Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

DocuSign Inc (NASDAQ:DOCU) released its Q2 FY26 earnings presentation on September 4, 2025, showcasing accelerating billings growth and continued progress on its strategic transition to a comprehensive Intelligent Agreement Management (IAM) platform. The company reported 9% year-over-year revenue growth while maintaining strong profitability metrics.

Quarterly Performance Highlights

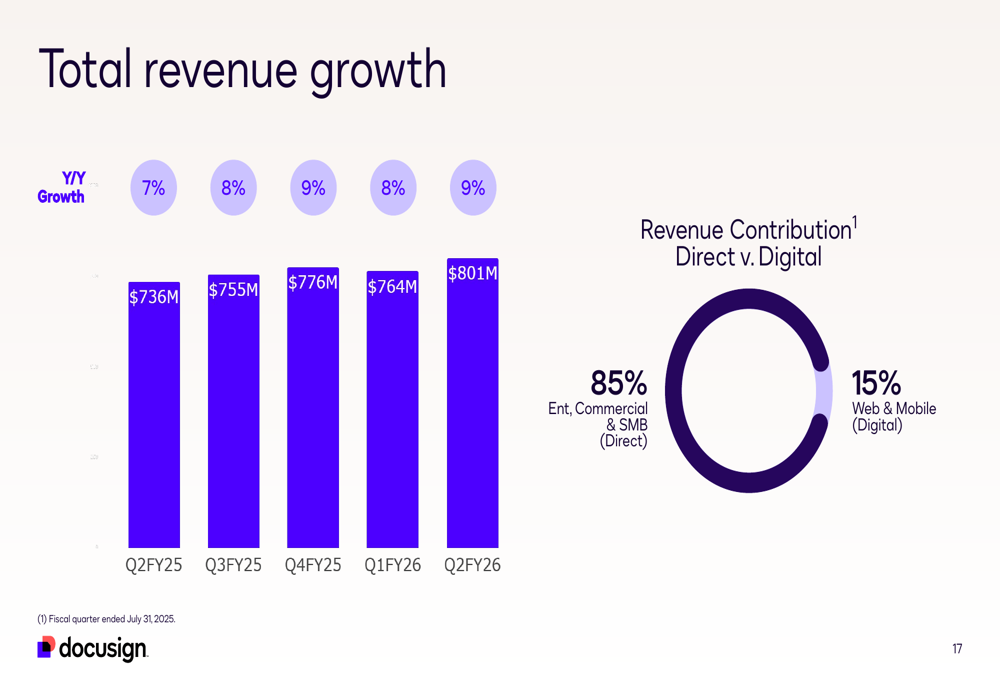

DocuSign reported total revenue of $801 million in Q2 FY26, representing 9% year-over-year growth, up from 8% growth in the previous quarter. Subscription revenue, which accounts for 98% of total revenue, also grew 9% year-over-year to $784 million. The company’s customer base expanded to over 1.7 million, with 95% of Fortune 500 companies using DocuSign’s solutions.

As shown in the following quarterly revenue chart, DocuSign has maintained steady revenue growth over the past five quarters:

