US LNG exports surge but will buyers in China turn up?

Introduction & Market Context

Donnelley Financial Solutions (NYSE:DFIN), a leading provider of regulatory compliance solutions, presented its Q1 2025 investor slides highlighting continued progress in its strategic transformation toward higher-margin software solutions. The company’s presentation, dated April 2025, showcases DFIN’s evolution from a print-heavy business to a software-focused enterprise serving corporations and investment companies with regulatory filing and compliance needs.

DFIN maintains leadership positions across its key markets, ranking as the #1 SEC filing agent for both corporations and fund companies, while also holding the top position in content management software with its ArcSuite product. The company serves over 200 Fortune 500 clients and approximately 80% of the top 50 global fund complexes.

As shown in the following overview of DFIN’s market position and offerings:

Quarterly Performance Highlights

DFIN reported Q1 2025 net sales of $201.1 million, with software solutions contributing $84.6 million, representing growth of 5.4% year-over-year or 5.8% on an organic basis. The company’s adjusted EBITDA reached $68.2 million, increasing by $13.0 million or 23.6% compared to Q1 2024, while the adjusted EBITDA margin expanded to 33.9%, up 680 basis points from the prior year.

The growth in software solutions was primarily driven by strong performance in Arc Suite and ActiveDisclosure. Arc Suite sales reached $32.7 million, growing approximately 20% year-over-year, while ActiveDisclosure sales increased by approximately 11%, fueled by continued adoption of service package offerings and subscription revenue growth.

During the quarter, DFIN repurchased approximately 861,000 shares of common stock for $41.8 million at an average price of $48.57 per share. The company also amended and extended its credit agreement, providing for a $115 million Term Loan A and extending the maturity of its $300 million revolving credit facility to March 13, 2030.

Strategic Initiatives

DFIN’s strategic transformation is centered on shifting its revenue mix toward higher-margin software solutions while reducing reliance on traditional print and distribution services. This shift is evident in the company’s evolving revenue composition, with software solutions growing from just 14% of total revenue in 2016 to 43% in Q1 2025 TTM.

As illustrated in the following chart showing DFIN’s revenue mix evolution and profitability improvement:

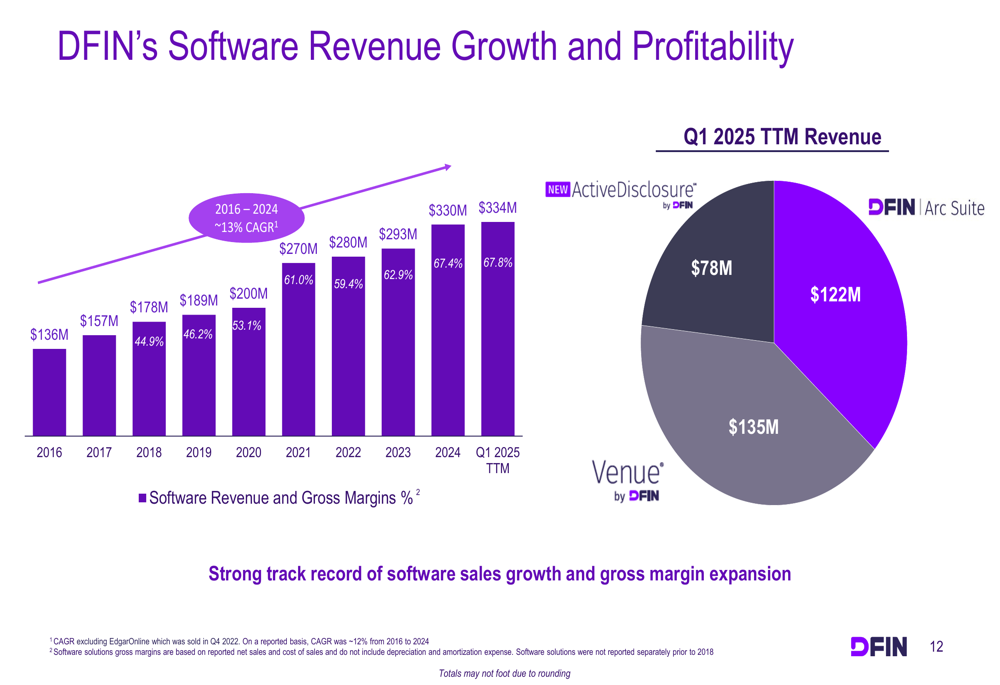

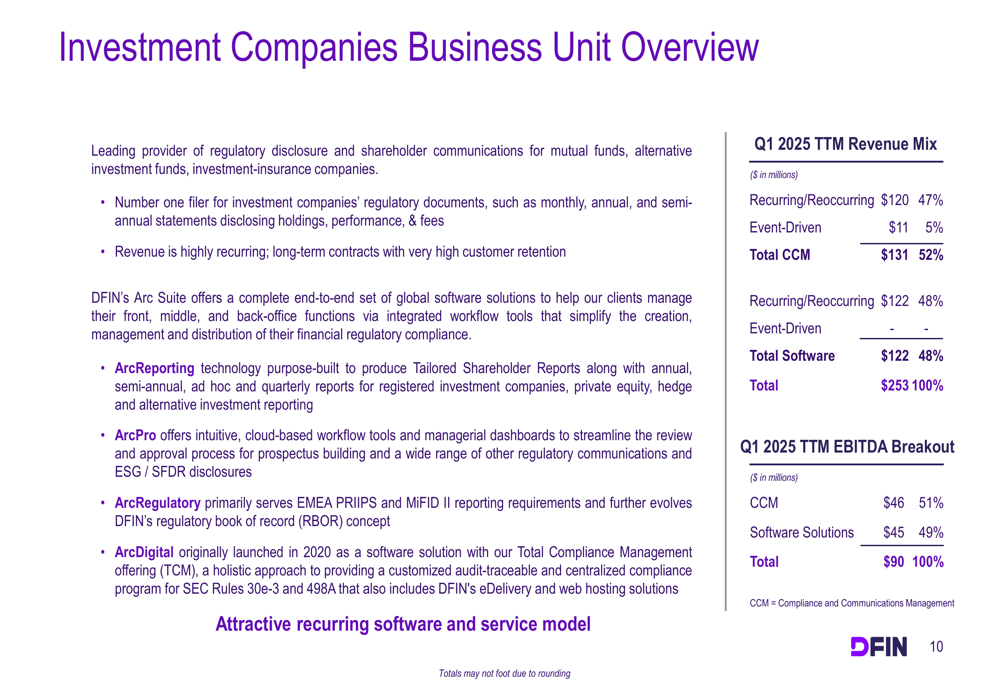

The company’s software portfolio includes key products such as Venue (virtual data room), ActiveDisclosure (disclosure management), and Arc Suite (content management). These solutions have demonstrated consistent growth, with a combined CAGR of approximately 13% from 2016 to 2024.

The following chart details the growth trajectory of DFIN’s software solutions and their improving gross margins:

Detailed Financial Analysis

DFIN’s financial performance reflects the benefits of its strategic transformation. For the trailing twelve months ending Q1 2025, the company reported:

- Total (EPA:TTEF) revenue of $779.6 million

- Adjusted EBITDA of $230.3 million (29.5% margin)

