Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Dorian LPG Ltd (NYSE:LPG) released its fourth quarter fiscal year 2025 investor presentation on May 22, 2025, revealing a substantial year-over-year decline in profitability despite positive trends in global LPG shipping volumes. The presentation comes as the company’s stock has faced pressure, trading at $22.66 as of the last close, down 3.2% and well below its 52-week high of $48.53.

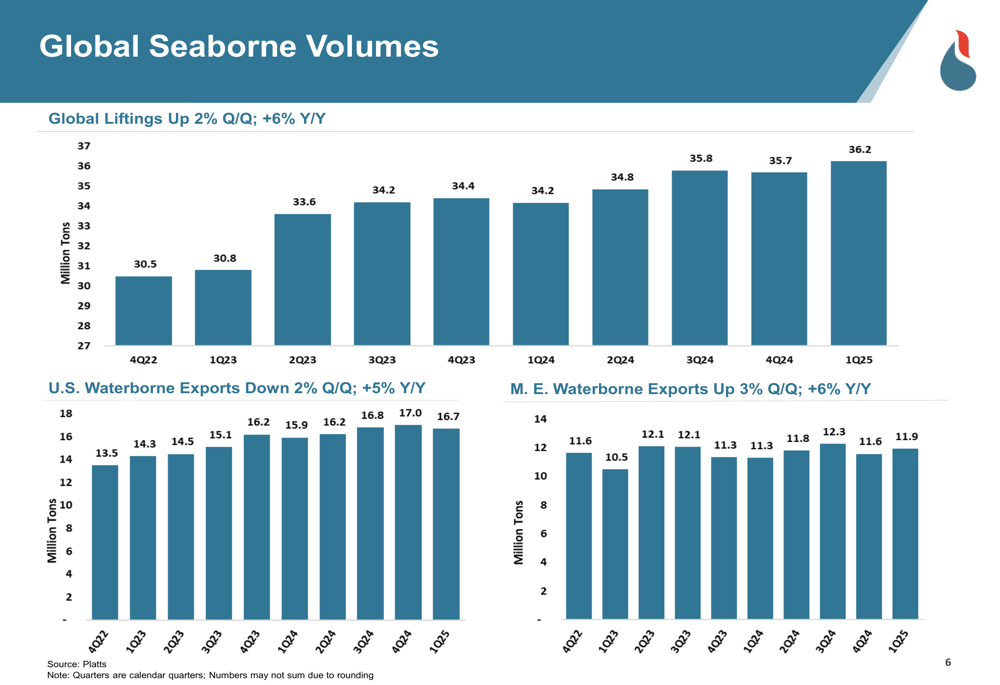

The LPG shipping market continues to show growth in global seaborne volumes, with overall liftings up 6% year-over-year. However, Dorian’s financial performance has not kept pace with these favorable market conditions, as evidenced by the sharp decline in quarterly earnings.