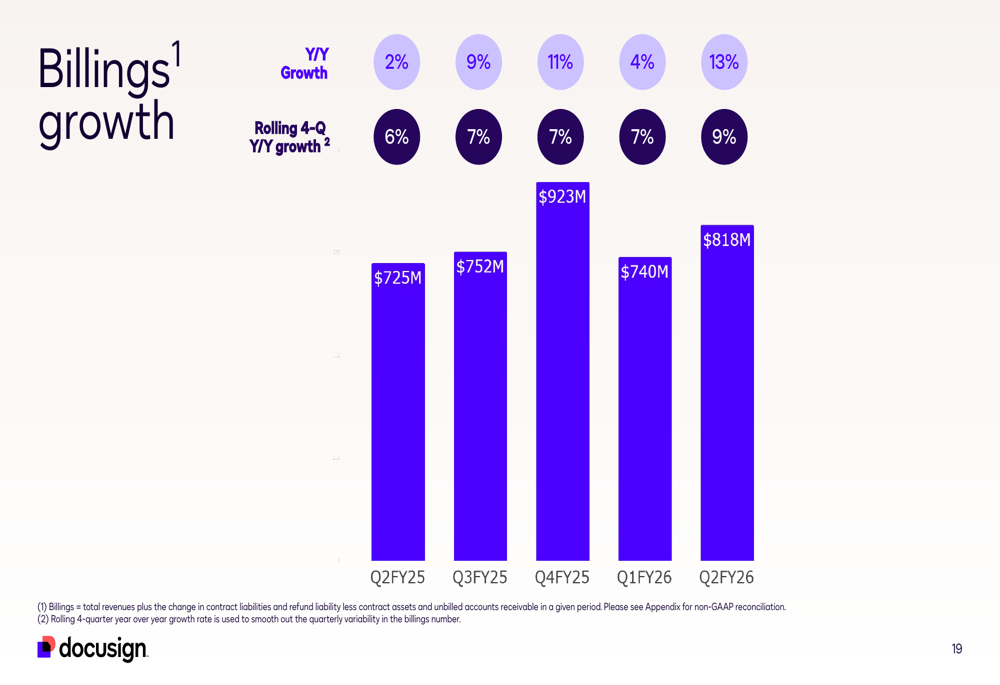

A notable highlight was the acceleration in billings growth, which reached 13% year-over-year in Q2 FY26, compared to just 2% in the same quarter last year. The rolling four-quarter billings growth also improved to 9%, indicating strengthening business momentum.

The following chart illustrates the acceleration in billings growth:

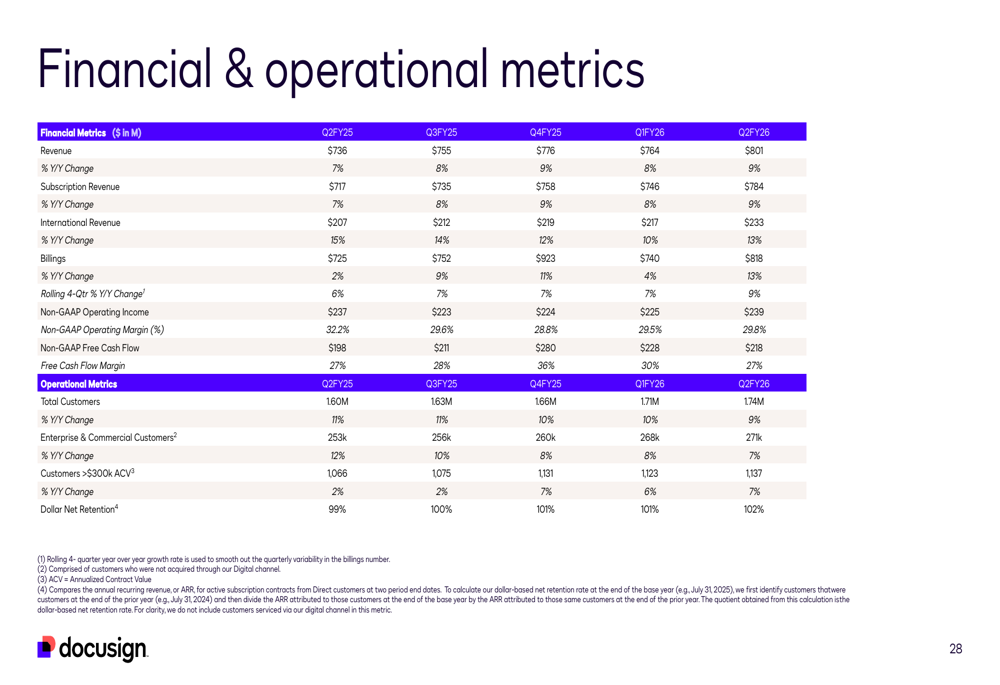

DocuSign’s operational metrics also showed improvement, with Dollar Net Retention increasing to 102% from 99% in the prior year. This metric is particularly important as it indicates the company’s ability to retain and expand revenue from existing customers.

