D-Wave Quantum falls nearly 3% as earnings miss overshadows revenue beat

Introduction & Market Context

DraftKings Inc. (NASDAQ:DKNG) presented its second-quarter 2025 earnings results on August 6, showing significant acceleration in growth and profitability metrics. The online sports betting and gaming company’s stock closed at $44.94 on the day of the presentation, up 0.97%, with a slight decline of 0.36% in after-hours trading. The company’s shares have traded between $29.29 and $53.61 over the past 52 weeks, indicating substantial volatility as the online gambling market continues to mature.

The Q2 results mark a significant improvement from the company’s Q1 2025 performance, when DraftKings missed analyst expectations on both revenue and earnings per share. This quarter’s strong performance demonstrates the company’s ability to accelerate growth while improving profitability metrics.

Quarterly Performance Highlights

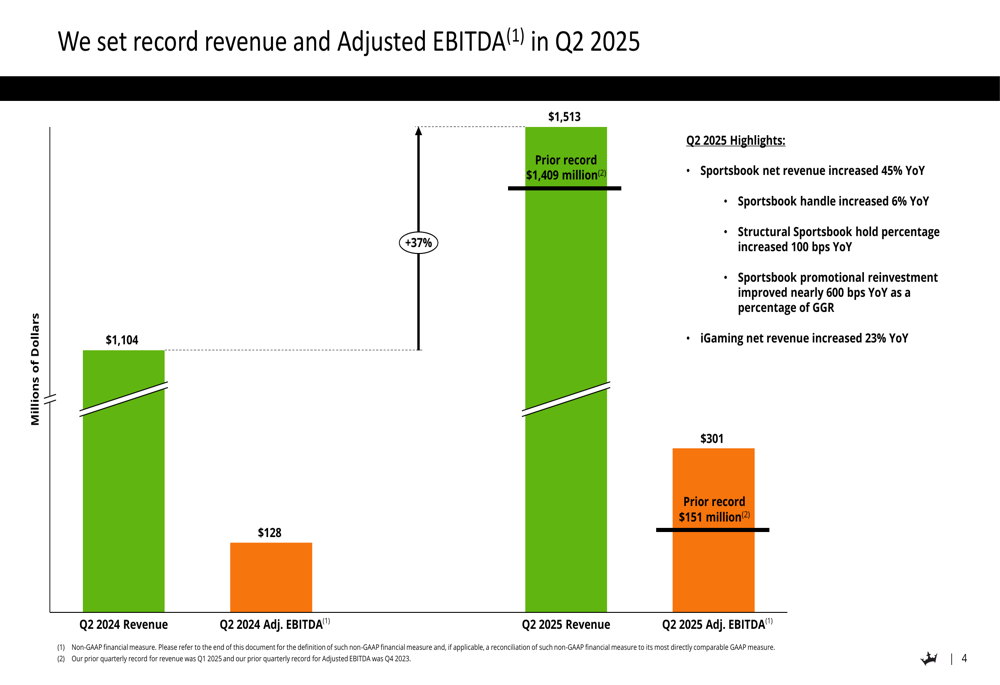

DraftKings reported record revenue of $1.513 billion for Q2 2025, representing a 37% year-over-year increase from $1.104 billion in Q2 2024. This growth rate marks an acceleration from previous quarters, with the company’s Sportsbook segment leading the way with a 45% year-over-year revenue increase. The company also achieved record Adjusted EBITDA of $301 million, substantially higher than the $128 million reported in the same period last year.

As shown in the following chart of quarterly revenue and Adjusted EBITDA:

The company’s performance was driven by multiple factors, including a 6% increase in Sportsbook handle, a 100 basis point improvement in structural Sportsbook hold percentage, and nearly 600 basis points improvement in promotional reinvestment as a percentage of gross gaming revenue. Additionally, iGaming net revenue increased by 23% year-over-year, contributing to the overall strong performance.

