Nvidia’s results, Indian tariffs, French markets - what’s moving markets

Introduction & Market Context

DNOW Inc. (NYSE:DNOW) presented its first quarter 2025 results on May 7, showing revenue and EBITDA growth despite flat drilling activity in key markets. The company reported a 6% year-over-year revenue increase to $599 million, while operating in an environment where U.S. rig counts remained flat sequentially at 588 and global rig counts held steady at 1,707.

The distribution company’s performance comes amid WTI crude oil prices averaging $72 per barrel during the quarter, with U.S. well completions declining 2% sequentially to 2,801 wells. Despite these challenging market conditions, DNOW managed to generate $1.4 million in annualized revenue per rig.

In premarket trading, DNOW shares were down 5.12% to $15.21, suggesting investors may have had higher expectations despite the company’s growth.

Quarterly Performance Highlights

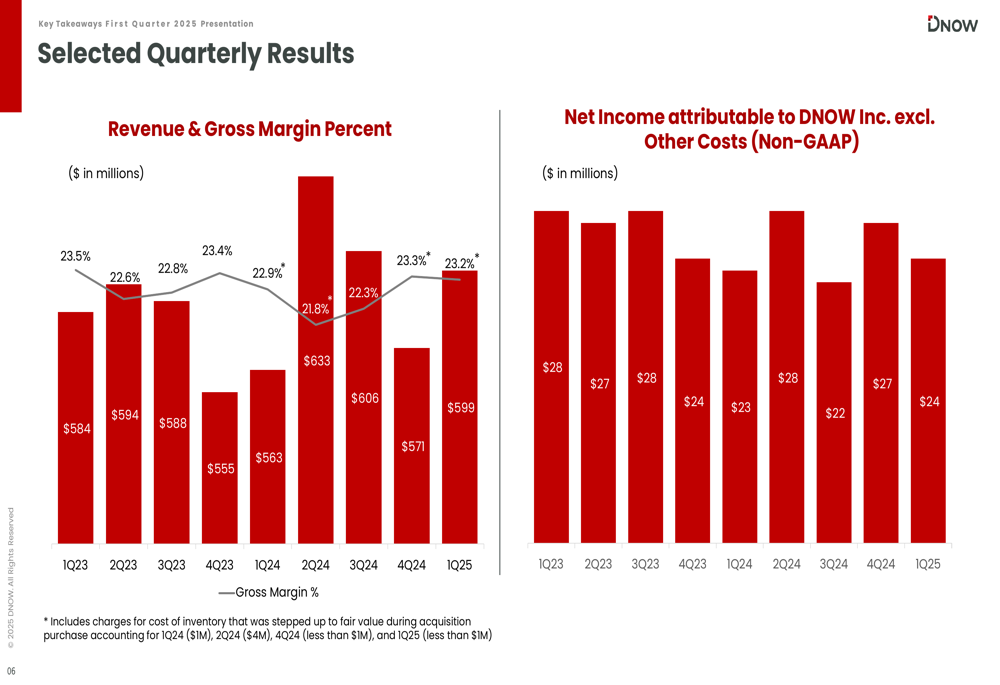

DNOW reported solid financial results for Q1 2025, with revenue increasing both sequentially and year-over-year. The company achieved GAAP net income of $22 million, translating to diluted earnings per share of $0.20, while non-GAAP net income reached $24 million or $0.22 per diluted share.

As shown in the following quarterly results chart, DNOW has maintained relatively stable revenue and gross margins over the past two years:

