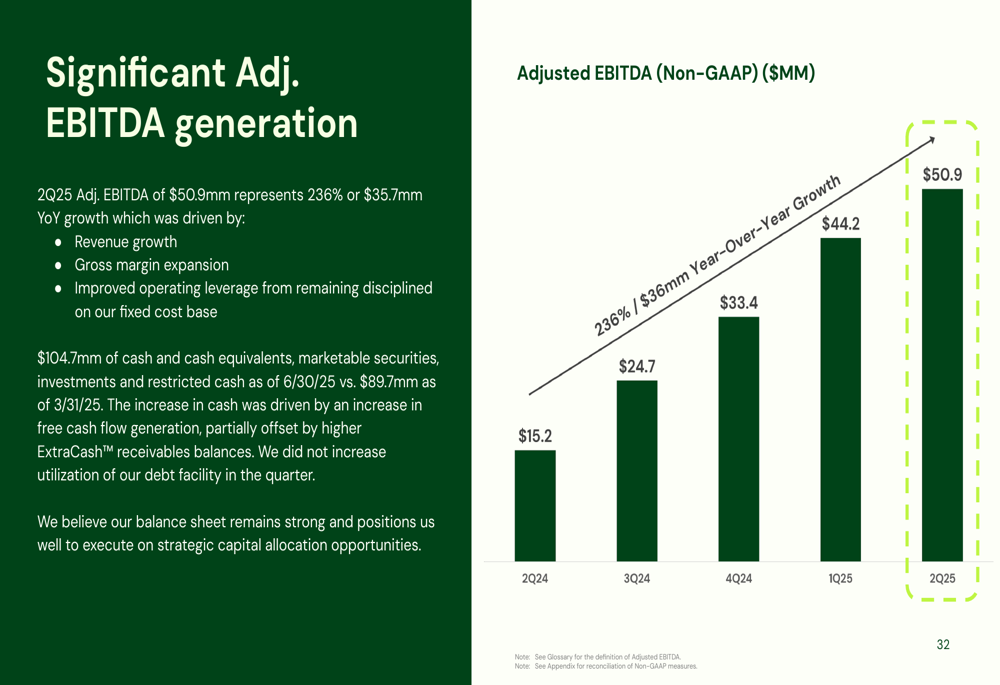

The company’s profitability metrics showed even stronger improvement, with non-GAAP gross profit increasing 78% year-over-year to $92 million. Most impressively, adjusted EBITDA surged 236% to $51 million, with an adjusted EBITDA margin of 39%.

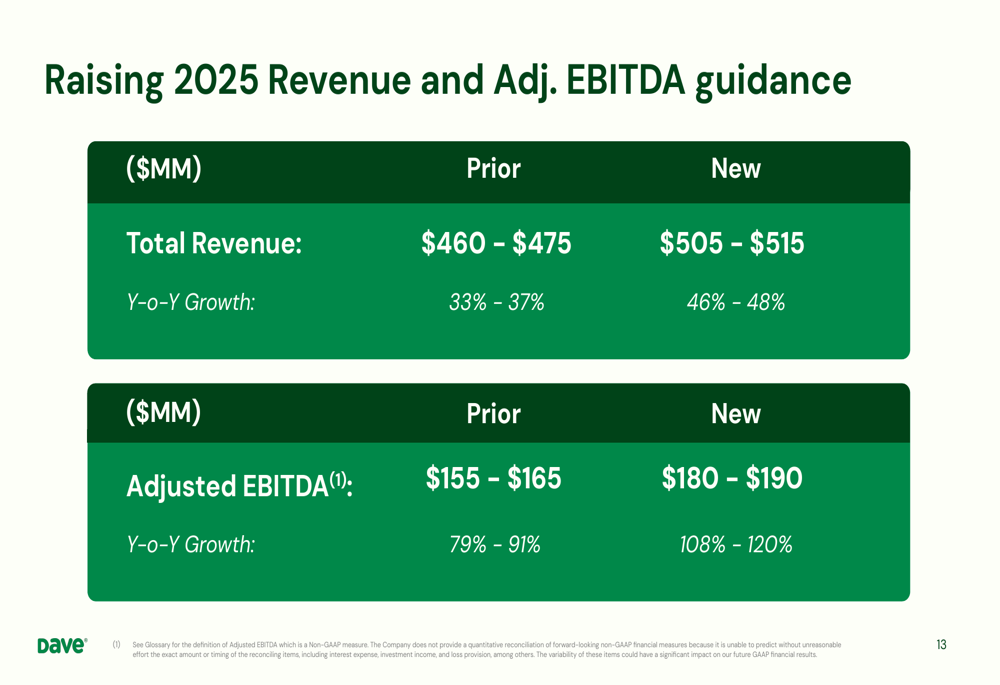

Based on these strong results, Dave has significantly raised its full-year 2025 guidance:

The company now expects total revenue between $505-$515 million (up from previous guidance of $460-$475 million), representing 46-48% year-over-year growth. Adjusted EBITDA guidance was raised to $180-$190 million (from $155-$165 million), representing 108-120% year-over-year growth.