The comprehensive financial and operational metrics table below provides a clear overview of DocuSign’s performance trends:

Strategic Initiatives: IAM Platform Transition

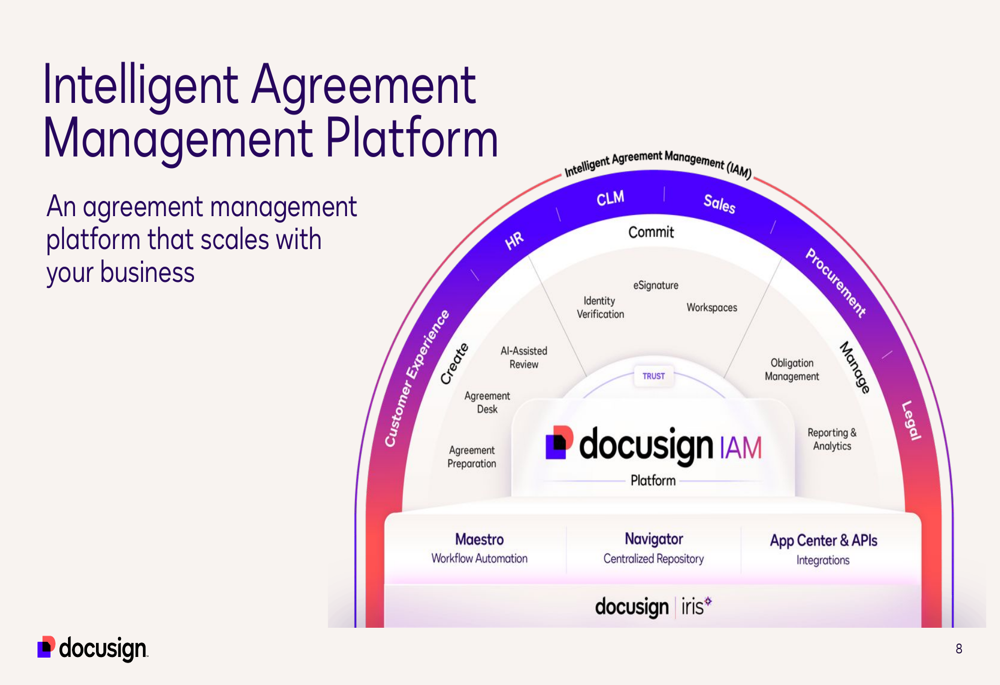

DocuSign continues to execute on its strategic evolution from a pure e-signature provider to a comprehensive Intelligent Agreement Management (IAM) platform. This transformation represents the third major phase in the company’s development, following its initial "Digital & Trusted" phase (2003-2017) and subsequent "Negotiation" phase (2018-2023).

The IAM platform addresses the entire agreement lifecycle from creation and commitment to management, helping organizations advance their agreement maturity. The company expects IAM to represent a low double-digit percentage of its subscription book by the end of FY26.

The following diagram illustrates DocuSign’s comprehensive IAM platform approach:

DocuSign’s CEO has positioned the IAM platform as central to the company’s growth strategy, emphasizing how it helps customers digitize, centralize, standardize, automate, and optimize their agreement processes.

International Expansion

International revenue grew 13% year-over-year in Q2 FY26, outpacing overall company growth, and now represents 29% of total revenue. DocuSign is implementing a tiered approach to international expansion, with different investment levels based on market potential.

The company’s international growth strategy is illustrated in the following map:

Financial Analysis

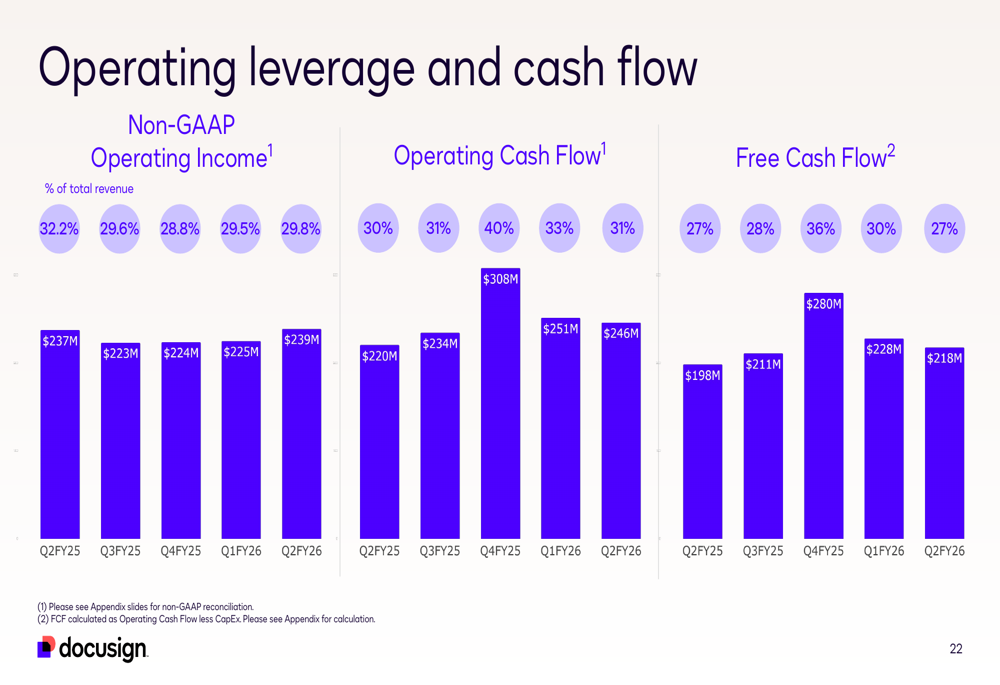

DocuSign maintained strong profitability in Q2 FY26, with a non-GAAP operating margin of 29.8%. The company generated $218 million in free cash flow, representing a robust 27% of revenue.

The following chart shows DocuSign’s operating leverage and cash flow performance:

Operating expenses as a percentage of revenue remained well-controlled, with sales and marketing at 31.2%, research and development at 13.1%, and general and administrative at 7.9% of revenue. This disciplined expense management has enabled DocuSign to maintain healthy profit margins while continuing to invest in growth initiatives.