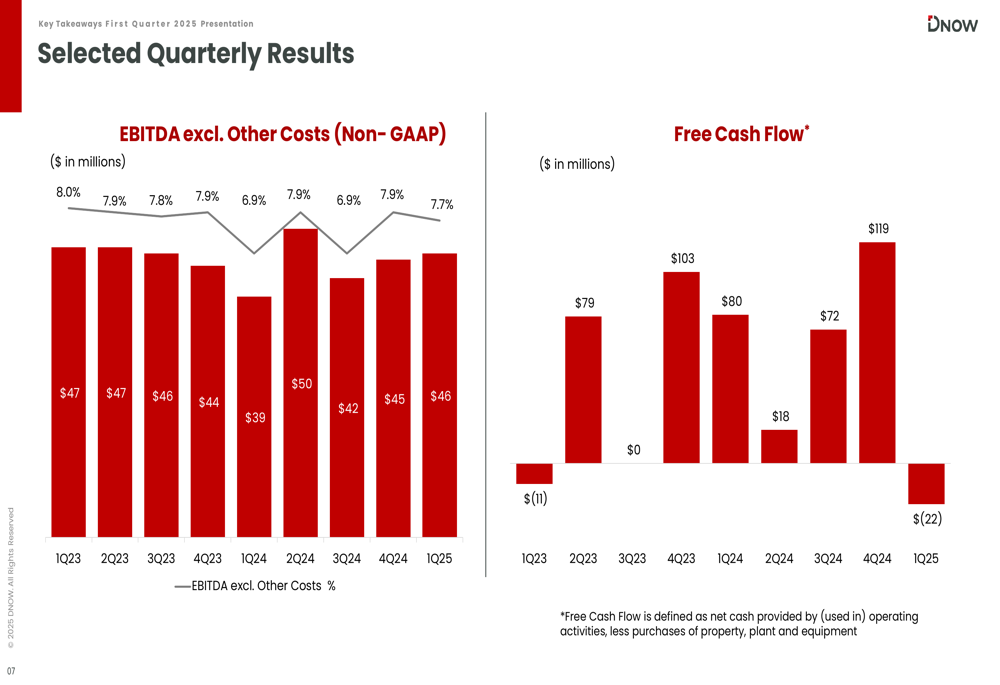

EBITDA for the quarter reached $46 million, representing 7.7% of revenue, a slight improvement from the previous quarter’s 7.6%. The company’s gross margins remained healthy at 23.2%, consistent with recent quarters. The following chart illustrates DNOW’s EBITDA performance and free cash flow trends:

Free cash flow was negative $22 million for the quarter, which follows a seasonal pattern as the first quarter typically shows negative free cash flow before improving throughout the year. This compares to $119 million in free cash flow during Q4 2024, which contributed to the company’s strong year-end cash position.

Segment Performance

DNOW’s segment results showed mixed performance across its geographic divisions. The U.S. segment, which represents approximately 79% of total revenue, grew to $474 million, up from $435 million in Q1 2024. This growth was primarily driven by acquisitions, partially offset by weakening drilling and completion activity.

The Canadian segment experienced a revenue decline to $62 million from $66 million in the prior year, primarily due to unfavorable exchange rates. However, operating profit improved to $4 million from $3 million due to lower operating expenses.

The International segment showed modest revenue growth to $63 million from $62 million year-over-year, with operating profit doubling to $4 million from $2 million, driven by increased project activity and reduced operating expenses.

Financial Position & Capital Allocation

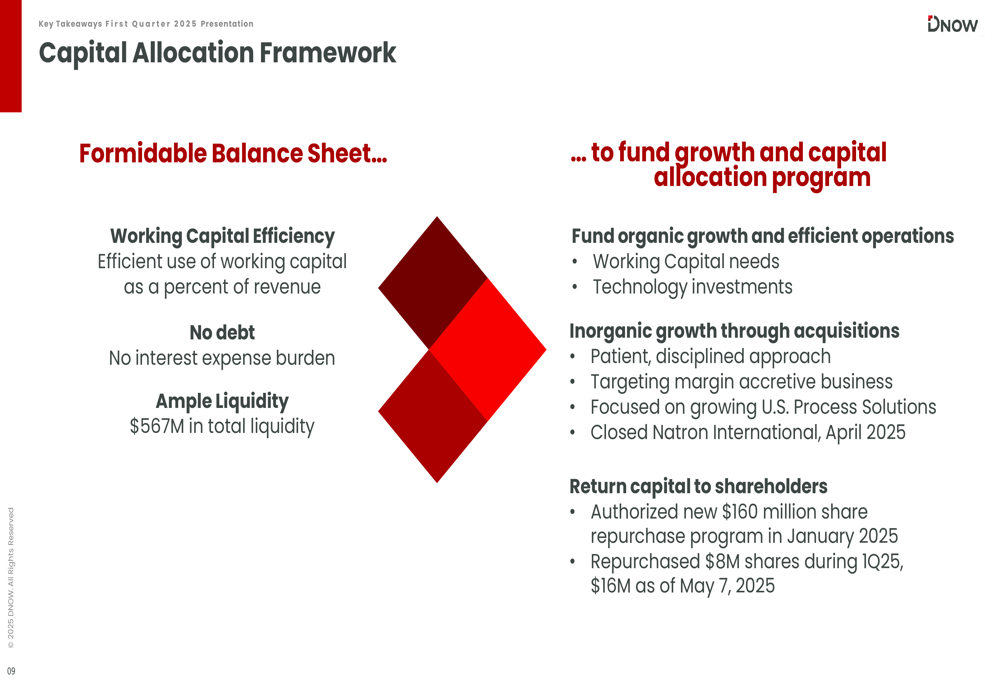

DNOW maintains a strong balance sheet with no debt and total liquidity of $567 million as of March 31, 2025, consisting of $348 million in cash and $219 million in credit availability. The company’s working capital excluding cash stood at $388 million, representing 16.2% of revenue.