Market Opportunity (SO:FTCE11B)

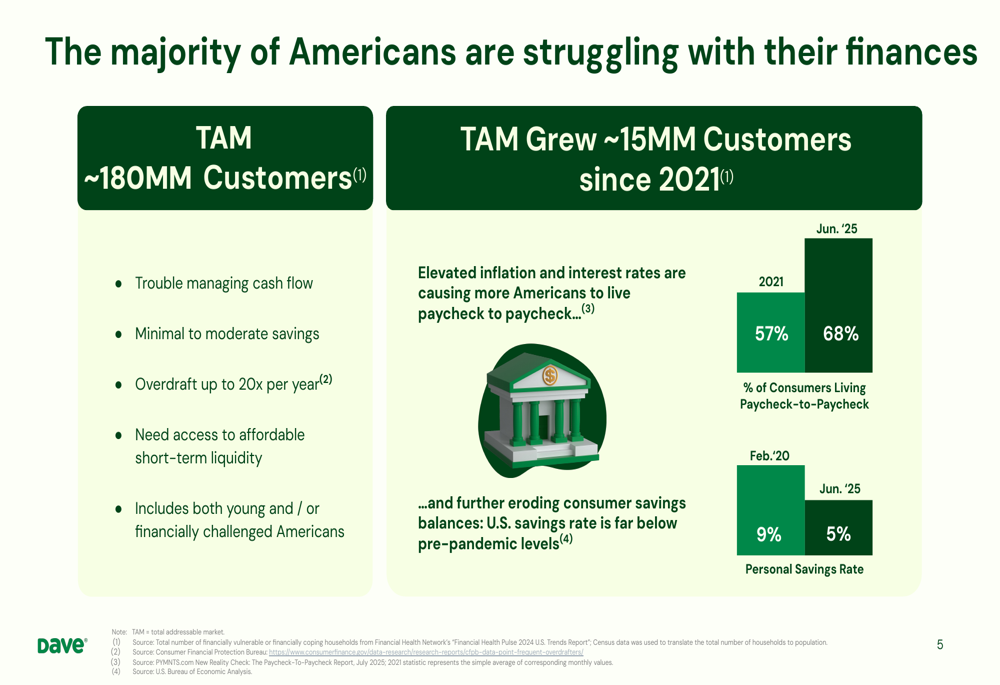

Dave’s presentation highlighted the growing market opportunity as more Americans struggle with their finances. According to the company, 68% of consumers were living paycheck-to-paycheck in June 2025, up from 57% in 2021 and 9% in February 2020. The personal savings rate has also declined from 9% in February 2020 to 5% in June 2025.

The company estimates its total addressable market at approximately 180 million customers, which has grown by about 15 million since 2021. Dave attributes this expansion to elevated inflation and interest rates causing more Americans to live paycheck-to-paycheck and eroding consumer savings balances.

