BitMine stock falls after CEO change and board appointments

Introduction & Market Context

Donegal Group Inc. (NASDAQ:DGICA) presented its third quarter 2025 results on October 30, highlighting a 19.9% increase in net income despite facing headwinds in premium growth. The regional insurer, which operates across Mid-Atlantic, Midwestern, Southern, and Southwestern states, continues to execute its strategy of emphasizing commercial lines while maintaining a profitable personal lines business.

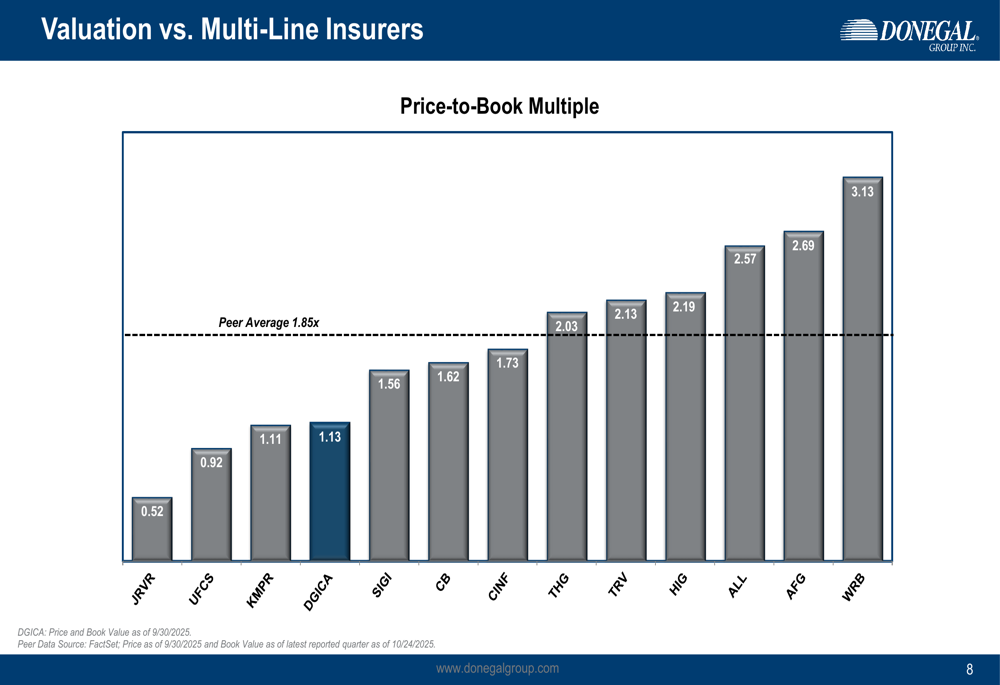

The company’s stock rose 1.88% in pre-market trading following the earnings release, reflecting investor confidence in its financial performance despite revenue challenges. With a current price-to-book multiple of 1.13, significantly below the peer average of 1.85x, Donegal appears undervalued compared to its multi-line insurer competitors.