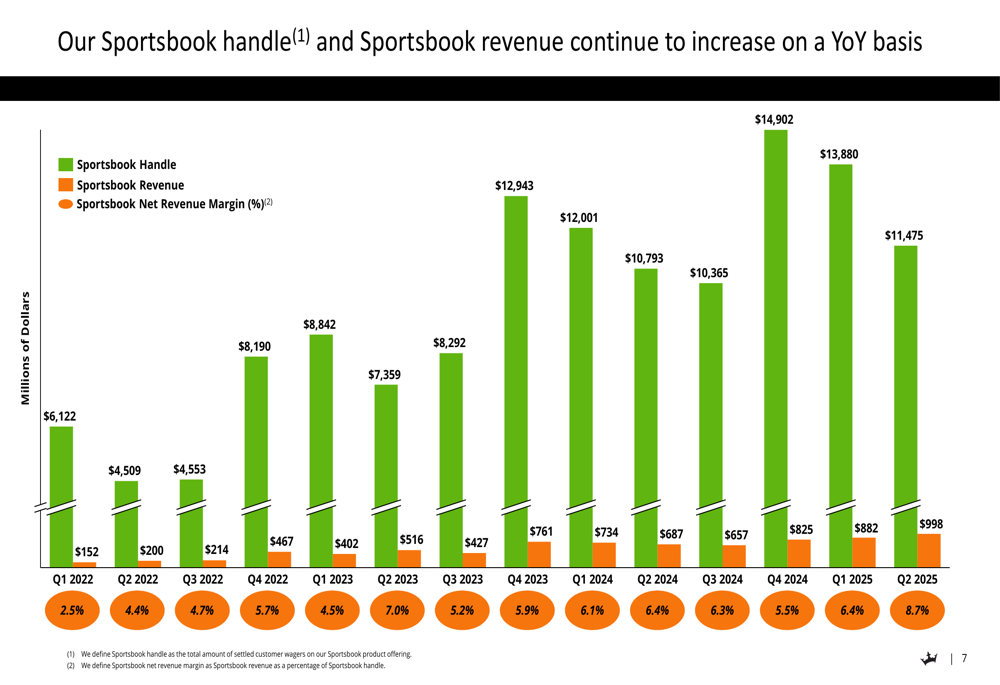

The historical growth trajectory of the Sportsbook segment is illustrated in this chart showing handle and revenue trends:

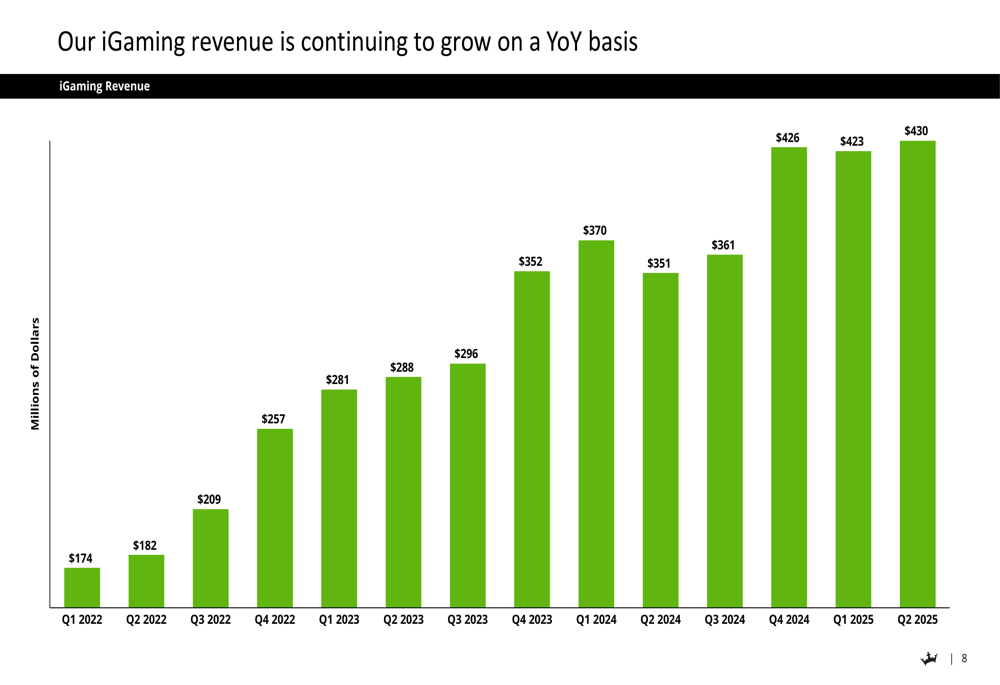

Similarly, the iGaming segment has shown consistent growth over recent quarters, as demonstrated in the following revenue chart:

Strategic Initiatives

DraftKings highlighted three key areas of innovation driving its platform development: Live Betting, Authentic and Relevant Experiences, and Community features. The company reported that live betting availability now exceeds 90% for MLB and NBA events, with over 1.5 million customers engaging with Live Bet Tracking in 2025.

