Goldman Sachs raises its gold price target to $4,900 by end-2026

Introduction & Market Context

DocuSign (NASDAQ:DOCU) presented its Q1 FY26 results on June 5, 2025, showing continued growth as the company expands beyond its core e-signature business. The presentation highlighted DocuSign’s evolution toward becoming a comprehensive agreement management platform while maintaining strong financial performance.

Following a strong Q4 FY25 where the stock surged 8.45% after beating earnings expectations, DocuSign’s shares traded at $93.84 at market close on June 5, 2025, down 0.9% for the day, with a slight recovery to $94.20 in after-hours trading.

Quarterly Performance Highlights

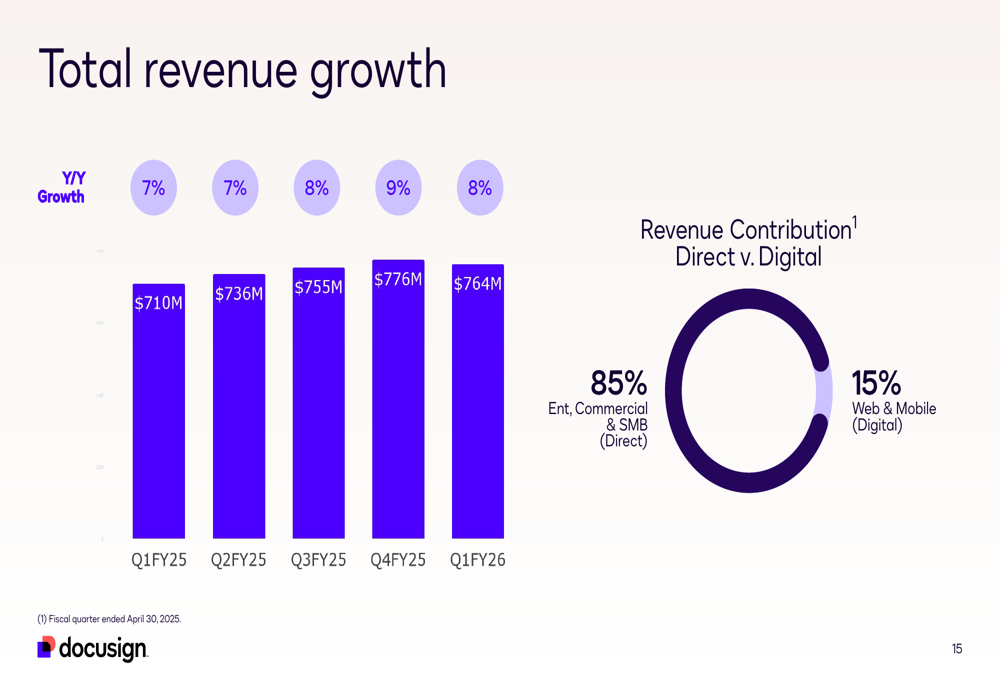

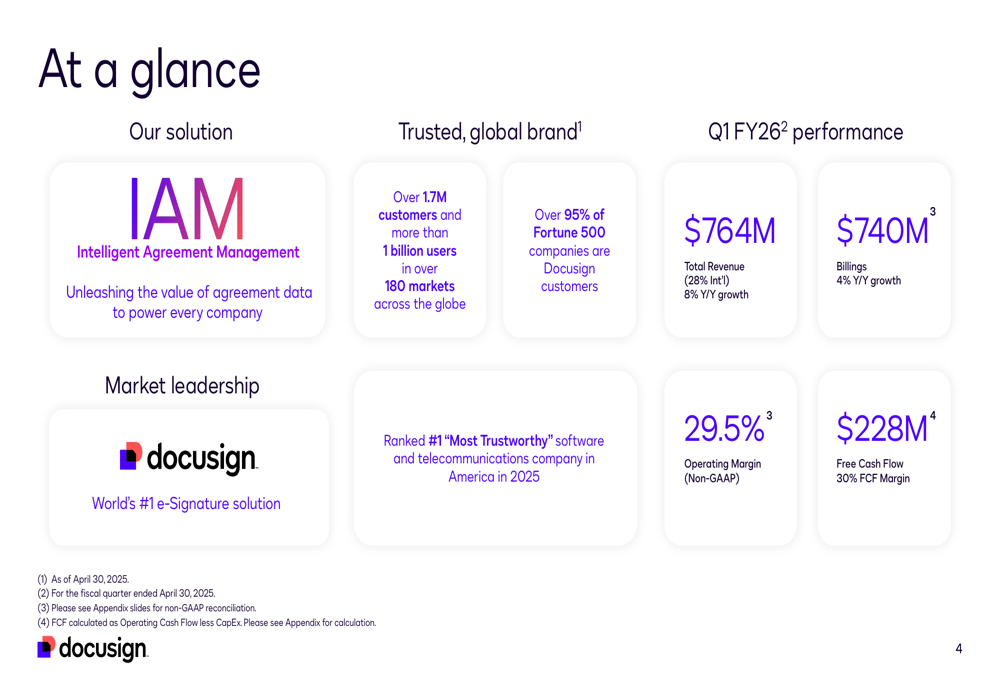