Quarterly Performance Highlights

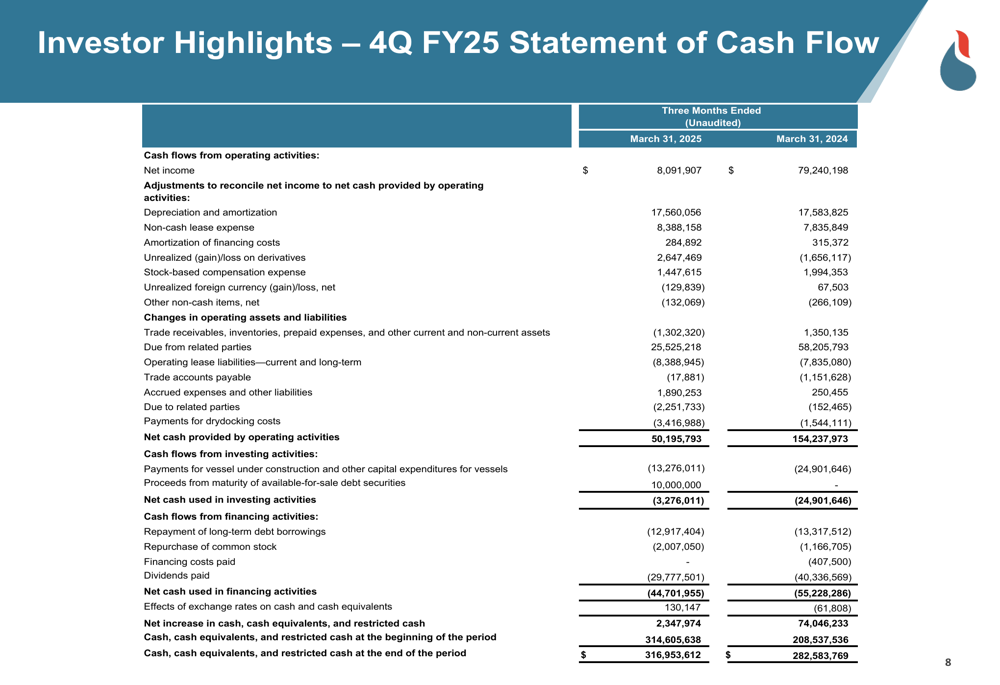

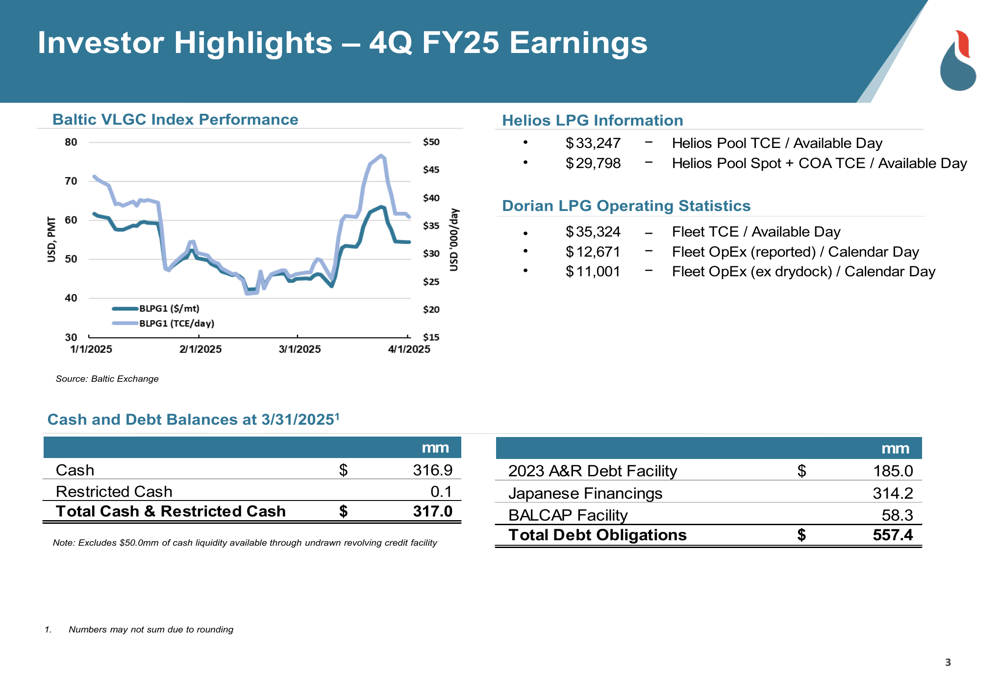

Dorian LPG reported a dramatic 90% decrease in net income for Q4 FY25, with profits falling to just $8.1 million compared to $79.2 million in the same period last year. This decline comes despite relatively strong operational metrics, with the company achieving a fleet Time Charter Equivalent (TCE) rate of $35,324 per available day.

The company’s statement of cash flows reveals the extent of the earnings deterioration:

Despite the significant drop in profitability, Dorian has maintained a strong cash position of $316.9 million, slightly higher than the $282.6 million reported at the end of Q4 FY24. Total (EPA:TTEF) debt obligations stood at $557.4 million, with the company noting an additional $50 million in available liquidity through an undrawn revolving credit facility.

The Baltic VLGC Index performance chart included in the presentation shows the freight rate environment during the quarter, with the company’s TCE rates reflecting the market conditions:

These results follow a disappointing Q3 FY25, when the company reported earnings per share of $0.43, significantly below analyst expectations of $0.74, and revenue of $80.7 million versus forecasts of $88.94 million.