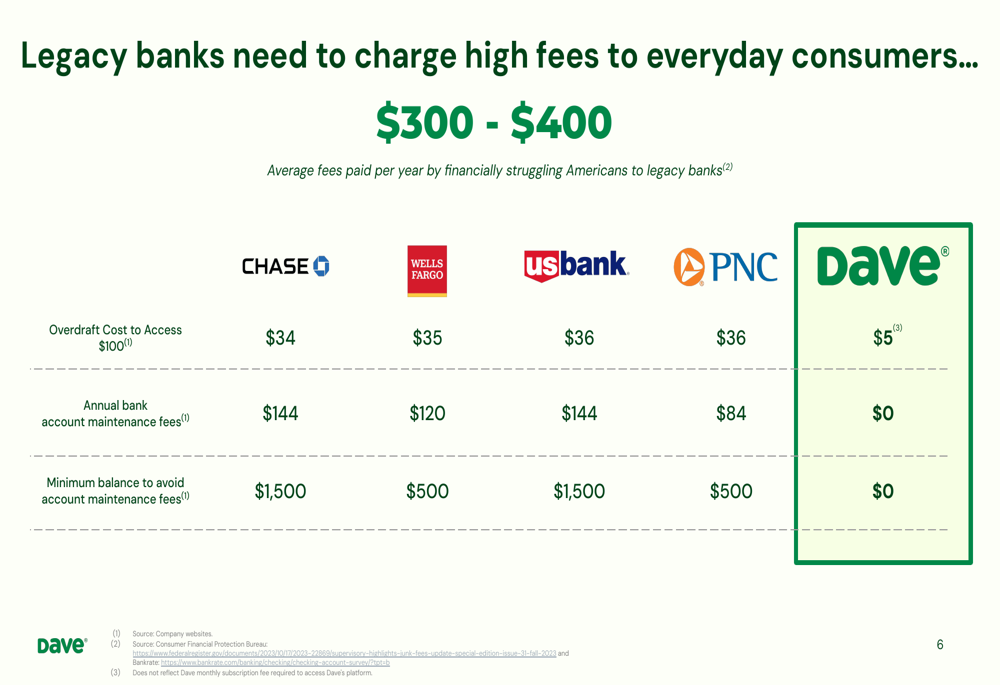

A key competitive advantage for Dave is its significantly lower fee structure compared to traditional banks:

While legacy banks charge $34-$36 for overdraft access to $100, Dave charges just $5. Similarly, Dave has no annual maintenance fees (compared to $84-$144 at legacy banks) and no minimum balance requirements (versus $500-$1,500 at traditional banks).

The company also highlighted its operational efficiency advantages, with a cost to serve of $48 (84% lower than legacy banks’ $300) and customer acquisition cost of $17 (97% lower than legacy banks’ $500).