The company’s capital allocation strategy emphasizes both organic growth and strategic acquisitions, as illustrated in this framework:

During Q1 2025, DNOW repurchased $8 million in shares as part of its $160 million share repurchase program, with a total of $16 million repurchased year-to-date as of May 7, 2025. This represents a continuation of the company’s commitment to returning capital to shareholders while maintaining financial flexibility.

Strategic Initiatives & Acquisitions

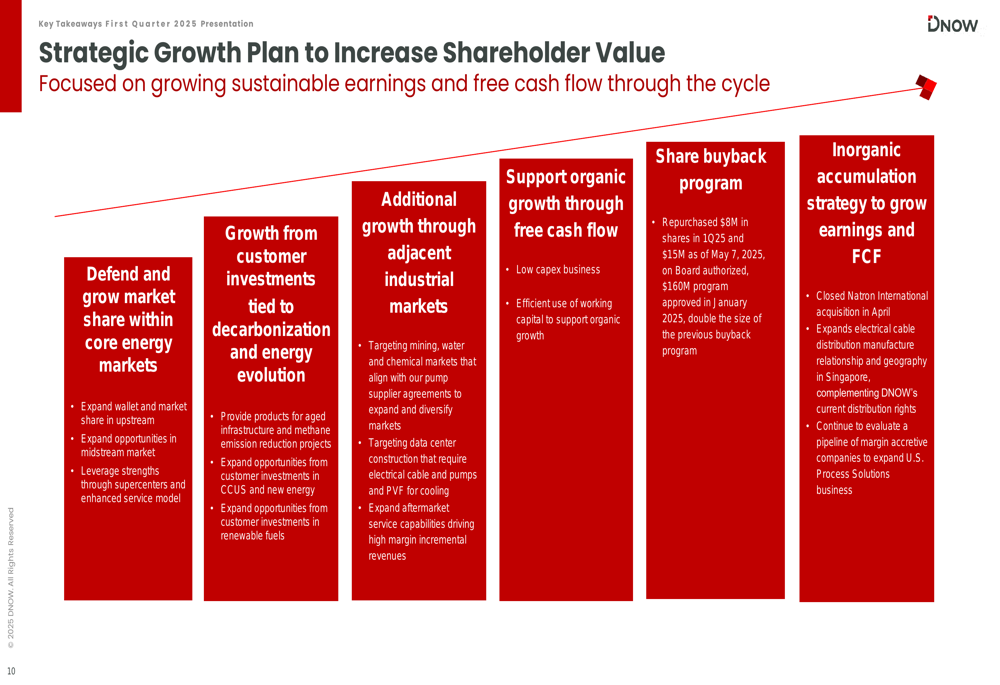

DNOW’s strategic growth plan focuses on defending and growing market share in core energy markets while expanding into adjacent industrial sectors and pursuing opportunities related to decarbonization and energy evolution.

The company completed the acquisition of Natron International in April 2025, expanding its international presence. Additionally, DNOW is targeting expansion of its electrical cable distribution manufacturing relationship and geographic footprint in Singapore.

As outlined in the strategic growth plan below, DNOW continues to evaluate acquisition targets that would be margin-accretive and expand its U.S. Process Solutions business:

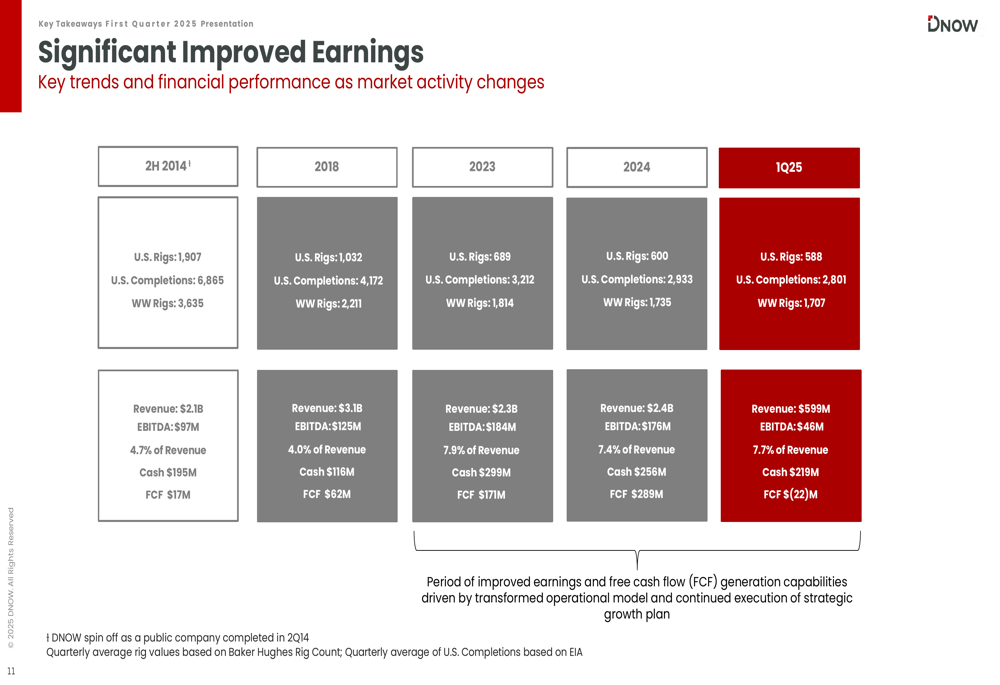

The company’s long-term performance demonstrates significant earnings improvement despite operating with substantially fewer rigs compared to historical levels. This transformation reflects DNOW’s successful operational model changes and strategic initiatives:

Forward-Looking Statements

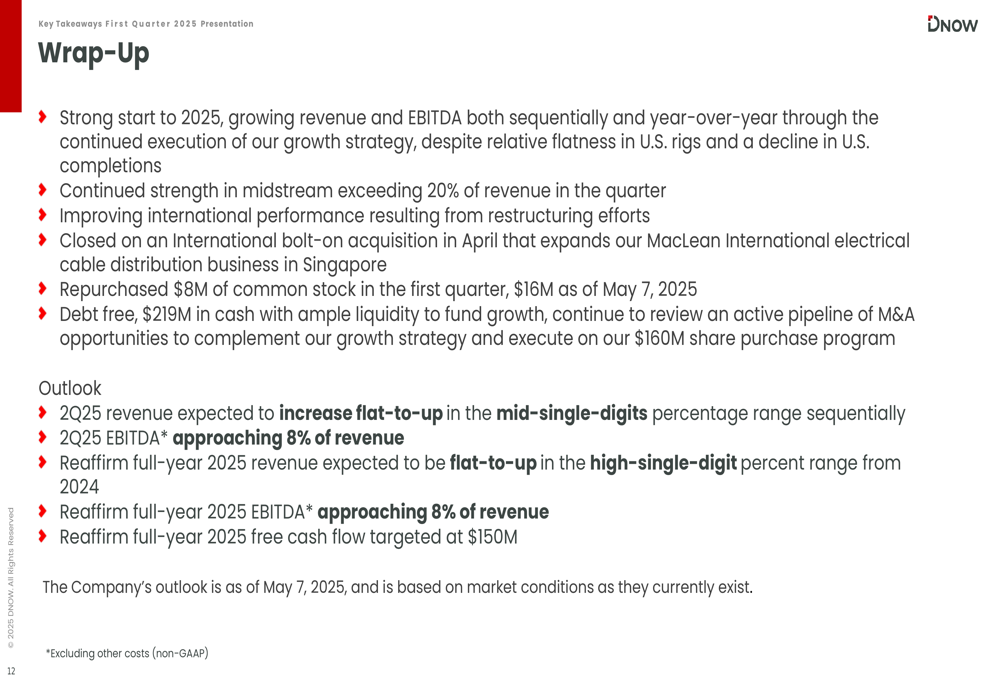

Looking ahead, DNOW expects second quarter 2025 revenue to increase flat-to-up in the mid-single-digits percentage range sequentially, with EBITDA approaching 8% of revenue. The company reaffirmed its full-year 2025 revenue and EBITDA guidance, targeting $150 million in free cash flow for the year.

Management highlighted continued strength in midstream markets and improving international performance as key drivers for future growth. The company’s debt-free balance sheet and ample liquidity position it well to pursue both organic growth opportunities and strategic acquisitions.

As summarized in the company’s wrap-up slide, DNOW started 2025 with sequential and year-over-year growth in both revenue and EBITDA:

Despite the premarket stock decline, DNOW’s Q1 2025 results demonstrate the company’s ability to grow revenue and maintain profitability in a challenging energy market environment through strategic acquisitions, operational efficiency, and disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.