Global Market Position

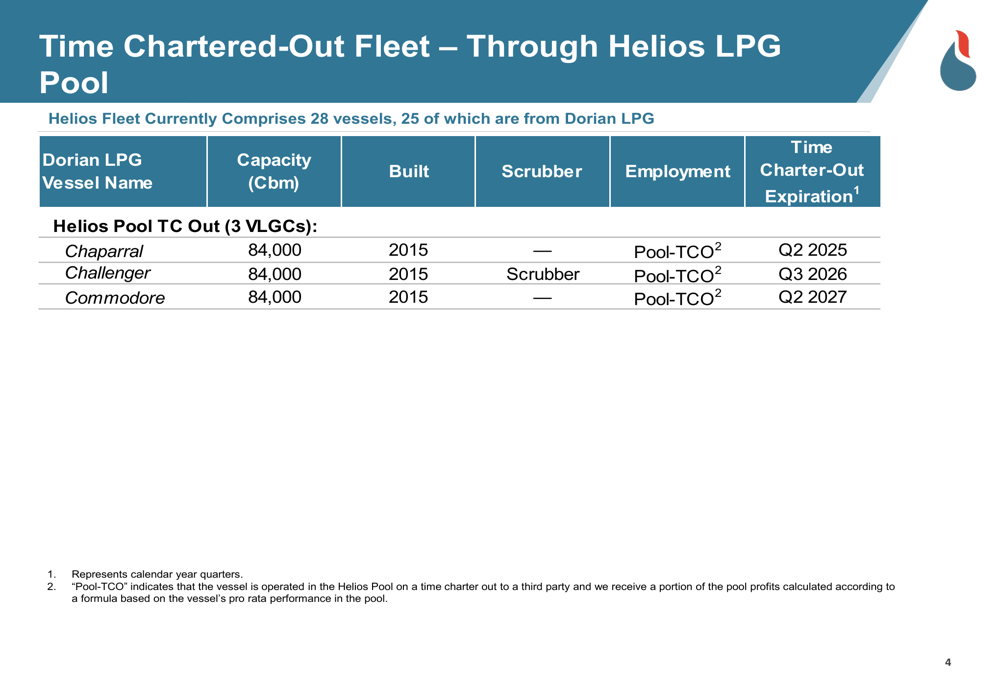

Dorian LPG continues to be a major player in the global LPG shipping market, with 25 vessels operating in the Helios Pool (NASDAQ:POOL), which comprises a total of 28 vessels. The company’s presentation highlighted positive trends in global LPG shipping volumes, with worldwide liftings increasing by 2% quarter-over-quarter and 6% year-over-year.

The data shows mixed regional performance, with U.S. waterborne exports declining 2% quarter-over-quarter but increasing 5% year-over-year, while Middle East exports grew both sequentially (3%) and annually (6%).

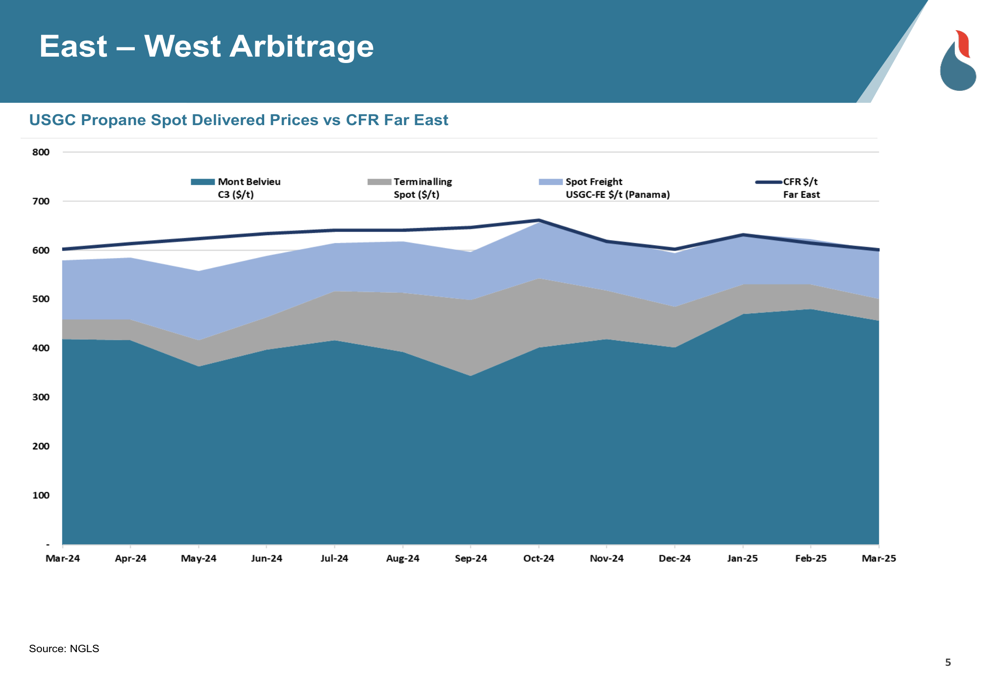

The company’s fleet remains well-positioned to capitalize on East-West arbitrage opportunities, which are a key driver of LPG shipping demand. The presentation included a chart showing the price differentials between U.S. Gulf Coast propane and Far East markets:

Dorian’s time-chartered fleet provides some revenue stability, with various vessels contracted through 2025-2027, helping to mitigate market volatility:

Strategic Initiatives

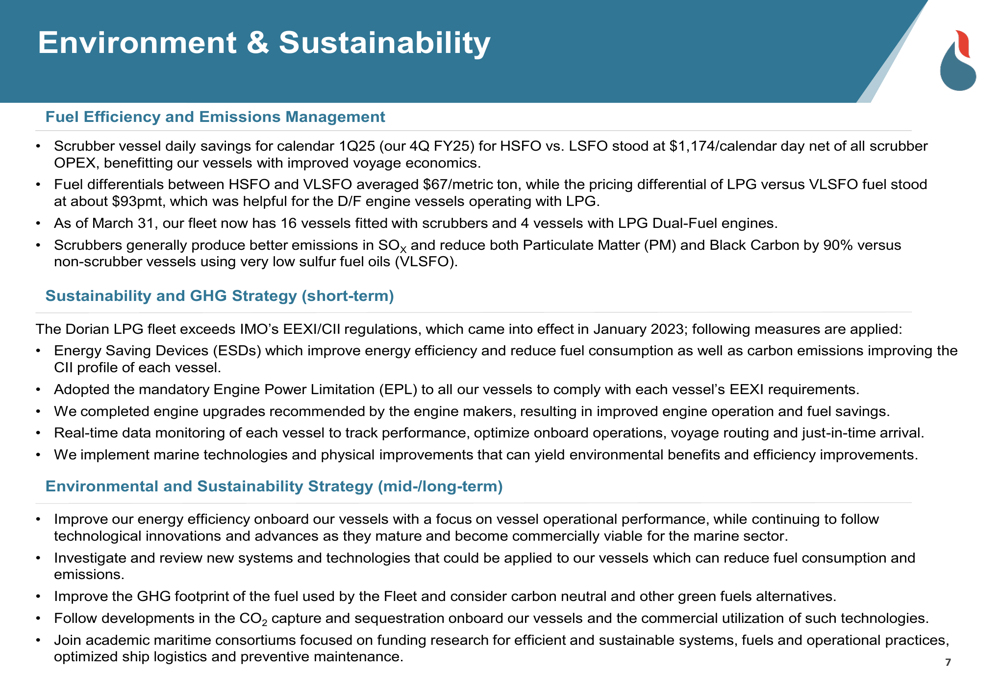

Amid challenging financial results, Dorian LPG is emphasizing its commitment to environmental sustainability and operational efficiency. The company detailed several initiatives aimed at reducing emissions and improving fuel efficiency, which could help control costs and ensure compliance with increasingly stringent regulations.

During the previous earnings call, CEO John Hadjipateras had emphasized the company’s commitment to fleet renewal opportunities, stating, "We continue to be on the lookout for fleet renewal opportunities." This strategy appears to remain in place, though the presentation did not provide specific details on new vessel acquisitions or fleet expansion plans.

Forward-Looking Statements

While Dorian LPG faces significant challenges in restoring profitability to previous levels, the company’s strong cash position provides financial flexibility. The global LPG shipping market continues to show growth, which could eventually support improved financial performance if freight rates strengthen.

However, investors should note the substantial disconnect between market growth and the company’s recent financial results. The 90% year-over-year decline in quarterly profits raises questions about Dorian’s ability to capitalize on favorable market conditions, and the stock’s performance reflects these concerns, trading closer to its 52-week low than its high.

The company’s focus on sustainability initiatives and fleet management suggests a long-term strategic approach, but near-term financial performance will likely remain a primary concern for investors as they assess whether the current earnings weakness is temporary or indicative of more persistent challenges in translating market growth into shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.