- Free cash flow of $94.4 million

- Net debt of $67.4 million, representing a leverage ratio of 0.8x

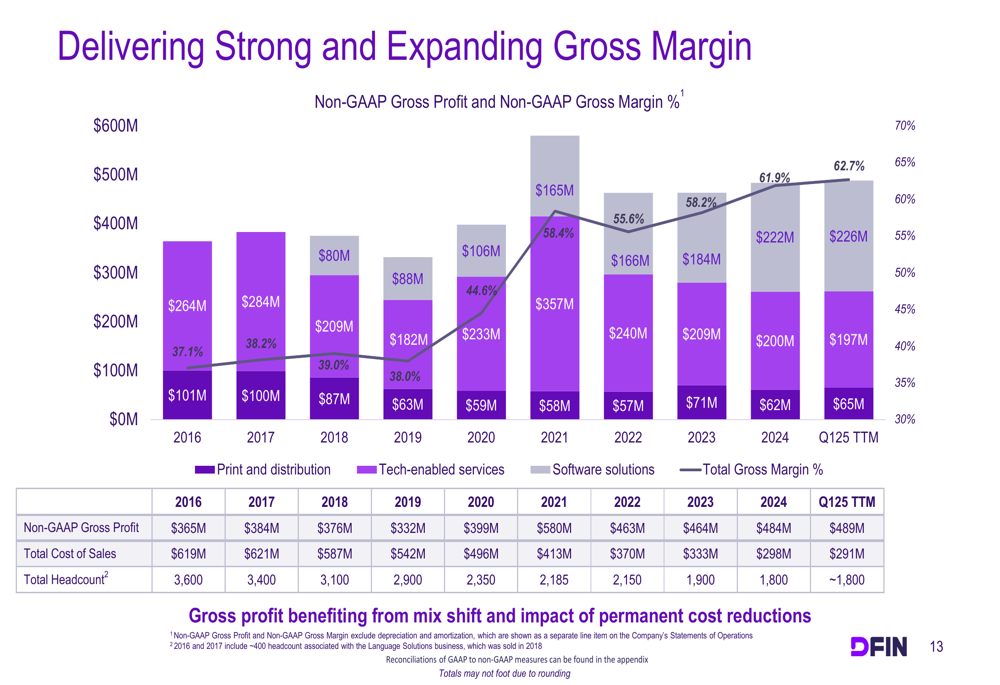

The company’s revenue is increasingly recurring or reoccurring in nature, with 43% coming from software solutions, 40% from tech-enabled services, and only 17% from print and distribution. This shift toward higher-margin, more predictable revenue streams has contributed to substantial margin expansion.

As shown in the following chart detailing DFIN’s gross margin improvement:

The company has achieved this margin expansion while significantly reducing its cost base. DFIN has decreased its headcount from approximately 3,600 to around 1,800, outsourced traditional print to a vendor network, and implemented a more efficient variable cost structure.

Capital Allocation Strategy

DFIN has maintained a disciplined approach to capital allocation, focusing on debt reduction, share repurchases, and strategic investments. Since 2016, the company has reduced its net leverage from 3.4x to 0.8x as of March 31, 2025.

The company has also been active in returning capital to shareholders through share repurchases. From 2020 to 2024, DFIN repurchased 8.3 million shares for $276.4 million at an average price of $33.42 per share. The company currently has a $150 million share repurchase program in place, expiring December 31, 2025.

As illustrated in the following overview of DFIN’s shareholder-friendly activities:

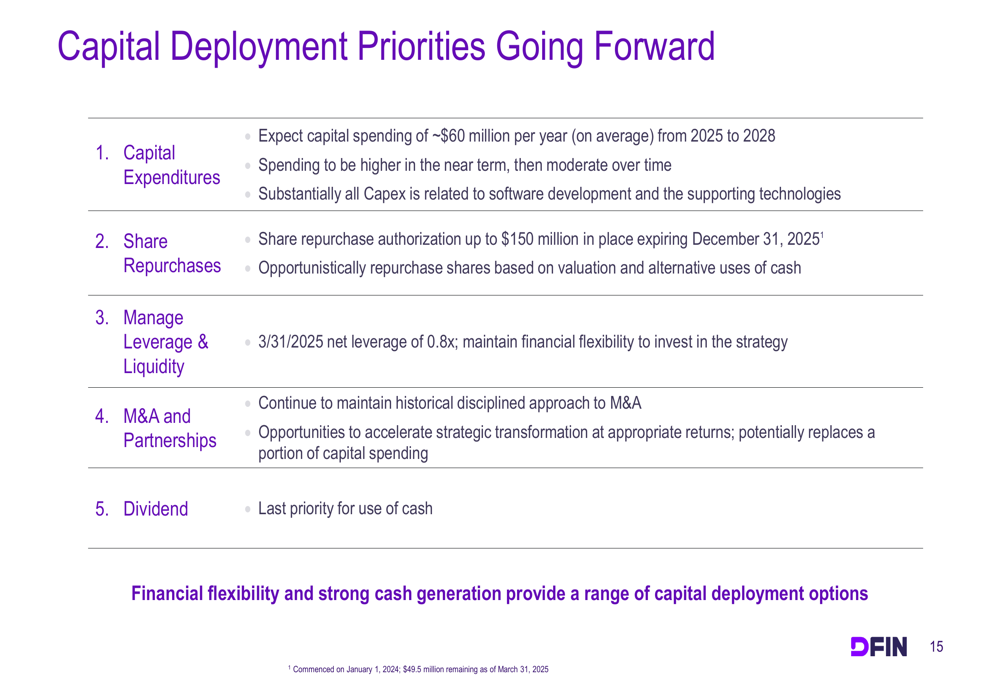

Looking ahead, DFIN’s capital deployment priorities include:

1. Capital expenditures of approximately $60 million per year from 2025 to 2028, primarily related to software development

2. Opportunistic share repurchases under the existing $150 million authorization

3. Maintaining financial flexibility with a target leverage ratio of 0.8x

4. Disciplined approach to M&A and partnerships to accelerate strategic transformation

5. Dividends as the lowest priority for cash use

Forward-Looking Statements

DFIN’s long-term financial projections reflect management’s confidence in the company’s strategic direction. The company expects:

- Low-single-digit total sales growth, improving from the historical CAGR of -2.2%

- Mid-teens growth in software solutions sales, building on the historical CAGR of 13.1%

- Mid-single-digit growth in recurring/reoccurring sales, reversing the historical CAGR of -0.6%

- EBITDA margin expansion to 30%+ from the current 28%

- Free cash flow conversion of approximately 45%

The following chart summarizes DFIN’s long-term financial projections:

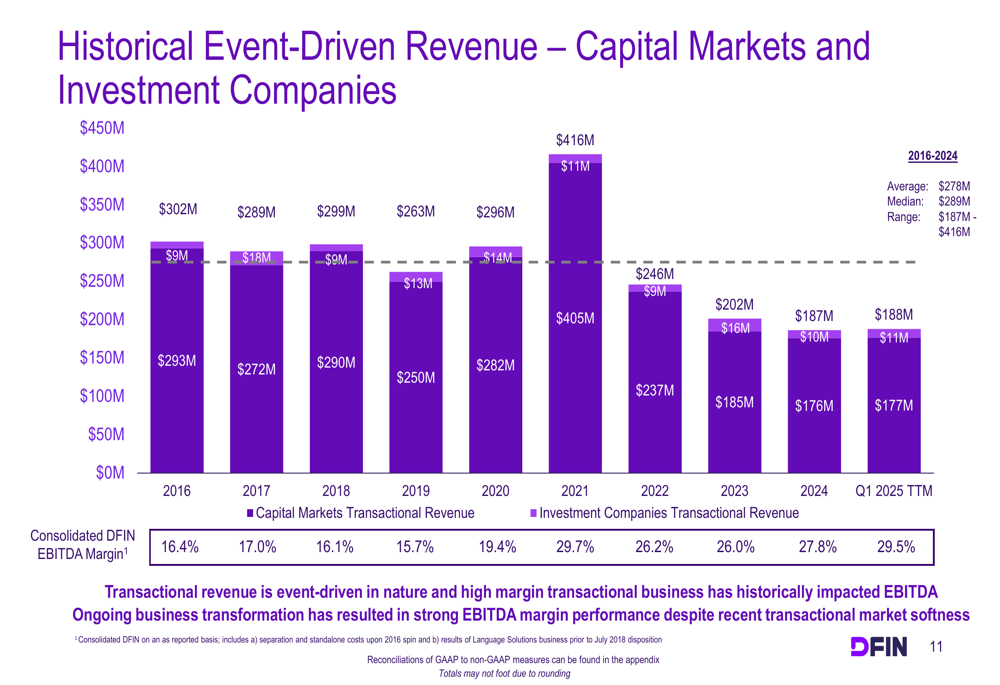

The company’s event-driven revenue, which is tied to capital markets transactions such as IPOs and M&A, has historically been volatile but remains an important contributor to overall profitability. Despite recent softness in transactional markets, DFIN has maintained strong EBITDA margins through its business transformation efforts.