Quarterly Performance Highlights

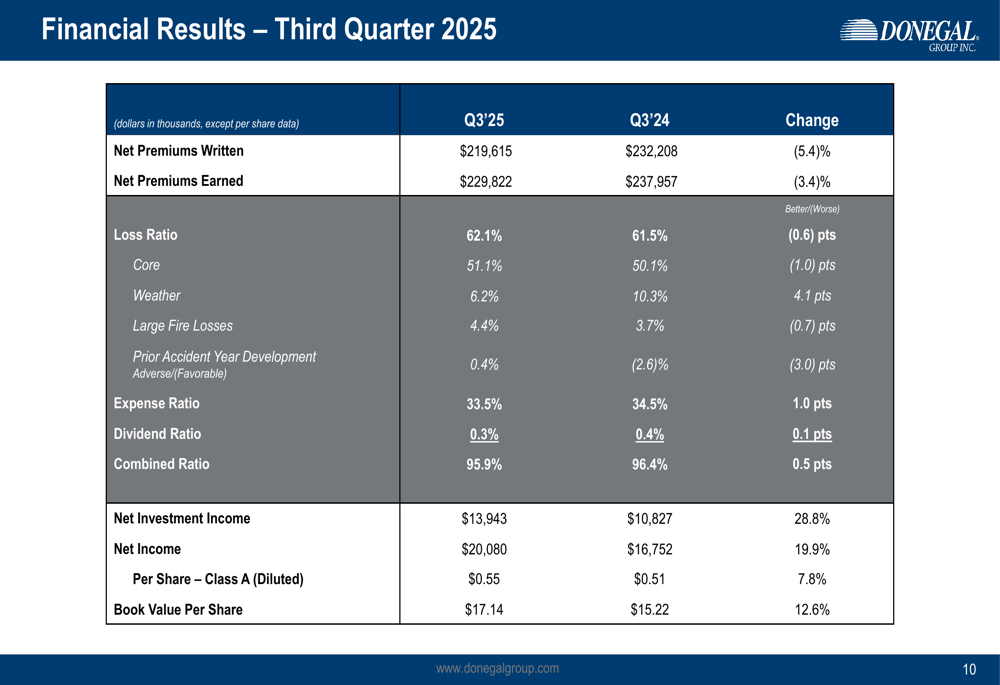

Donegal reported net income of $20.1 million for Q3 2025, a 19.9% increase compared to the same period in 2024. Diluted earnings per share for Class A shares reached $0.55, up 7.8% year-over-year. This performance exceeded analyst expectations of $0.44 per share by approximately 18%.

The company’s combined ratio improved to 95.9%, down 0.5 percentage points from 96.4% in Q3 2024, indicating better underwriting profitability. This improvement came despite a slight increase in the loss ratio to 62.1% (up 0.6 points), as the expense ratio decreased to 33.5% (down 1.0 points).

As shown in the following financial results comparison:

Net premiums written decreased 5.4% to $219.6 million, while net premiums earned fell 3.4% to $229.8 million. According to CEO Kevin Burke, who was quoted in the earnings call as saying, "We are now operating from a position of strength," this decline reflects the company’s strategic decision to focus on profitability over premium growth.

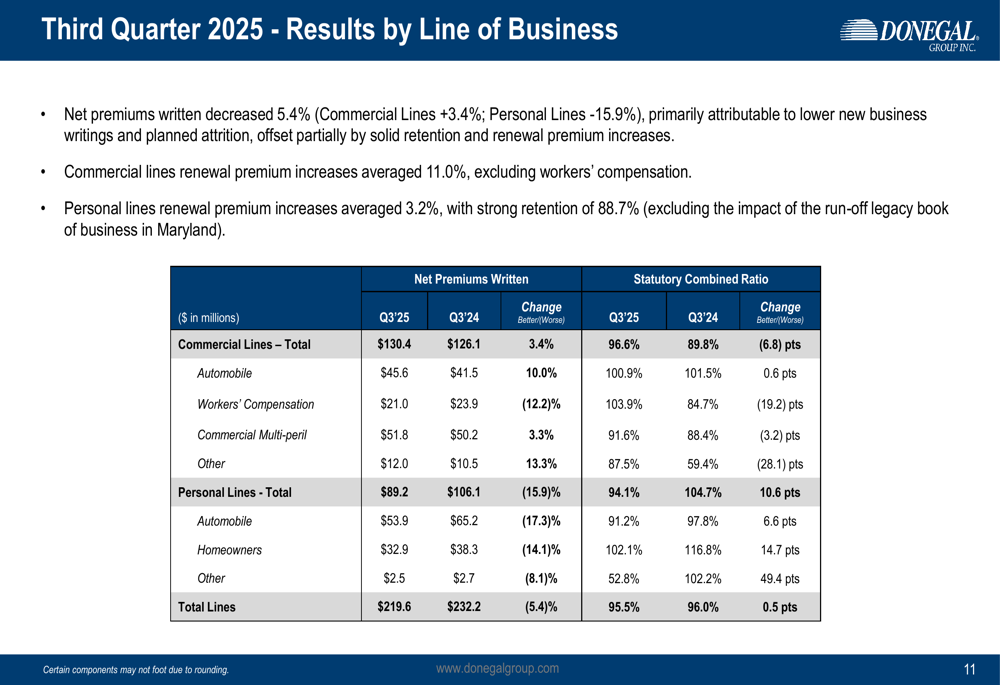

The breakdown of results by line of business reveals divergent trends between commercial and personal segments:

Commercial lines net premiums written increased 3.4% to $130.4 million, while personal lines saw a 15.9% decrease to $89.2 million. This shift aligns with Donegal’s long-term strategy of growing its commercial business while maintaining a smaller but profitable personal lines portfolio.

