Beamr video compression achieves up to 50% improvement for AVs

Digital Realty Trust Inc . (NYSE:DLR) presented its second-quarter 2025 financial results on July 24, showing record commencements, strong bookings, and improved financial guidance. The data center REIT’s stock rose 0.51% in aftermarket trading to $180.15 following the presentation, building on the positive momentum seen after its Q1 results.

Quarterly Performance Highlights

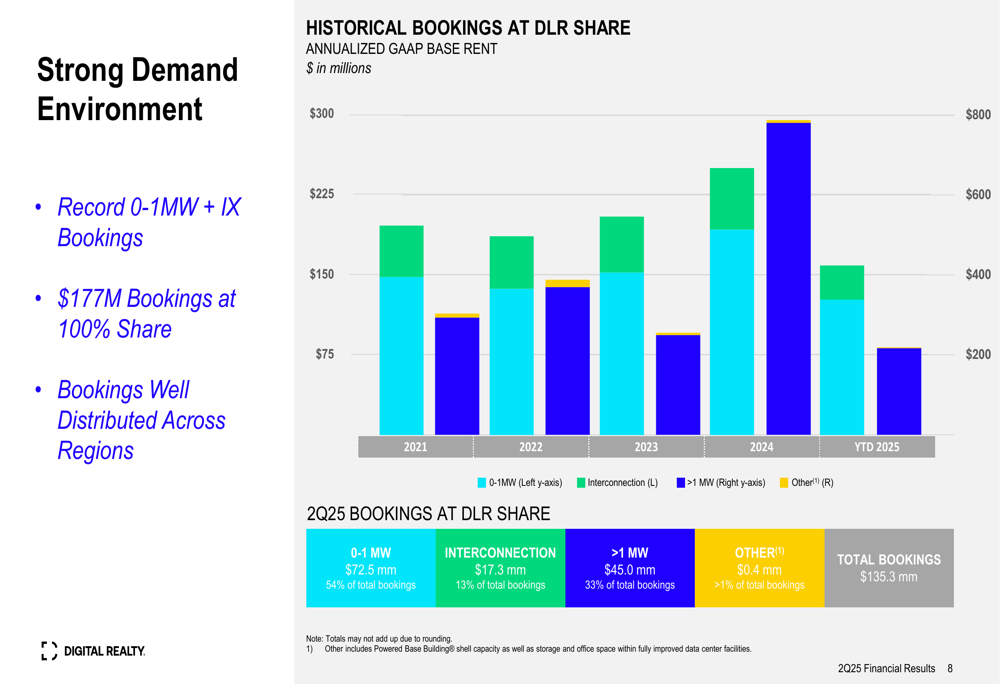

Digital Realty reported record commencements of $228 million and achieved 11% year-over-year growth in data center revenue. The company’s cash flow from operations (CFFO) reached $1.87 per share, demonstrating solid operational execution. Total (EPA:TTEF) bookings at Digital Realty’s share reached $177 million, with a notable $90 million in bookings from the 0-1MW and interconnection segment.

As shown in the following chart of historical bookings, the company has maintained strong demand across its different market segments, with the 0-1MW and interconnection business representing 66% of total Q2 bookings:

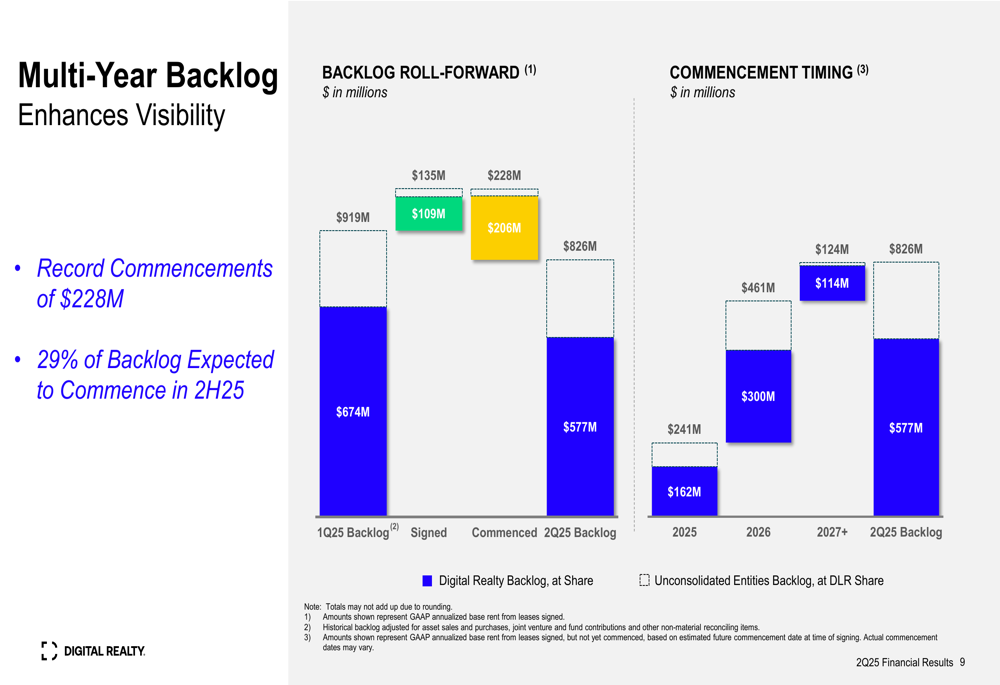

The company’s multi-year backlog stood at $826 million at the end of Q2, providing significant visibility into future revenue streams. According to the presentation, 29% of this backlog is expected to commence in the second half of 2025, with the remainder spread across 2026 and beyond.

As illustrated in this backlog roll-forward chart:

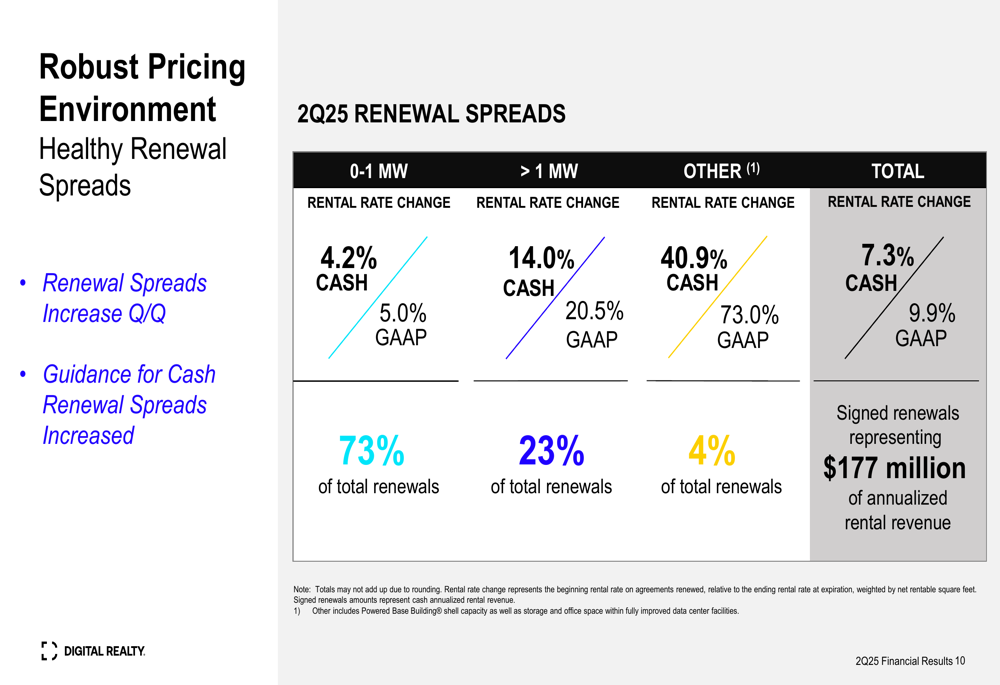

Digital Realty also demonstrated pricing power with healthy renewal spreads. Cash renewal spreads increased to 7.3% overall, with particularly strong performance in the >1MW segment at 14.0% cash renewal spread. This pricing strength led the company to increase its guidance for cash renewal spreads.

The following table details the renewal spread performance across different segments:

Strategic Capital Initiatives

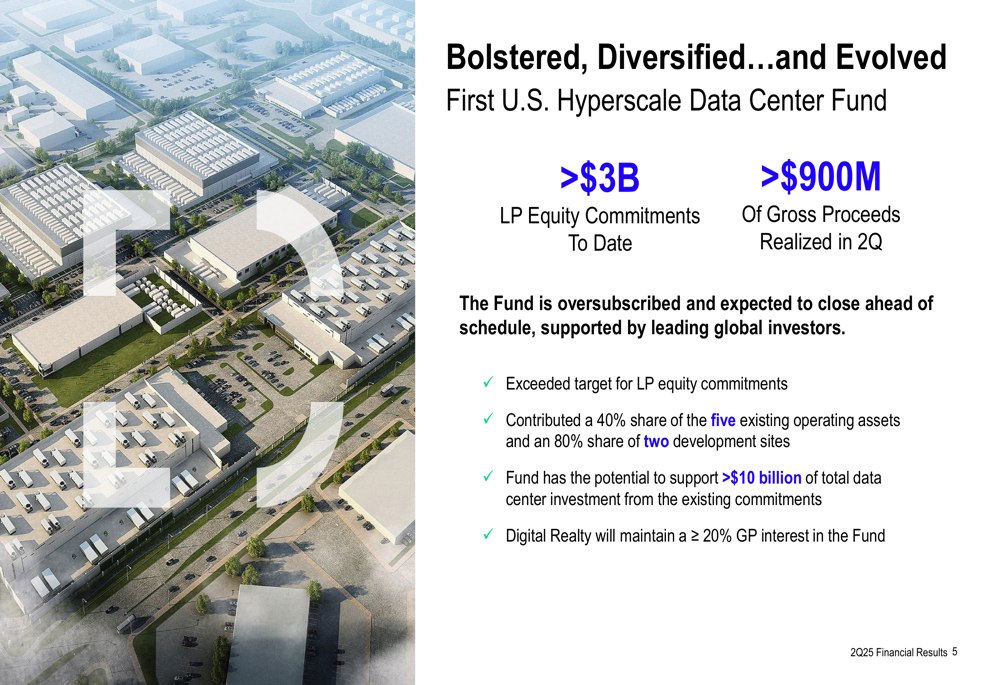

A major highlight of the presentation was Digital Realty’s U.S. Hyperscale Data Center Fund, which has secured over $3 billion in limited partner equity commitments to date and realized more than $900 million of gross proceeds in Q2. The fund is oversubscribed and expected to close ahead of schedule, supported by leading global investors.

According to the presentation, the fund has the potential to support more than $10 billion of total data center investment from existing commitments, with Digital Realty maintaining at least a 20% general partner interest.

The following slide details the fund’s structure and achievements:

The company’s debt profile remains well-managed with a weighted average maturity of 4.6 years and a weighted average coupon of 2.7%. The debt is predominantly unsecured (96%) and fixed-rate (94%), providing stability in the current interest rate environment.

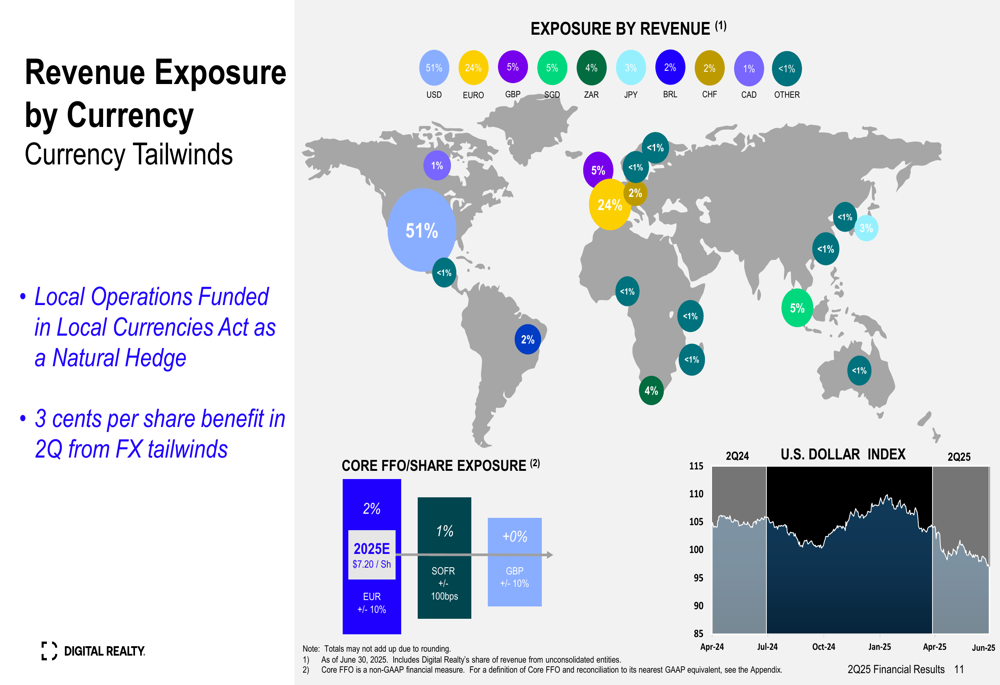

Digital Realty also benefited from currency tailwinds in Q2, which contributed approximately 3 cents per share to results. The company’s revenue is diversified across multiple currencies, with 51% in USD, 24% in Euro, and the remainder spread across various global currencies.