Detailed Financial Analysis

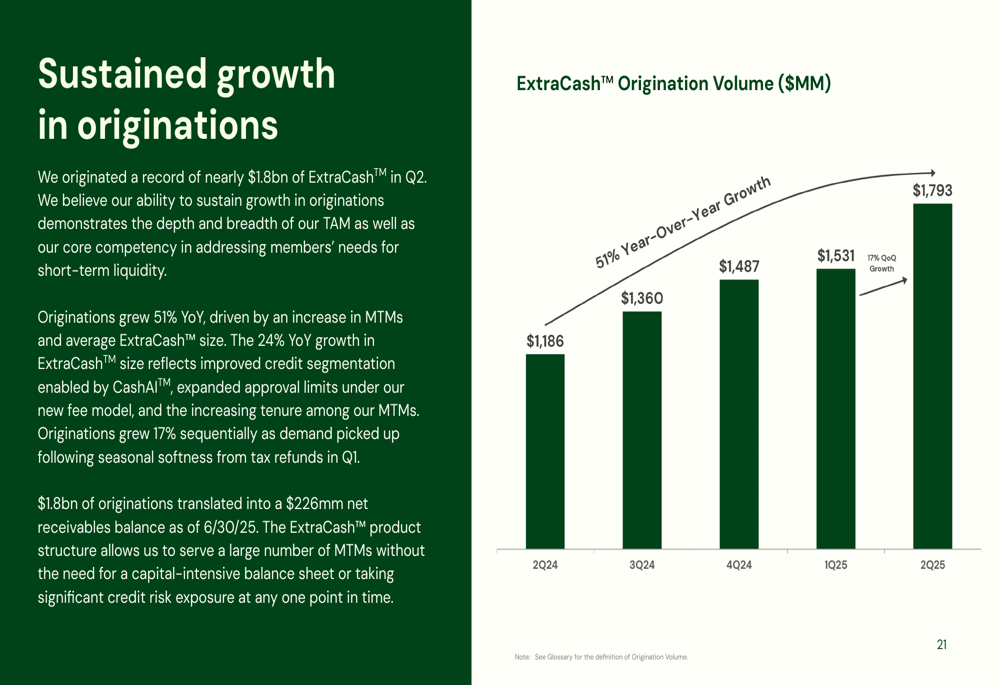

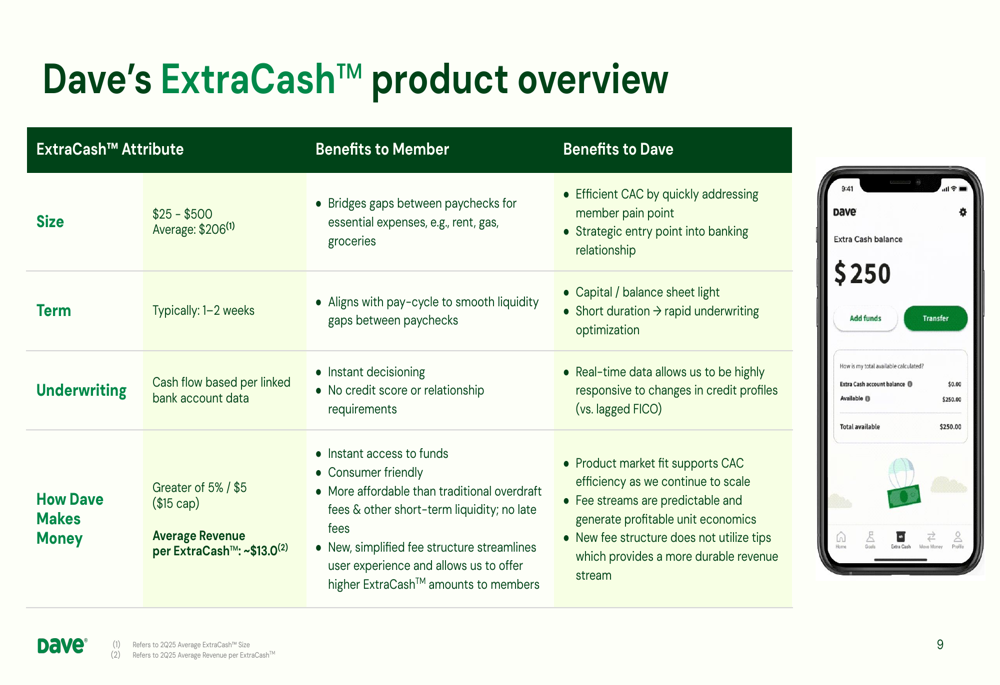

Dave’s ExtraCash product, which provides short-term liquidity to customers, continues to show strong growth. The origination volume reached $1.79 billion in Q2 2025, a 51% year-over-year increase:

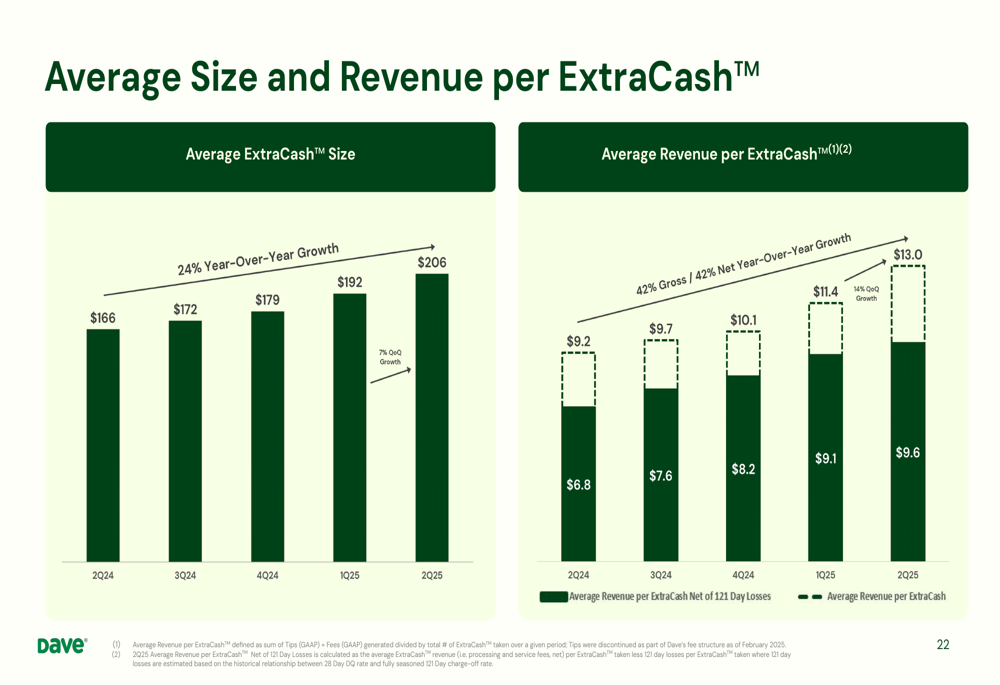

Both the average size of ExtraCash advances and the revenue per advance have increased significantly:

The average ExtraCash size grew 24% year-over-year to $206, while average revenue per ExtraCash increased 42% to $13.0. These metrics indicate that customers are utilizing larger advances and generating more revenue for the company.