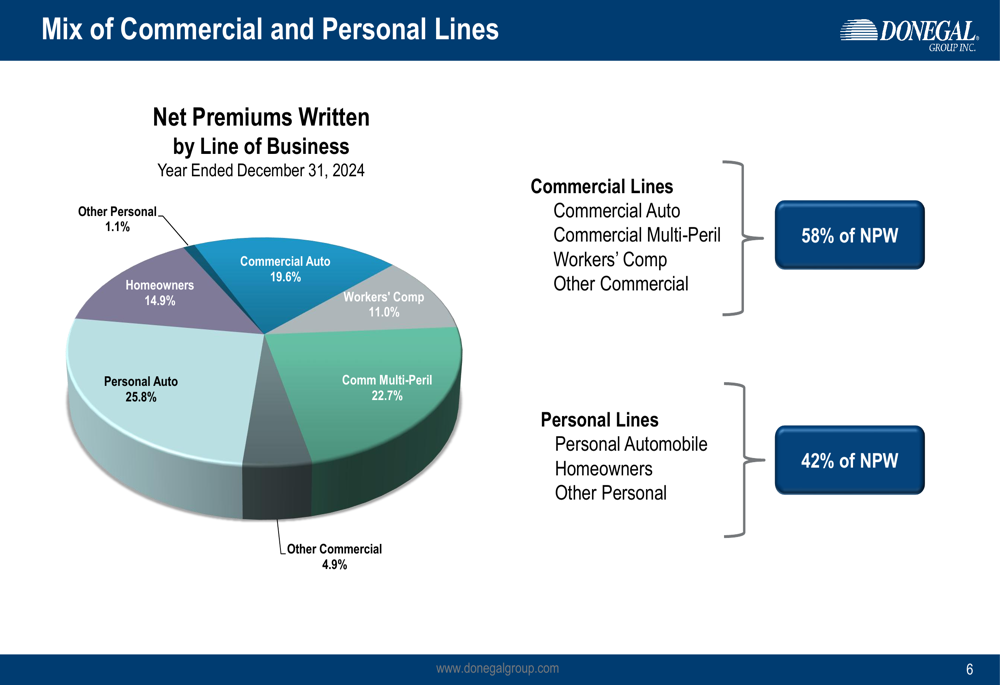

Business Mix and Strategic Direction

Donegal continues to emphasize its commercial lines business, which now represents 58% of net premiums written compared to 42% for personal lines. The company’s business mix is distributed across several key segments:

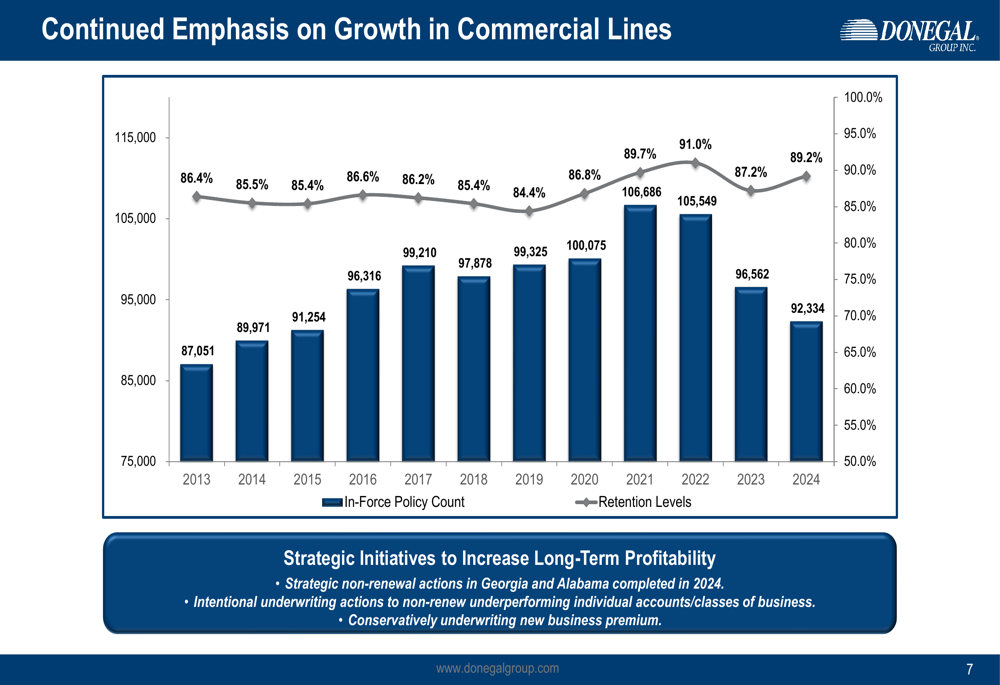

The company’s focus on commercial lines is yielding positive results, with in-force policy counts growing from 87,051 in 2013 to 92,334 in 2024, while retention levels improved from 86.4% to 89.2% over the same period:

During the earnings call, COO Dan Dellamater emphasized the company’s disciplined approach, stating, "Rate adequacy is clearly important, and we’re not interested in chasing underpriced new business." This philosophy has guided Donegal’s strategic non-renewal actions in underperforming markets like Georgia and Alabama, which were completed in 2024.

Commercial lines renewal premium increases averaged 11.0% (excluding workers’ compensation), while personal lines renewal premium increases averaged 3.2%. The company maintained strong retention of 88.7% across its book of business.

Investment Strategy and Results

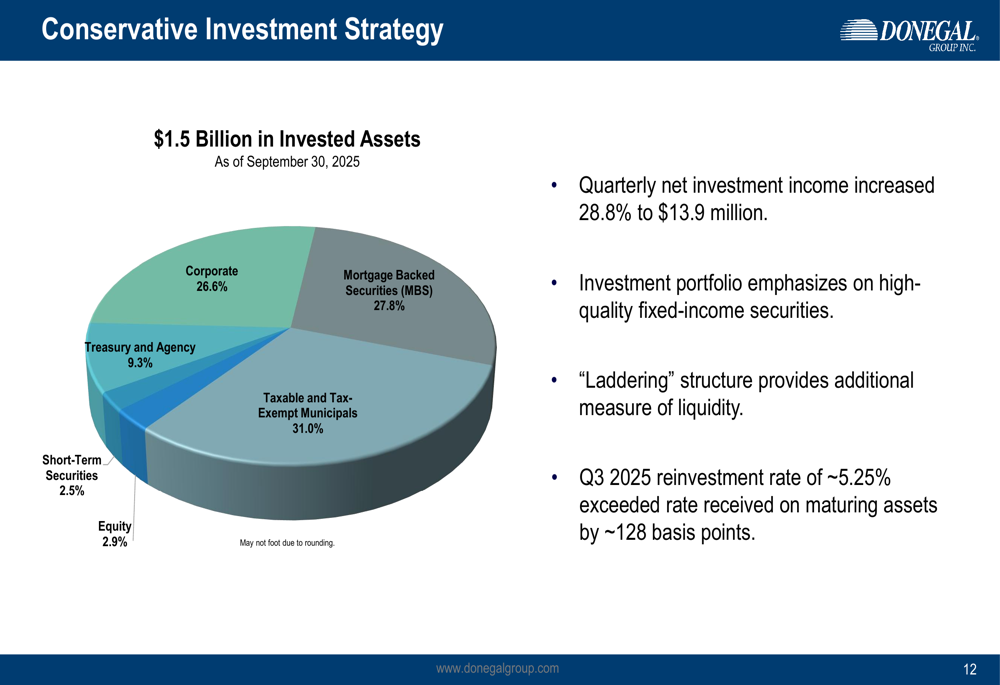

A bright spot in Donegal’s quarterly results was the significant growth in net investment income, which increased 28.8% to $13.9 million. The company maintains a conservative investment approach with a portfolio valued at $1.5 billion as of September 30, 2025:

The investment portfolio emphasizes high-quality fixed-income securities, with a "laddering" structure providing additional liquidity. The company benefited from a favorable interest rate environment, with Q3 2025 reinvestment rates of approximately 5.25% exceeding the rates received on maturing assets by 128 basis points.