DocuSign reported Q1 FY26 revenue of $764 million, representing an 8% year-over-year increase, while billings grew 4% to $740 million. The company maintains its position as the leading e-signature solution globally, serving over 1.7 million customers across 180+ markets, including more than 95% of Fortune 500 companies.

As shown in the following chart of quarterly revenue growth, DocuSign has maintained steady revenue growth between 7-9% over the past five quarters:

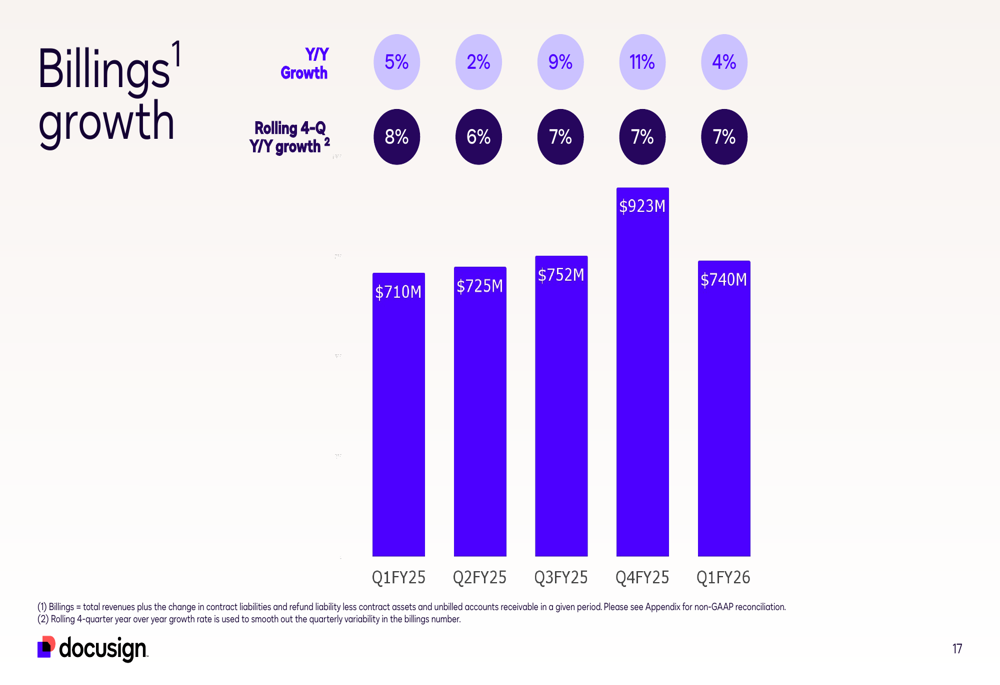

Subscription revenue, which accounts for 98% of total revenue, reached $746 million in Q1 FY26, also growing 8% year-over-year. The company’s billings growth has been more variable, with Q4 FY25 showing the strongest performance at 11% growth, while Q1 FY26 billings growth moderated to 4%.

The following chart illustrates DocuSign’s billings performance over recent quarters:

Strategic Initiatives

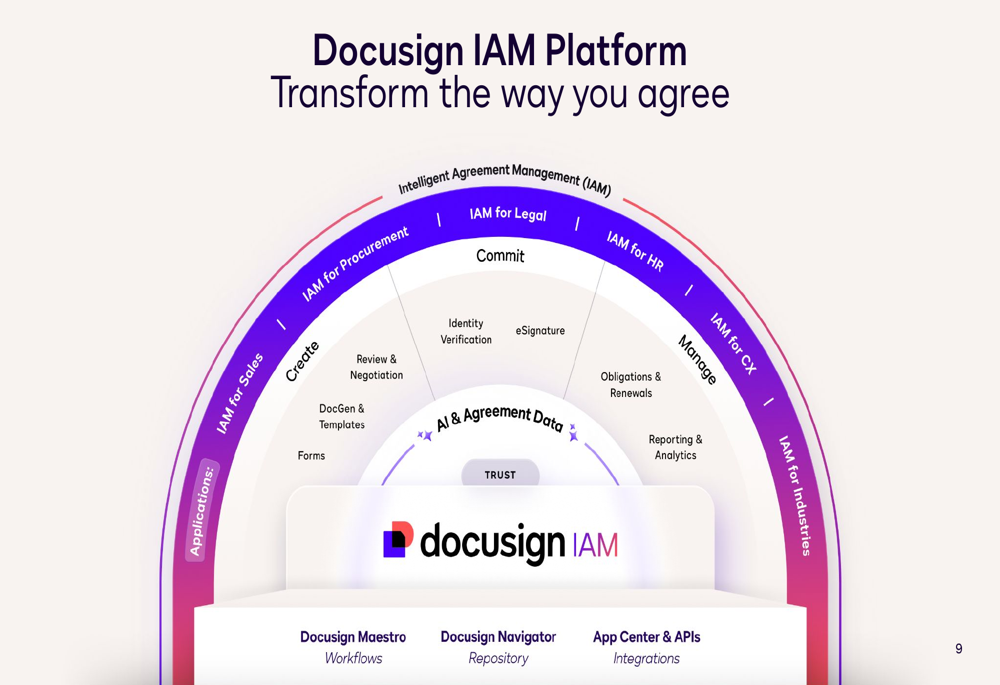

A central theme of DocuSign’s presentation was the company’s strategic focus on its Intelligent Agreement Management (IAM) platform, which aims to transform how organizations create, commit to, and manage agreements. The IAM platform represents DocuSign’s evolution from a single-product e-signature company to a comprehensive agreement lifecycle management provider.

The company’s IAM platform architecture is illustrated in the following diagram:

DocuSign expects IAM to represent a low double-digit percentage of its subscription business by the end of FY26, indicating the growing importance of this strategic initiative.

International expansion continues to be a key growth driver for DocuSign, with international revenue growing 10% year-over-year in Q1 FY26 and now representing 28% of total revenue. The company employs a tiered approach to international growth, focusing direct investment on Tier 1 markets while leveraging partners and digital channels for Tier 2 and Tier 3 markets.

The following map illustrates DocuSign’s international growth strategy:

Financial Analysis

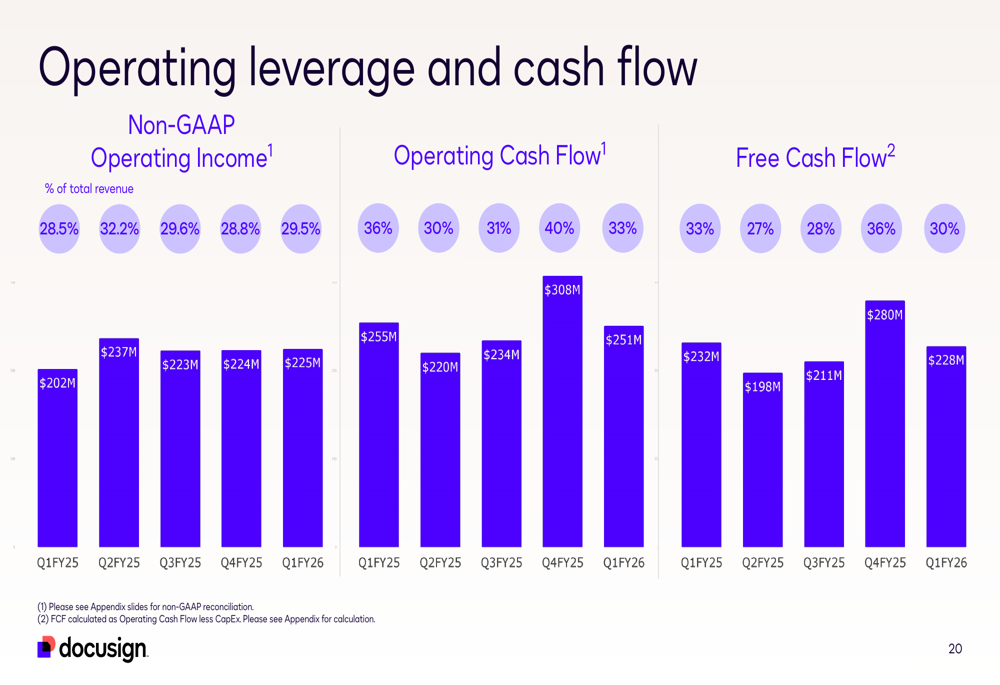

DocuSign maintained strong profitability in Q1 FY26, with a non-GAAP operating margin of 29.5% and free cash flow of $228 million, representing a 30% margin. The company’s gross margins remained stable at 82.3% (total) and 84.0% (subscription).