Forward-Looking Statements

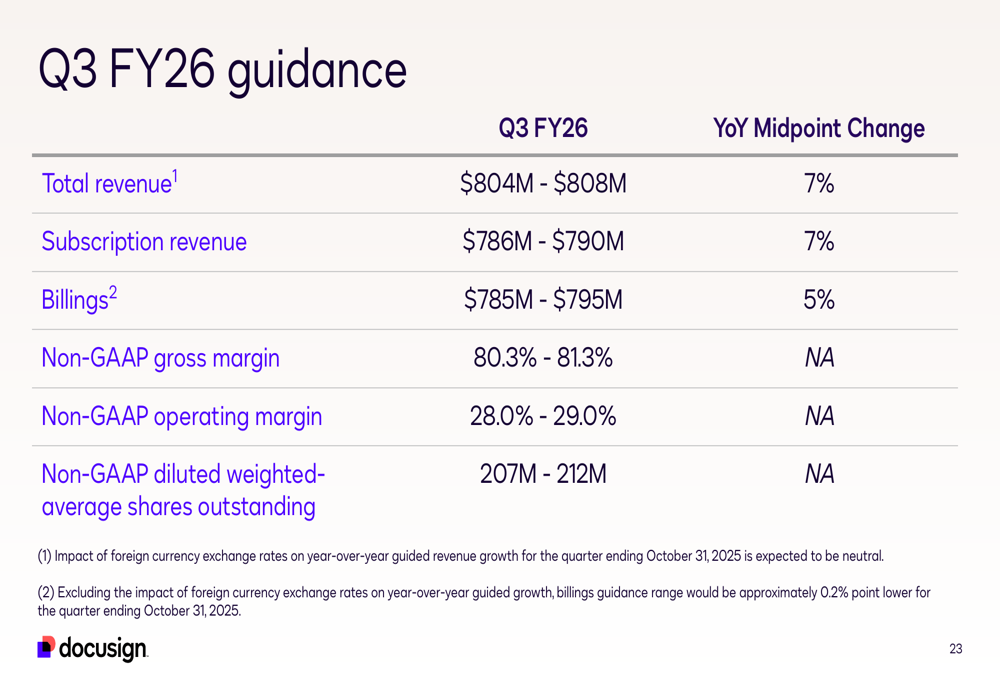

For Q3 FY26, DocuSign provided guidance for total revenue of $804-808 million (7% year-over-year growth) and billings of $785-795 million (5% year-over-year growth). The company expects a non-GAAP operating margin between 28.0% and 29.0%.

The Q3 guidance details are shown in the following table:

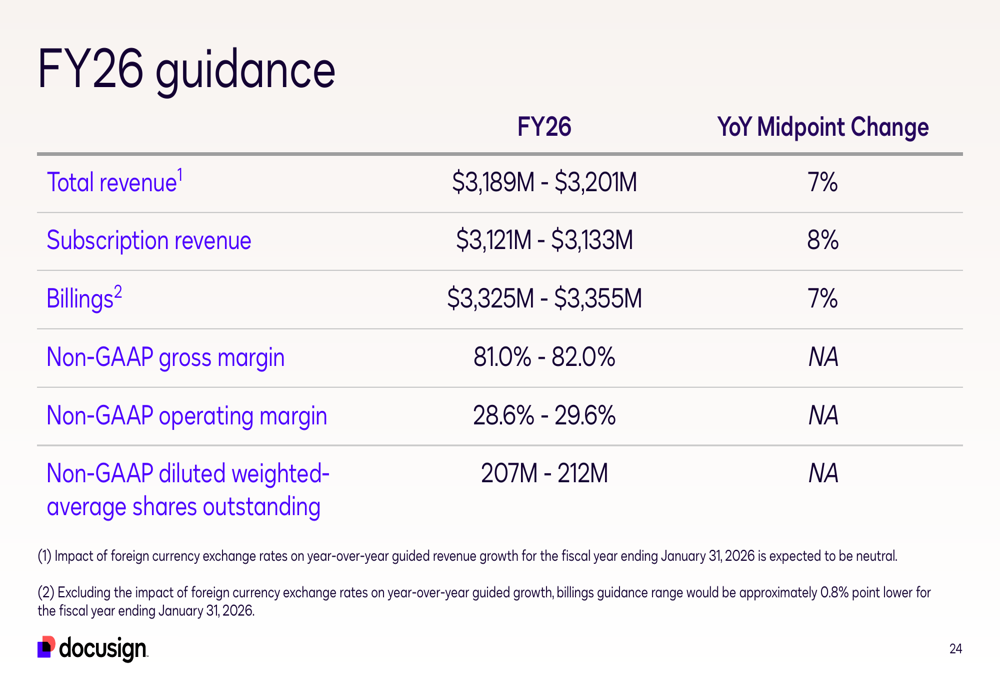

For the full fiscal year 2026, DocuSign projects total revenue of $3,189-3,201 million (7% year-over-year growth) and billings of $3,325-3,355 million (7% year-over-year growth). The company maintains its full-year non-GAAP operating margin guidance of 28.6% to 29.6%.

The full-year guidance is detailed in the following table:

Management noted that foreign currency exchange rates are expected to have a neutral impact on both Q3 and full-year results. The company also highlighted that early renewal impacts would make full-year billings growth approximately 1 percentage point higher year-over-year, leading to modest acceleration.

Following the earnings presentation, DocuSign’s stock closed at $75.90, up 0.47% for the day, though it showed a slight decline of 0.53% in aftermarket trading. The stock remains within its 52-week range of $54.32 to $107.86, suggesting mixed investor sentiment despite the company’s improving operational metrics.

As DocuSign continues its transition from a pure e-signature provider to a comprehensive agreement management platform, investors will be watching closely for continued acceleration in billings growth and further improvements in customer retention metrics as indicators of the strategy’s success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.