This strong investment performance helped offset the challenges in premium growth and contributed significantly to the overall improvement in net income.

Competitive Positioning and Valuation

Donegal’s price-to-book multiple of 1.13 positions it below the peer average of 1.85x, suggesting potential undervaluation compared to other multi-line insurers:

The company maintains an A.M. Best rating of A (Excellent), reflecting its strong financial position. With a market capitalization of approximately $675.77 million and a P/E ratio of 6.61 (significantly below industry averages), Donegal presents an interesting value proposition for investors.

Forward-Looking Statements

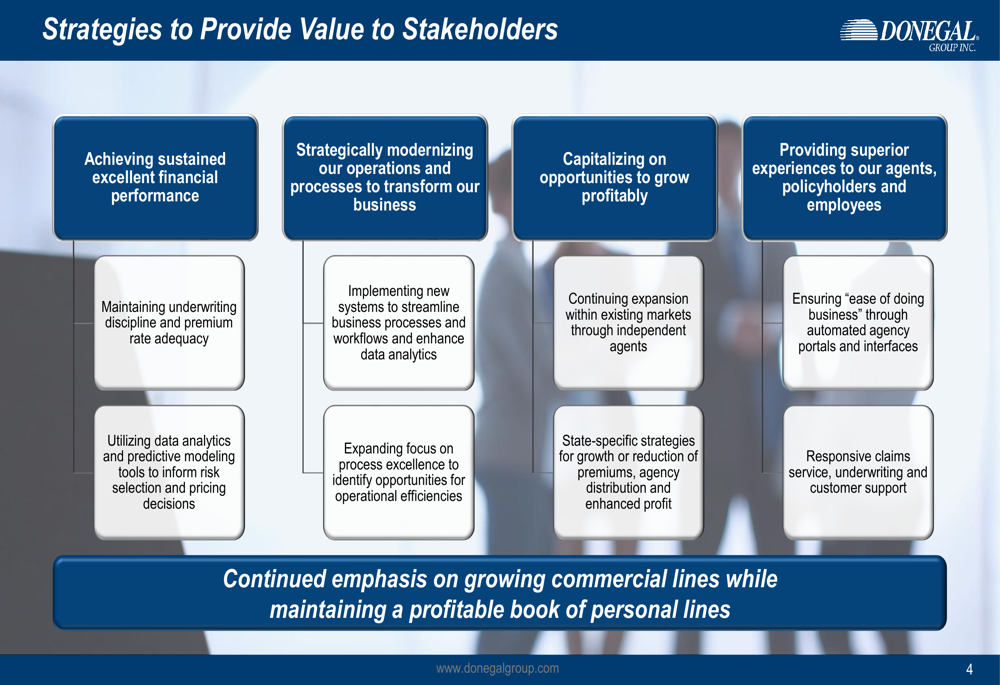

Looking ahead, Donegal outlined four key strategies to provide value to stakeholders:

The company plans to prioritize growth in its small and middle-market commercial segments for 2026, while continuing technology modernization initiatives. Management projects $115 million in portfolio cash flow over the next 12 months.

Chief Underwriting Officer Jeff Hay noted during the earnings call that "We enjoyed historically favorable weather conditions during the quarter," which contributed to the improved combined ratio. However, the company faces challenges in maintaining growth in personal lines and navigating economic uncertainties that could impact small and mid-sized business segments.

Despite these challenges, Donegal’s strong financial foundation, disciplined underwriting approach, and strategic focus on profitable commercial lines position it well for sustainable long-term growth. The company’s book value per share increased 12.6% year-over-year to $17.14, providing a solid foundation for future shareholder value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.