The following chart shows DocuSign’s operating leverage and cash flow performance:

Operating expenses as a percentage of revenue have been well-managed, with sales and marketing at 31.8%, research and development at 13.1%, and general and administrative at 7.9% in Q1 FY26 on a non-GAAP basis.

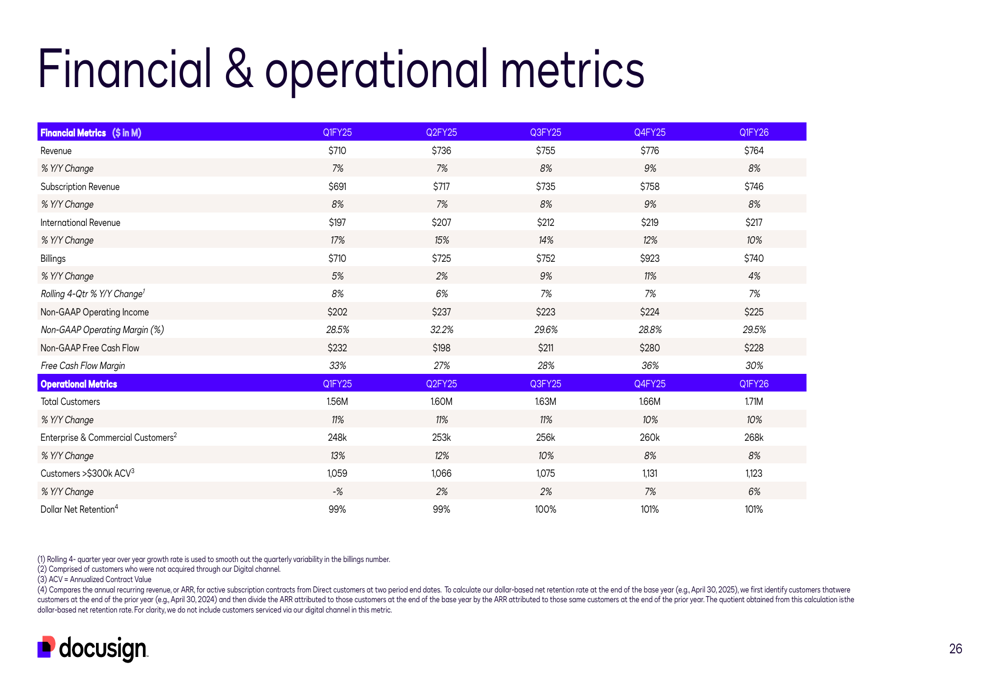

DocuSign’s comprehensive financial and operational metrics are summarized in the following table:

Forward Guidance

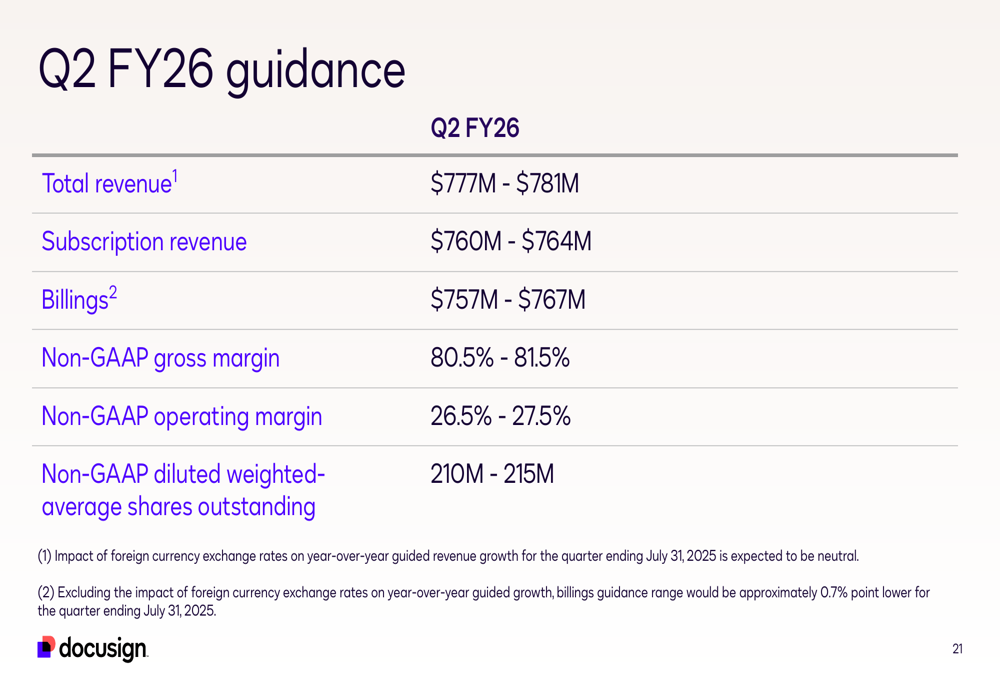

For Q2 FY26, DocuSign projects total revenue between $777-$781 million and subscription revenue between $760-$764 million. Billings are expected to reach $757-$767 million, with a non-GAAP operating margin between 26.5-27.5%.

The detailed Q2 FY26 guidance is presented in the following slide:

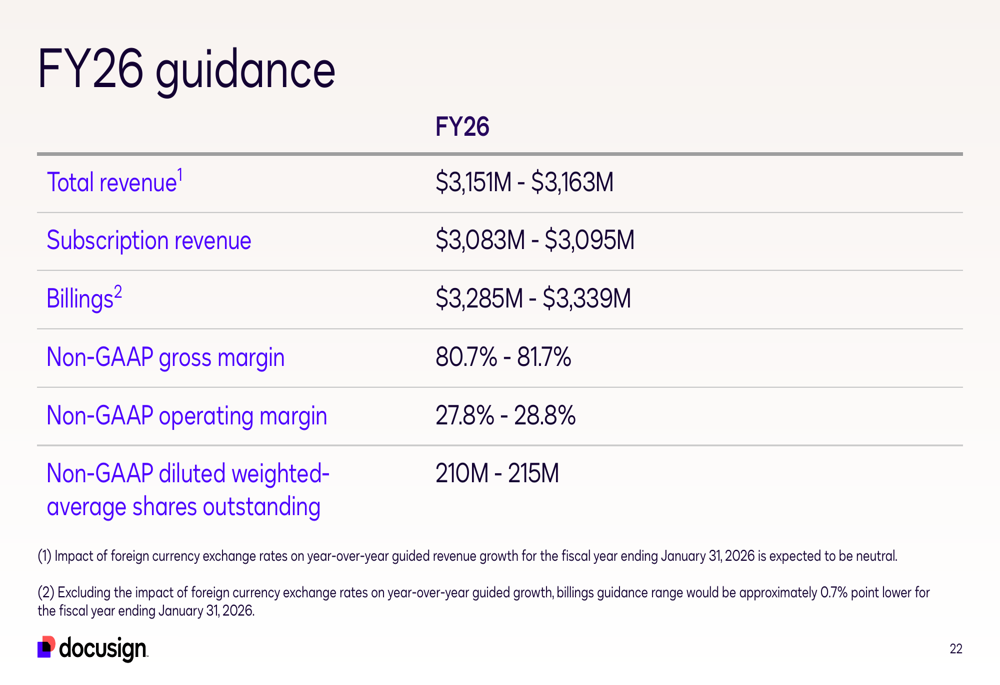

For the full fiscal year 2026, DocuSign forecasts total revenue of $3,151-$3,163 million, representing approximately 5% growth year-over-year. The company expects billings of $3,285-$3,339 million and a non-GAAP operating margin between 27.8-28.8%.

The full-year guidance is illustrated in the following slide:

Management noted several modeling considerations for investors, including an expected 1% headwind to gross margins due to ongoing cloud migration and a 1.5% headwind to operating margins from cloud migration and comparison items. The company expects dollar net retention rate to moderately improve throughout the year.

DocuSign’s key metrics presentation provides a comprehensive overview of the company’s current position and strategic direction:

As DocuSign continues its transition from an e-signature provider to a comprehensive agreement management platform, the company’s steady revenue growth and strong margins demonstrate its ability to execute on strategic initiatives while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.