The social aspects of the platform have gained significant traction, with 25 million "tailed" social bets from over 600,000 unique customers in 2025 year-to-date. Social platform handle increased 180% year-over-year, while engagement across social media handles grew 200% year-over-year. The company’s Discord community has expanded by 400% compared to the previous year.

DraftKings is also exploring opportunities in federally-regulated Prediction Markets and continues to allocate capital to maximize shareholder returns, including the repurchase of 6.5 million shares in the first two quarters of 2025.

Detailed Financial Analysis

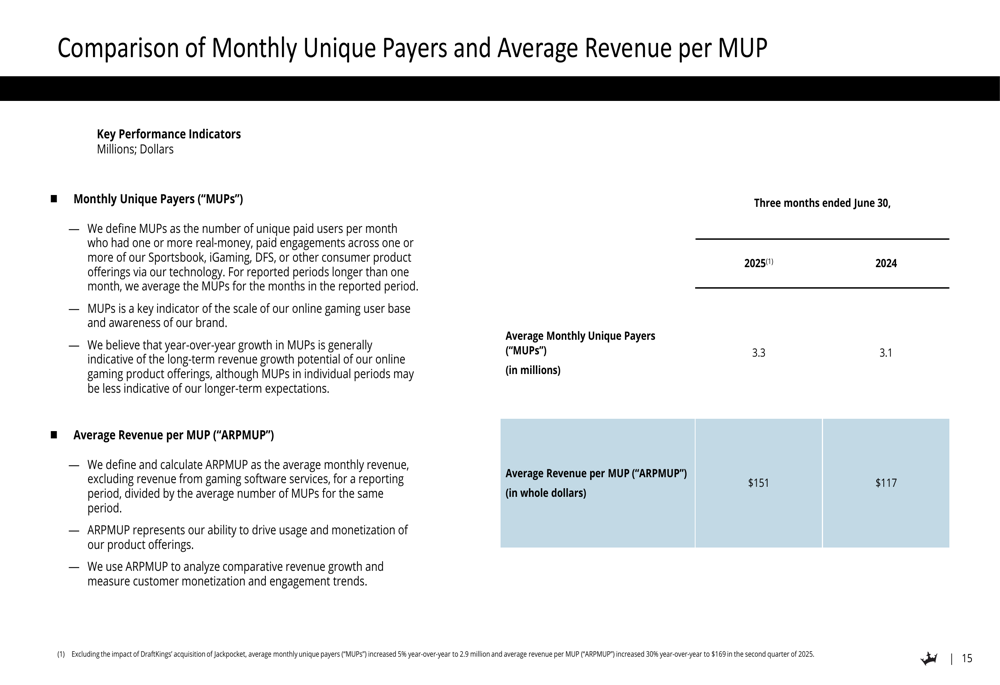

DraftKings’ user metrics showed healthy growth, with Monthly Unique Payers (MUPs) increasing to 3.3 million in Q2 2025 from 3.1 million in Q2 2024. More importantly, the Average Revenue per MUP (ARPMUP) jumped significantly to $151 from $117 in the same period last year, representing a 29% increase.

The following chart illustrates these key user metrics:

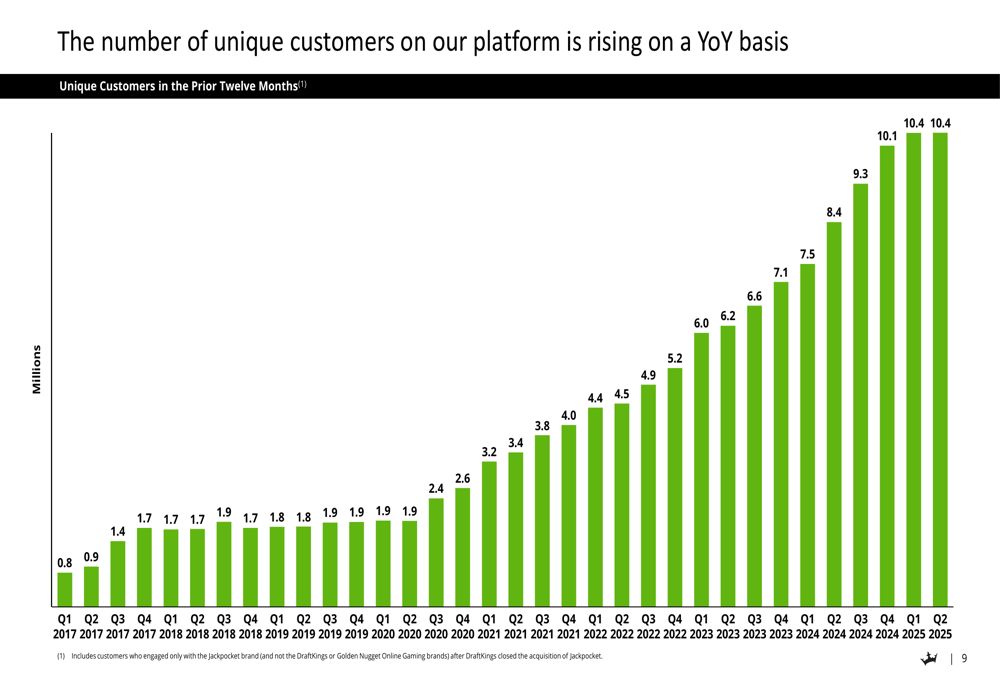

The company’s unique customer base continues to expand, with 10.4 million unique customers in the prior twelve months as of Q2 2025, as shown in this growth chart:

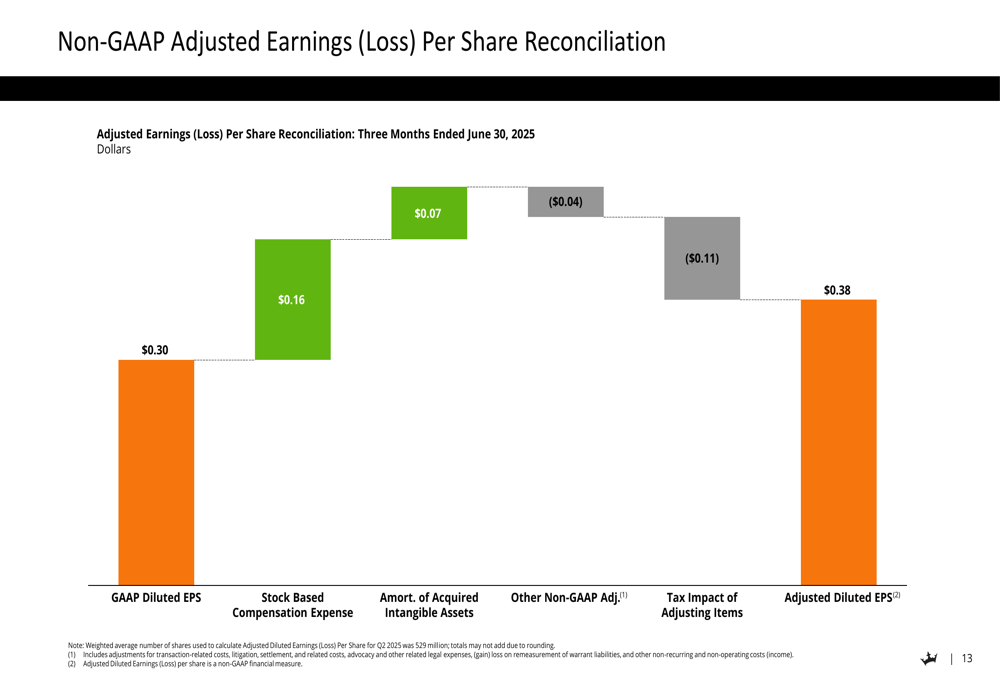

On the earnings front, DraftKings reported GAAP Diluted EPS of $0.30 for Q2 2025, with Adjusted Diluted EPS of $0.38. The reconciliation between these figures is broken down in the following chart:

This represents a substantial improvement from Q1 2025, when the company reported EPS of $0.12, missing analyst expectations of $0.20. The Q2 performance demonstrates DraftKings’ ability to translate revenue growth into bottom-line results.

Forward-Looking Statements

Despite the strong Q2 results, DraftKings maintained its full-year 2025 revenue guidance range of $6.2 billion to $6.4 billion and Adjusted EBITDA guidance of $800 million to $900 million. This guidance is consistent with the revised outlook provided after Q1 2025, when the company lowered its revenue guidance from the original $6.3-$6.6 billion range.

The company expressed confidence in its positioning for the fall sports season, highlighting ongoing innovation in its Sportsbook app. Management also indicated they are monitoring federally-regulated Prediction Markets for potential opportunities to enhance shareholder value.

DraftKings’ consistent user growth, improving monetization metrics, and strategic focus on innovation suggest the company is well-positioned to maintain its growth trajectory in the competitive online sports betting and gaming market. However, investors should note that the company’s decision to maintain rather than raise guidance despite the strong Q2 performance may indicate caution about the second half of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.