As shown in the following chart of historical event-driven revenue:

Competitive Industry Position

DFIN operates in a competitive landscape with specialized players across its various business segments. The company evaluates its valuation using a sum-of-the-parts framework, comparing different business units to relevant competitors:

- Venue (virtual data room): Compared to Intralinks (SS&C) and Datasite

- ActiveDisclosure: Compared to Workiva (NYSE:WK)

- Arc Suite: Compared to Confluence and FilePoint

- Compliance and transaction services: Compared to Toppan Merrill and Broadridge

DFIN’s current enterprise value of $1.5 billion represents approximately 6.5x Q1 2025 TTM EBITDA, which management views as attractive relative to peers and the company’s growth profile.

Executive Summary

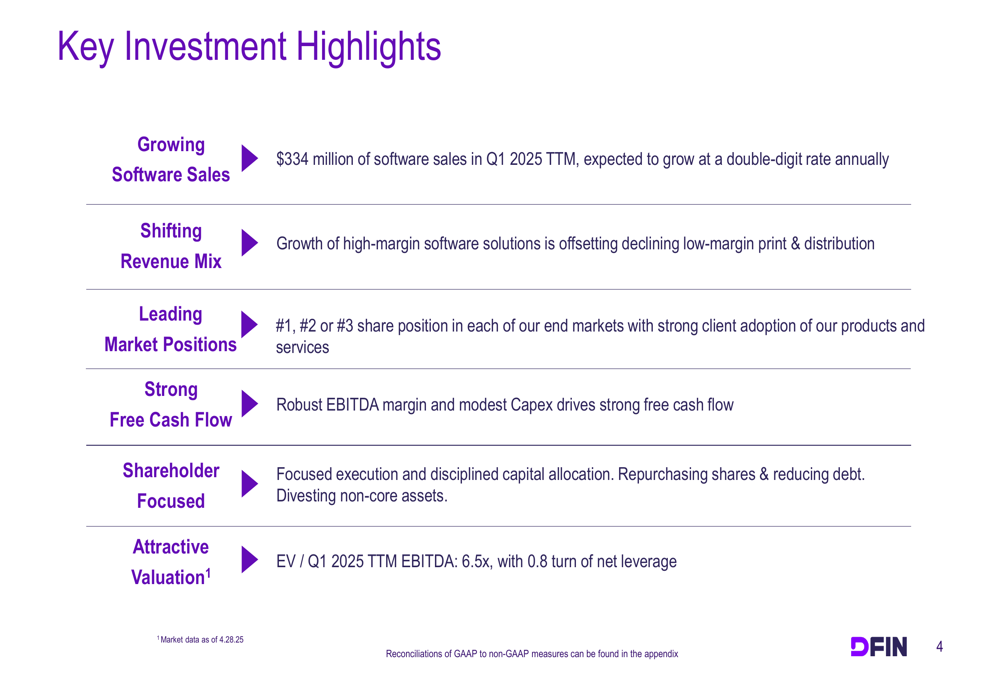

Donnelley Financial Solutions continues to execute on its strategic transformation toward higher-margin software solutions, as evidenced by its Q1 2025 results and investor presentation. The company’s focus on growing its software portfolio while optimizing its traditional business has resulted in significant margin expansion, strong free cash flow generation, and a strengthened balance sheet.

With a clear capital allocation strategy, DFIN is well-positioned to continue returning value to shareholders while investing in future growth opportunities. The company’s long-term financial projections reflect management’s confidence in sustaining double-digit software growth and further margin expansion, despite the inherent volatility in its event-driven transactional business.

As DFIN approaches the midpoint of 2025, investors will be watching closely to see if the company can maintain its momentum in software growth while navigating the cyclical nature of capital markets activity. Based on the latest presentation, management remains confident in the company’s strategic direction and long-term value creation potential.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.