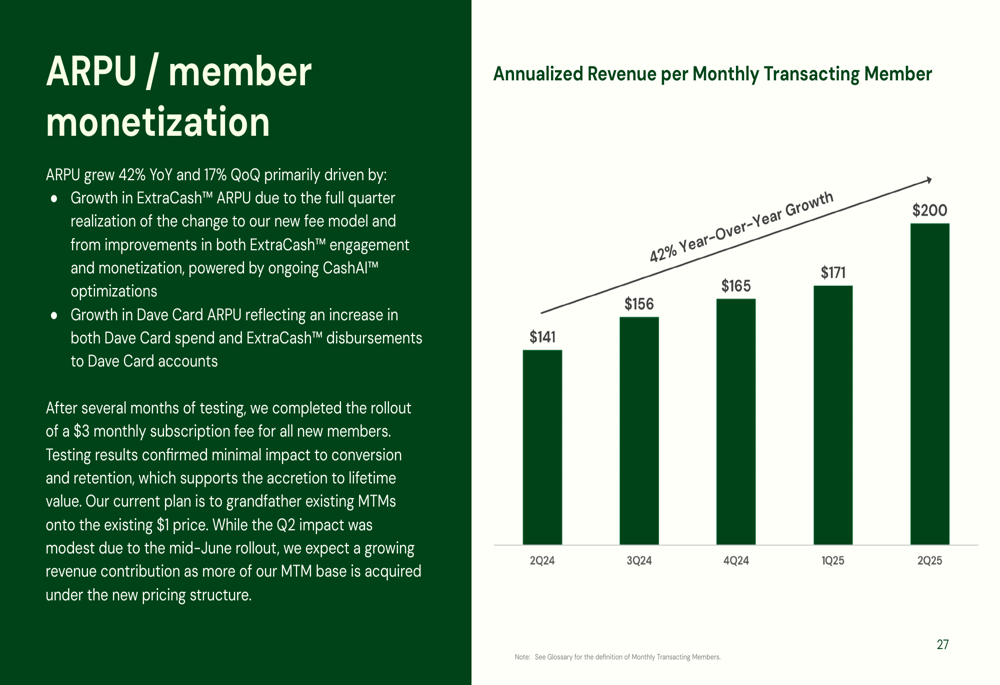

Dave’s efficiency in monetizing its user base is also improving, with annualized revenue per monthly transacting member reaching $200, a 42% year-over-year increase:

The company’s revenue growth has been consistently strong over the past several quarters:

Meanwhile, Dave has significantly improved its operational efficiency, with fixed expenses as a percentage of total revenue declining from 32% to 21%, representing an 1,100 basis point year-over-year improvement. This operational leverage has contributed to the dramatic improvement in adjusted EBITDA:

Strategic Initiatives

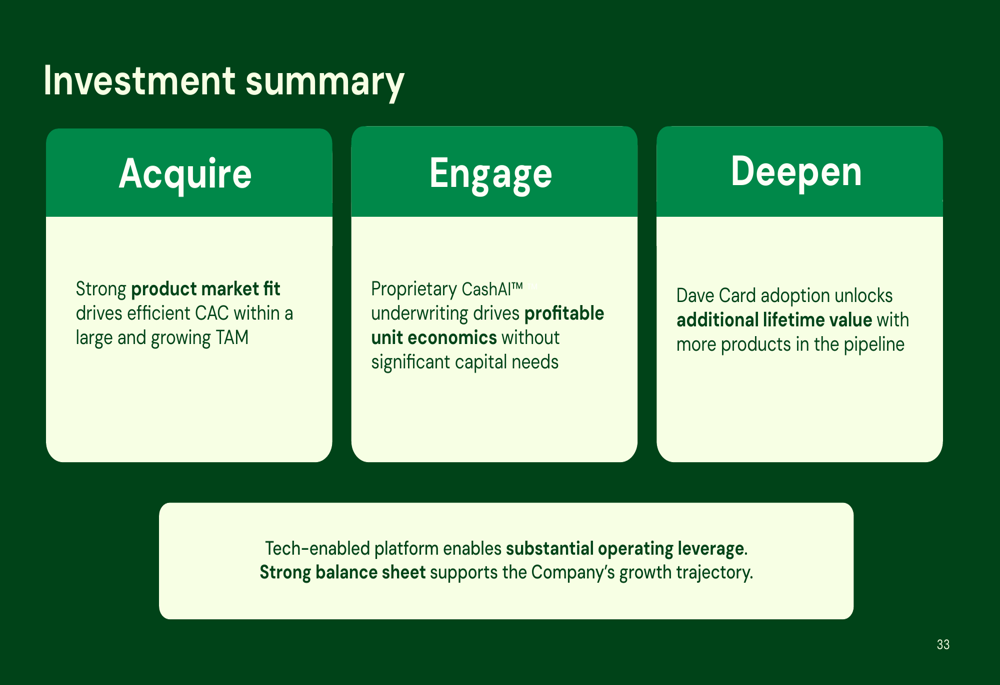

Dave’s business strategy follows a three-stage approach: Acquire, Engage, and Deepen. In the Acquire stage, the company efficiently markets to address liquidity pain points with attractive LTV/CAC ratios. The Engage phase centers around ExtraCash, providing short-term liquidity enabled by CashAI, the company’s AI-driven underwriting system. The Deepen stage focuses on the Dave Card, a full-service banking solution with no mandatory fees.

The ExtraCash product serves as both a revenue generator and a pathway to deeper customer relationships:

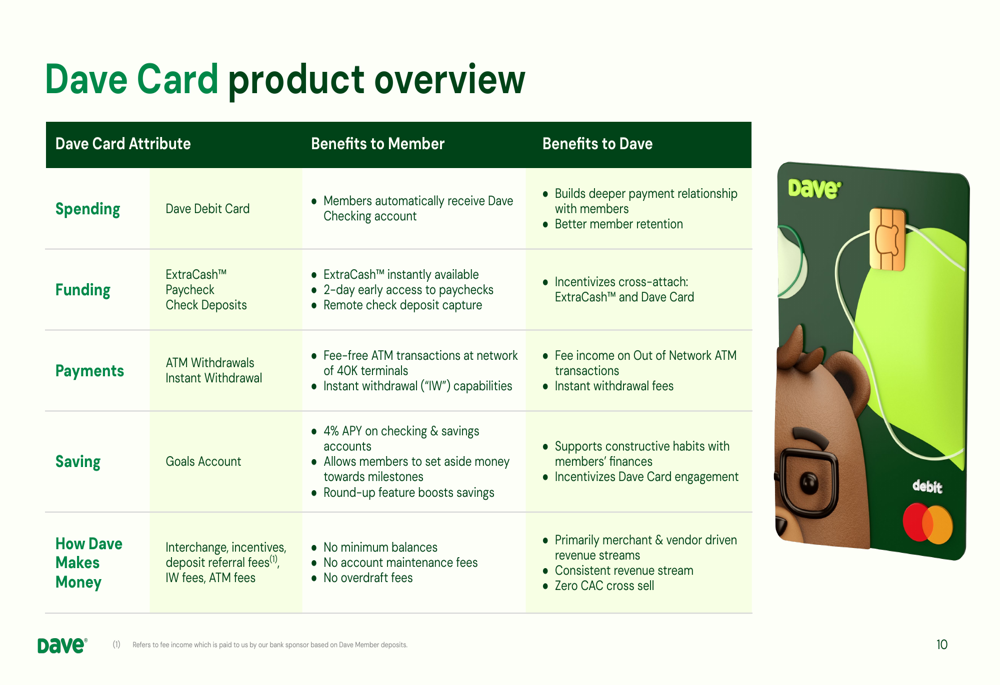

The Dave Card further enhances customer relationships by providing a full banking solution:

This strategy appears to be working effectively, as Dave Card spend volumes have increased 27% year-over-year to $493 million in Q2 2025. The company has also improved its customer acquisition efficiency, with CAC at $19 in Q2 2025 and the payback period improving from 5 months to 4 months.

Forward-Looking Statements

Beyond the raised guidance for 2025, Dave’s presentation highlighted several strengths that position the company for continued growth:

The company emphasized its strong product-market fit within a large and growing total addressable market, proprietary CashAI underwriting technology that drives profitable unit economics without significant capital needs, and increasing Dave Card adoption that unlocks additional lifetime value.

While Dave faces risks including potential market saturation, economic uncertainties affecting consumer spending, and operational challenges as it continues to scale, the company’s strong Q2 results and raised guidance suggest management is confident in its ability to navigate these challenges and continue its growth trajectory.

As Dave continues to execute on its strategy of providing affordable financial services to financially struggling Americans, its Q2 2025 presentation demonstrates that the company is successfully growing its user base, increasing engagement, and improving profitability metrics across the board.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.