As shown in this currency exposure breakdown:

Global Expansion and Sustainability

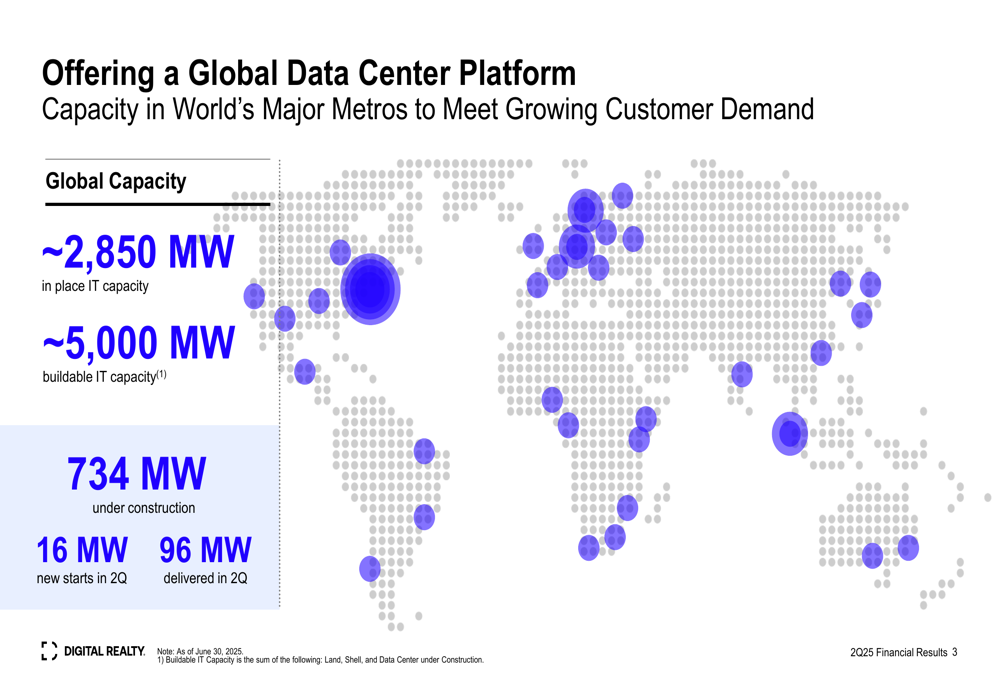

Digital Realty continues to expand its global data center platform, which now includes approximately 2,850 MW of in-place IT capacity and approximately 5,000 MW of buildable IT capacity. The company delivered 96 MW of new capacity in Q2 and initiated 16 MW of new construction starts. Currently, 734 MW are under construction across the company’s global footprint.

The following map illustrates Digital Realty’s global data center presence:

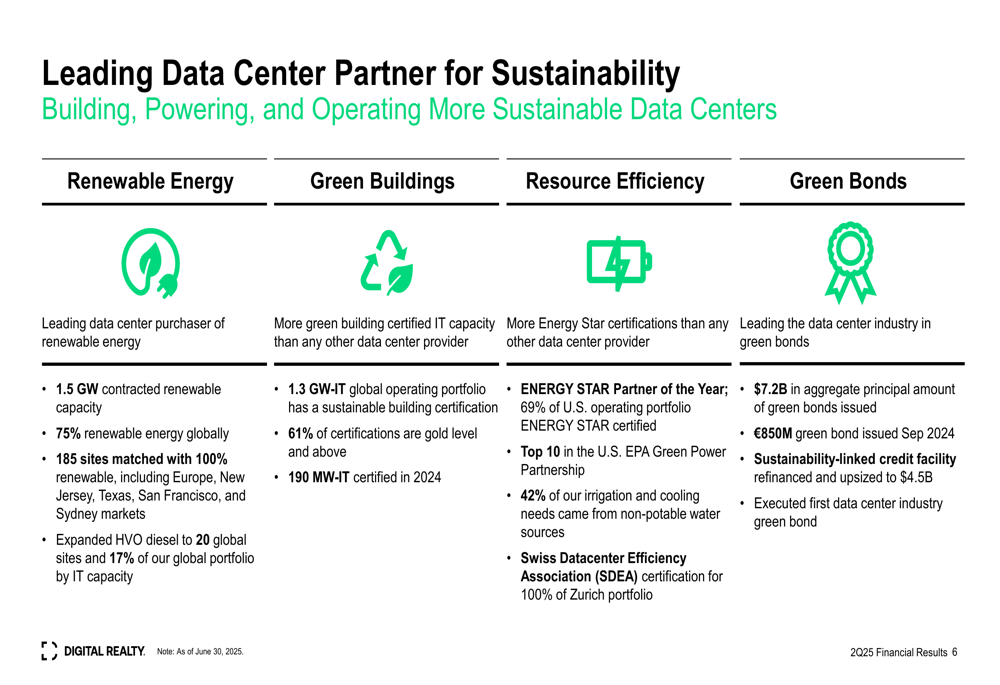

Sustainability remains a core focus for Digital Realty, with 75% of its global energy coming from renewable sources. The company has contracted 1.5 GW of renewable capacity and has 185 sites matched with 100% renewable energy. Additionally, 1.3 GW-IT of the global operating portfolio has sustainable building certifications, with 61% of these certifications at gold level or above.

The company’s comprehensive sustainability initiatives are detailed in this slide:

Financial Outlook and Guidance

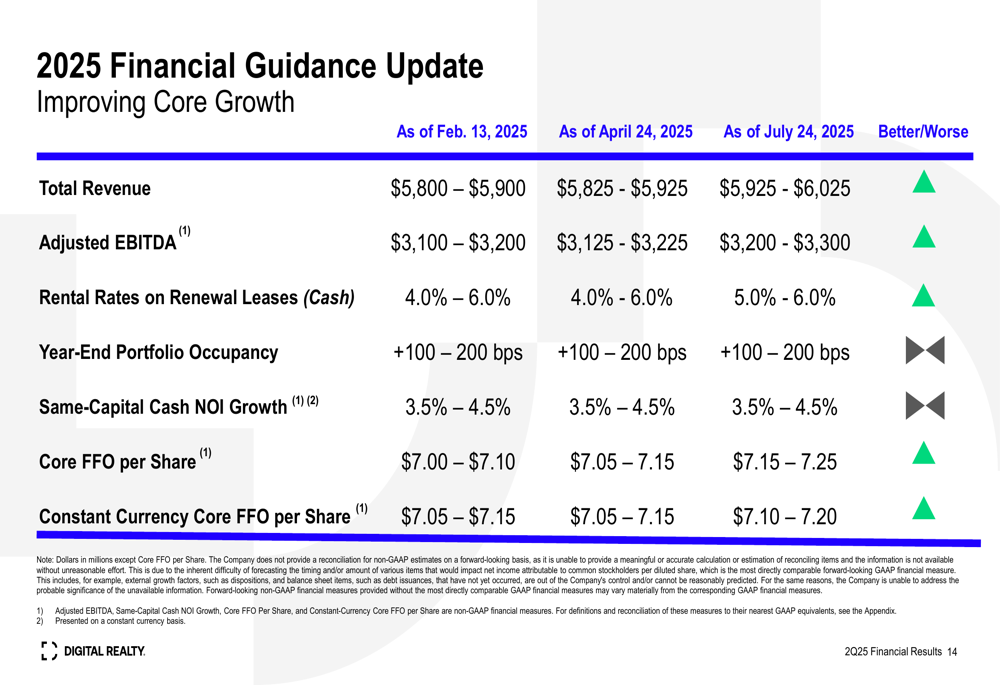

Based on strong Q2 performance, Digital Realty raised its full-year 2025 financial guidance across multiple metrics. Core FFO per share guidance increased from $7.00-$7.10 to $7.15-$7.25, while total revenue guidance was raised from $5,800-$5,900 million to $5,925-$6,025 million. Adjusted EBITDA guidance also improved from $3,100-$3,200 million to $3,200-$3,300 million.

The company maintained its guidance for same-capital cash NOI growth at 3.5%-4.5% and year-end portfolio occupancy growth at +100-200 basis points. Cash renewal rate guidance was increased from 4.0%-6.0% to 5.0%-6.0%, reflecting the company’s pricing strength.

The following table summarizes the updated 2025 financial guidance:

The quarterly cadence of core FFO per share for the remainder of 2025 is expected to be influenced by several factors, including fee income tied to record commencements in Q2, seasonally higher operating expenses in the second half of the year, and increased interest expense following a July refinancing.

Digital Realty’s strategic vision focuses on strengthening its customer value proposition, innovating and integrating for customers, and diversifying capital sources. The company’s Q2 initiatives included record bookings, land acquisitions in three key U.S. metros, and a partnership with Oracle (NYSE:ORCL) Solution Centers to streamline enterprise deployments.

With strong demand for data center capacity, particularly driven by AI-related projects as noted in previous earnings, Digital Realty appears well-positioned to capitalize on the growing need for digital infrastructure globally while maintaining its focus on sustainability and financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.